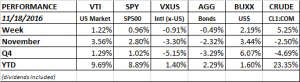

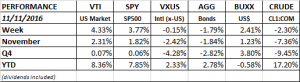

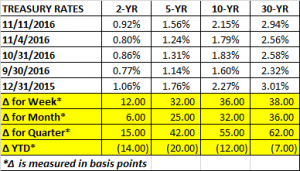

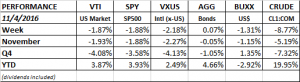

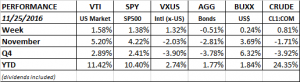

PERFORMANCE

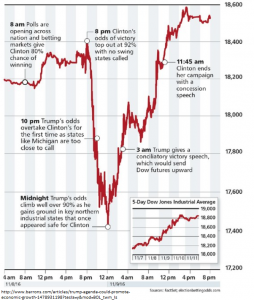

It was a repeat performance for the markets. Stocks up, bonds down, dollar and crude were up. The only difference was that international equities rebounded. The US indexes have advanced for three weeks. The Dow and the SP500 were up every day during the week and both hit record highs. Small stocks as measured by the Russell 2000 are up 15.8% over the last three weeks and have been up 15-days in a row.

One way to justify the recent run up in equity prices is Trump’s proposed corporate tax cuts. A cut in corporate taxes would go direct to the bottom line. Trump wants to drop rates from 35% to 15%. If the tax rate drops just halfway to 25%, that might raise SP500 earnings by about 10%. According to Factset, the 12-month forward EPS estimate is $131.19. If tax cuts increased earnings by 10%, that would be $144.30 and that would lower the forward 12-month p/e ratio from 16.87 to 15.33.

Based on history, SP500 earnings estimates going out one year are usually too high and will come down as we move forward. But even with that, a tax cut makes the p/e ratio much more reasonable.

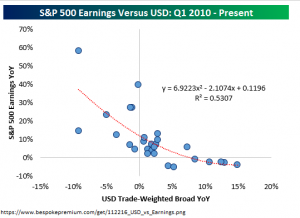

One factor working against the SP500 is the rise of the dollar. The USD is up over 6% this quarter, that makes exports more expensive by cutting into sales, and it also reduces foreign earnings that are translated back into dollars. As illustrated in the graph below, as the dollar rises, the impact on SP500 earnings is negative.

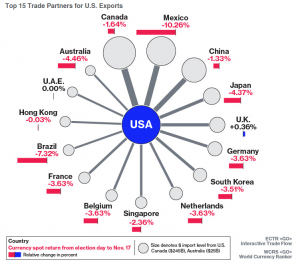

A rising dollar and a sinking Chinese yuan could spell trouble at some point. But the market has been ignoring that for now. And of course, the big wildcard remains what happens with trade. So far, Trump has been moderate when talking trade.

The market has strong momentum now but optimism is extremely high. That is often a contrary indicator.

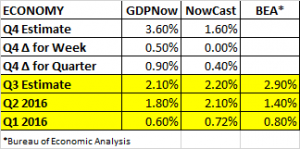

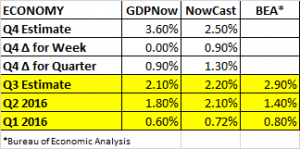

ECONOMY

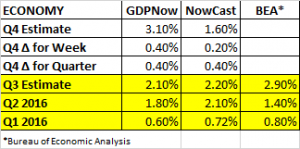

The Atlanta Fed’s GDPNow model is forecasting growth of 3.6% for Q4. That is unchanged from last week. The durable manufacturing report was positive but that was offset by a decline in the forecast for Q4 residential investment. The NY Fed’s estimate for Q4 growth is 2.5%.

SHARES BUYBACK

Goldman Sachs analysts are projecting that SP500 companies will buy back $780 billion in stock next year. The 30% increase over this year would be a result of cash coming back into the US via Trump’s repatriation plan. Trump plans to lower the tax to encourage companies to bring back cash now parked overseas.