A good column by Nick Kristoff which gives us reasons to be optimistic.

MARKET RECAP

Stocks advanced again, by 0.48% in the US and 1.10% outside the US. International stocks have outpaced their US counterparts so far in December, up 4.8% versus 3.1% in the US.

According to a report by Mastercard Spending Pulse, holiday shopping from November 1st to December 24th was up by a strong 3.4%. And Customer Growth Partners, a retail firm that provides research on retailers, calculates that the Saturday before Christmas was the biggest single shopping day in US retail sales, totaling $34.4 billion.

There was also good news for workers. Wages are rising a the fastest pace in more than a decade. Pay for the bottom 25% of wage earners was up by 4.5% in November according to the Federal Reserve of Atlanta.

The risk is that higher wages are sometimes a leading indicator of future inflation.

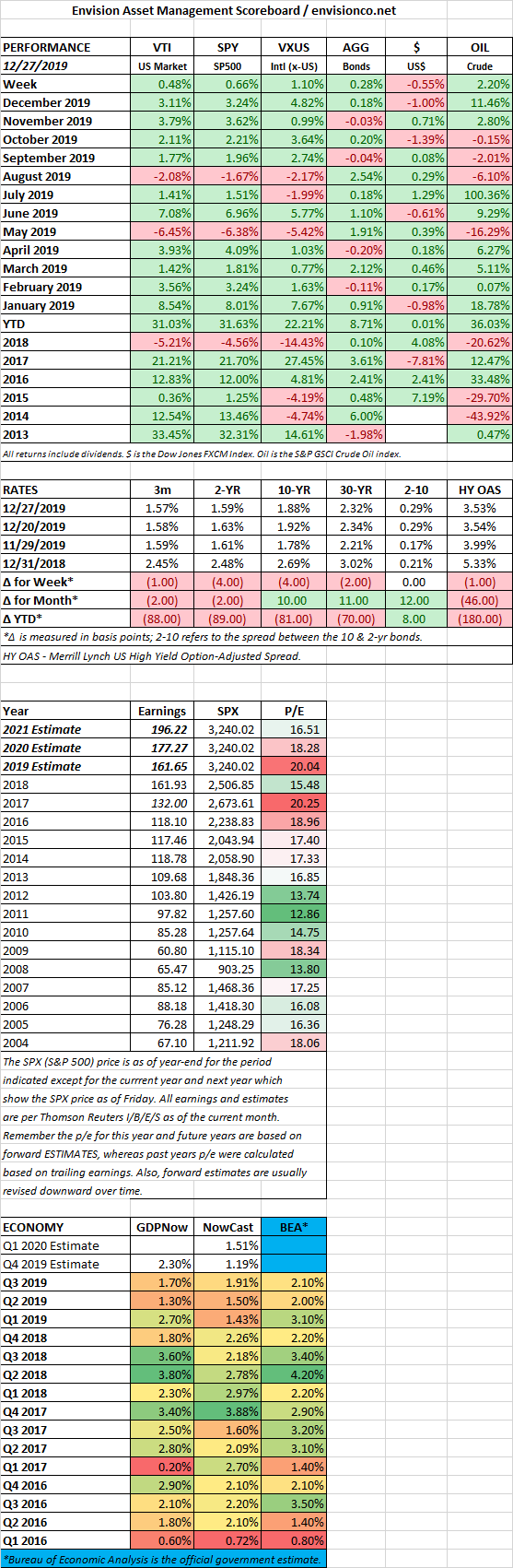

SCOREBOARD

HIGHLIGHTS

MARKET RECAP

Stocks continued their relentless advance, hitting record highs every single day of the week. In the US, equities were up by 1.77% and outside the US, +0.88%. Since October 28th, when the US stock market broke through resistance, stocks are up by 7.7%.

However, one year ago at this time, it was just the opposite. US stocks hit their low on 12/24/2018, having fallen by 16.3% since 12/3/18. Market sentiment was about as negative as possible. CNN’s Fear and Greed Index showed extreme fear at the time, measuring a 5 out of a possible 100. That is in contrast with the reading on Friday of 91, indicating extreme greed.

