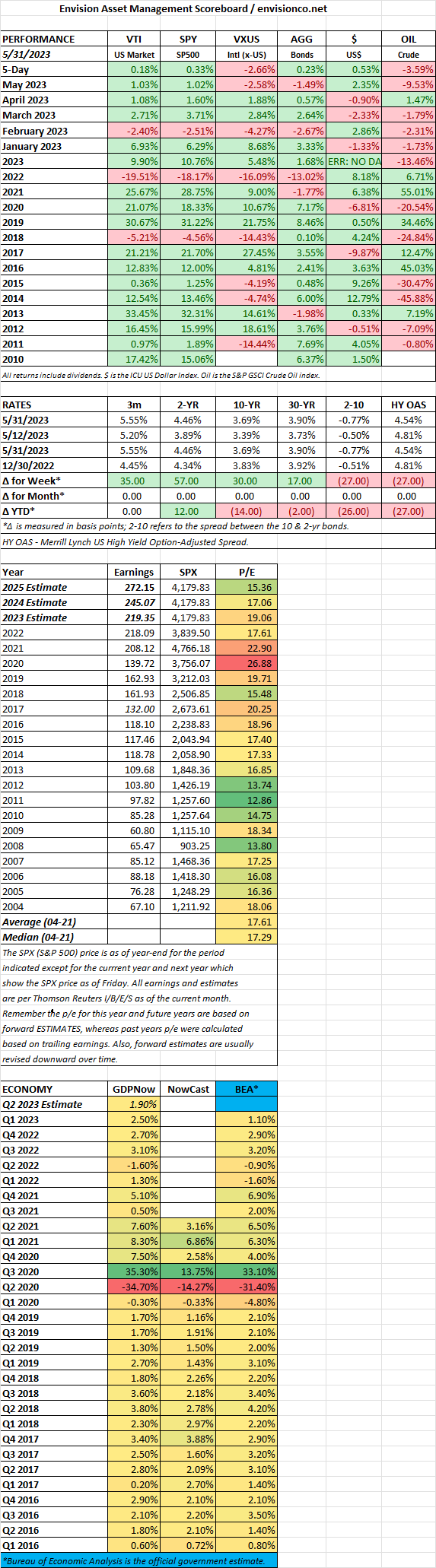

Monthly Archives: May 2023

Week Ending 5/19/2023

MARKET RECAP

- US stocks +1.70%, international +0.65%, bonds -1.32%.

- The market continues up despite all the bad news and the consensus that it should go down.

- Tech stocks are flying especially if they are connected to AI.

- The Leading Economic Indicators (LEI) have now fallen for 13 straight months.

- The debt ceiling is still not fixed with time running out.

- BofA’s global fund survey shows managers expect a soft landing.

