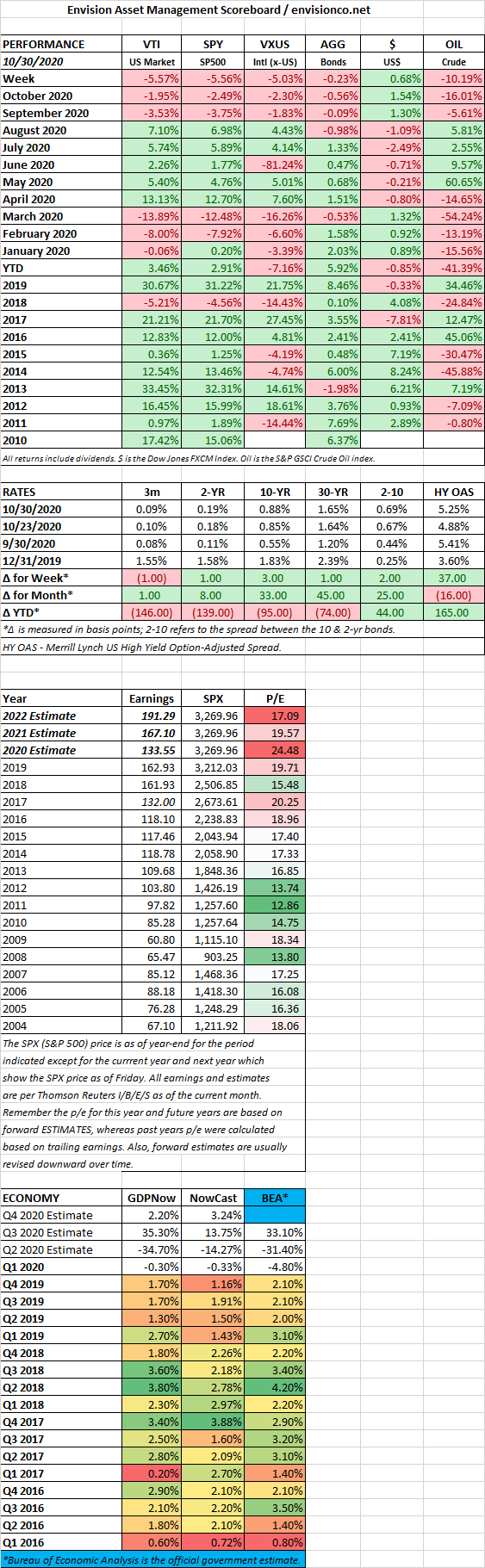

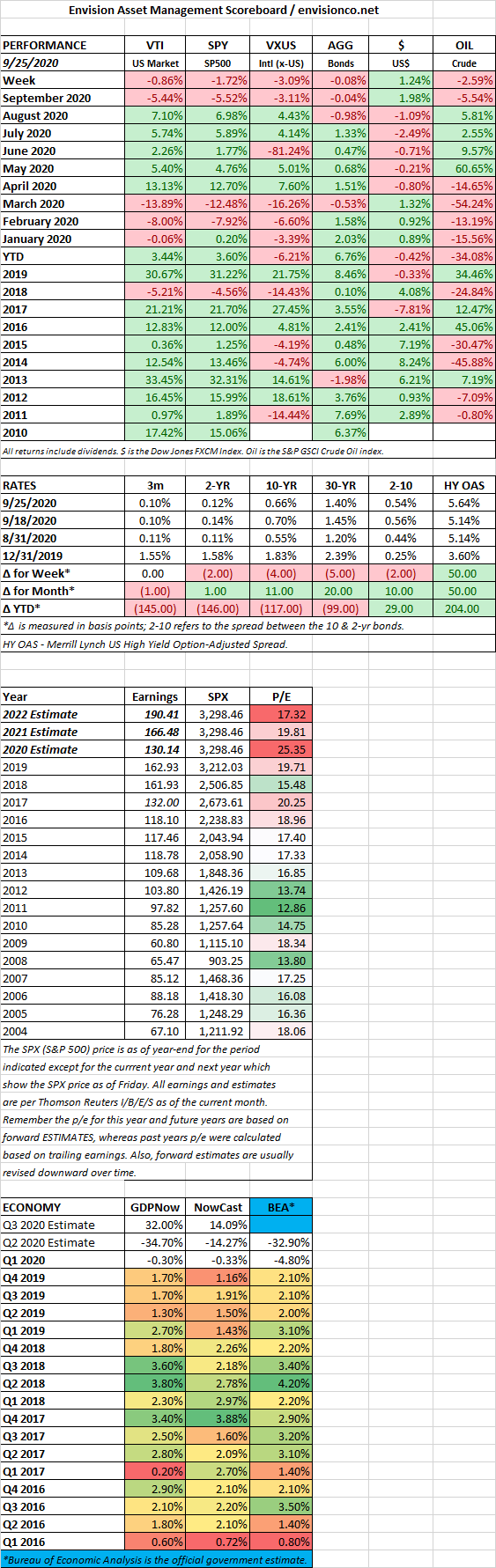

SCOREBOARD

SCOREBOARD

HIGHLIGHTS

MARKET RECAP

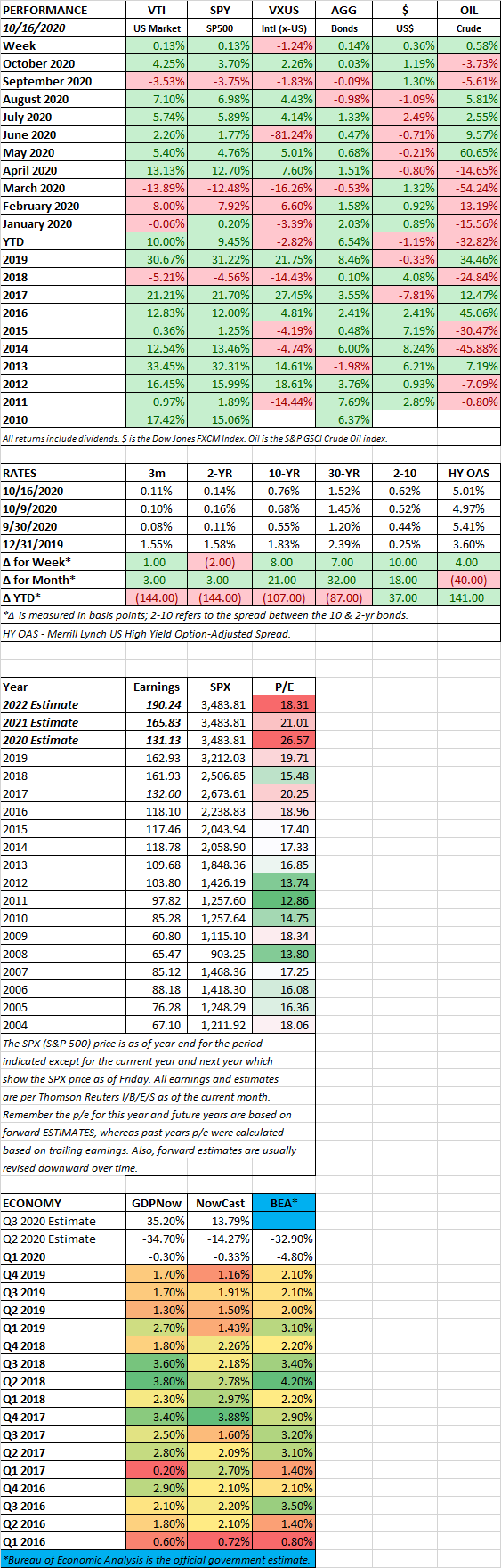

The market was anticipating a Biden romp, a blue wave, and a huge fiscal package that would offset higher tax rates. Investors figured that was a good formula and stocks ran up in anticipation. What they got might even be better. Biden will be the President, a Senate that might lean Republican, and the Republicans even managed to pick up seats in the House. What it all means is the US gets a civil, decent, and more predictable President, someone that will act as a unifier and a leader for all, and that will be restrained from doing anything too crazy given the mix of the Senate. The market liked the look of that and turned in its best week since April, up 7.35%, it was the best election week return since 1932, and that was coming off the worst pre-election week ever.

