Monthly Archives: June 2023

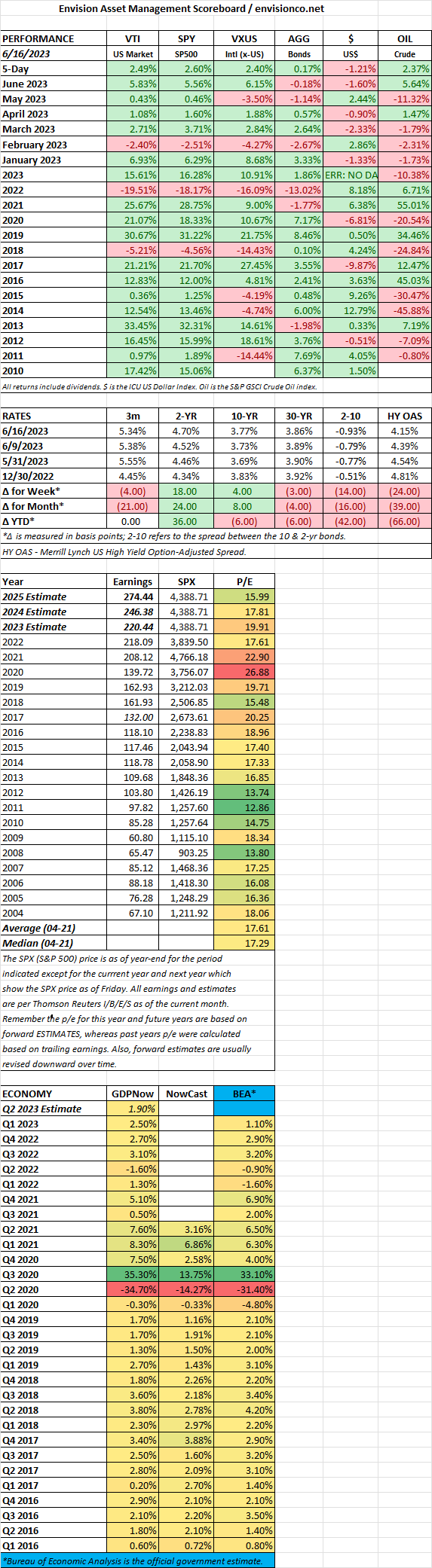

Week Ending 6/16/2023

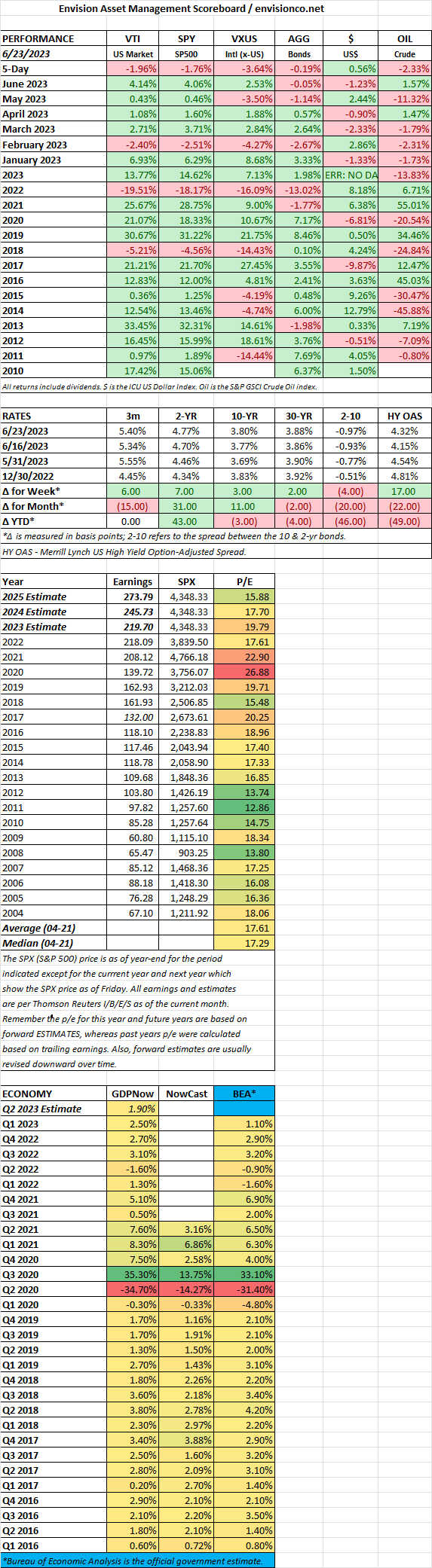

SCOREBOARD 6/16/2023

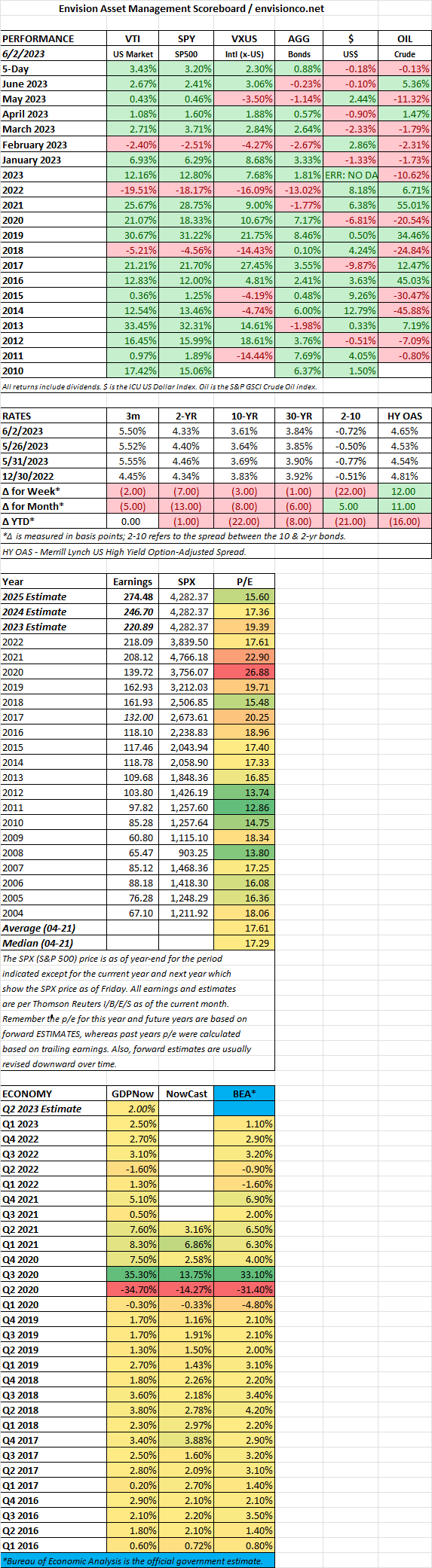

Week Ending 6/3/2023

MARKET RECAP

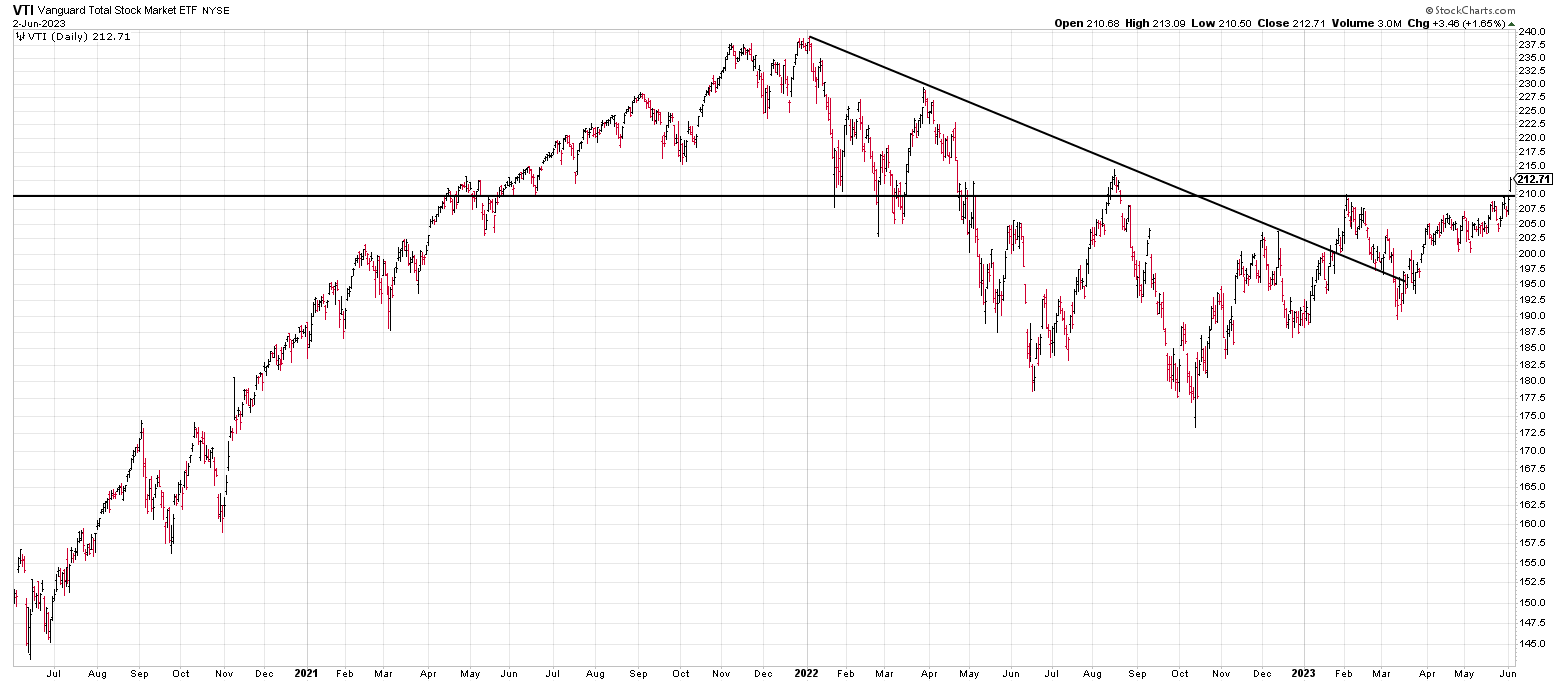

US stocks had a breakout week, up by 3.43% and moving up through resistance. Despite all the bad news out there, stocks continue to push higher.

Washington managed to make a deal to save the country from default. Of course, according to Bloomberg economists Anna Wong and Maeva Cousin, it will barely make a dent in the continued disastrous trajectory of US debt, estimated to rise from 97% of GDP to 130% by 2033.

Biden signed the debt deal into law on Saturday, meaning a tidal wave of US Treasuries will come to market this week. It will be interesting to see how the market handles it.

Non-farm payrolls were up by 339,000, beating the 195,000 consensus. Bianco Research said it was the 14th consecutive monthly reading in which payrolls topped economist expectations. The prior two months were revised up by almost 100,000. The labor-force participation rate was 62.6%, the same as in May and lower than the prepandemic level of 63.3%. The average workweek fell to 34.3 hours, the lowest since April 2020.

