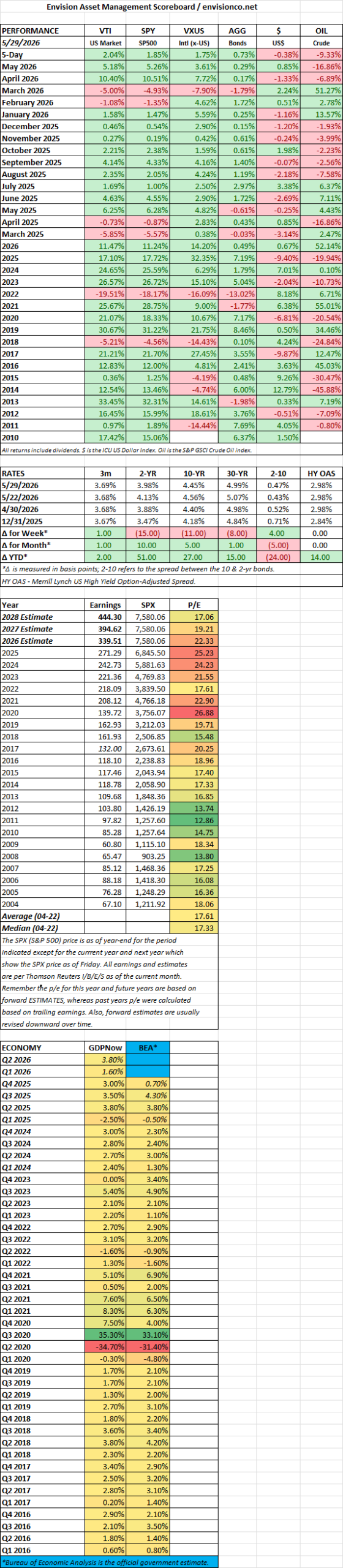

MARKET RECAP

US stock markets delivered strong results during the abbreviated trading week ending May 29, 2026, pushing major indexes to fresh record highs on the back of robust corporate earnings, AI enthusiasm, and reduced geopolitical risks. The S&P 500 advanced 1.4%, finishing at 7,580.06 compared to 7,473.47 the previous Friday. The Dow Jones Industrial Average increased 0.9% to close at 51,032.46, marking its first-ever trip above the 51,000 level. The Nasdaq Composite outperformed, rising 2.4% to end at 26,972.62.

Bitcoin declined modestly by around 2.8%, moving from near $75,488 to approximately $73,372, while Gold held relatively steady in the mid-$4,500-per-ounce range with limited net movement.

Financial Markets & Technology Sector

- Bull Market Milestone: The current market trajectory officially crossed 1,325 days, surpassing the 1962–1966 run to become the ninth longest bull market on record. The index is up 111.5% during this period.

- Tech Sector Streaks: The S&P 500 Technology sector achieved sequential monthly gains of over 10% in April (17.4%) and May (16%), marking a massive two-month gain of 36.1%.

- Market Breadth Anomaly: A notable divergence persists between rising indexes and overall participation.

