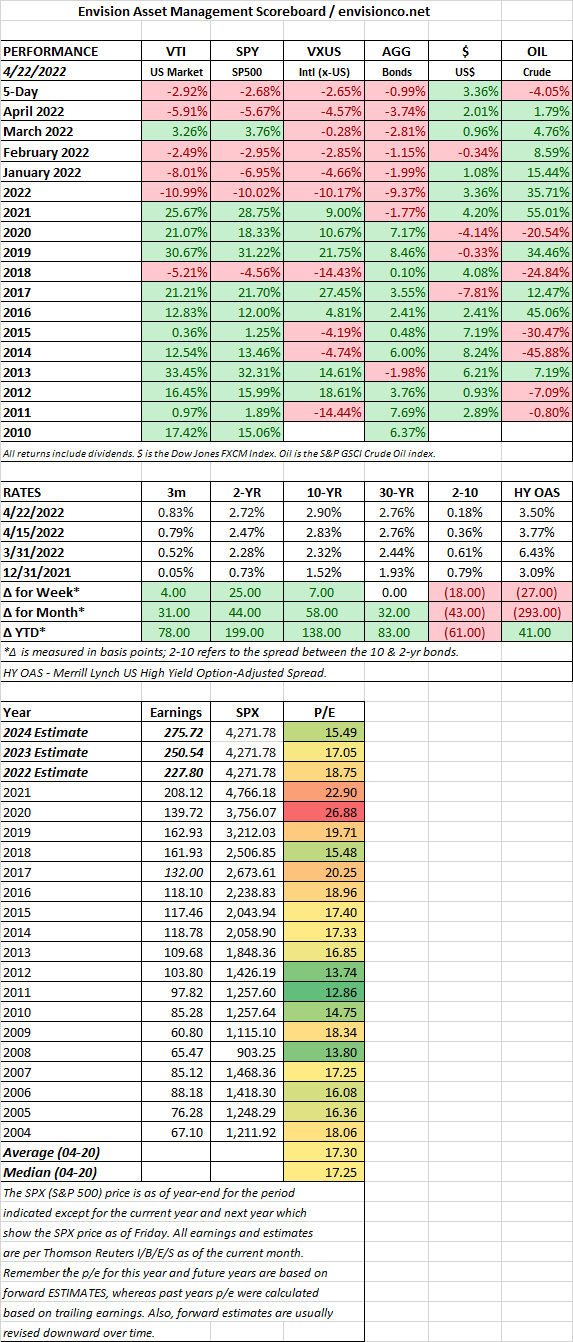

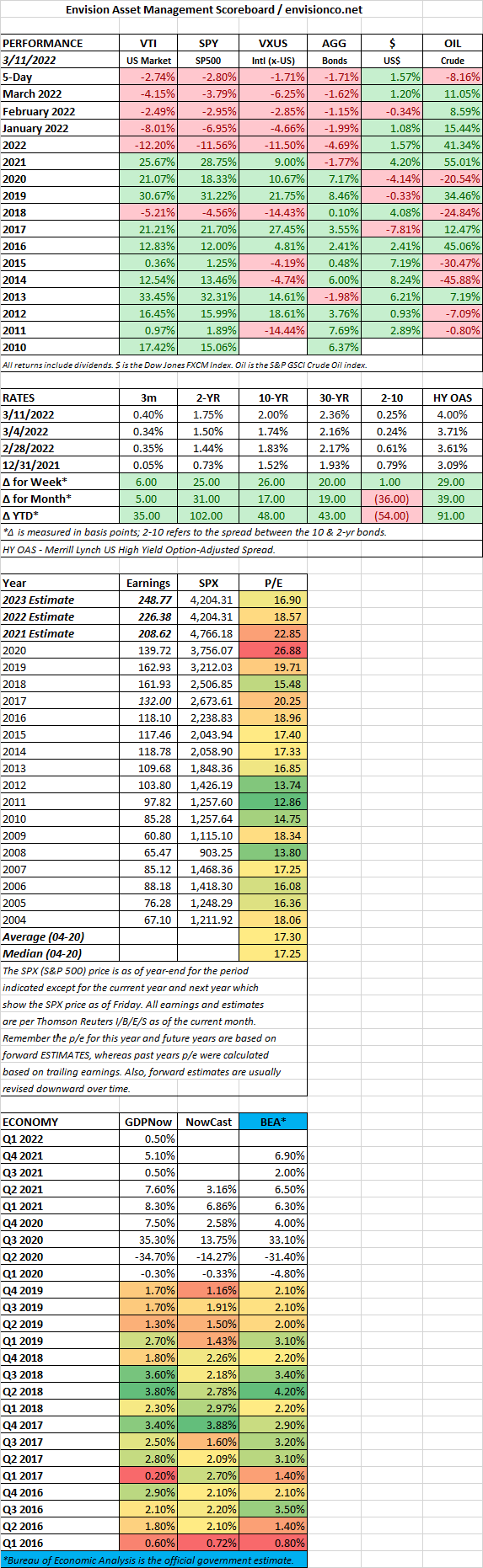

US stocks fell by 2.76% for the week. Stocks were actually up after the Wednesday close by about 1.5%, but that is when Fed Chair Powell pretty much much promised a half-point increase at the next meeting on May 3-4. And then St. Louis Fed President James Bullard started talk of a 3/4 point rate increase, although said he prefers a series of half-point increases. Maybe the back to back comments were enough to jar investors into believing what the Fed has more or less been saying for weeks, that much higher rates are on the way. The market would then fall by almost 4% on Thursday and Friday.

The Fed-funds futures market is looking for 1/2 point next month, and 3/4 of a point for the June meeting, and then 1/2 point in late July. That increased the 2-year note by 27 basis points to 2.71%.

PMI reports are indicating a slight slow down in economies around the world The composite PMI for the US came in at 55.1, down from 57.7 in March. It was the lowest reading in three months. Services took the brunt of the hit, down to 54.7 from 58 while manufacturing was strong, rising to 59.7 from 58.8, the highest reading in seven month.

Overseas, Europe’s biggest economy, Germany, reported a drop in the composite PMI to 54.5 in April from 55.1 in March.

The job market is still strong, weekly jobless claims was less than 200,000 for the ninth consecutive week. The job market hasn’t been this strong since 1969. Housing starts are also strong, permits for new homes is 6.7% higher from one-year ago.

