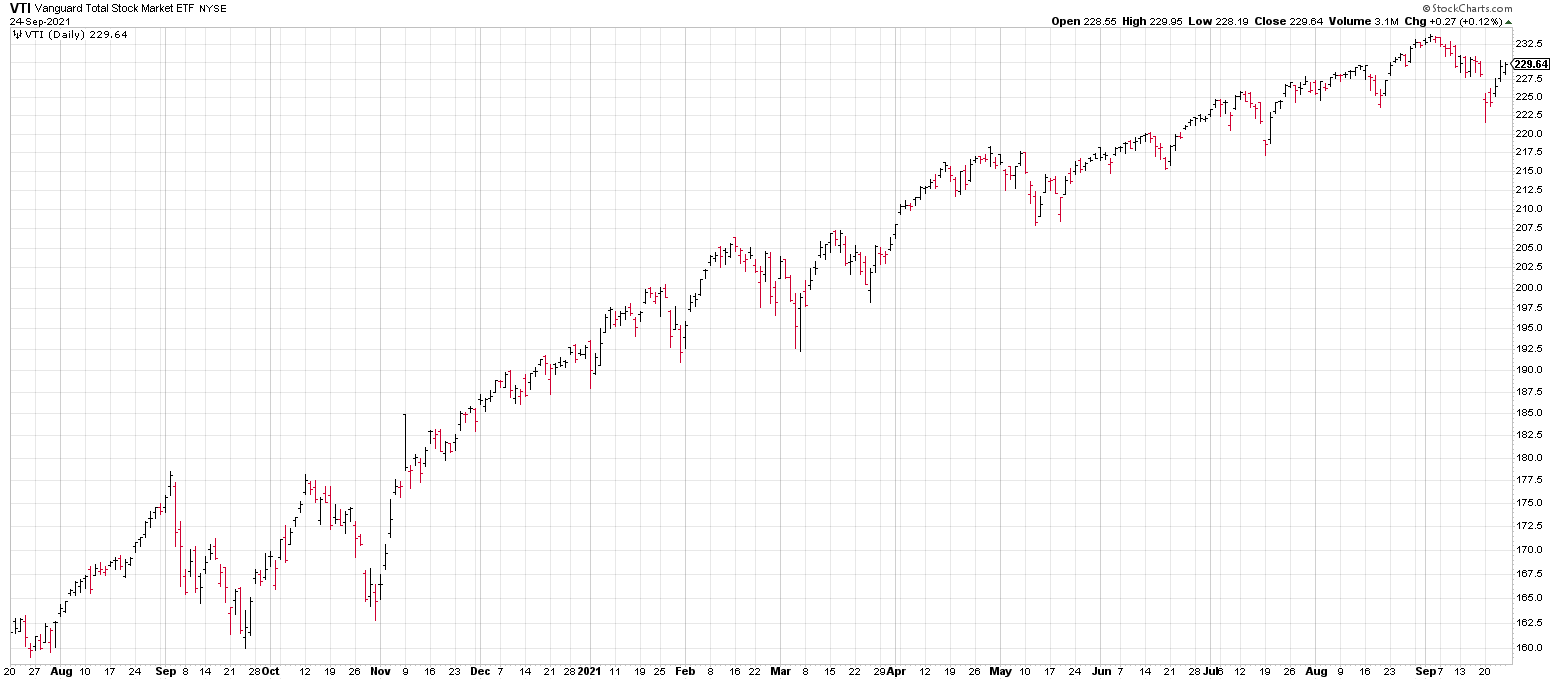

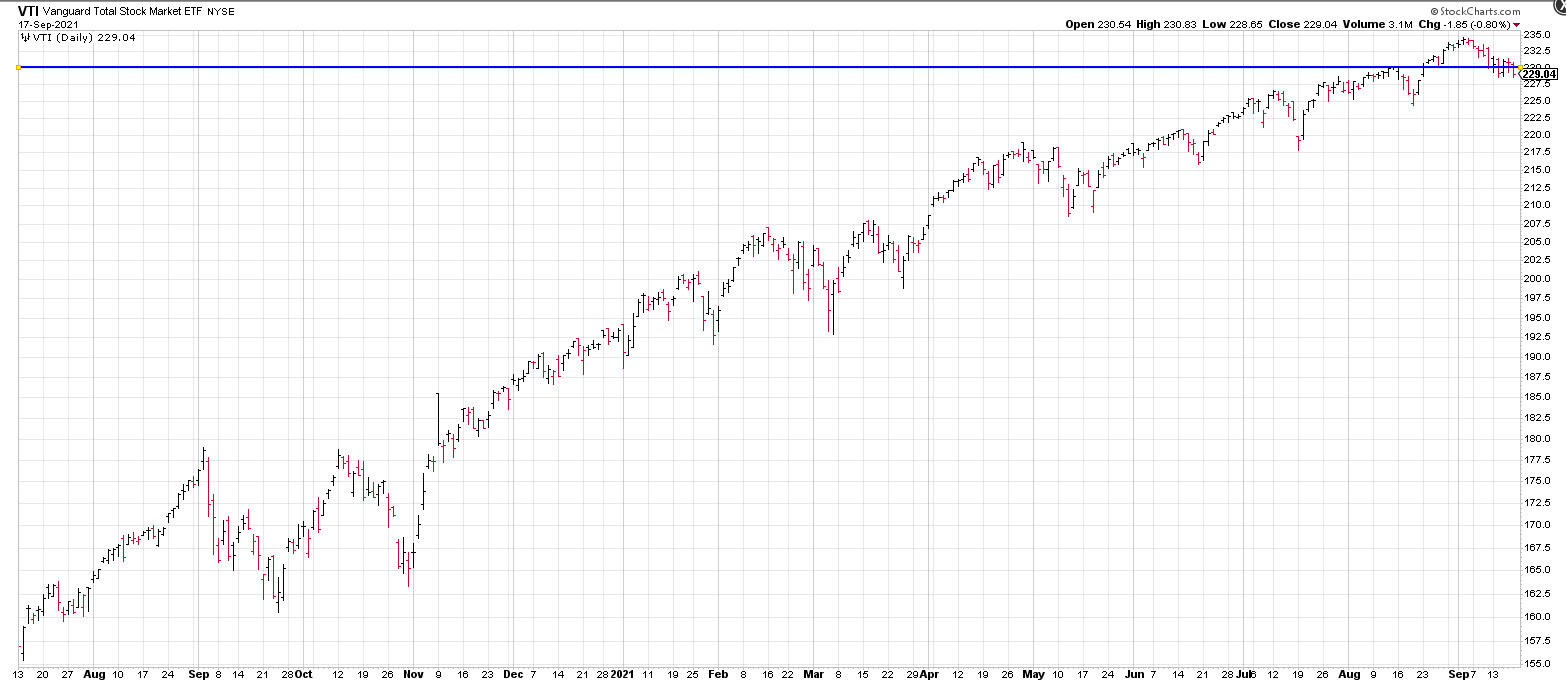

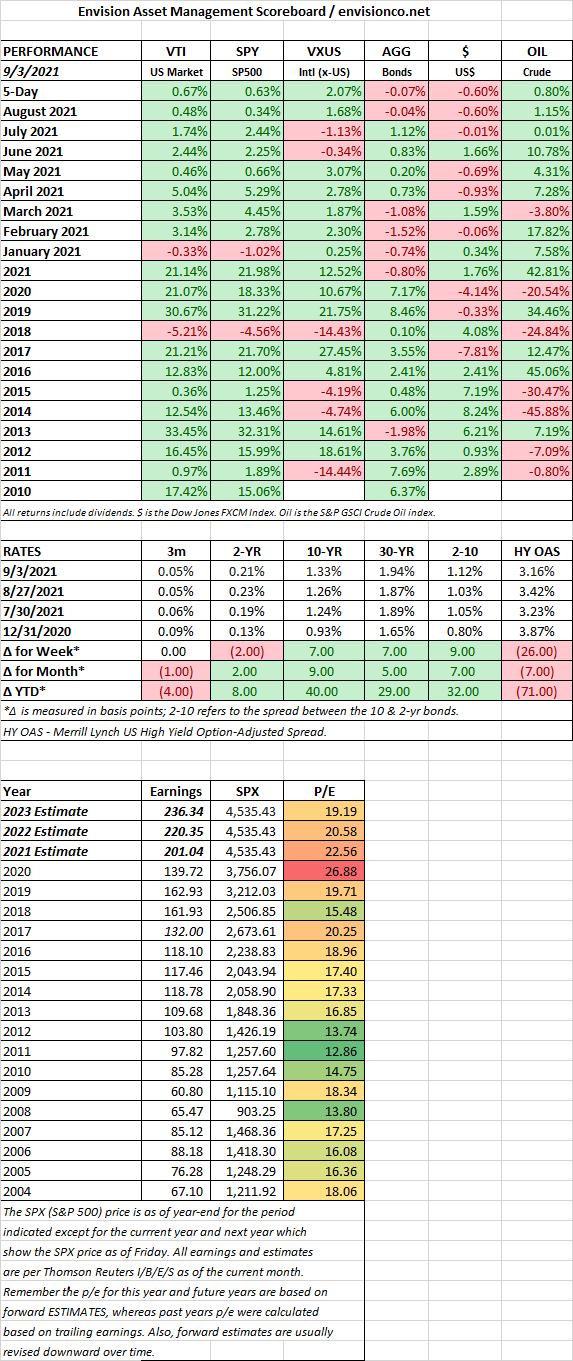

MARKET RECAP

Stocks were up in the US by 0.67% and by 2.07% outside the US.

August jobs were up by 235,000 but that was