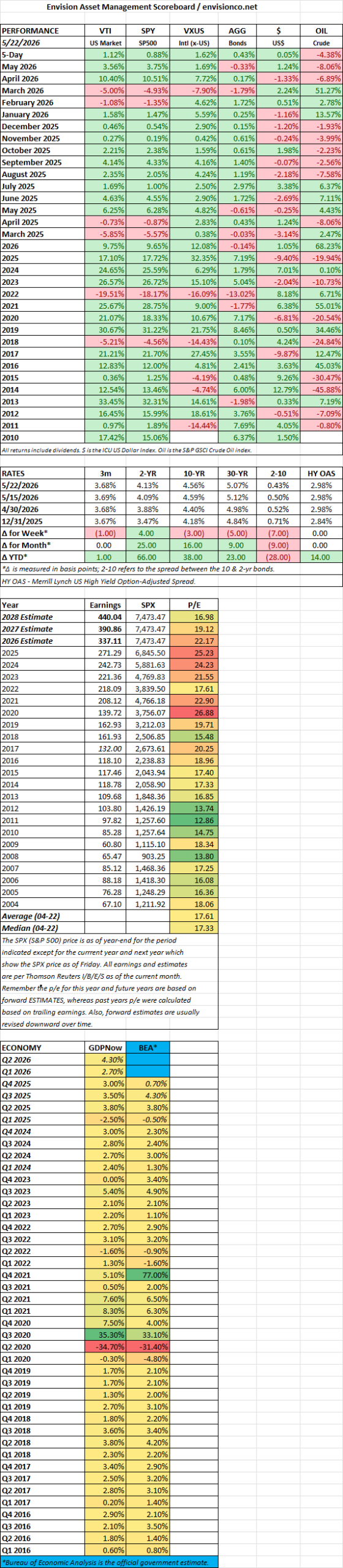

MARKET RECAP

Hawkish Shift in Fed Sentiment: The Federal Reserve’s April meeting minutes signaled a growing willingness to increase interest rates if core inflation remains stubborn. Policymakers noted that returning to their 2% target could take significantly longer than expected, elevating real yields to one-year highs and further flattening the Treasury curve.

Economic Divergence: Economic data painted a mixed picture. While overall employment trends remained strong and private sector job growth accelerated, surging input prices and geopolitical headwinds caused localized layoffs and production bottlenecks across several manufacturing lines.

-

High-Profile Tech Supply: Equity markets are shifting focus to an upcoming wave of mega-cap tech listings, highlighted by SpaceX filing its S-1 registration statement for a highly anticipated public offering.

-

Valuation Disconnect: Internal segment details for SpaceX reveal a sharp contrast: its core rocket launch and satellite internet branches are seeing rapid user growth and stable financials, whereas its heavily capitalized artificial intelligence and social operations consumed billions in capital expenditures against stagnant revenues.

-

Index Rebalancing Fears: Though investors expressed anxiety that massive new listings (such as SpaceX and OpenAI) might trigger heavy passive selling across older market components, strict float-adjusted weighting rules by key index providers will severely limit their initial footprint, capping broader index displacement.

- Surging Soft Commodities: Agricultural markets broke free from a multi-year downtrend. Wheat and soybeans staged double-digit rallies due to geopolitical adjustments, while constraints in raw materials pushed global fertilizer prices higher.

-

Persistent Meat Inflation: Wholesale beef prices remained near historic, inflation-adjusted highs. Due to the aggregate U.S. cattle herd contracting to record lows, meat production constraints continue to pressure corporate downstream processors’ operating margins.