Warren Buffet on the problems with inflation, written in 1977. Click here.

Author Archives: Bruce Konners

Week Ending 8/4/2017

HIGHLIGHTS

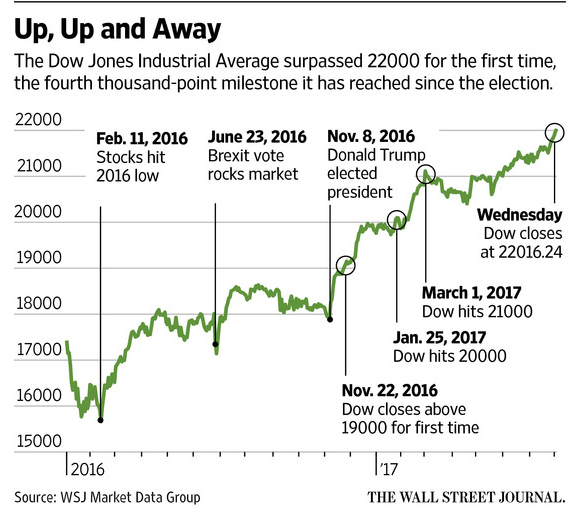

- The Dow Jones Industrial Average sets another record, breaking 22,000.

- Broader indexes are flat, transports are down.

- Solid payroll report

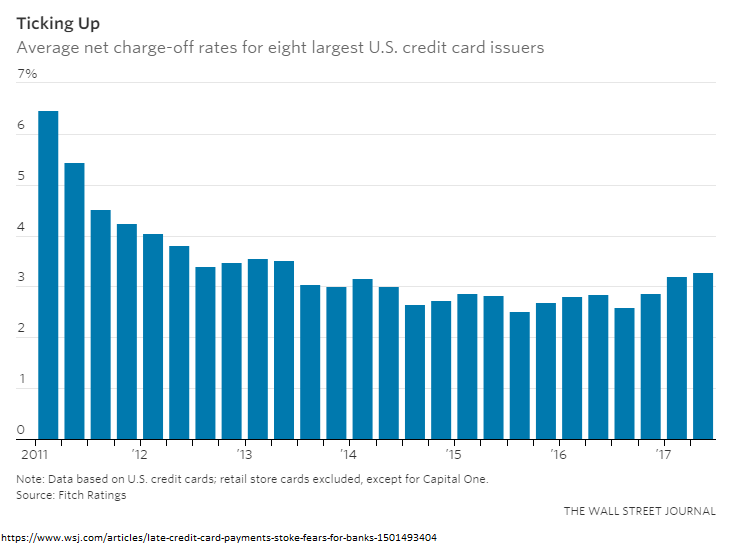

- Late credit card payments increase

PERFORMANCE

The Dow broke through another milestone, cracking the 22,000 barrier and ending the week at 22,092.81, plus 1.20% for the week. However, the broader indexes were closer to flat. The SP500 was up 0.19% and the Nasdaq Composite fell 0.36%. International equities rose by 0.82%.