BEARISH BETS

One place that isn’t showing extreme optimism is the Skew Index. Bearish bets on the fall of the S&P 500 have been increasing in recent months. The CBOE Skew Index, which measures trader expectations of extreme moves in the stock market, reached its highest level since September. Likewise, the cost of options betting on a falling market versus those betting a higher market has been near the highest levels of the year.

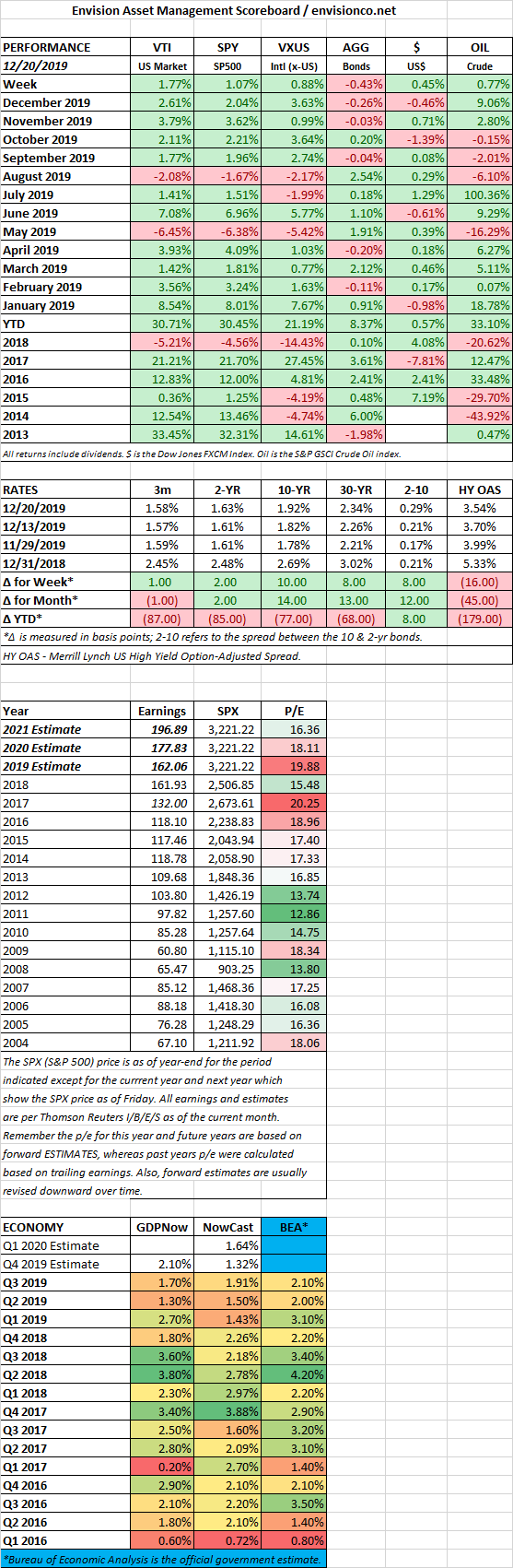

SCOREBOARD

HIGHLIGHTS

MARKET RECAP

Stocks were up again on several positive developments. The US advanced by 0.65% and international stocks jumped by 1.74%. The US and China reached a “phase one” trade deal, the Democrats have agreed to support the North American trade pact (with some minor changes), Boris Johnson’s Conservative Party had a runaway victory in the UK, and both the Federal Reserve and the European Central Bank announced that low-interest rates would continue. Now it is true that the market had anticipated most of this, but at least they are in the bag now. We will see if the market “sells on the news.”

