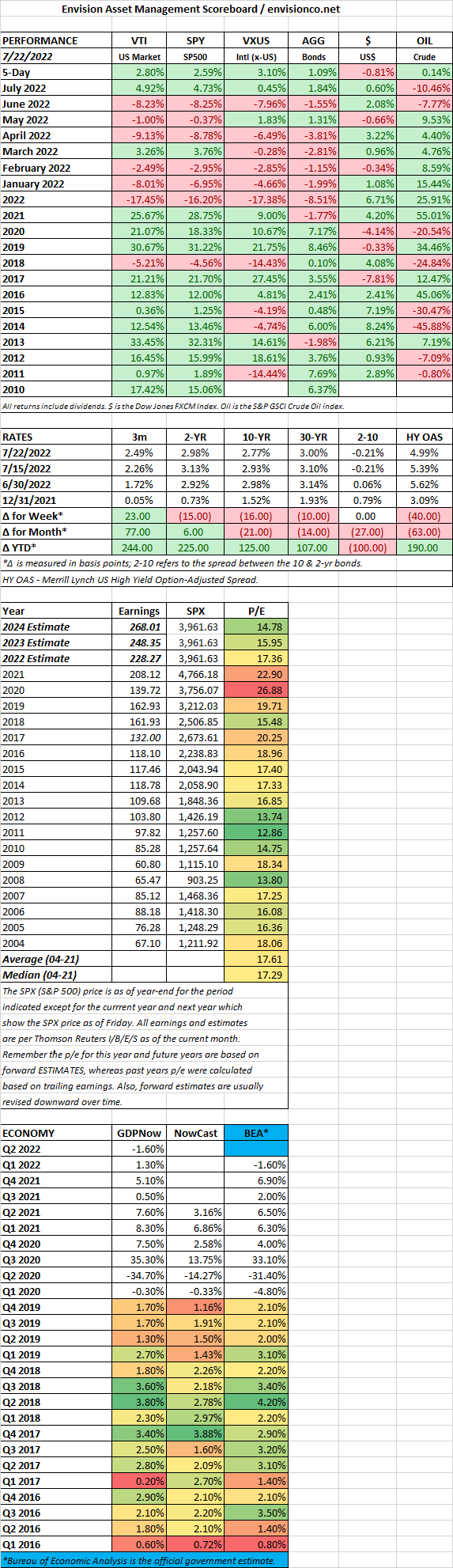

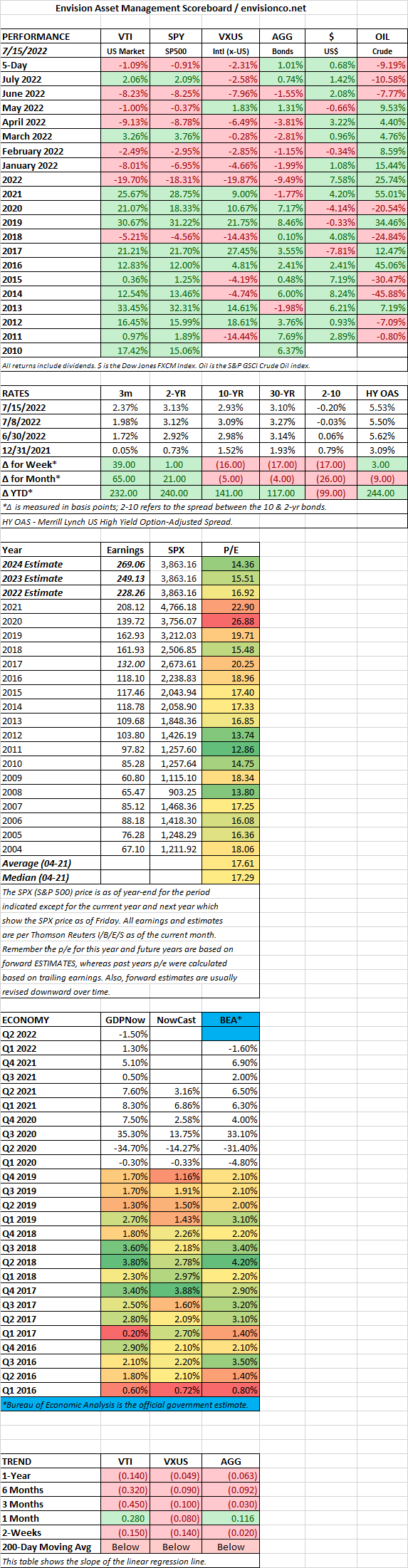

MARKET RECAP

US stocks increased by 2.8% for the week, putting in its best performance in a month. The international markets were up by 3.1%, and bonds jumped by 1.09% as interest rates fell sharply. But stocks did not close the week well, on Friday, the S&P 500 fell by 0.9% on disappointing earnings by Snap, which dropped by 39%. Meta and Alphabet fell in sympathy, registering drops of 7.6% and 5.6%.

S&P 500 companies have beaten estimates by 3.6% according to FactSet, lower than the five-year average of 8.8%. About 20% of companies have reported. But there is a chance that earnings growth will actually be lower when all is said and done, after backing out energy profits.

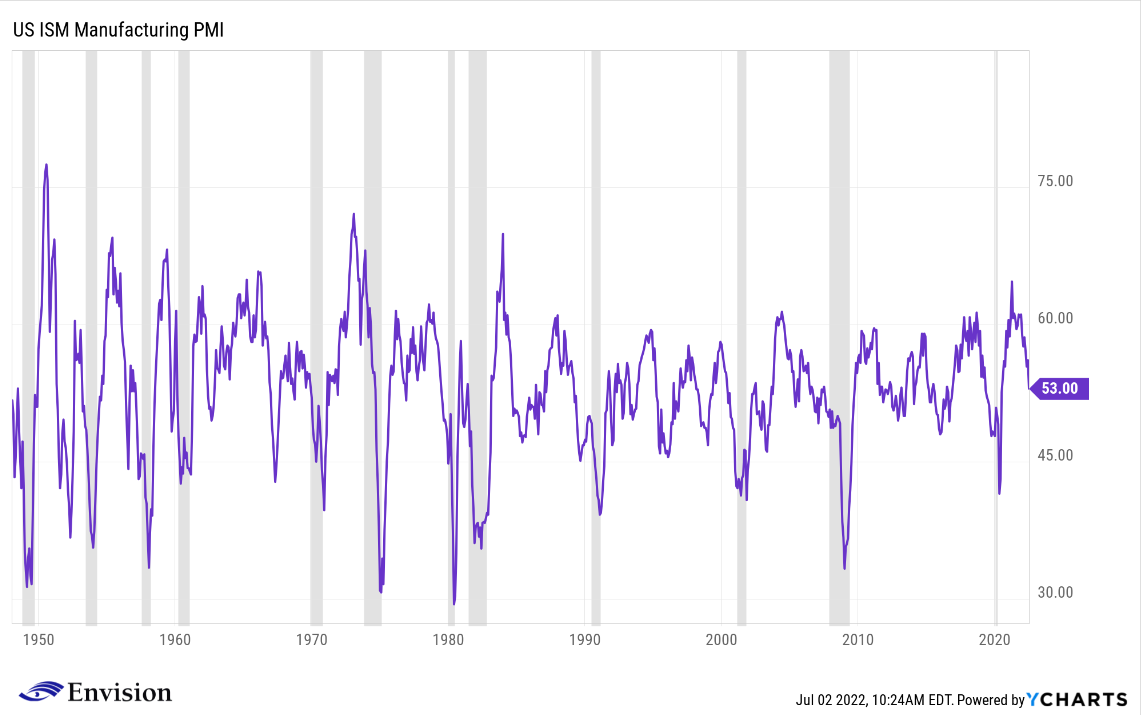

The Markit Composite Purchasing Managers Index fell into contractionary mode, registering a 47.5 score. Also, the Conference Board’s leading indicators turned negative. The composite PMI for Europe fell to 49.4 from 52.

Jobless claims continued their slow, but steady rise, with a 7,000 increase from last week to 251,000. The four-week average was up by 4,500 to 240,500. Continuing claims totaled 1.4 million and was up from 1.3 million the week prior. Guy Berger, the principal economist at LinkedIn said “It doesn’t look recessionary…but it’s definitely less good than it was before.”

The ECB raised rates by 50 basis points, bringing their key interest rate out of negative territory to zero. They also unveiled a plan to buy debt from the weaker countries.

SCOREBOARD