SCOREBOARD

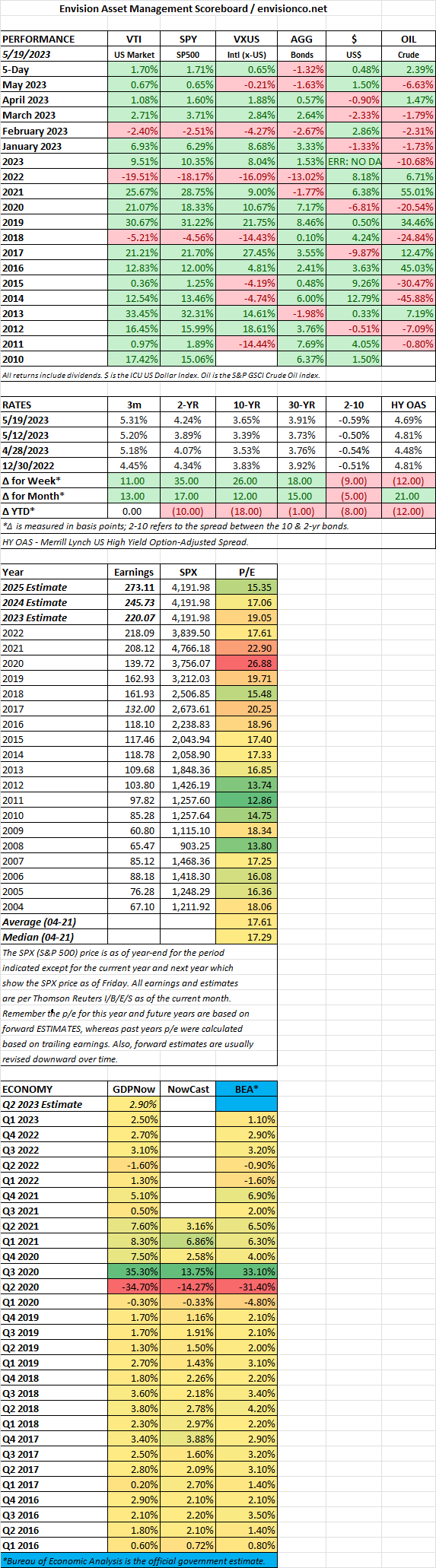

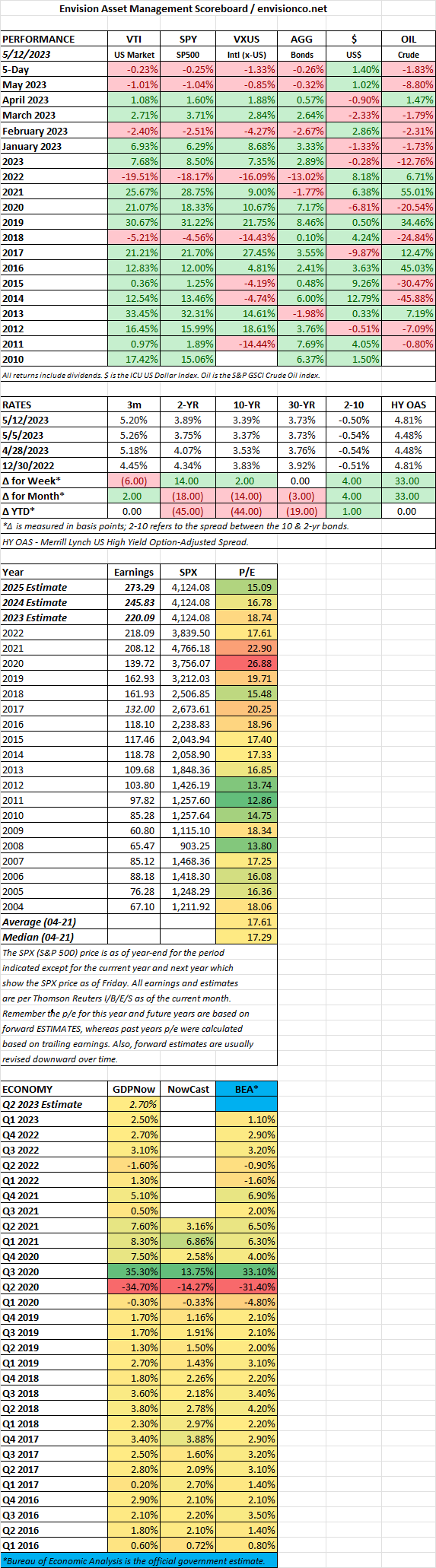

Week Ending 5/12/2023

MARKET RECAP

- US stocks fell by 0.23%, barely budging despite no debt limit deal with about two weeks remaining.

- The S&P 500 moved less than 1% in either direction in the sixth week in a row.

- One-month t-bills were yielding 5.79% due to the risk of default.

- Biden has an approval rating of 37%, the lowest since Truman’s second term. This, despite a 3.4% unemployment rate.

- Jonathan Golub, chief US equity strategist at Credit Suisse, says the S&P 500 has returned 16.9% on average in the 12 months following the last interest rate hike of a cycle.

- But there are still lots of negatives – the probability of default; inflation is still high, more potential problems in the banking system, high p/e ratio in the market, and negative earnings growth.

- CPI declined for the 10th straight month (4.9% YoY), and PPI is increasing at its slowest rate since 2021.

- Discretionary investors are underweight stocks, in the 9th percentile historically, providing possible fuel if the market starts moving higher.

