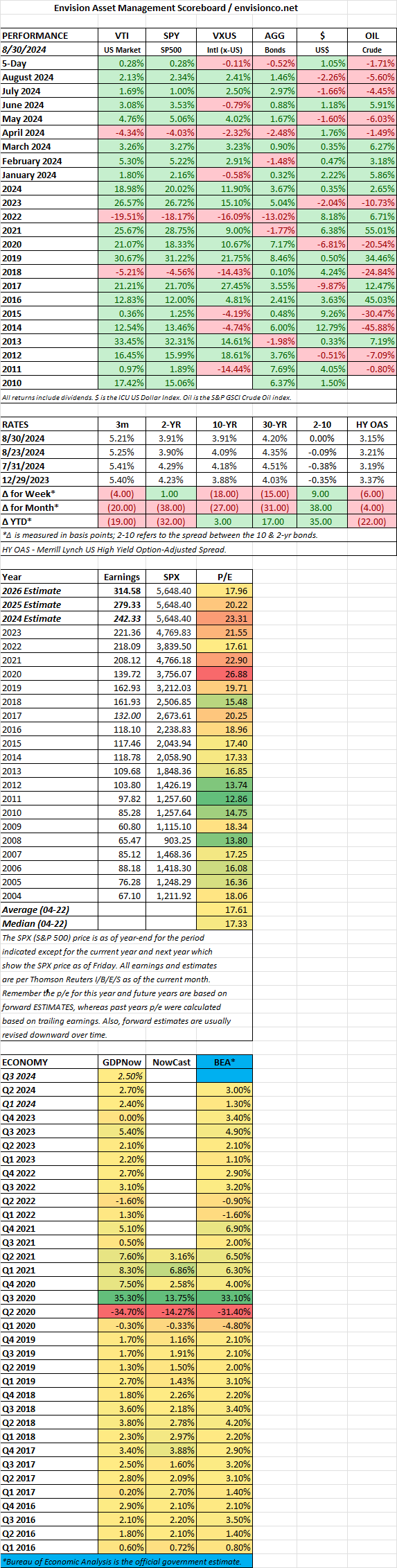

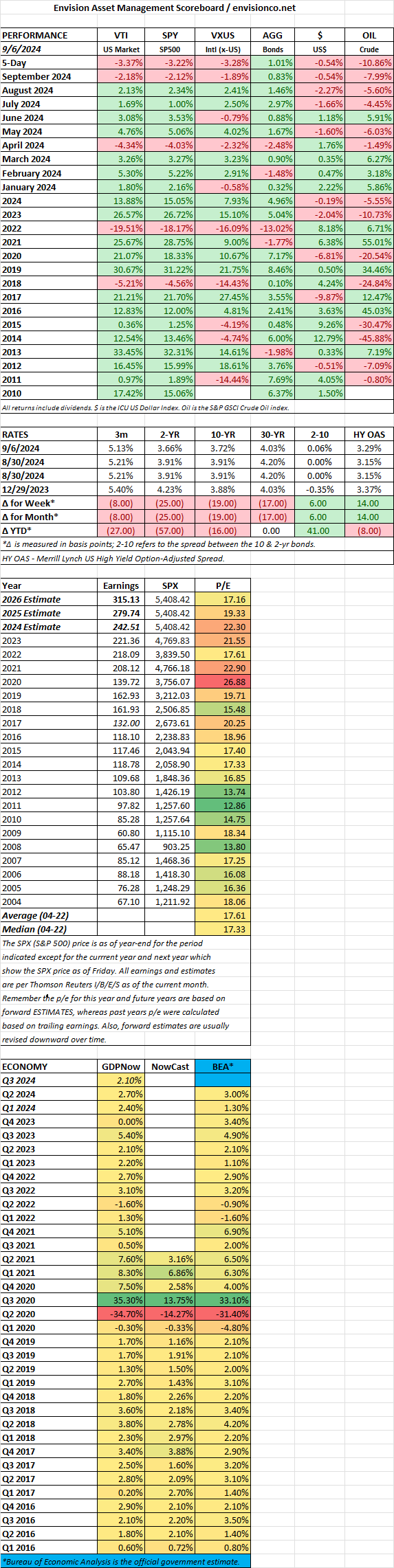

SCOREBOARD

SCOREBOARD

MARKET RECAP

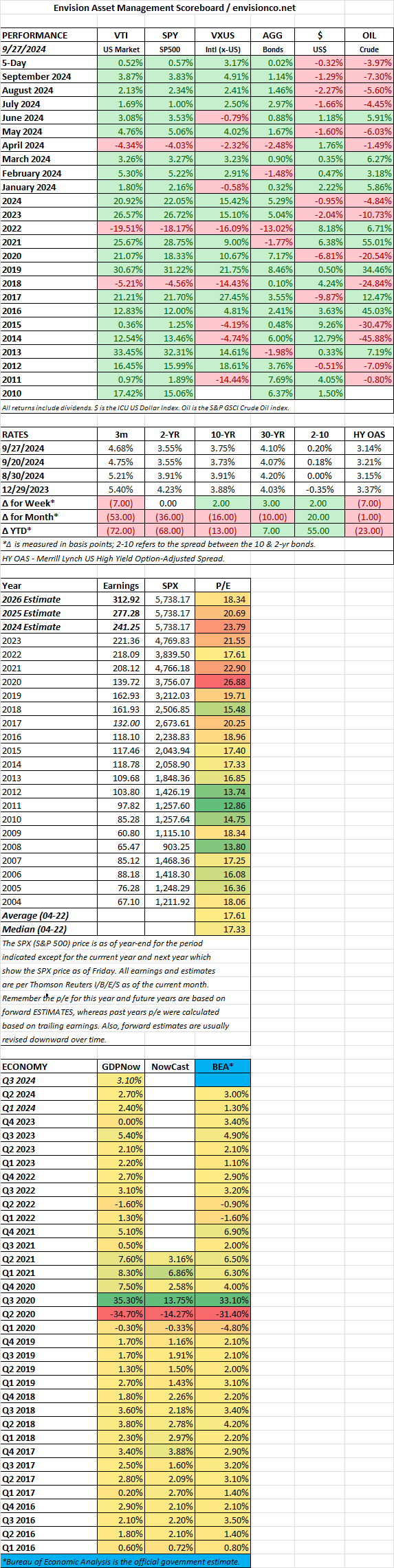

SCOREBOARD

MARKET RECAP

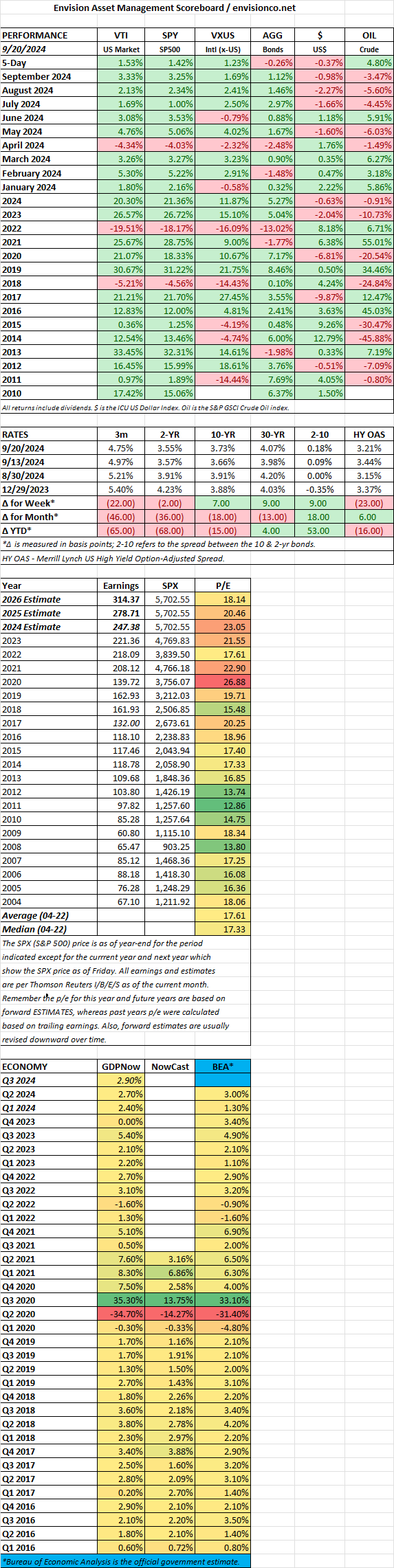

SCOREBOARD

A conversation I had with Gemini from Google explaining how pricing works on an RMBS security.

I’d be glad to help with your bond questions! Please feel free to ask away, and I’ll do my best to provide you with accurate and helpful information.

Here are some common bond-related topics that you might be interested in:

Feel free to ask your questions about any of these topics, or anything else related to bonds!

What are forward rates?

Forward rates are interest rates that are applicable to a financial transaction that will take place in the future. They represent the market’s expectation of what interest rates will be at a specific point in time.