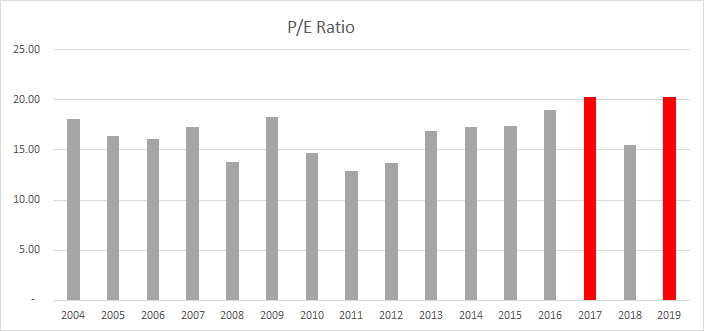

Stock prices have gone up, but earnings estimates haven’t. The estimate for earnings on the S&P 500 is now $162.06, down 6.8% from the projection at the end of 2018. The S&P is now selling at a price/earnings ratio of 19.55, just shy of the highest year-end ratio of 20.25 level (since 2004) reached at the end of 2017, indicating that stocks are getting expensive based on this metric.

PHASE ONE TRADE DEAL

The US and China agreed to a limited trade deal. Existing tariff rates on Chinese goods will be reduced by about half, the new levies that were set to start on Sunday will be canceled, and China will buy $200 billion over two years of agricultural goods, along with energy and other products, in 2020. If China fails to follow through, the tariffs will be reinstated.

Key US issues such as subsidies to Chinese businesses and technology transfer do not appear to be part of this deal.

RETAIL SALES MISS ESTIMATES

Retail sales fell short of estimates in November. Sales were up 0.2% compared to an expected 0.5%. Take out autos and gas and sales were flat. The disappointing report follows an October when sales exceeded expectations.

PAUL VOLKER’S FINAL NOTE TO AMERICANS

Paul Volker, the legendary former Federal Reserve Chair who broke the back of inflation in the 1980s, passed this week. In an essay published in the Financial Times posthumously, Volker said, “When I was writing my book, I observed that President Donald Trump had not attacked the independent U.S. Federal Reserve, for which I was grateful. To say that is no longer true would be an understatement. Not since just after the second world war have we seen a president so openly seek to dictate policy to the Fed. That is a matter of great concern, given that the central bank is one of our key governmental institutions, carefully designed to be free of purely partisan attacks. I trust that the members of the Federal Reserve Board itself, the members of Congress responsible for Fed oversight, and indeed the public at large, will maintain the Fed’s ability to act in the nation’s interest, free of partisan political purposes.”

POLITICIANS GONE WILD

The election of Boris Johnson as UK Prime Minister will bring along a surge in government spending. Johnson has promised voters $128 billion in infrastructure spending and billions more on healthcare.

The UK will be the latest government to go on a wild spending spree. The US is a leader of the pack, as the US budget deficit topped $1 trillion in the fiscal year ended 9/30/2019. Japan just approved a $120 billion stimulus plan.

Adam Posen, from the Peterson Institute for International Economics, thinks the public spending is needed. Low-interest rates and investing in infrastructure that needs improvements could bring a positive payoff. But Ken Rogoff, an economics professor at Harvard, says that governments need to be aware that low-interest rates may not last forever, “The notion that it’s just free, that we can just spend more money and no one’s going to pay for it, is very naive,” he said. We agree.

SCOREBOARD

HIGHLIGHTS

MARKET RECAP

It was a tale of two halves (to use a sports cliche), at the low midday Tuesday US stocks were down by 2.71% from the prior week close, but then rallied into the close and then again on Wednesday. Prices were steady on Thursday and then finished up by .89% on Friday on the blockbuster jobs report to scratch out a 0.17% gain for the week. International stocks fared better, +0.96% for the week, and bonds were off slightly, down by 0.08%.

JOBS

There were 266,000 jobs added in November, the biggest increase since January, and 100,000 more than what economists had forecast. The unemployment rate dropped to 3.5%, the lowest level since 1969. Initial unemployment claims also are historically low at 203,000 for last week. And to top it all off, wages increased by 3.1%. Jobs were added in health care, transportation, and leisure and hospitality.

The strong payroll numbers affirm the Fed’s recent decision to hold rates steady, instead of cutting further. If anything, a strong report like this would normally give the Fed a lean towards raising rates. But Fed Chair Powell has indicated that the Fed would need to see inflation at or above the 2% target for an extended period of time before the next increase.

