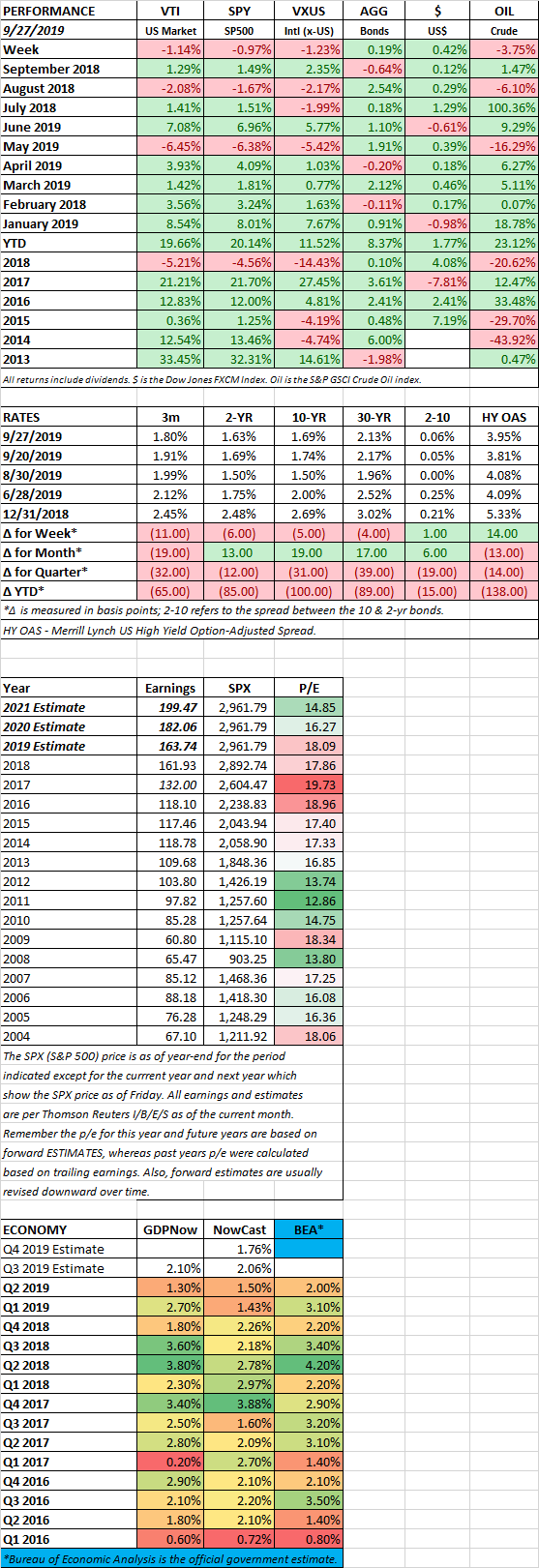

MARKET RECAP

US stocks dropped by 1.14% and international stocks were down by 1.23%. An impeachment inquiry began on Trump, the repo market needed more help, and Germany seems close to a recession, add on to that a word that the US might delist Chinese companies from US markets, and it was enough to push stocks lower for the week.

TRUMP

House Speaker Nancy Pelosi began an impeachment inquiry of Trump after a whistle-blower complaint that the President withheld military aid to Ukraine in order to pressure them to investigate Joe Biden and his son.

REPO MARKET

The Repo market was in need of continued help this week. The Fed injected $50 billion on Monday and then doubled that by midweek. The problems most likely stem from the draining of reserves from the system.

