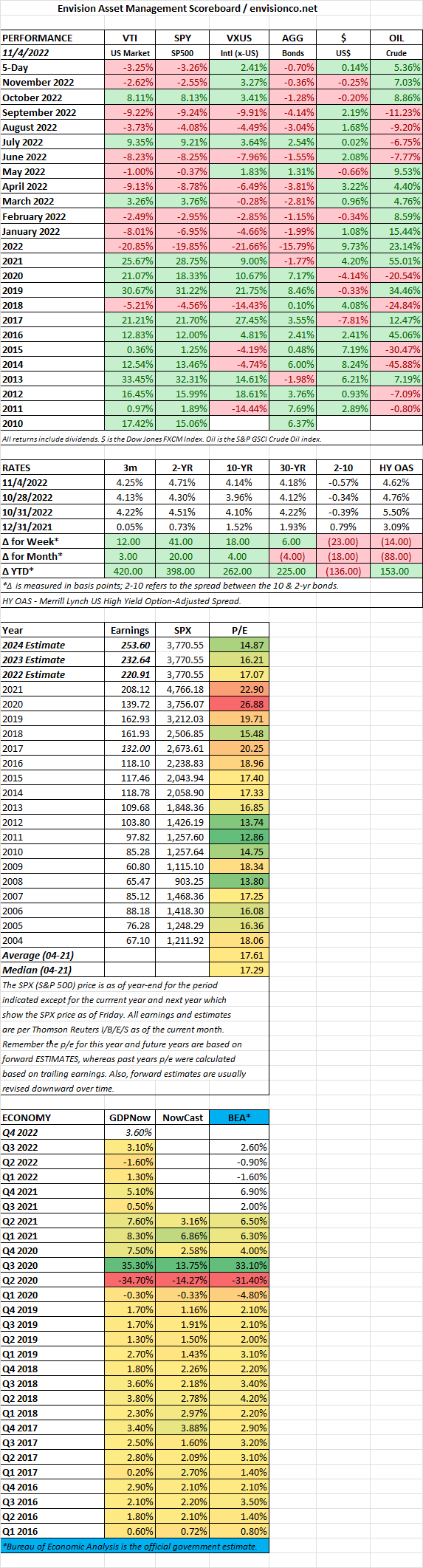

SCOREBOARD

SCOREBOARD

MARKET RECAP

Stocks were down this week, by 0.87% in the US and 0.73% outside the US. The bond index rallied by 0.51%, interest rates fell by 35 basis points on the 10-year.

Producer prices were up by 8% compared to last year, which was lower than 8.4% in September and 11.7% at the March peak.

The spread between the 10-year and the 2-year treasury has reached its highest point since the early 80s at 69 basis points. Such a differential was a precursor to recessions in the past. Meanwhile, Q4 looks on track for solid growth. The Atlanta Fed’s GDPNow model has Q4 growth at 4.2%. There was also a strong retail sales report, up 1.3% in October, the best gain since February and higher than the 1% consensus.

The incredible FTX saga continues. It turns out the financials are a complete mess. John Ray, who took over as CEO and is a restructuring expert, said “never in my career have I seen such a complete failure of corporate controls and such a complete absence of trustworthy financial information.”

There appears to be $900 million in marketable assets against $9 billion of liabilities just before the bankruptcy filing. There were minor cryptocurrencies held on the balance sheet for big amounts that had negligible value. Supposedly Serum was recorded at $2.2 billion but is worth less than $100 million if even that. Furthermore, Serum was a token that FTX created (read Matt Levine’s article at Bloomberg for much more).