GOLD/COPPER

The recent rise of copper versus the fall of gold has been reflective of market sentiment. As fears of a recession began to fade, and the forecast for a stronger economy began to pick up, copper, an industrial metal has rallied. Meanwhile, gold, which is considered a market hedge, has been falling.

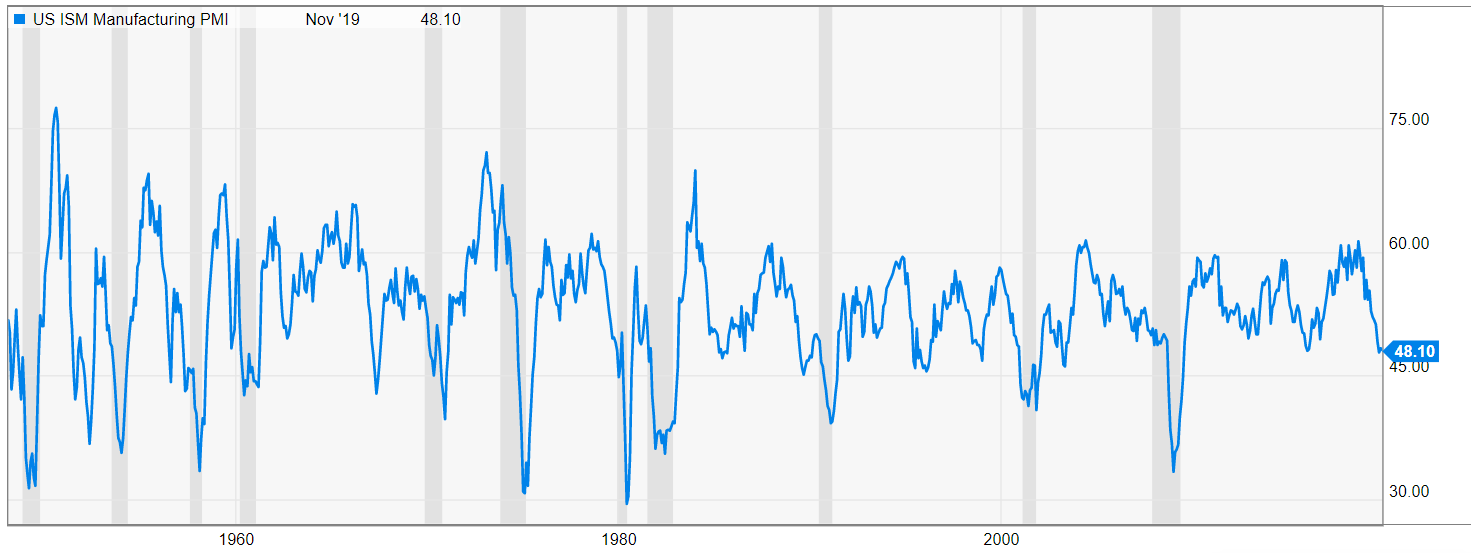

MANUFACTURING

Despite the upbeat news outlined above, manufacturing is still at a weak point. The Institute of Supply Management’s (ISM) Purchasing Manager’s Index was measured at 48.1% in November, down from 48.3% in October, and a decent amount less than the 50% breakeven level that represents the difference between expansion (greater than 50%) and a contraction (less than 50%).

Timothy Fior, Chair of the ISM, said “Comments from the panel were consistent with the previous month, with sentiment improving compared to October. November was the fourth consecutive month of PMI® contraction, at a faster rate compared to the prior month. Demand contracted, with the New Orders Index contracting faster, the Customers’ Inventories Index remaining at ‘too low’ levels and the Backlog of Orders Index contracting for the seventh straight month (and at a faster rate). The New Export Orders Index returned to contraction territory…consumption (measured by the Production and Employment indexes) contracted…Inputs — expressed as supplier deliveries, inventories, and imports — were again lower in November, due primarily to a contraction in inventories that was partially offset by supplier deliveries returning to ‘slowing.’… Overall, inputs indicate (1) supply chains are meeting demand and (2) companies are less confident that materials received will be consumed in a reasonable time period. Prices decreased for the sixth consecutive month, at a slower rate.”

SCOREBOARD