US stocks fell by 2.1% as worries about the war in Ukraine, inflation, Fed tightening, higher interest rates, and lower profit margins dragged on the market. International markets were off by 1.18% and bonds dropped by 1.23%.

The Producer Price Index (PPI) was up by a record 11.2% in March, year over year. Vegetables were up by 82%, grain by 40%, meat and fish by 23%.

The Consumer Price Index (CPI) was up by 8.5% in March compared to the previous year, the biggest increase since 1981. Higher gas prices fueled by Russia’s invasion of Ukraine caused most of the damage.

The debate is on as to if the economy is booming or busting, or maybe both at the same time.

Airlines have been booked solid this holiday weekend without pushback on higher fares, according to the President of Delta.

Consumer sales are up, but not in real (inflation-adjusted) terms.

Lower-income households are using their credit cards more, indicating they may be struggling with higher prices. Households with incomes under $50,000 spent more on their credit cards on utilities, gasoline, and food.

Trucking activity indicates a slow-down in activity.

Hourly earnings are showing the strongest gains among lower income groups.

Stephanie Pomboy of Market Mavens says that a $41.8 billion surge in consumer credit in February signals that consumers are “now are resorting to desperate measures.”

Markets fell this week on worried about an economic slowdown and a more aggressive tightening by the Fed.

