Monthly Archives: October 2021

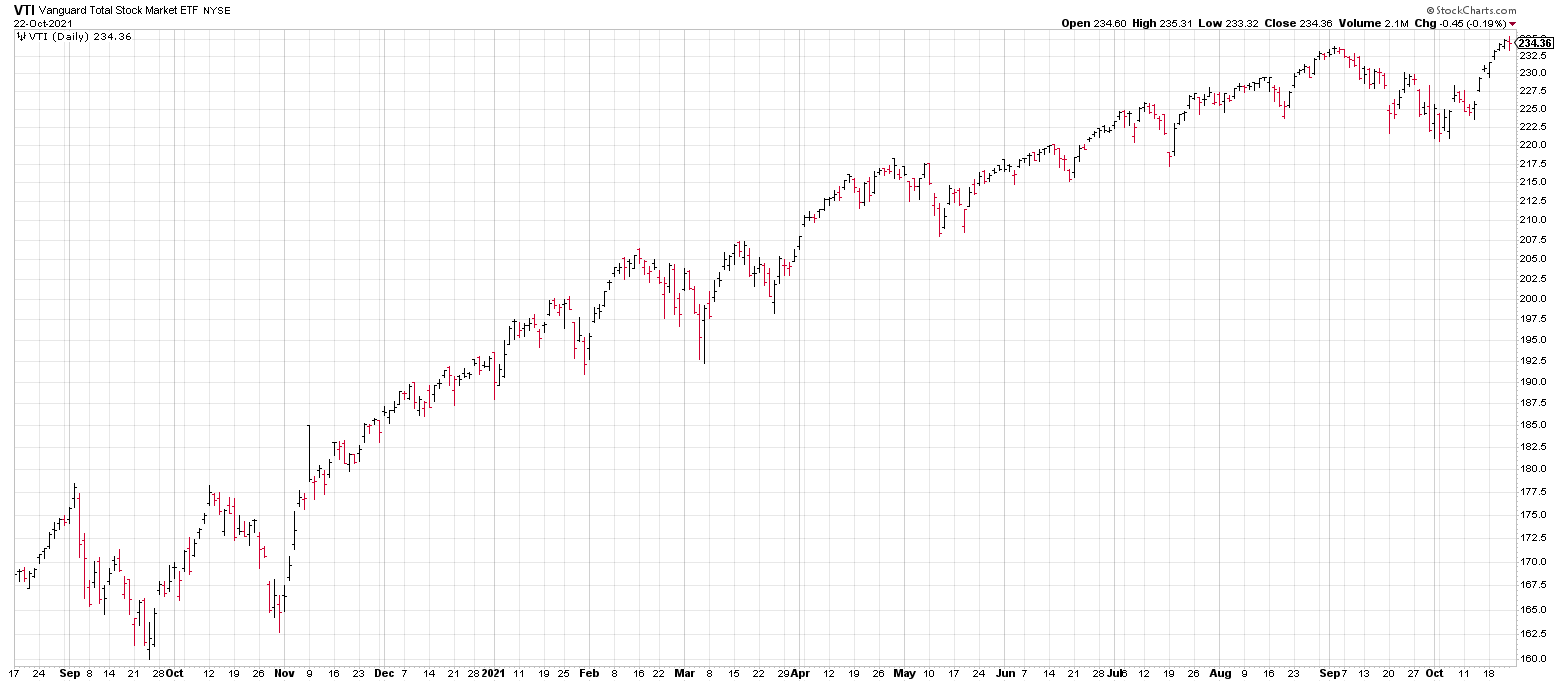

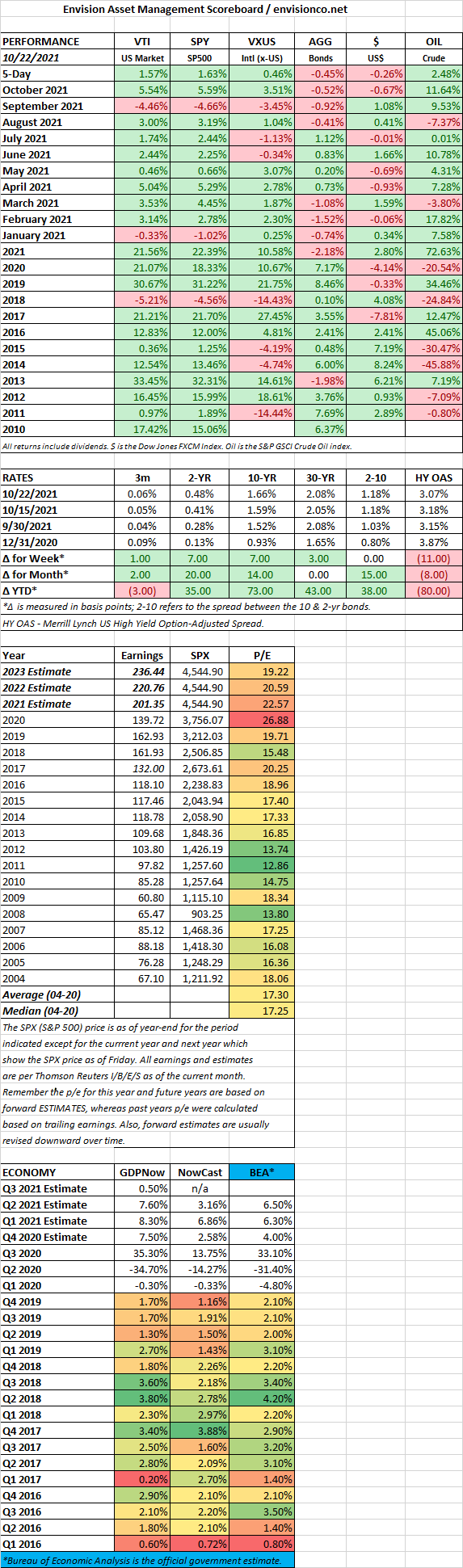

Week Ending 10/22/2021

MARKET RECAP

Stocks finished the week just off the Thursday record high, up by 1.57% for the week. From September 2nd to October 4th, the overall US market fell by 5.1%. Since then, stocks have rallied and are now about 0.3% above the September 2nd close.