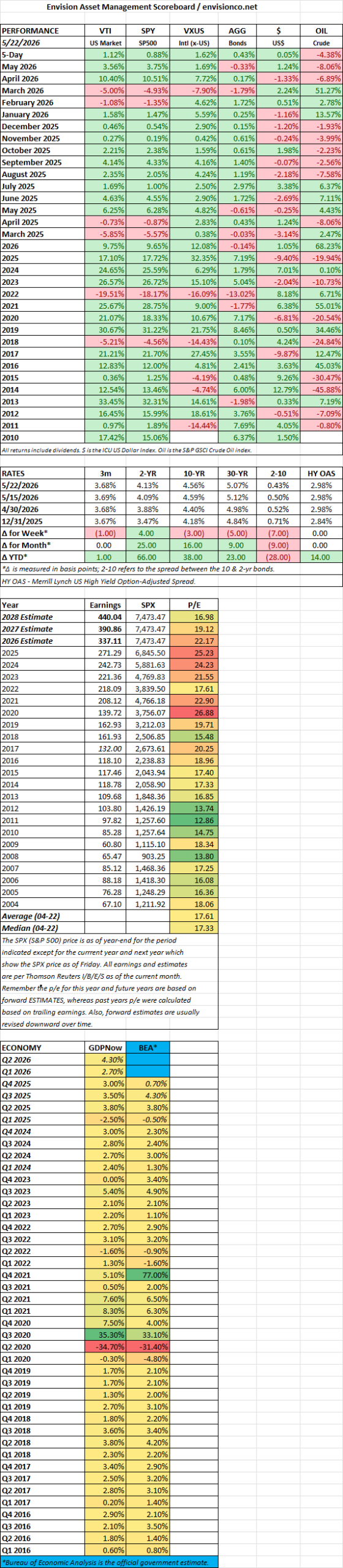

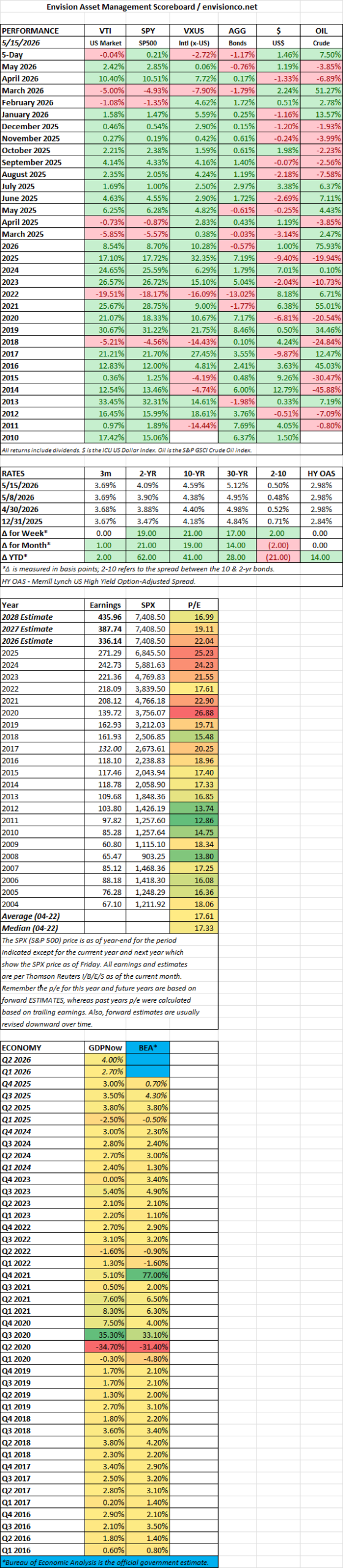

Gross Domestic Product (GDP) Revisions

The Q1 GDP headline figure was revised downward by 0.4 percentage points down to an annualized rate of 1.6%. The primary drags were soft inventories and downward corrections in services consumption. Conversely, non-residential AI technology and software infrastructure investments remained massive growth drivers.

Consumer Pressures & Savings Drop

A combination of stagnant hiring, moderating wage increases, and heightened inflation has restricted general household purchasing power. Real disposable personal income plummeted by 1% year-over-year in April. To fuel ongoing expenditures, consumers slashed their personal savings rate from over 5% last year down to 2.5%.

Inflation Metrics

Core prices jumped by a steep 4.4% annualized in Q1, registering the fastest non-pandemic core inflation surge since the early 1990s.

Regional Manufacturing Surveys & Corporate Pricing

- Five Fed Composite: The regional manufacturing current conditions composite dipped slightly by 0.3 points in May but maintains a general expansionary reading of 53.8. Price metrics continue to sit in the highest historical quintiles.

- Pricing Restrictions: Special corporate surveys indicate that while most manufacturing firms intend to raise prices in the upcoming year, they are limited from maximizing their target margins. More than 70% of companies noted that customers refuse to accept steeper price updates, fearing immediate losses in market share.

- AI Adoption Stalling: Special surveys by the Dallas Fed highlighted a brief plateau in AI integration, though roughly two-thirds of surveyed companies operate as active users. The vast majority (84%) indicate that the tool has caused no immediate shifts to their total headcount.

Hardware, Storage, & Data Centers

An extreme imbalance between soaring AI infrastructure demand and limited manufacturing capacity has propelled data storage stocks to new heights. Producers like Micron Technology (joining the trillion-dollar market cap club), Seagate, and Western Digital have all tapped fresh multi-week highs. Compute prices continue to rise alongside rental pricing index spikes for next-generation Nvidia chips.

Private Credit Structural Shift

A private credit arrangement was engineered to fund Anthropic’s hardware acquisition cost efficiently. A financed special purpose vehicle (SPV) backed by Apollo and Blackstone will buy tensor processing units from Alphabet and lease them to Anthropic. Broadcom will act as a secondary shortfall guarantor. This underscores Anthropic’s asset-light business model, which has allowed its annualized revenue run rate to swell to $47 billion.