July 2023: Market Basking in Summer Sun, But Whispers of Autumn Chill the Air

July 2023 brought continued sunshine to financial markets, extending the gains of June, but whispers of cooler autumn winds started to ruffle investor confidence. Here’s a closer look at the key themes:

Equity Market Resilience:

- Major indices climbed for the fifth consecutive month, defying some earlier worries about a second-quarter earnings recession.

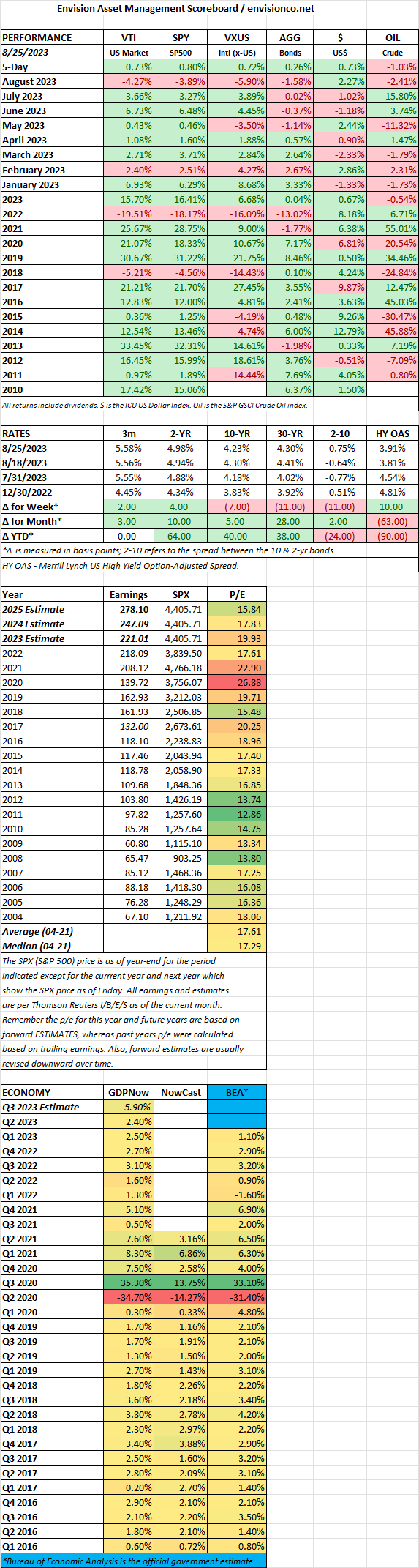

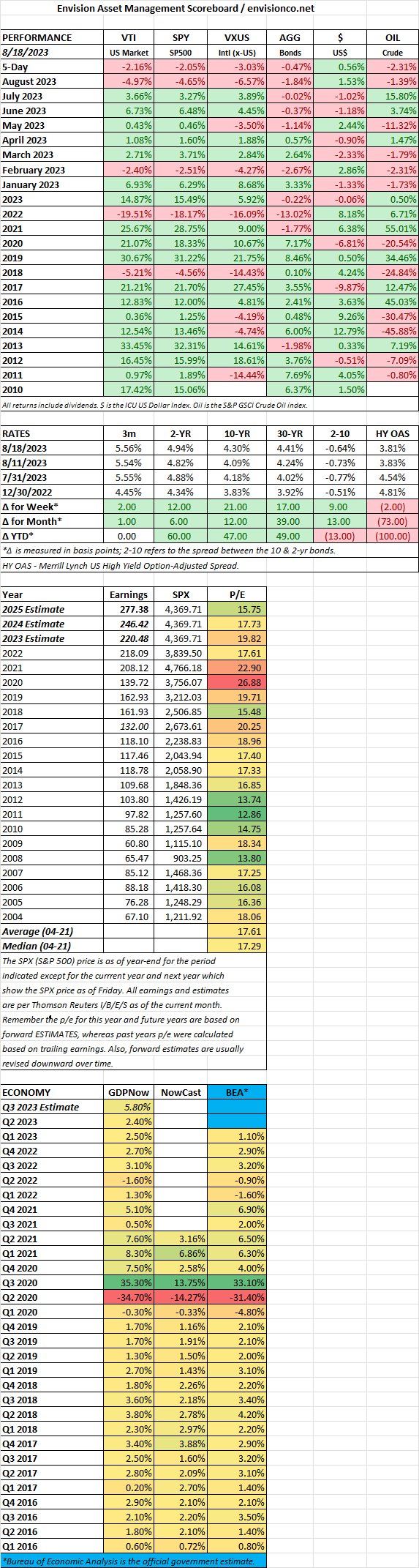

- The S&P 500 rose 3.2%, marking its longest sustained rally since August 2021. The Dow Jones climbed 3.4%, and the Nasdaq Composite gained 4.05%.

- Small-cap and micro-cap stocks outperformed mega-caps, reversing the recent trend.

Earnings Beat and Economic Data Uptick:

- Corporate earnings largely beat expectations, with the average EPS surpassing forecasts by 5.7%.

- Economic data was generally positive, with stronger-than-expected GDP growth and job numbers.

- Lower inflation in several developed markets, including the US, boosted optimism for a soft landing scenario despite the Fed’s continued rate hikes.

Shifting Risk Appetite:

- Despite positive numbers, some investor groups turned cautious. Bearish institutional investors started capitulating, indicating potential waning enthusiasm for equities.

- Fixed-income markets saw a modest decline in government bonds, while corporate bonds outperformed.

Sector and Regional Differences:

- Energy was the best-performing sector, benefiting from improved demand and supply constraints.

- Consumer discretionary stocks also did well, fueled by positive economic data and earnings reports.

- Foreign developed equity markets slightly outperformed the US in July, with the MSCI EAFE leading the S&P 500. Emerging markets surged almost 6.3%, showcasing their strong comeback after previous slumps.

Other Notable Events:

- The Federal Reserve raised rates by another 25 bps, bringing the benchmark rate to 5.25-5.50%, and hinted at slowing the pace of future hikes.

- The US Treasury yield on the 10-year note briefly topped 4.0% but ended July at 3.954%.

- Geopolitical tensions remained elevated, with the war in Ukraine and US-China relations presenting uncertainties.

Overall, July 2023 was a positive month for financial markets, but the optimism was tempered by concerns about future Fed actions and potential headwinds in the second half of the year. The upcoming months will be crucial in determining whether the summer rally can hold its heat or if the whispers of autumn chills become a reality.