dramatically below the 750,000 estimate, but the stock market didn’t care. The market will turn every piece of news, good or bad, into a reason to for stocks to go higher. However, the the Initial Jobless Claims report was good. Ithit a new pandemic low coming in at 340,000 for the week ending August 28th.

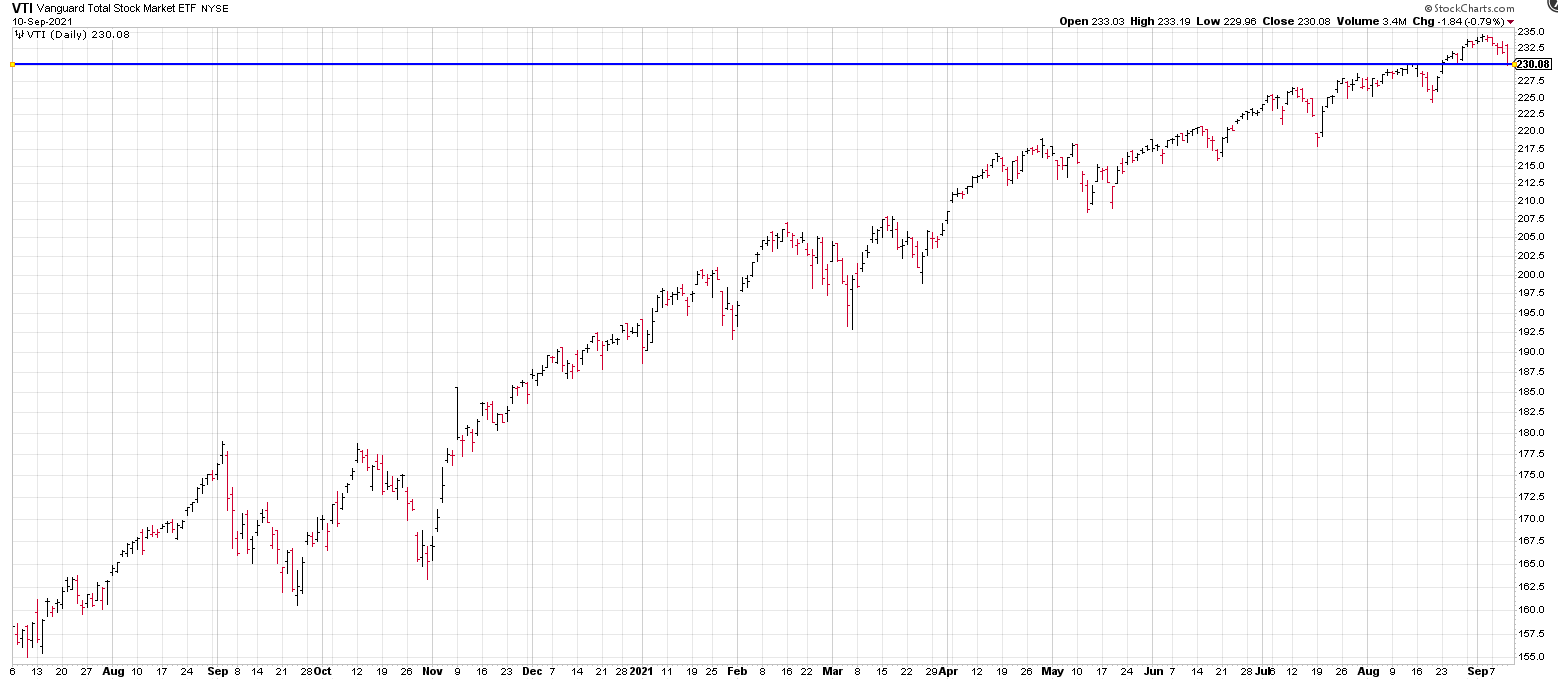

August closed out on Tuesday and stocks were up for the 7th straight month, the S&P was up by 2.4% while the Nasdaq increased by 4% for the month.