Between the strong jobs report and the debt ceiling resolution, the Dow jumped by just over 700 points on the news, the largest one-day gain since November.

SCOREBOARD

May Recap

May 2023: A Fragile Rally Under Uncertain Skies

May painted a complex picture for financial markets, offering a glimpse of potential recovery tinged with worries about the future. Here’s a breakdown of the key themes:

Global Stock Market Divergence:

- In dollar terms, global equities slipped 1.1%, highlighting a divergence in regional performance.

- The US Nasdaq Composite soared 5.93%, fueled by continued enthusiasm for artificial intelligence and strong tech earnings.

- Conversely, the Dow Jones Industrial Average dipped 3.17%, and the S&P 500 managed a meager 0.43% gain, reflecting broader economic anxieties.

- European markets fared better, with the DAX and CAC 40 registering positive returns.

Mixed Signals on Inflation:

- April’s disinflationary trend continued, with the Consumer Price Index (CPI) edging down to 4.9%.

- However, this was offset by a tenth Federal Reserve rate hike, pushing the 10-year Treasury yield up to 3.635%.

- This mixed bag of data left investors unsure about the future trajectory of inflation and Fed policy, leading to market unease.

Sector Rotation and Commodity Reversal:

- Value stocks, particularly energy and financials, outperformed growth, reflecting concerns about rising interest rates and their impact on tech-heavy sectors.

- Commodities prices tumbled, with the Bloomberg Commodity Index falling 5.64%, as recessionary fears dampened demand.

- Oil prices plunged, reflecting worries about slowing global economic growth.

Other Notable Events:

- The US debt ceiling was temporarily suspended, averting a potential fiscal crisis.

- The Bank of England and the European Central Bank began their own tightening cycles, adding to global monetary policy divergence.

- Geopolitical tensions remained high, with the war in Ukraine and increasing China-US rivalry impacting market sentiment.

Overall, May 2023 showcased a fragile rally fueled by specific sectoral trends, but overshadowed by concerns about economic uncertainty, rising interest rates, and geopolitical factors. The upcoming months will be crucial in determining whether this tentative resurgence can translate into sustained market growth or if anxieties prevail.