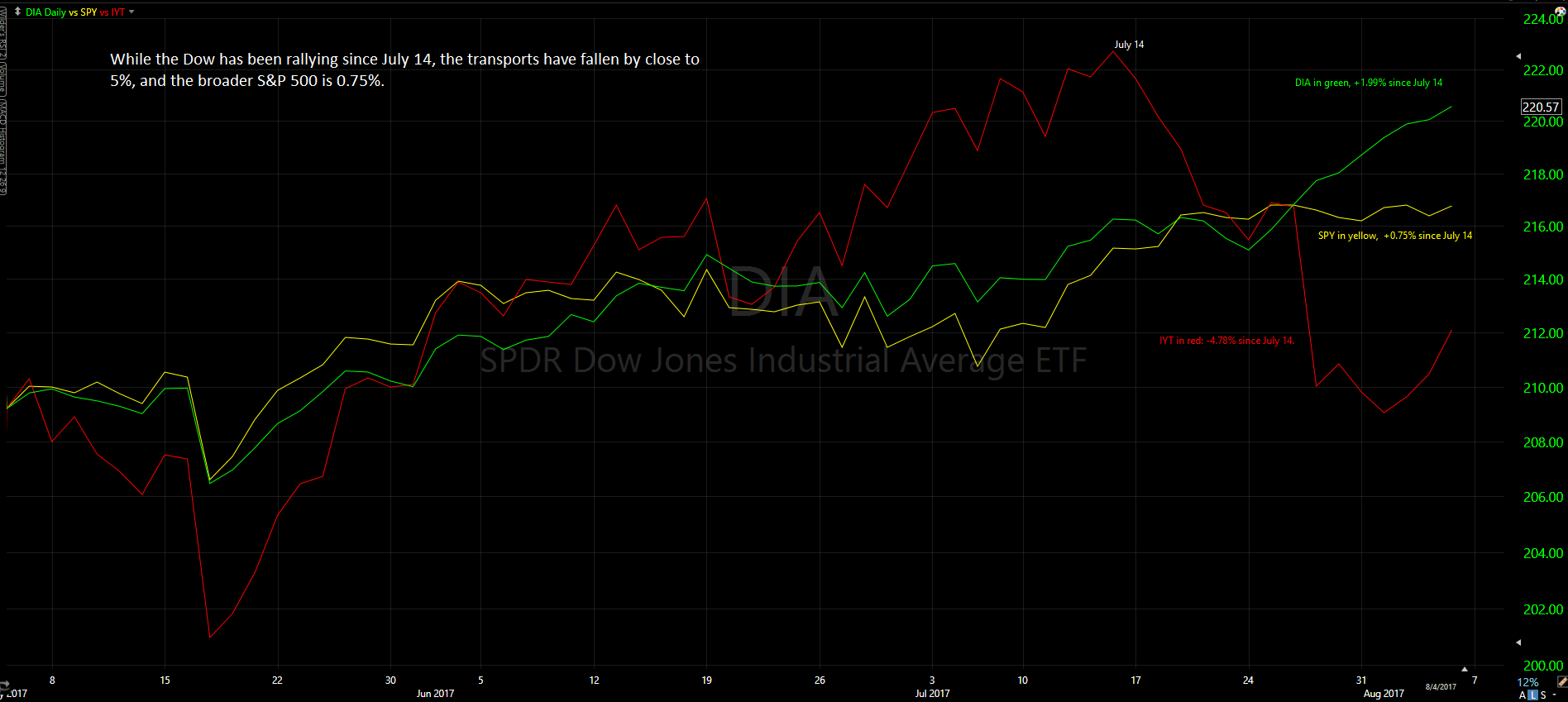

After peaking on July 14, transport stocks have been down. The IShares Dow Jones Transportation Average Index Fund (IYT) has fallen by 4.78% while the Dow (DIA) has increased by about 1.99% during that time. A divergence between the two signifies a market warning based on the 117-year-old Dow Theory. The Dow Theory states that a rally in an index like the Dow should be confirmed by a rally in the transports (the Rails back in 1900). Times have changed since then and there have been several times in this market rally over the last few years where we did not get this confirmation, but it is worth a mention.

Bonds were up by 0.19% as the treasury yield curve going out from five years fell a few basis points.

ECONOMY

The first look at Q3 growth from the Atlanta Fed’s GDPNow model came in at a strong 4.0%. However, by week end it had dropped to 3.70%. The New York Fed’s Nowcast has Q3 growth at a much milder 1.98%.

SOLID PAYROLL REPORT

Non-farm payrolls increased by 209,000 in July, higher than the consensus estimate of 180,000. It was the 82nd straight month of job creation, the longest such streak ever. As shown in the chart below, this expansion has been noteworthy for a slow but very steady and long pace.

The May and June non-farm payroll numbers were also revised higher. The unemployment rate fell to 4.3% from 4.4%, the lowest number in 16 years. The labor force increased to 62.9%, up 0.1%. Average hourly earnings were up 2.5% year over year. Almost half of the gains were in bars and restaurants, and healthcare.

LATE CREDIT CARD PAYMENTS

Credit-card issuers are starting to have collection problems. The average net-charge off for large US card issuers increased to 3.29%, the highest level in four years. Losses are still low based on historical levels. Around 2014 banks started relaxing underwriting standards, which led to a big increase in credit-card spending. That might have led to the higher charge-offs now.

SCOREBOARD

Interview with Peter Bernstein

Transcript of a PBS interview with market historian Peter Bernstein, from the 1990s. Click here.