At least one area of irrational exuberance has cooled off. The SPAC market has lost $75 billion in market cap over the last six months. That is about 25% of the combined value of the 137 SPACs that merged by mid-February. During that same period, IPOs that came public were off about 12% while the Dow Jones Industrial Average was up 13%.

Home prices continued to hit records. The S&P CoreLogic Case-Shiller National Home Price Index rose 18.6% year over year in June, up from 16.8% the prior month, and the highest annual rate since the index began in 1987.

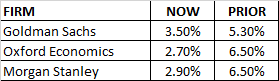

West Virginia Senator Joe Manchin wrote a good common-sense editorial on “Why I Won’t Support Another $3.5 trillion“. Manchin sites the risk of inflation, runaway debt, the future unknowns of the pandemic, the problems with artificial deadlines, and the impact on future generations.” Lets see if it makes any difference.

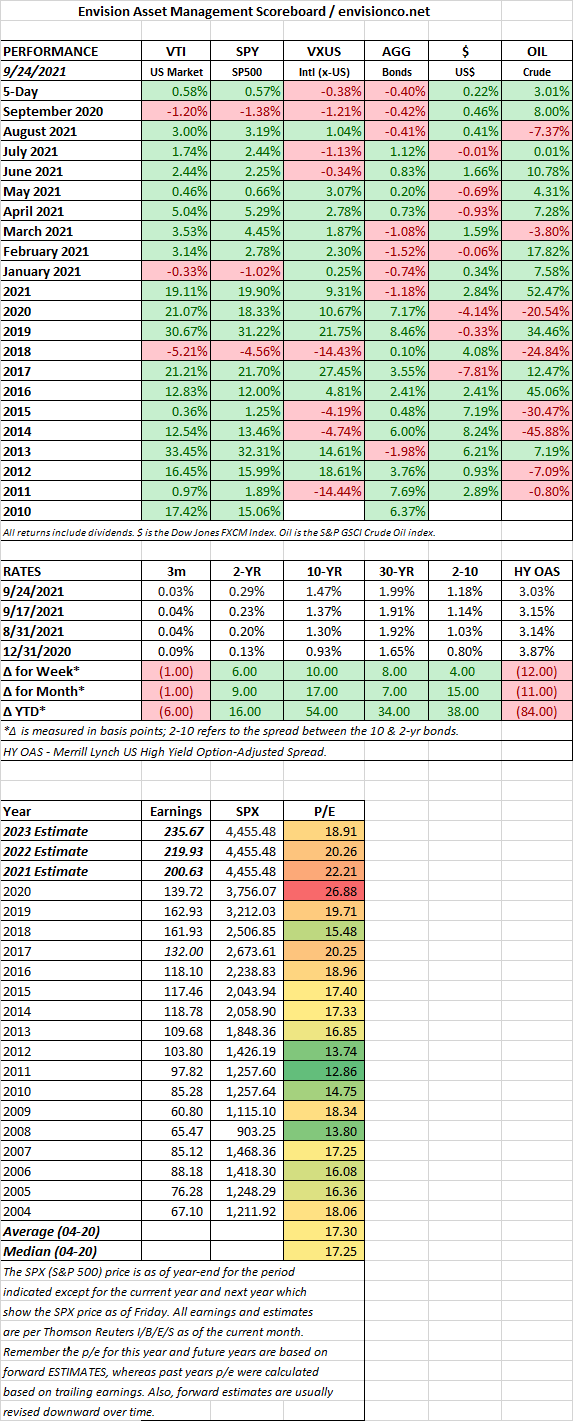

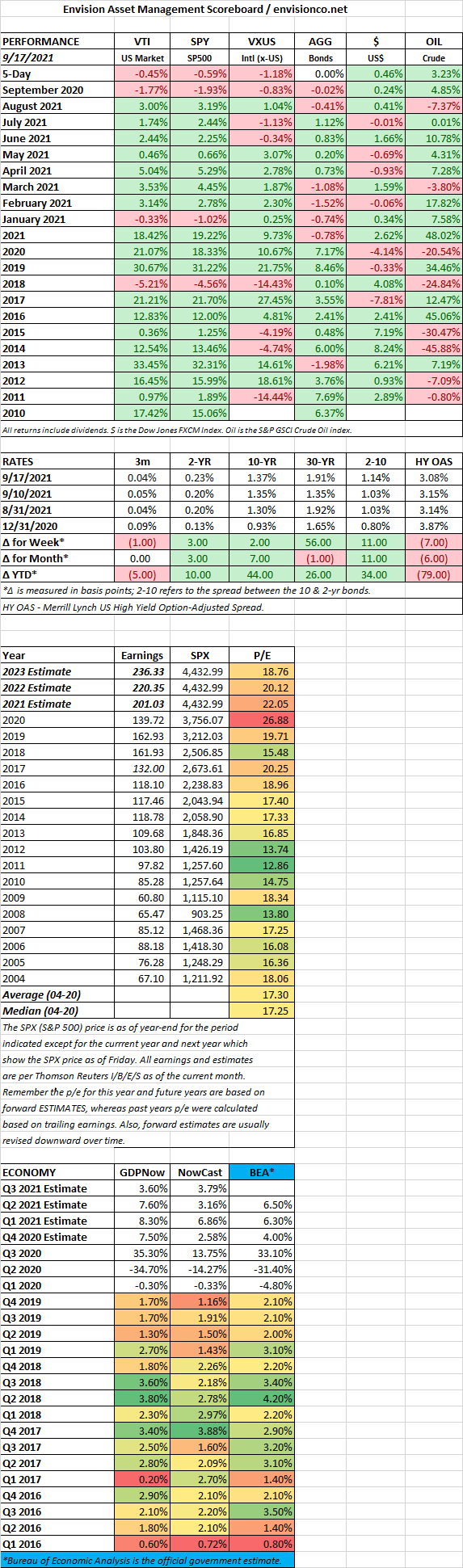

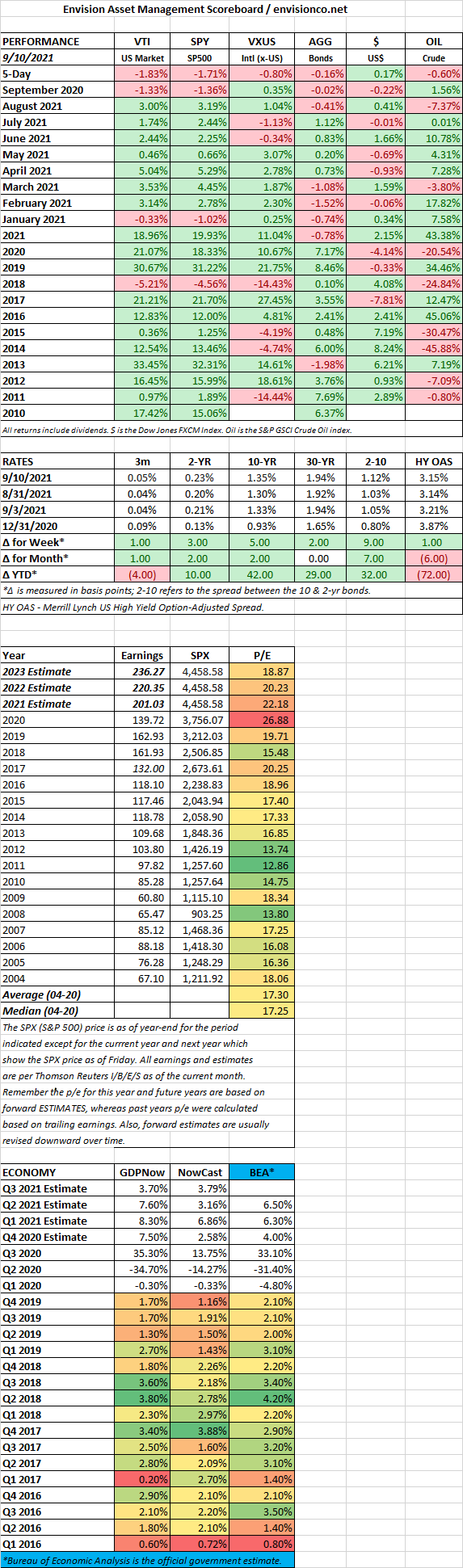

SCOREBOARD