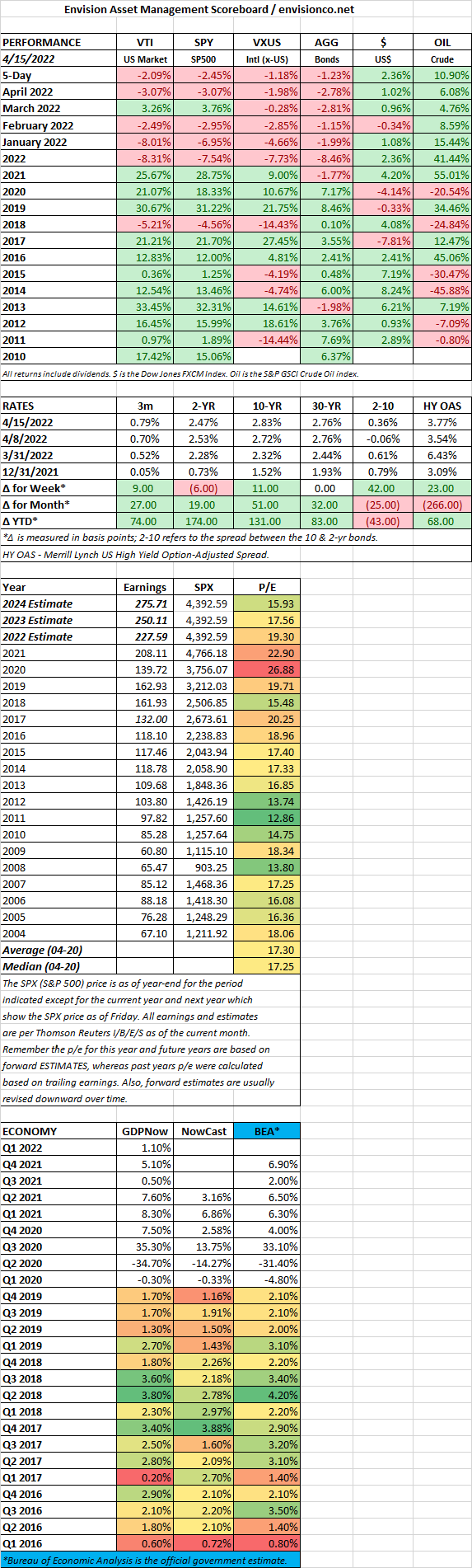

Just about everyone at the Fed is talking about tightening quickly. Lael Brainard, the Fed governor awaiting Senate confirmation said the central bank needs to shrink its balance sheet “rapidly.” In a release of the Fed’s minutes from last minutes, officials spoke about reducing the balance sheet by $95 billion per month. That led to a rise in the yield of the 10-year to 2.72%, up 32 basis points for the week, while the 2-year was just up a few basis points to 2.53%, thereby opening up a positive spread between the 10-year and the 2-year.

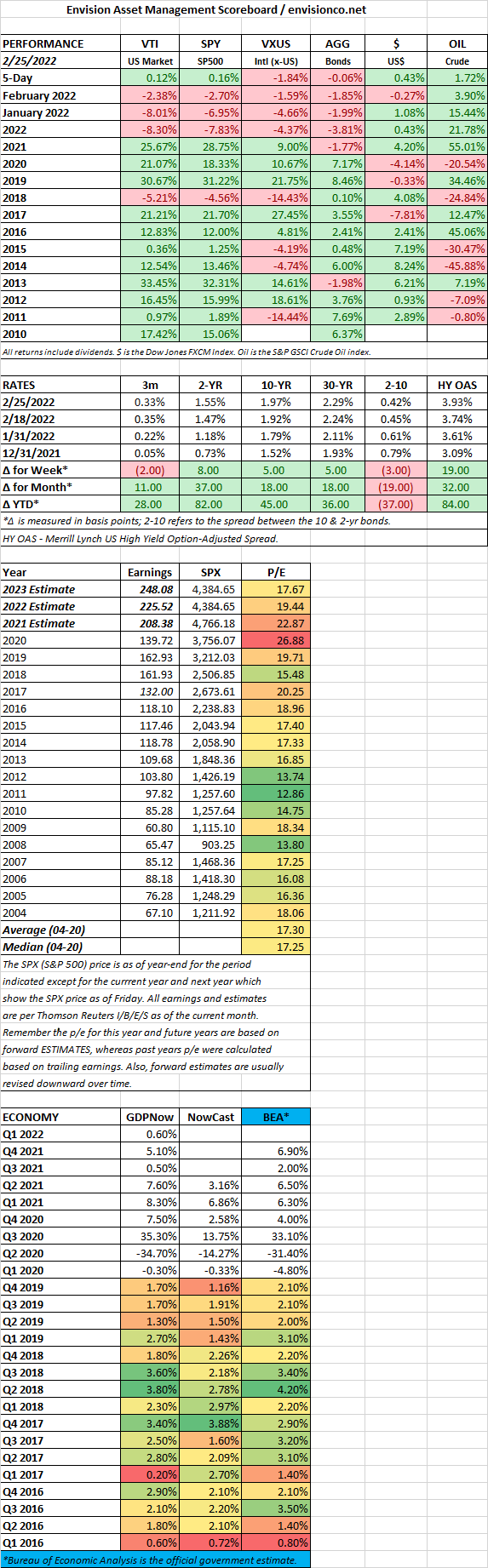

Stocks rallied by 0.21% in the US and by 0.89% outside the US. Bonds were up by 0.76% as interest rates on the 10 and 30-year bonds dropped.