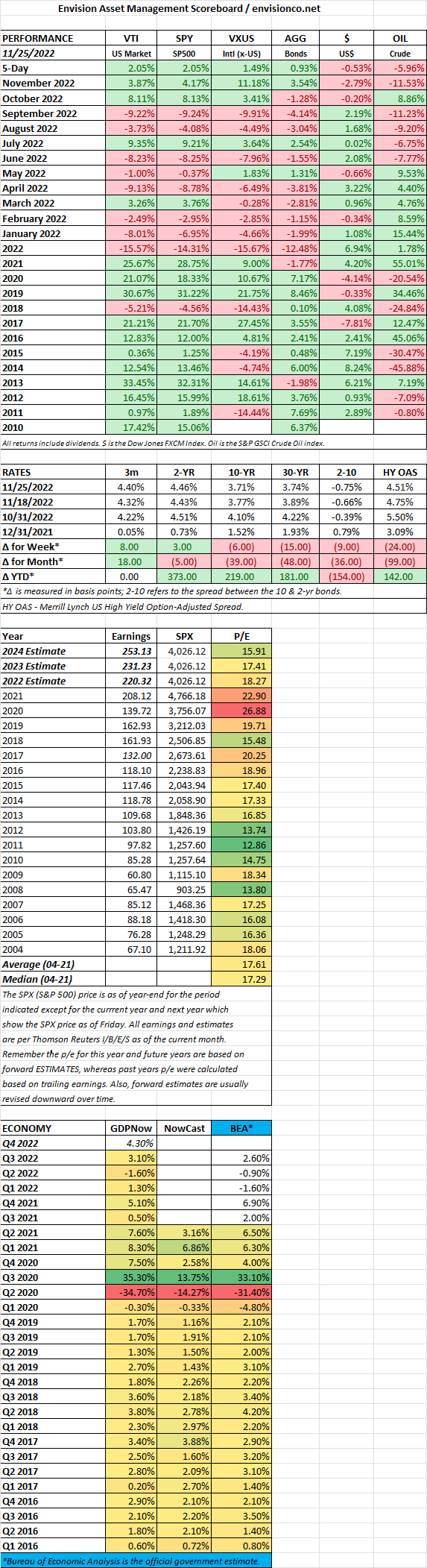

SCOREBOARD

Tracy Alloway from Bloomberg writes about the collapse of FTX, the comparison to the Beanie Baby phenomenon in the ’90s, and how when speculation collapses, all that is left is the utility value, and if there no utility value, that means $0.

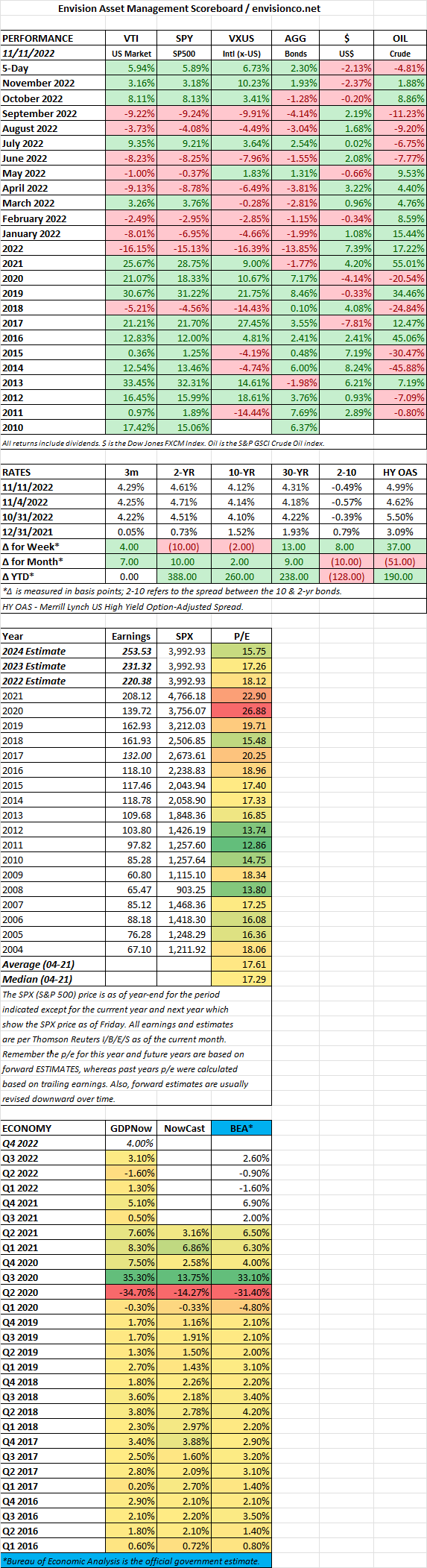

MARKET RECAP

A big week for stocks worldwide as the inflation report came in slightly less than the consensus estimate. US markets were up by 5.94%, international stocks increased by 6.73%, and bonds rallied by 2.30% on lower interest rates. The October consumer price index was up by 7.7% compared to last year, below the estimate of 8%, and lower than the September print of 8.2%. Investors also will get a split government, as it looks like the House will slide just barely to the Republicans, and the Democrats will keep the Senate. That formula has generally worked out well for investors.

But the Republicans certainly were not happy with that outcome. It was a big underperformance given all the cards stacked up in their favor. At some point, the Republicans have to finally get the message, that Trump has been a disaster for their electoral hopes since he was elected back in 2016. In the 2018 mid-terms, despite a strong economy, the GOP lost 41 house seats. He lost the 2020 presidential election. When it was discovered that he was pressuring state officials in Georgia to turn the vote in his favor, his actions probably cost the GOP the Senate runoff. And then this past week, most of his endorsed candidates failed miserably in elections that would have been winnable with normal, sane candidates. Despite high inflation, high mortgage rates, the threat of a recession, and an unpopular President, it looks like the Democrats will only lose about 11 House seats, and they held on to the Senate, in what should have been a big year for the Republicans.