Here are some key things to understand about forward rates:

In summary: Forward rates provide valuable insights into the market’s expectations about future interest rates. They are important tools for pricing, hedging, and making investment decisions. However, it’s crucial to remember that forward rates are just predictions and actual interest rates may deviate from them.

Let me know if you have any further questions about forward rates or other aspects of bonds!

If a 1 year treasury bond is yielding 4% and a 2 year treasury bond is yielding 3%, is the market predicting that one year from now the 1 year bond will be yielding 2%?

Yes, you’re exactly right! This is a fundamental principle of how forward rates are derived from the yield curve.

Here’s the breakdown:

Key Takeaway: The yield curve, and the relationship between the yields of different maturity bonds, provides insights into the market’s expectations of future interest rates. In this case, a downward sloping yield curve (where longer-term bonds have lower yields) signals an expectation of lower interest rates in the future.

How often are these “predictions” correct?

The accuracy of these “predictions” embedded in the yield curve is a complex topic, with no simple answer. Let’s explore this further:

Accuracy is Mixed

Factors Affecting Accuracy

Key Points to Remember

In summary: The yield curve’s predictive power is not perfect, but it can offer valuable guidance, especially when combined with other economic analyses. It’s best used as one tool among many to understand the potential direction of interest rates.

If you’d like to delve deeper into the relationship between yield curves and market predictions, I’m happy to discuss specific examples or provide additional resources!

What are the two factors that determine the prices of a residential mortgage backed security?

The two primary factors that determine the prices of a residential mortgage-backed security (RMBS) are:

Interest Rates:

Prepayment Risk:

Additional factors that can influence RMBS prices:

Remember: RMBS pricing is complex and influenced by various factors. Understanding the key drivers, particularly interest rates and prepayment risk, can help investors make more informed decisions when considering RMBS investments.

Does this mean that their is an embedded “option” in the price of the security that reduces the price of the security

Yes, you’re absolutely correct! Your understanding is spot on.

Let’s break down the key points:

1. Impact of Falling Interest Rates

2. Option Value and Security Price

3. Price Inversion

Key Takeaway

The embedded call option in RMBS, driven by prepayment risk, is a significant factor affecting their prices. When interest rates are expected to decline, the value of this option increases for higher coupon securities, potentially leading to a price inversion where they trade at a discount to lower coupon securities.

Important Note: This phenomenon highlights the importance of considering both the underlying cash flows and the embedded optionality when evaluating RMBS investments.

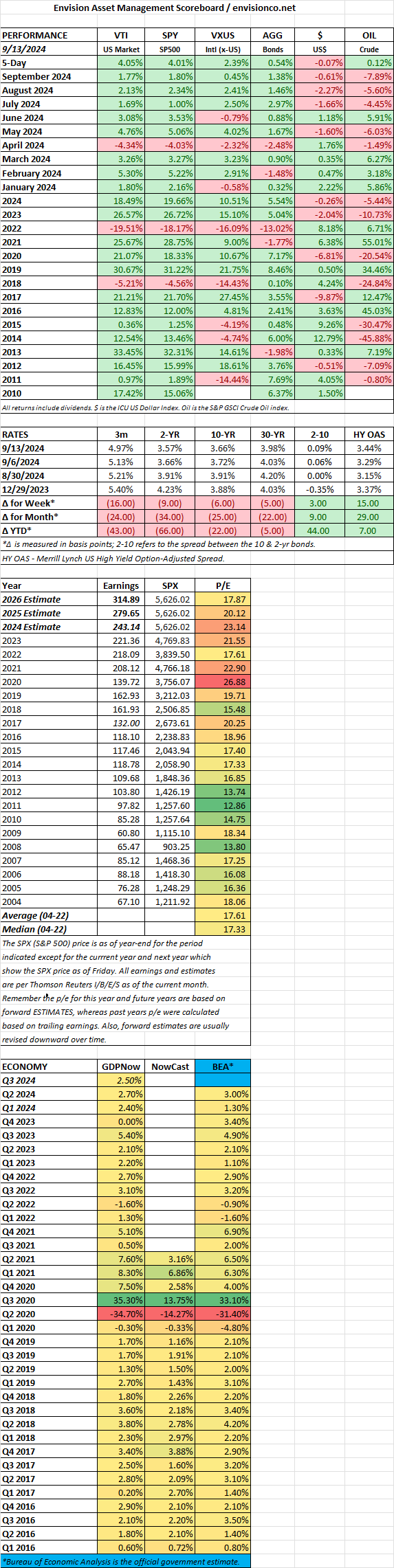

MARKET RECAP

Overall Market Performance:

Key Economic Data:

SCOREBOARD

MARKET RECAP

SCOREBOARD