The US added half a 430,000 jobs in March and February was revised up to 750,000. The unemployment rate fell to 3.6%. Interest rates rose on the news as the numbers reflect a strong job market. Average hourly earnings were up 5.6% from one year ago. The labor force participation rate increased to 62.4%

But while the jobs report looked good, the Institute for Supply Management’s Purchasing Manger Index (PMI) has been slipping. The March number came in at 57.1%, down from 58.6% in February (above 50 is considered expansionary). The new-order index was 53.8%, a sharp drop from 61.7% in February.

Biden said he would release one million barrels a day from the strategic reserve for six months to try to lower gasoline prices. Another bad move as that oil should be saved for when we really need it.

Amazon workers in Staten Island voted to form a union.

Most economists see a 1 in 3 chance of a recession in the next 12 to 18 months due mainly to the Fed’s not so great record in the past of avoiding recessions when hiking rates.

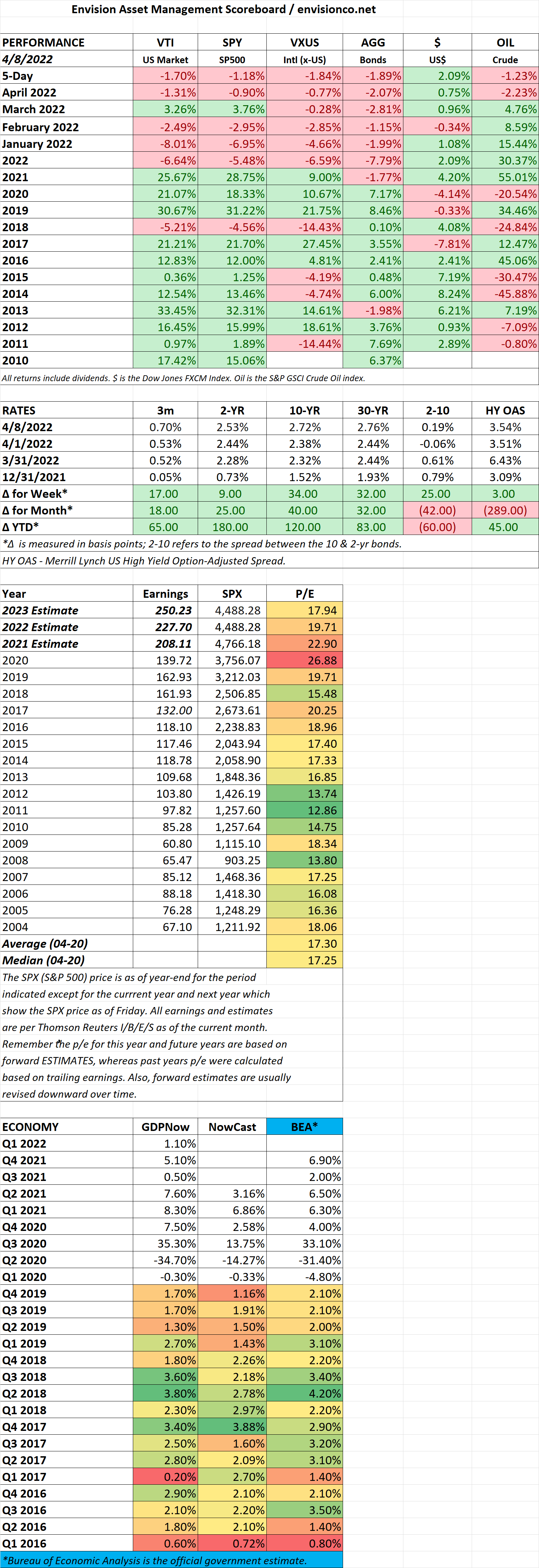

US stocks were up by 1.61% while international stocks were flat. Bonds got hit hard, declining by 1.85% as the yield on the 2 and the 10-year treasury bonds were up by 33 and 34 basis points, respectively, for the week. Crude oil shot higher by 10.49%.