Week Ending 7/21/2017

PERFORMANCE

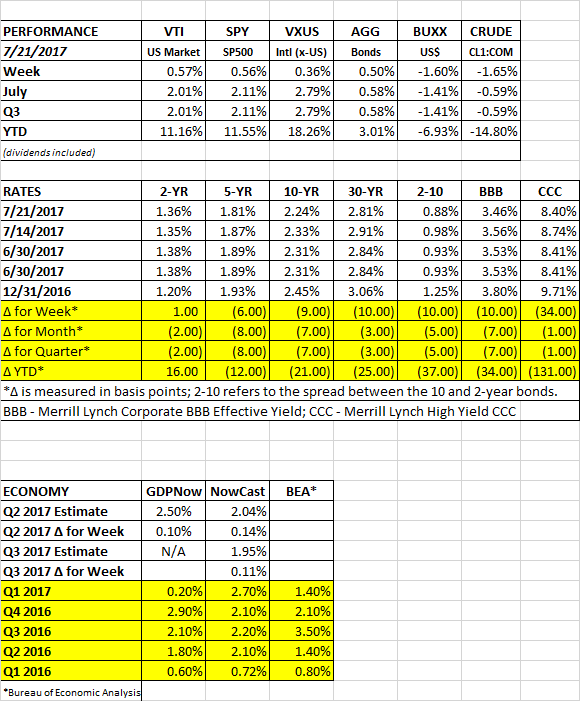

It was another good week for investors as equity and fixed income markets were generally up by about 1/2%. The US markets increased by 0.57%, international +0.36% and the bond aggregate +0.50%. The US dollar fell by 1.60% and crude dropped by 1.65%.

The markets have been helped by strong earnings, which in turn have been helped by a lower dollar. The dollar is now down about 7% on the year. A lower dollar provides a tailwind to earnings. According to Dubravko Lakos-Gujas from JP Morgan, S&P500 earnings increase by about 1% for every 2% decline in the dollar. Overall, 19% of S&P 500 companies have reported earnings this quarter, and they have come in 7.8% above estimates (per FactSet).

Interest rates generally declined but at the short-end of the curve, they increased. The 5, 10 and 30 year bonds all had lower yields. But the two-year was up by 1 basis point and the 3-month yield increased by 12 basis points. Bond investors are worried about the up-coming battle over the debt ceiling, probably sometime in October, 3-months away.

POLITICS

While the market continues to advance, the political environment continues to deteriorate. Special Counsel Robert Mueller expanded his investigation into Trump’s Russia connections, including historical personal transactions. White House Press Secretary Sean Spicer resigned and Trump criticized his attorney general. The Republicans cannot pass a healthcare bill and cannot even figure out how to take a vote on one. That was just this week.

ECONOMIC

The Conference Board’s Leading Economic Index was up by the most since December of 2014, increasing 0.6%. A strong report on building permits led the way.

Initial jobless claims fell to 233,000. Down 15,000 from last week.

SCOREBOARD

Rolling Over Your Retirement Plan

Q3 Market Review/Outlook

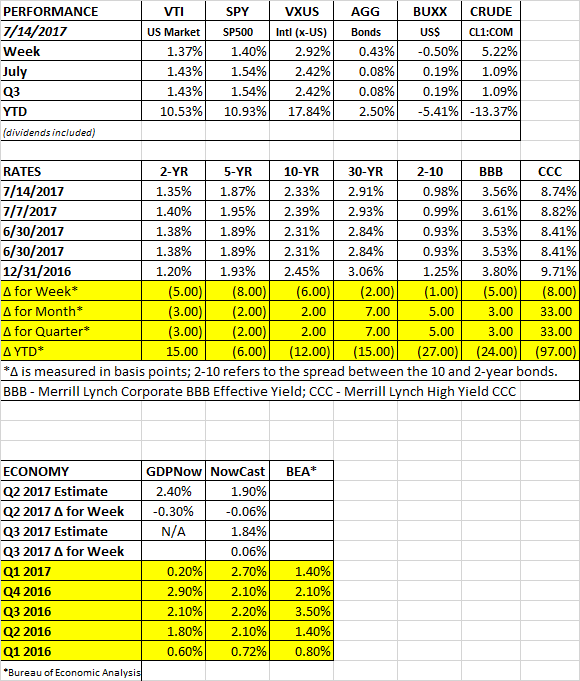

Week Ending 7/14/2017

REVIEW

The market broke out to another high, continuing the stair-step pattern of consolidation, then another step higher. Fed Chair Janet Yellen testified before Congress and emphasized that rate hikes would be very deliberate and moderate. The market took that as good news and shot equities higher.

Bonds moved up by 0.43% as interest rates dropped on the testimony. The 10-year fell to 2.33% from 2.39%. Crude rallied by 5%.

