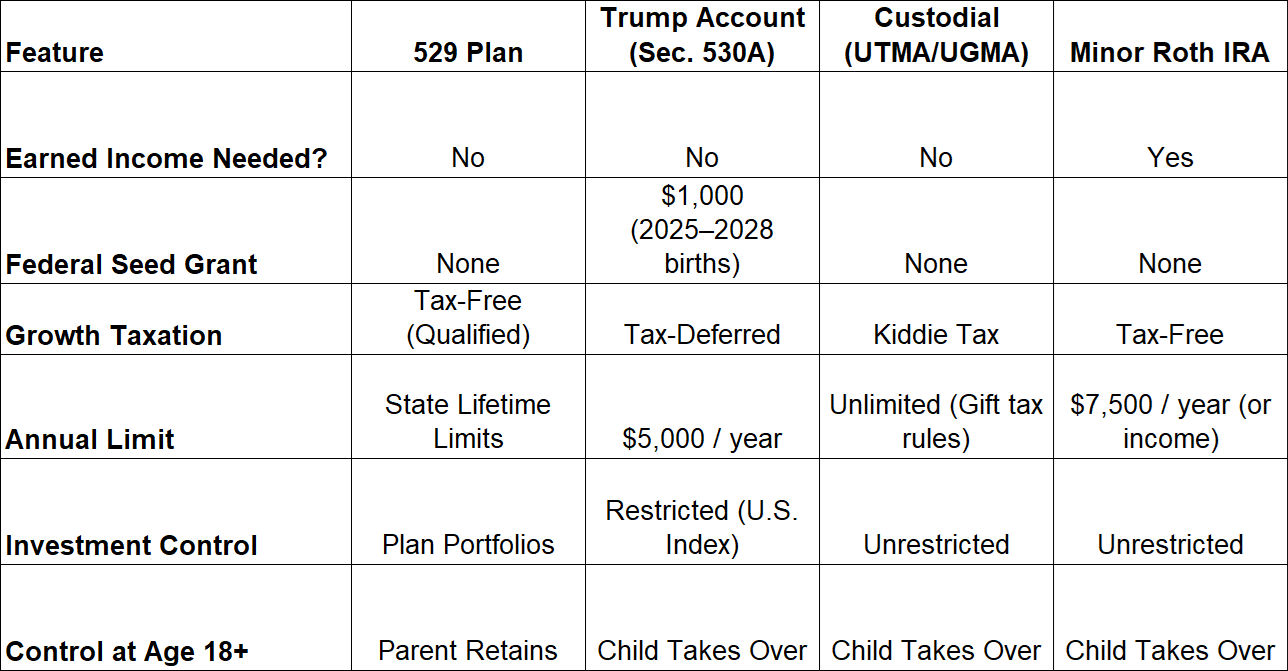

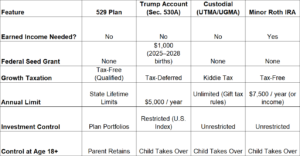

Beyond the Headlines: Navigating “Trump Accounts,” 529s, and Custodial Options for Your Child’s Future

With the passage of the One Big Beautiful Bill Act (OBBBA), parents and caregivers have a new financial tool to evaluate: Section 530A “Trump Accounts”. These accounts join established options like 529 Plans, Custodial Brokerage Accounts (UTMA/UGMA), and Minor Roth IRAs.

Choosing the right account—or combination of accounts—requires balancing immediate tax benefits, long-term growth potential, investment control, and the intended use of the funds.

Here is a breakdown of how these vehicles compare and a strategic framework for prioritizing your contributions.

Understanding the Landscape: Account Summaries

1. Section 530A Trump Accounts

Trump Accounts are structured as a child-centric version of a Traditional IRA.

-

The Pitch: Children born between January 1, 2025, and December 31, 2028, who are U.S. citizens are eligible for a one-time $1,000 federal grant.

-

Funding: Anyone can contribute using after-tax dollars, up to $5,000 annually per beneficiary. Uniquely, the child does not need earned income to accept contributions.