The recent equity rally is being helped by higher interest rates pushing down the price of bonds, and cash getting murdered by inflation, moving investors back into equities.

The aggregate bond index is down by 6.8% year-to-date as yields continue to soar and markets price in more tightening and higher rates down the road. Investors are now anticipating half point hikes at the next two Fed meetings in May and June.

There are small signs that labor participation is beginning to pick up, rising by 0.4% in the three months ending 2/28/22. 1.87 million people went back into the work force which was 3x the rate from the prior three months. There are also indications that the “quit” rate is slowing down.

Higher inflation and interest rates will slowdown economic growth, with the offset being fading worries about Covid. How that mix all plays out will determine where the economy goes from here.

Stocks had a sharp rally at the US market was up by 6.22% and international equities were up by 6.67%, the best gain since November of 2020. Oil dropped by 3%, bonds were down by 0.29%.

With this weeks rally, stocks put in a higher low and a higher high, too early to tell if this is the end of this correction, but it has to start with a series of higher lows and higher highs.

The Fed raised its fed-funds target rate by 1/4% to 0.25%-0.50%.It is the first of probably 6-7 rate increases this year, but the general consensus is the Fed is way, way behind the curve. David Rosenberg, or Rosenberg Research, says that tightening cycles have led to a recession 75% of the time, “The Fed has never tightened into such a maelstrom before – a shooting war, a pandemic, a weak and wobbly stock market, and an incredibly flat yield.” Talk about having your hands full!

The 10/2 spread is just 20 basis points. An inverted 10/2 curve has signaled a future recession every time since the 1960s. But the 10-year/3-month curve, which economists also closely follow, still has a 1.7% point differential.

US stocks fell by 2.74% while international stocks and bonds both fell by 1.71%. The yield on the 10-year treasury increased by 26 basis points to an even 2.00%.

