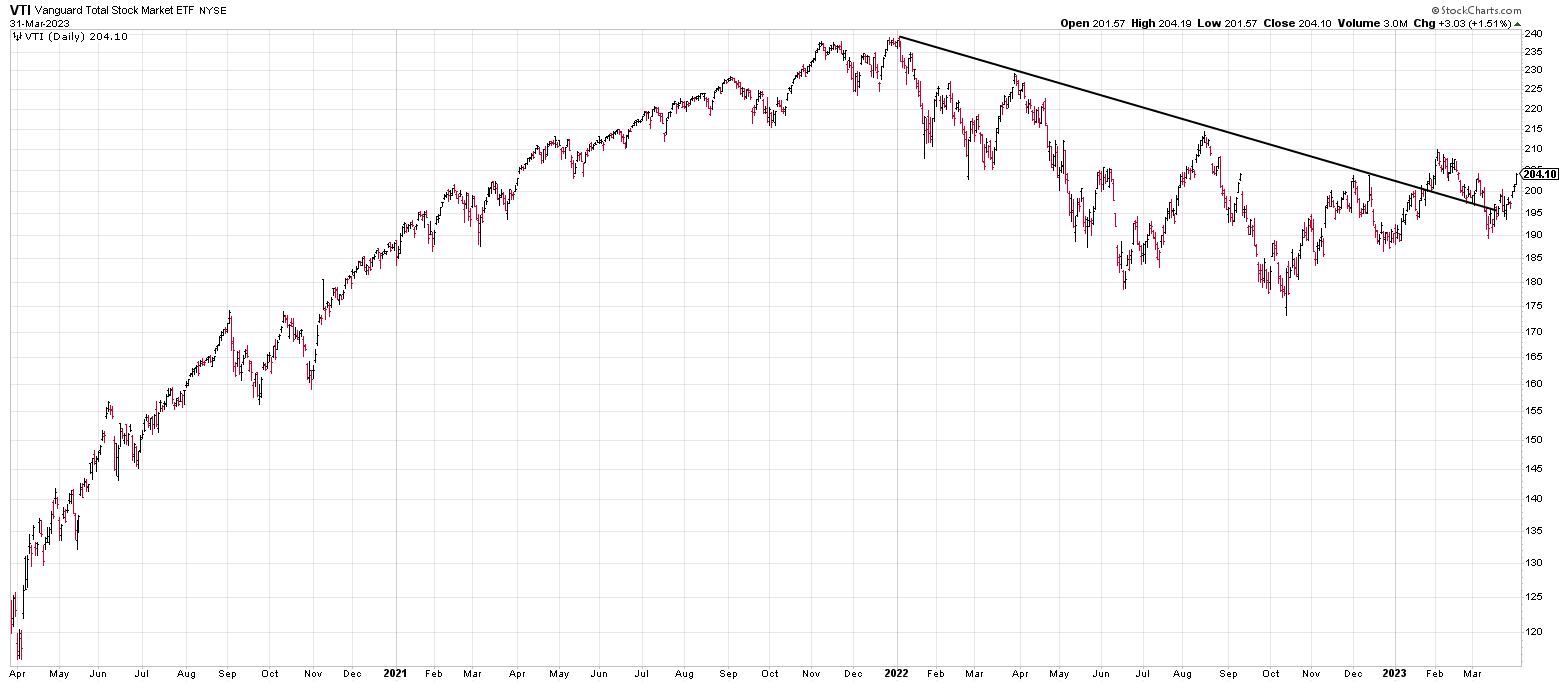

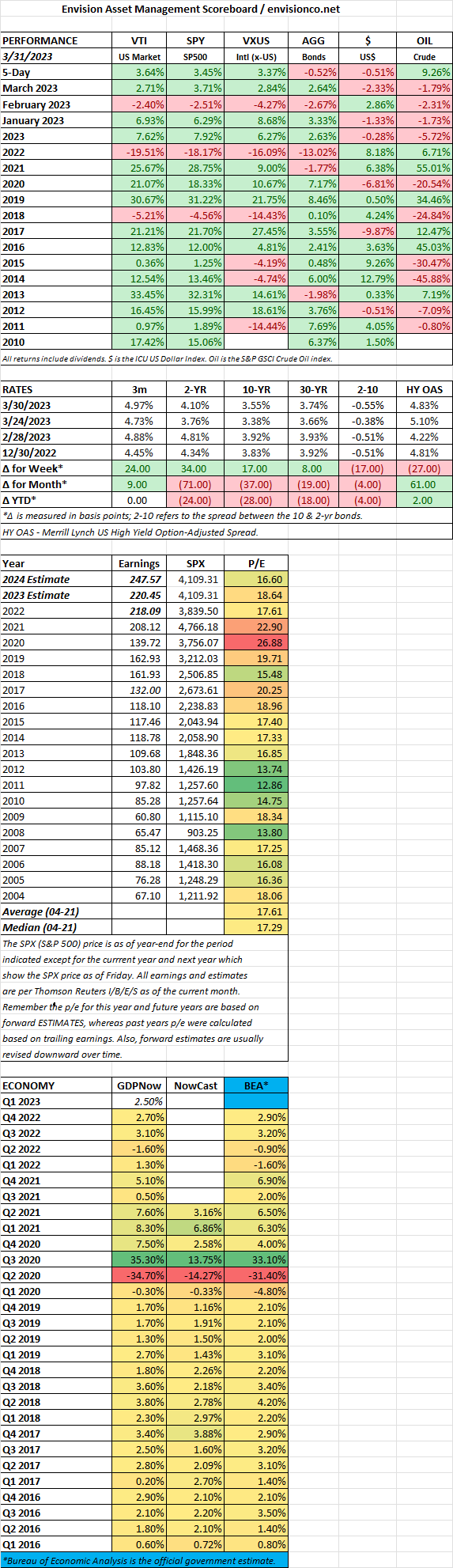

March 2023: Rebounding Spirits Amidst Banking Jitters

Following February’s pullback, March saw a rebound in sentiment for financial markets, albeit amidst new concerns. Here’s a breakdown of the key highlights:

Equity Market Bounce:

- Major indices recovered, defying some negative forecasts.

- The S&P 500 climbed 4.5%, the Dow Jones 3.4%, and the Nasdaq a staggering 17.05%.

- Growth stocks continued their outperformance, leading the charge in the recovery.

Fading Concerns Over Inflation:

- The CPI fell for the first time since October 2021, fueling hopes for peak inflation.

- This dovish sentiment led to a decline in long-term bond yields.

Central Bank Tightrope Walk:

- The Federal Reserve maintained its 0.25% rate hike pace, while acknowledging the potential for slower economic growth.

- Global central banks like the Bank of England and the European Central Bank also began a gradual process of policy tightening.

Banking Sector Stress:

- The collapse of Silicon Valley Bank, a key financial institution, rattled the banking sector and created short-term volatility.

- However, government interventions and broader market resilience minimized the damage.

International Markets Uptick:

- Developed markets like the MSCI EAFE recovered 4.2%, while emerging markets, particularly China, also bounced back with a 2.3% gain.

Other Notable Events:

- China set a lower GDP growth target of “around 5%” for 2023, indicating concerns about its economic slowdown.

- The ongoing war in Ukraine continued to contribute to supply chain disruptions and energy price volatility.

Overall, March was a month of renewed optimism for financial markets. The fading threat of inflation and cautious central bank actions allowed for a rally, despite the temporary shock of the banking crisis. However, uncertainty remains regarding the sustainability of the uptrend, with factors like geopolitics and potential economic headwinds playing a role.