Stocks have managed to rally despite rising interest rates. The 10-year Treasury has increased from 1.19% on August 3rd to 1.66% as of Friday. Projected inflation is measured at 2.66%, the highest rate in 15 years. Over the last few weeks there seems to have been a shift from the mantra that inflation is “transitory” to something that will be a bit longer, maybe a lot longer, than that. The Fed has indicated that tapering will start in November. Oil prices are at the highest level since 2014. Estimates for economic growth are falling. The Atlanta Fed’s GDP model now projects Q3 growth at only 0.5%. In China, the Evergrande Group, the real estate behemoth, is on the edge of bankruptcy, with a likely negative impact on the Chinese real estate sector, which represents 30% of China’s output. None of this seems to matter to the market, which is back at new highs.

Exxon is supposedly considering dropping several oil and gas projects, as directors are worried about carbon emissions. This at a time when energy prices are surging and capex across the industry is falling. Exxon’s board took a turn when a hedge fund with a 0.02% interest, Engine No. 1, managed to get their nominees added to the Company’s Board.

SCOREBOARD

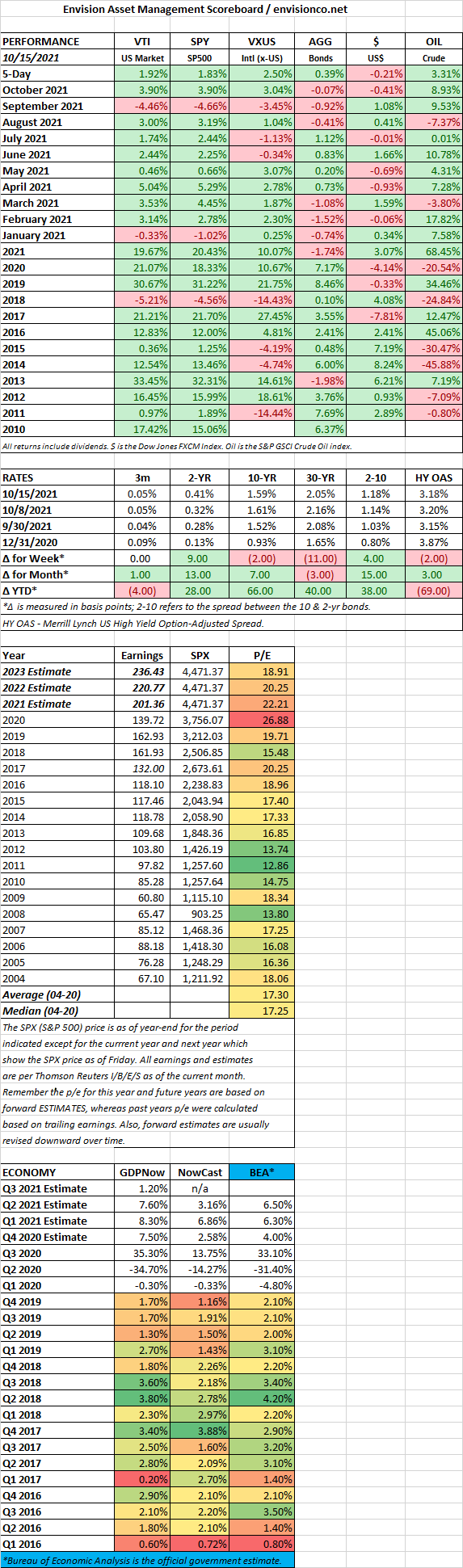

Week Ending 10/15/2021

MARKET RECAP

US stocks were up by 1.9%.

Surprise, inflation was up more than forecast in September, increasing by 0.4% from August and up by 5.4% year over year, the biggest increase since 2008. Supply chain issues, higher commodity prices and wages get the blame. The report confirms that the Fed will need to start tapering soon.

The combination of higher inflation and the hit the economy took from the Delta virus is weighing on economic growth. The Atlanta Fed now expects Q3 growth of only 1.2%, this is down from over 6% at the end of July. A JPM survey shows that 42% of respondents expect stagflation somewhere down the line. The good news is that Covid cases have been on the decline since August.

The copper/gold ratio hits its highest level since 2013 indicating strength in industrial demand.

SCOREBOARD

Week Ending 10/1/2021

Durable goods hit a record in August, up 1.8% from July to $263.5 billion. Durable goods are product meant to last three years or more. The estimate was for a 0.6% increase. The big increase indicates that businesses are investing for the future.

Home prices continued to increase at record rates in July. It was the fourth straight month of record increases. The S& P CoreLogic Case-Shiller National Home Price Index was up 19.7% in the year that ended in July, up from an 18.7% annual rate in June. July marked the highest annual growth rate since the index began in 1987.

But the pace of increases might be slowing. The Conference Board’s consumer-confidence index fell to 109.3 in September from 115.2 in August and the share of respondents planning to buy a house in the next six months fell for the third month in a row.