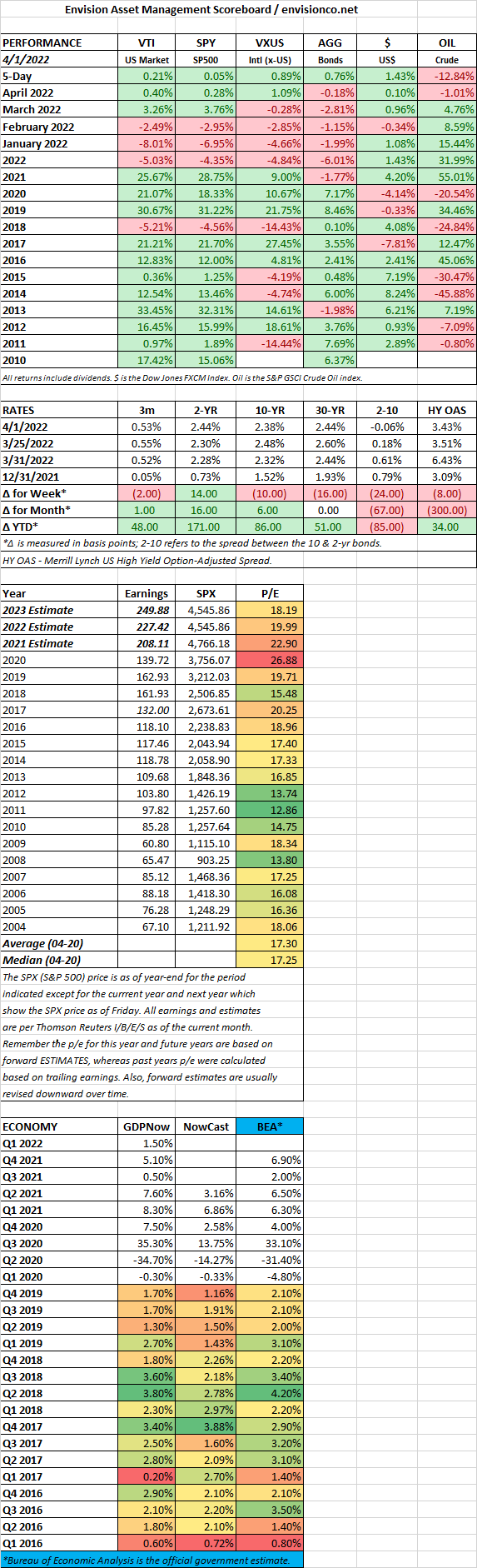

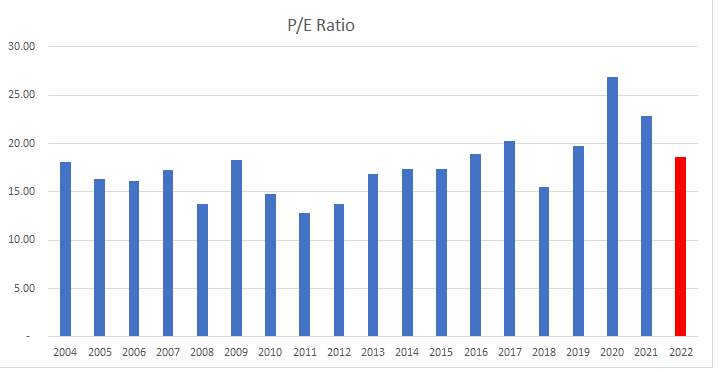

If earnings estimates hold for 2022, probably unlikely, but if they do, the current p/e on the S&P 500 is 18.57 (see the red bar below), not much higher (about 5%) than the average since 2004 of 17.66.

The Fed’s bond buying program finally ended this past Wednesday. Incredibly, the Fed was pumping money into the economy while the economy was soaring and the government was literally pumping in trillions via fiscal stimulus. And now they wonder why there is an inflation problem.

Markets are beginning to price in a recession. According to Nikolaos Panigirtzoglou, from JP Morgan’s global quantitative team, the US equity market has priced in a 50% probability of a recession and the investment grade bond market is assuming a 43% chance.

US stocks fell by 1.56% while international stocks got hammered, down by 5.84% due to the war in Ukraine. Bonds were up by 0.81%, oil skyrocketed by 26.37%.

Russia and Ukraine account for about 3% of world GDP, however, the war can induce a supply shock that will impact the global economy in a bigger way,

JP Morgan has cut its annual global GDP growth by 0.8% to 3.1% through Q4 2022,

Their inflation projection has been increased by 0.9% to 4.6%.

The US GDP growth has been cut by 0.15 to 2.7% and CPI is now forecast at 4.9%, up by 1%.

Previous spikes in oil prices have led to recessions, two in the 1970s and one in 2008. Although all were bigger in scale than the current one (at least so far).

According to Ned Davis Research, looking back at more than 50 crisis events starting with the Panic of 1907, the Dow fell an average of 7% immediately after the event but was up by 4.2%, 6%, and 9.6% in the following three weeks, nine weeks, and 18 weeks.

A strong jobs report, payrolls were up by 678,000.

Over 75% of Nasdaq stocks and 51% of S&P stocks have already declined by more than 20%.

After weeks of denying that he would invade Ukraine, Putin and the Russians did just that.

Apparently investors followed Baron Rothschild’s sage advice to “buy when there’s blood in the streets” as markets skyrocketed from 2.75% down on early Thursday morning to up 6.96% at the close on Friday.

The war is likely to lead to higher oil prices and thereby, higher inflation.

For the week US stocks were up by 0.93% while international stocks fell by 1.22%.

Prior to the rally, the NASDAQ 100 was close to a bear market, off by 18.46% on a closing basis, at the same time, Brent crude oil hit more than $100 per barrel. The Russell 2000 was off by 24% from its high.

Average home prices in major metropolitan areas rose by 18.8% for the 12-months ending in December. Home price growth is expected to slow going forward.

US stocks fell by 1.60%, international stocks by 0.37%, and bonds by 0.21%. The spread on high-yield bonds has expanded by 65 basis points year-to-date.

Russia continues to inch closer to a war with Ukraine. The Russians deny it, but all available intelligence suggests otherwise.

The 10-year treasury peaked on Tuesday at 2.05%, the highest rate since July of 2019. The rate fell to 1.92% by Friday. Some are making the case that a slowing economy and a possible war with Ukraine will cause interest rates to drop.

The debate is rising on how the Fed can get inflation under control without throwing the economy into recession. The Fed probably saved the economy from a depression when Covid hit, but went way overboard, along with Congress/Trump/Biden in pumping trillions and trillions into the system when we were well on the way to recovery. Now the Fed has to dig out of this mess.

Mortage rates are at their highest point since January of 2020.