MARKET RECAP

Stocks advanced again last week, with US markets up by 1.77% followed by international markets at 1.48%. For November, stocks rallied 16.59%. It was the best November since 1928. Bonds declined by 0.57% for the week as the yield on the 10-year Treasury rose by 13 basis points.

91% of S&P 500 companies are trading about their 200-day moving average, the highest percentage since July of 2013.

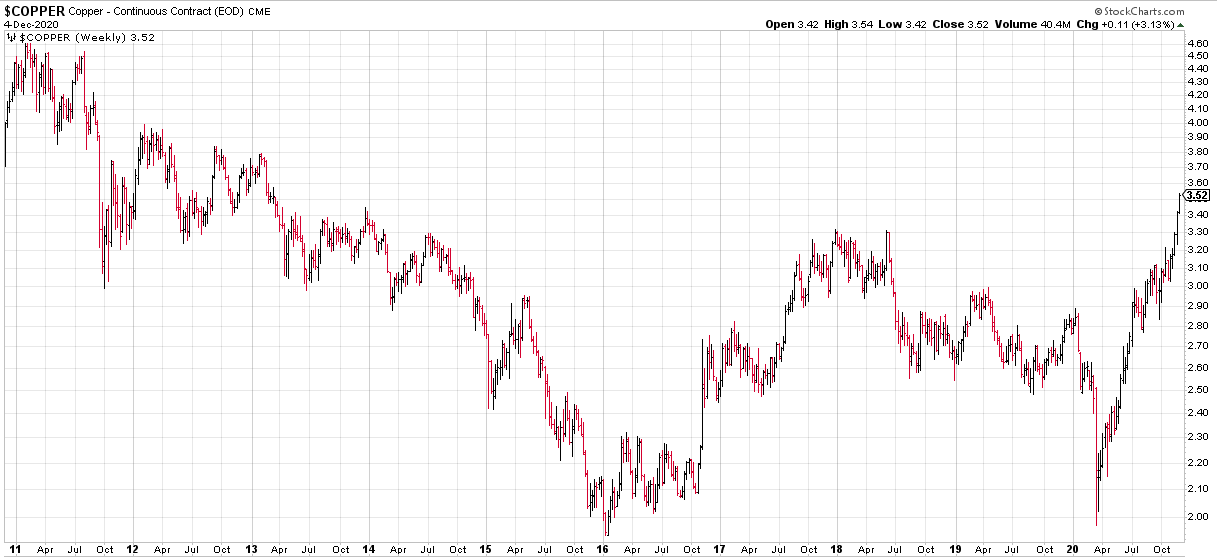

Super-low interest rates and hopes for a spectacular recovery are fueling the rally. Industrial metals are anticipating a surge in activity, copper is at a seven-year high, and the other industrial metals are all way up in price.

But the anticipated slow-down in the labor market that we have written about in the last couple of months appears to be here. Non-farm payrolls were up by only 245,000 in November, down from 610,000 jobs in October. The unemployment rate did fall to 6.7%, but that was due to 400,000 people leaving the workforce. The weak report might spur Washington to move quicker on a stimulus plan. The latest proposal centers on a $900 billion stimulus package.

22 million jobs were lost at the beginning of the pandemic, and the US has regained 12 million of those. Government payrolls were down by 100,000 while hiring was up in transportation and warehousing, reflecting e-commerce, which has been the big beneficiary of the virus.