The Crypto world continues to fall apart. In an incredible turnaround from King of the block (chain) to bankruptcy, FTX disintegrated in five days, and CEO Sam Bankman-Fried, who was doing a good white knight impersonation of JP Morgan from 1907 just a few months ago, went from a net worth of $25 billion to $0 in a flash. So far the crash hasn’t spilled over into the traditional financial markets but time will tell.

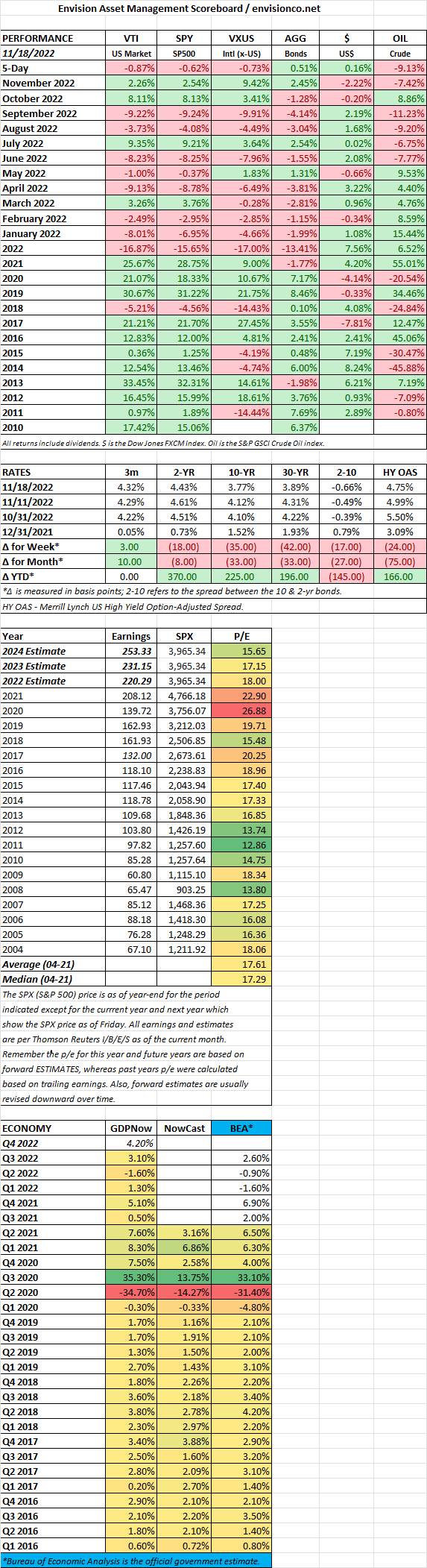

SCOREBOARD

MARKET RECAP

The S&P 500 fell by 3.35% and the Nasdaq was off by 5.65% on fears of more interest rate increases. The Fed doesn’t seem concerned that they might be overdoing it and is intent on increasing rates until inflation breaks, no matter what the damage. Similar to what they did on keeping interest rates at essentially zero for way too long, no matter what the damage.

The market has now retraced about half of the recent market gain.

Fed Chair Jerome Powell said, “We still have some ways to go, and incoming data since our last meeting suggest that the ultimate level of interest rates will be higher than previously expected.”

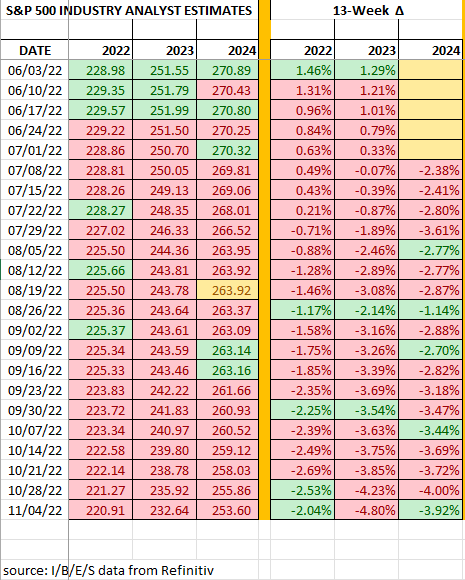

Projected earnings estimates have been dropping at an accelerating rate. The 2023 estimates have fallen by 4.80% over the last 13 weeks. But economic growth for Q4 is looking decent, the Atlanta Fed’s GDP Model has Q4 growth at 3.6%.

Employment increased by 261,000 jobs in October, the lowest amount since December of 2020, but still greater than the pre-pandemic average of 198,000. The unemployment rate increased to 3.7%. The report shows that the jobs market, while still positive, is beginning to lose momentum. Twitter, Lyft, and Stripe all announced layoffs this week. Average hourly earnings were up by 0.4% in October versus 0.3% in September. But year over year, the increase was 4.7% compared to 5% in October, both off from the 5.6% March high point.

SCOREBOARD