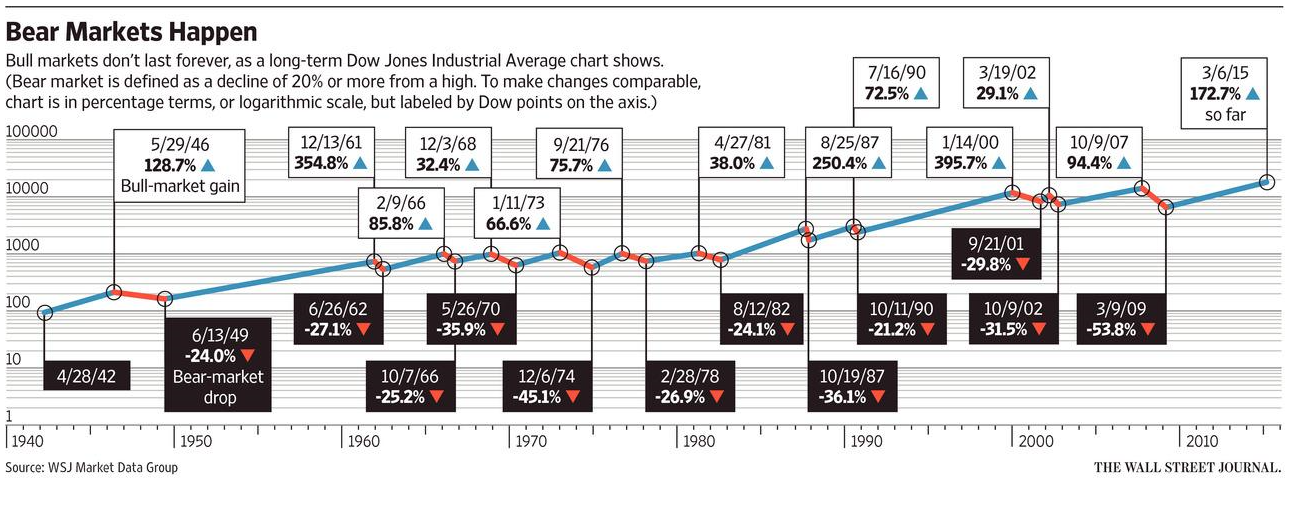

For the week, the VTI fell by 0.367%, the SPY 0.65%, the VT by 1.06% and the AGG by 1.47%. The equity markets have fallen two weeks in a row now but it hasn’t been much of a fall. The VTI hit a high on May 21 of 110.51 and is now down 1.45%, the SPY is down 1.75% over that same period.

The situation in Greece is still up in the air. Some payments were delayed to creditors last week.

Fears of a rate hike continue to spook the market impacting interest sensitive stocks much harder. REITs have taken a beating, the VNQ is down 3.67% since May 21 and are down 10.64% since March 23. There are some quality REITs now yielding 5% or better and some around 6%. Long bonds resumed their downtrend, the TLT (20-Year Plus Treasury bond ETF) was down 4.16% for the week. The five-year yield has jumped 26 basis points, the 10-year 29 basis points, and the 3-year yield was up 23 basis points since the end of May pushing bond prices lower.

Anything with yield is getting punished, but there is starting to be some value as prices decline in certain sectors. In addition to some of the traditional REITS, some of the mortgage REITS are selling at big discounts to book value. Companies like Capstead (CMO) invest in short-term adjustable rate mortgages that should not be that exposed to interest rate risk.

Then there are companies that should benefit by rising rates. MET is up almost 7% since April 30. Many banks have been doing well. JPM is up 6.6% and C is up 5.58% in that time frame.

Assuming a September rate increase, Jeremy Siegel thinks the market can do well in Q4 when the market figures out that the world won’t end (http://www.cnbc.com/id/102725157). And at a few companies, like GM, GE and CVX, there has been some good insider buying of late.

The economic reports this week were strong. Auto sales hit an annual rate of 17.71 million which is a new high. The employment numbers surprised to the upside and unit labor costs were higher, a small signal of possibly higher inflation down the road and lower profit margins.