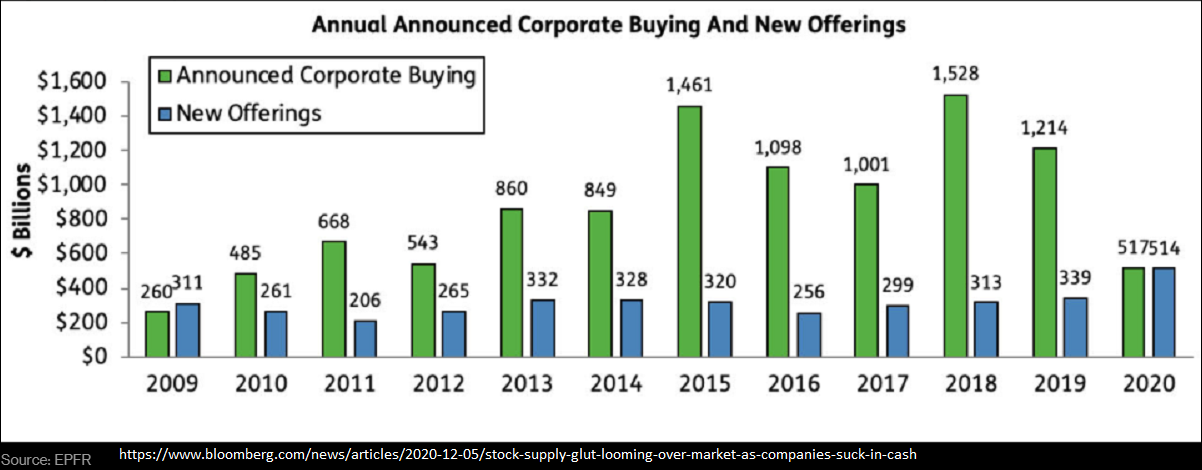

Over the last decade, equity taken out of the stock market, mainly via stock buybacks and takeovers, outpaced equities issues, via initial and secondary stock offerings, by a 3 to 1 ratio. But this year, the numbers have evened out. That makes the stock rally this year even more impressive, as stocks are up 18.65% without that tailwind. But it might be giving a message on valuation, with companies selling stock into the market to “sell high” and holding back on buybacks given high prices and valuations.

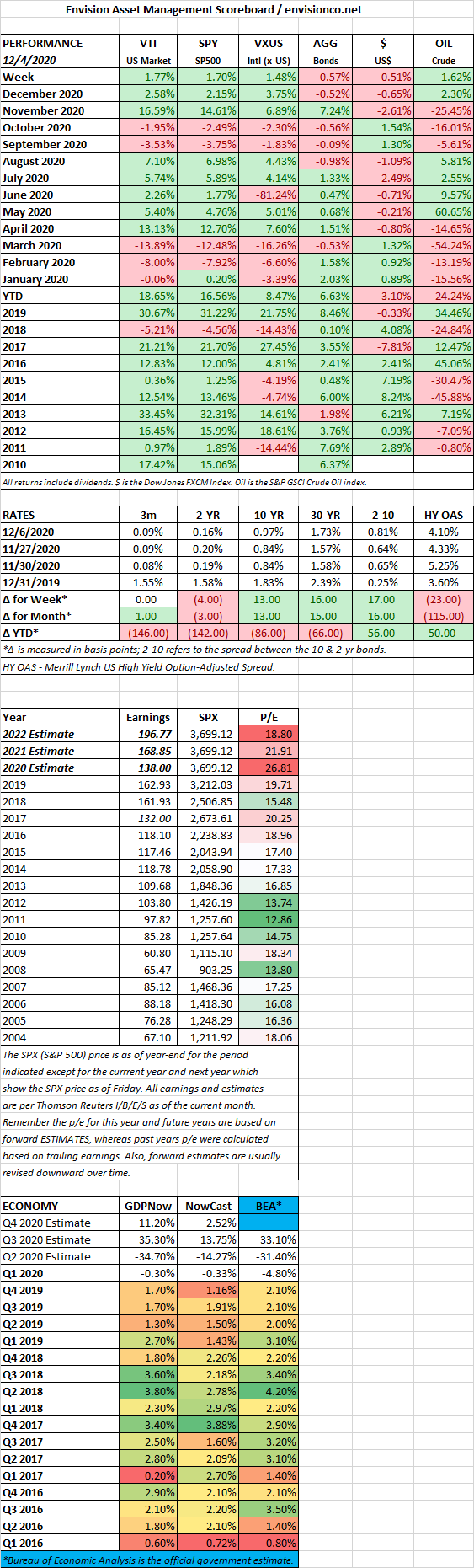

SCOREBOARD