GERMANY

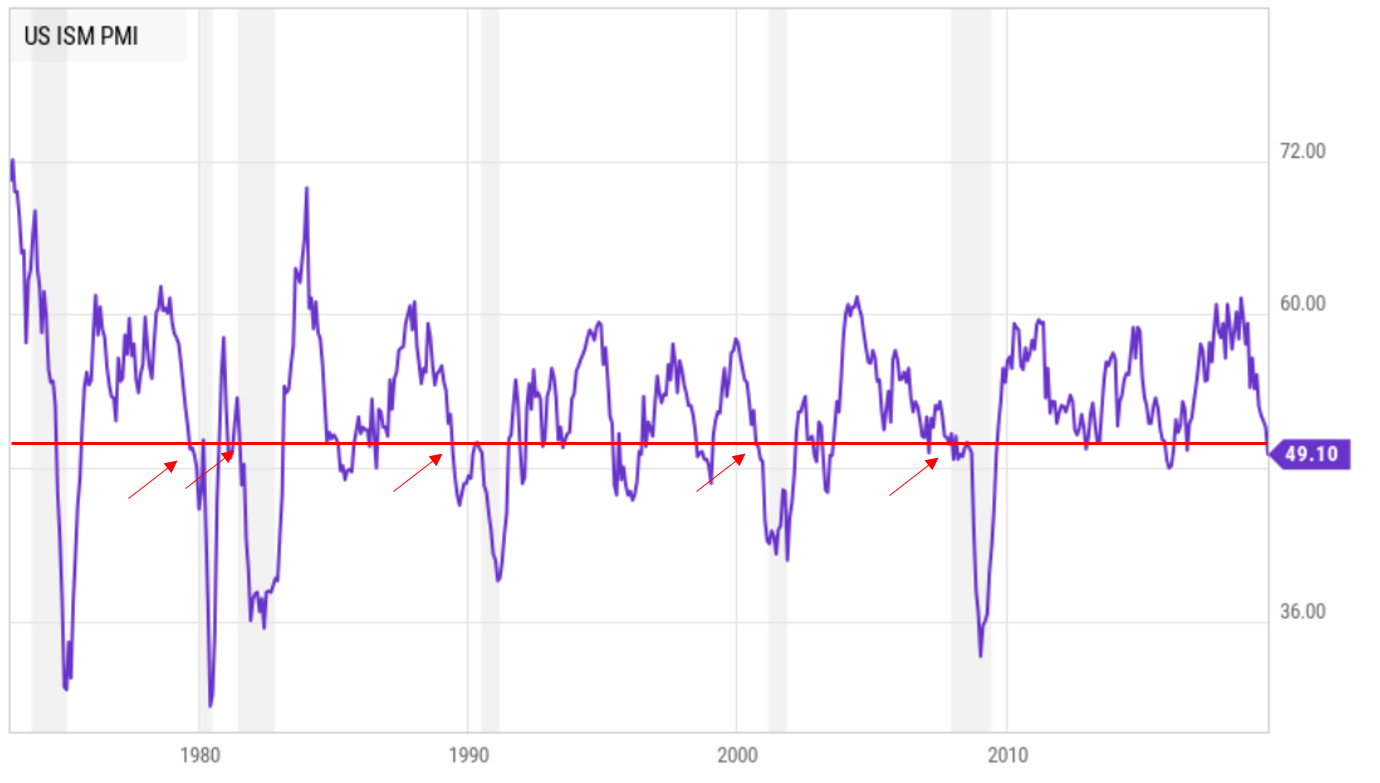

The German IHSMarkit composite output index entered contractionary territory for the first time since April of 2013. The rate of decline was the steepest in seven years. Growth in the service sector slowed sharply. For the manufacturing index, it was the eighth straight decline in output.

Phil Smith, Principal Economist at IHS Markit said: “Another month, another set of gloomy PMI figures for Germany, this time showing the headline Composite Output Index at its lowest since October 2012 and firmly in contraction territory. “The economy is limping towards the final quarter of the year and, on its current trajectory, might not see any growth before the end of 2019. “The manufacturing numbers are simply awful. All the uncertainty around trade wars, the outlook for the car industry and Brexit are paralyzing order books, with September seeing the worst performance from the sector since the depths of the financial crisis in 2009. With job creation across Germany stalling, the domestic-oriented service sector has lost one of its main pillars of growth. A first fall in services new business for over four-and-a-half years provides evidence that demand across Germany is already starting to deteriorate.”

WE WORK / PELOTON

We Work pulled its IPO last week after it was apparent that the public markets would not value the Company at any level close to its recent private valuations. Adam Neumann, We’s dynamic founder, subsequently stepped down after pressure from its lead investors.

Peloton didn’t have to pull back its IPO, but its offering did not go as expected, dropping 10% on its first day. Further evidence that the public markets are taking a more rational approach to valuation, and that artificially low-interest rates and easy money have given many start-ups and their private investors a sense that positive cash flow simply doesn’t matter, but ultimately, it does, at least recently.

SCOREBOARD