Investors now view the probability of another interest rate hike this year as less likely. Yellen’s testimony, coupled with less than sanguine economic reports, makes it more likely that a September hike is off the table and lowers the probability of a December increase.

QUARTERLY WEBINAR

Our quarterly webinar was this weekend, click here.

SCOREBOARD

Week Ending 7/7/2017

PERFORMANCE

US equity markets were basically even, +0.06% while international markets fell by almost 1/2%. Bonds declined as interest rates continued to rise and the yield curve steepened. The dollar was up and crude was down.

INTEREST RATES

It was one year ago, on July 6, 2016, that the 10-year treasury bond hit its all time-low yield of 1.367%. One year later, we are one point higher at 2.37%. The 10-year has traded in a range between 2.1% and 2.6% since the election and we are back in the middle of that range now.

Over the last couple of weeks, consensus has tilted back towards higher rates going forward. Minutes released from the June Federal Reserve meeting showed that members want to begin reducing the balance sheet before year-end. And European Central Bank minutes indicate that there were discussions of ending their pledge to buy bonds if the economy weakened. Depending upon the rate of increase, higher interest rates at some point would likely put pressure on equities. The interplay between higher earnings and interest rate will have a lot to do to determine the direction of the equity markets.

EMPLOYMENT

The June employment report came in strong. Non-farm payrolls increased by 222,000 and the two prior months were revised higher by 47,000. The unemployment rate increased to 4.4% from 4.3% due to more entries into the workforce, which is considered a positive sign. The average workweek rose by 0.1 hours to 34.50 and average hourly earnings were 2.50% higher year over year.

SCOREBOARD

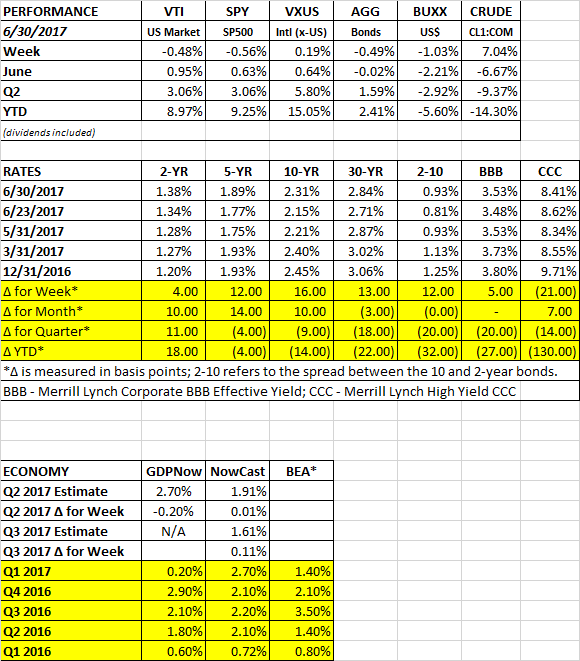

Week Ending 6/30/2017

PERFORMANCE

US equity markets were down by about 1/2% while international markets managed a 0.19% advance. The dollar fell and crude rallied by 7%.

Interest rates rose. The yield curve got steeper. The 10-year rose by 16 basis points. Central bankers are beginning to align themselves on the path to higher rates. The Fed has been increasing rates and have signaled more is on the way, as well as laying out the plan to reduce their bond holdings. But now some central bankers overseas might be joining the party. Mario Draghi of the ECB suggested that the bank might be close to ending its bond buying. And Mark Carney of the Bank of England suggested that a rate hike might be on the way.

EARNINGS

As the quarter ended, analysts are forecasting Q2 earnings of $31.50, down from $32.13, according to FactSet. The 2% decline is lower than the drop-in forecasts in prior quarters, which have averaged 5.9% over the last 10 years.

ECONOMY

Q1 GDP was revised up to 1.4% from 1.2%. The original estimate for Q1 real growth was 0.7%, and that was later revised up to 1.2%. GDP growth has picked up in Q2, the Atlanta Fed’s GDPNow model currently has Q2 growth at 2.7%. The first official estimate from the Commerce Department will be released on July 28.

The current economic expansion began in July of 2009 and is currently the third longest on record, surpassed only by expansions in the 1960s and the 1990s. However, the growth rate during this expansion has been sub-par, probably due to lower productivity and a decline in the labor force.

SCOREBOARD

SCOREBOARD