MARKET RECAP

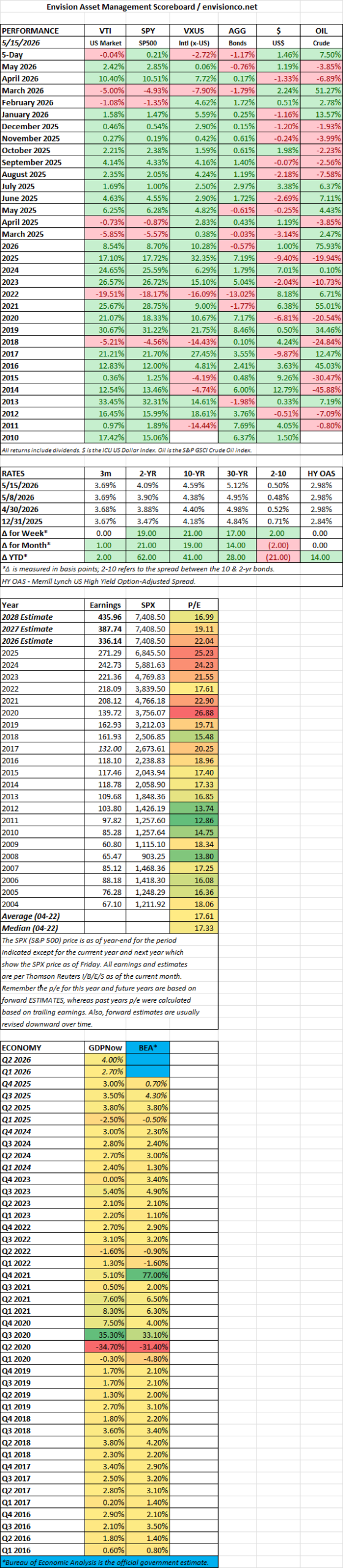

US equity markets ended the week ending May 15, 2026, with modest or flat performance after hitting records mid-week but pulling back sharply on Friday amid rising yields and hotter-than-expected inflation data. The S&P 500 closed at 7,408.50 on May 15 (up from 7,398.93 on May 8), for a weekly gain of about +0.13% (roughly +9.57 points, or around +0.1–0.21% depending on exact intra-week references). The Dow Jones Industrial Average closed at 49,526.17 (down from 49,609.16 the prior Friday), posting a small weekly loss of about -0.2%. The Nasdaq Composite closed at 26,225.14 (down from 26,247.08), ending essentially flat to slightly negative for the week.

International stocks, proxied by the Vanguard Total International Stock ETF (VXUS), faced downward pressure late in the week. VXUS closed at $83.11 on May 15 (down from around $85.43 on May 8), reflecting a weekly decline of roughly 2.7%. This mirrored broader global equity softness amid a stronger US dollar and rising Treasury yields, though international markets had shown relative strength earlier in 2026.

The bond market came under pressure as Treasury yields rose notably on persistent inflation concerns. The 10-year Treasury yield climbed from around 4.38% on May 8 to approximately 4.59% by May 15 (up roughly +21 basis points), driven by hotter CPI and PPI readings, resilient jobs data, and shifting Fed expectations. This led to lower bond prices and contributed to the late-week equity selloff.

Bitcoin and gold showed mixed-to-negative results. Bitcoin traded in the $78,000–$81,000 range and closed the week modestly higher (around +0.7% in some daily snapshots, ending near $80,000–$81,000). Gold faced selling pressure and declined on the week (down roughly 1–3.5% depending on exact spot/futures tracking), closing around the $4,500–$4,650 area as higher yields and a stronger dollar weighed on the safe-haven metal.

Overall, the week featured resilient US equities early on (supported by earnings and AI themes) but gave way to volatility from macro pressures. Focus remains on inflation trends, Fed policy, and global developments heading into the next week.

SCOREBOARD