SCOREBOARD

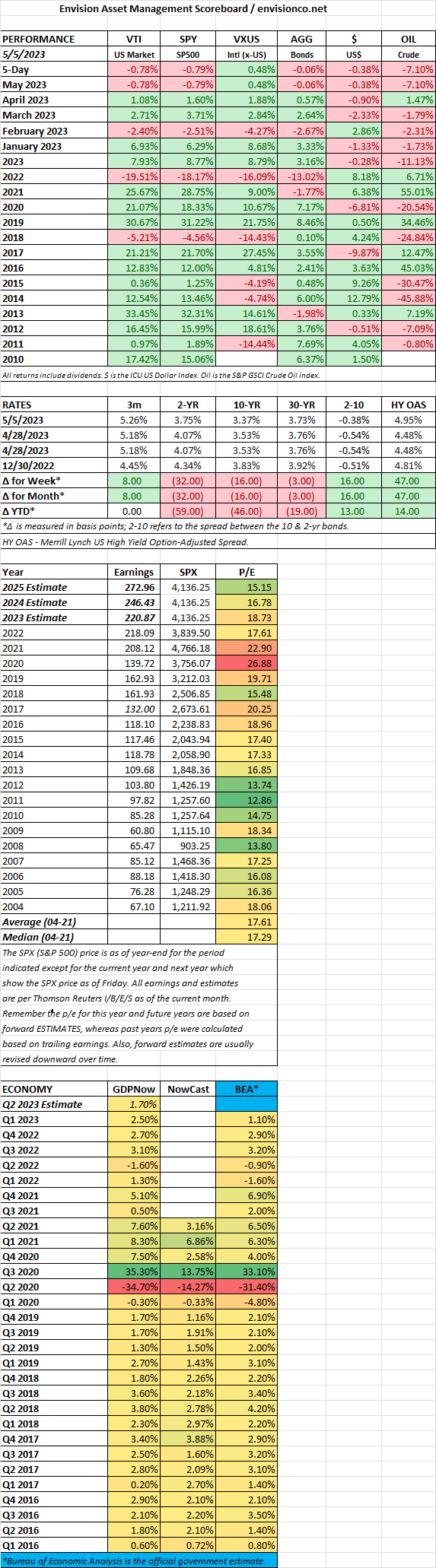

Week Ending 5/5/2023

MARKET RECAP

US stocks fell by 0.78%, while international stocks managed an advance of 0.48%.

The US added 253,000 jobs in April, indicating that the labor market continues to be solid, despite rising rates and the banking crisis. It was the best gain since January. The unemployment rate fell to 3.4%. Wages were up by 4.4% year over year.

During the week, the Fed raised its benchmark interest rate by one-quarter point to between 5% and 5.25%. Powell indicated the Fed might pause hikes until they have a better understanding of the impact of all of the recent increases. But the strong labor report might change that calculation.

Banking continues to be an area of concern. The SPDR Regional Banking ETF, KRE, fell by 10% on the week.

SCOREBOARD

April Recap

April 2023: Financial Markets Navigate a Sea of Calm (with Undercurrents)

April brought a sense of relative calm to financial markets, a welcome change after the volatility of previous months. However, beneath the surface lurked currents of uncertainty that could impact the future trajectory. Here’s a snapshot of the key themes:

Market Consolidation:

- Major indices saw modest gains, with the S&P 500 up 1.6%, the Dow Jones rising 2.6%, and the Nasdaq barely inching forward at 0.1%.

- The subdued trading reflected a balance between positive earnings surprises from large tech companies and lingering concerns about global inflation and ongoing geopolitical tensions.

Bond Market Stability:

- Interest rates stabilized, with the 10-year U.S. Treasury note holding steady at around 3.45%.

- This reflected the market’s perception of a measured pace of Federal Reserve rate hikes, despite continued hawkish rhetoric.

Mixed Sector Performance:

- Value stocks outperformed growth, with energy and financials leading the charge.

- Technology lagged behind, despite solid earnings from individual companies.

Global Market Divergence:

- Developed markets performed slightly better than emerging markets, with the MSCI EAFE rising 2.8% compared to the MSCI EM’s 1.1% decline.

- China’s economic slowdown and regional geopolitical anxieties weighed on emerging markets.

Other Notable Events:

- The International Monetary Fund (IMF) downgraded its global growth forecast, citing increased economic risks.

- The Bank of Japan maintained its ultra-loose monetary policy under new Governor Kazuo Ueda, highlighting the divergence in global monetary policy strategies.

Overall, April 2023 was a month of market consolidation marked by cautious optimism. However, the underlying currents of economic uncertainty and potential policy divergences could shape the next phase of the market’s performance. The ability of central banks to navigate the tightrope of inflation control and economic growth will be crucial in determining the future direction of financial markets.