-

Investment Profile: Prior to age 18, assets are locked into broad-market U.S. index funds (such as S&P 500 trackers).

-

Taxation: Growth is tax-deferred. Withdrawals after age 18 are taxed as ordinary income on the growth/pre-tax portions. Non-qualified withdrawals prior to age 59½ face standard IRA restrictions and a 10% penalty (with exceptions for qualified higher education, first-time home purchases, and minor emergencies).

2. 529 Education Savings Plans

The premier vehicle for education-targeted savings.

-

Tax Edge: Contributions are made with after-tax dollars, but all growth and withdrawals are completely federal- and state-tax-free when used for qualified education expenses (higher education, trade schools, or up to $10,000/year in K–12 tuition).

-

Control & Flexibility: Parents retain full control indefinitely. Beneficiaries can be changed to other family members, and up to $35,000 in unused funds can be rolled over into a Roth IRA for the beneficiary (subject to annual IRA limits and account tenure rules).

3. Custodial Accounts (UTMA / UGMA)

Taxable brokerage accounts managed by an adult for the benefit of a minor.

-

Taxation: Subject to “Kiddie Tax” rules. The first $1,350 of unearned income is tax-exempt, the next $1,350 is taxed at the child’s lower tax bracket, and earnings above $2,700 are taxed at the parents’ rate.

-

Flexibility & Control: Zero restrictions on how money is spent, provided it directly benefits the child (cars, sports travel, early milestones). However, full control shifts entirely to the child once they reach the legal age of majority (18 to 21, depending on the state).

4. Minor Roth IRAs

The ultimate tax-free retirement chassis for working youth.

-

Requirement: The child must have legitimate earned income (W-2 or documented self-employment).

-

Tax Edge: Contributions are made after-tax, but growth and qualified withdrawals in retirement are 100% tax-free. Original contributions can be withdrawn at any time without tax or penalty.

-

The Recommended Funding Hierarchy

Determining where to deposit the next dollar comes down to tax efficiency and intended use. Here is a recommended framework for families:

Tier 1: Free Government Money – claim the $1,000 Federal Grant (Trump Account, if eligible)

Tier 2: Education Savings – fund a 529 Plan (to cover projected K-12 / College costs)

Tier 3: Earned Income Optimization – fund a Minor Roth IRA (if the child works)

Tier 4: Long-Term Wealth & Pre-18 Flexibility – Trump account contributions or a custodial account

Step 1: Claim Free Capital First

If you have a child born between 2025 and 2028, file IRS Form 4547 (electronically or with your tax return) to establish a Trump Account and capture the $1,000 federal grant. Even without adding personal funds, that initial seed compounded over decades provides an automatic head start.

Step 2: Prioritize Tax-Free Vehicles for Targeted Goals

If education is a priority, direct long-term savings into a 529 Plan. Complete tax-exemption on investment growth provides a significantly higher net return than the tax-deferred growth of a Trump Account. Furthermore, if funds remain unused, up to $35,000 can be rolled into a Roth IRA later on.

Step 3: Utilize a Minor Roth IRA for Working Children

If your child earns income (modeling, refereeing soccer matches, household W-2 employment), prioritize a Minor Roth IRA over a Trump Account. Both use after-tax contributions, but the Roth IRA yields tax-free distributions down the road rather than taxable distributions.

Step 4: Balance Remaining Surplus Between UTMA and Trump Accounts

When deciding where to park additional general-purpose savings:

-

Select a Trump Account if you value tax-deferred compounding for long-term adult milestones (retirement, first home) and prefer automated, low-cost index investing.

-

Select a UTMA/UGMA Account if you need liquidity to pay for major pre-18 expenses (e.g., competitive sports fees, a vehicle) or want complete freedom over custom asset allocation.

Bottom Line

No single account meets every need. Combining the free seed money of a Trump Account with the tax-exempt growth of a 529 Plan creates a balanced foundation for both early adult needs and ultra long-term financial independence.

Disclaimer: Tax laws are complex and subject to change. Consult a Certified Public Accountant (CPA) or financial advisor to customize an investment structure tailored to your family’s tax bracket and financial goals.