Of course, Trump refused to concede defeat, embarrassing himself in the process, claiming the votes that put Biden over the top were illegitimate and filing lawsuits wherever possible. But no one is buying it, Biden will be the next President after the lawsuits run their course.

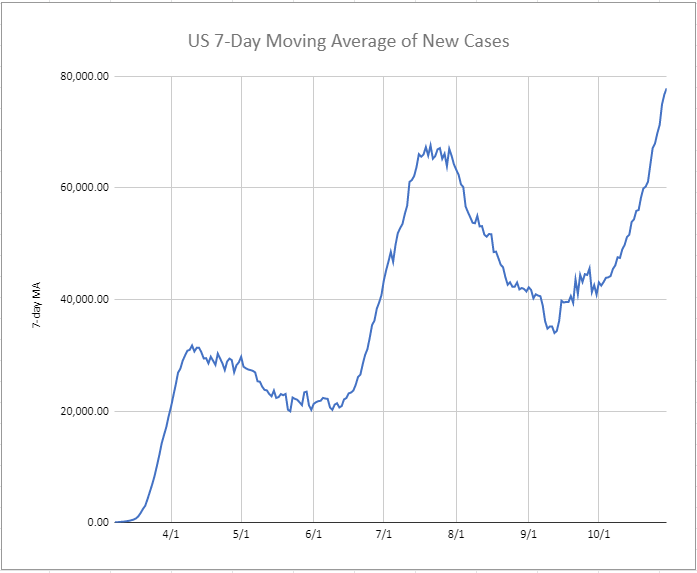

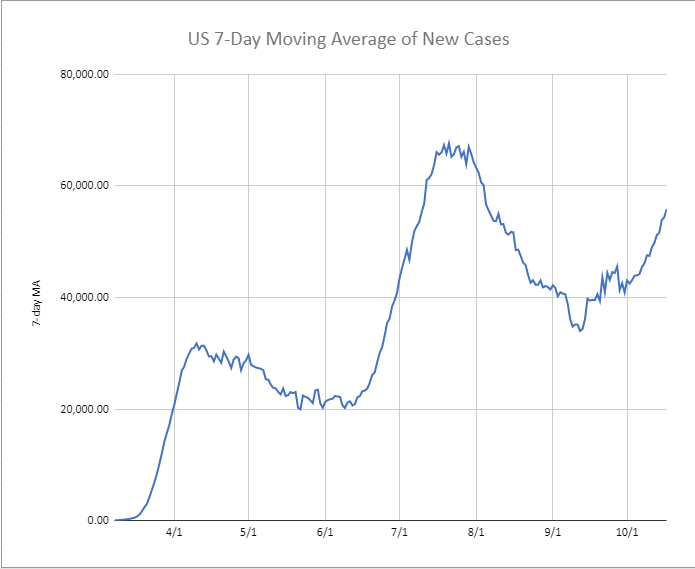

While the political news was good, the virus news wasn’t. The virus is taking on an exponential growth rate and that is bound to impact the economy until it gets under control.

In the meantime, the economy continues to rebound. The Institute for Supply Management’s manufacturing index increased to its highest level, 59.3, since 2018. New orders reached its highest point in 17 years. The October payroll report was also strong, as the US added 638,000 new jobs and the unemployment rate fell to 6.9%.

Stocks are getting support from interest rates that basically don’t exist, at least above zero. Bloomberg reported that negative-yielding debt hit $17.05 trillion on Friday, surpassing the August 2019 mark. On top of that, the Fed is buying $120 billion per month in treasuries and agency mortgage-backed securities each month. The Fed’s balance sheet has ballooned to $7.1 trillion from $4.1 trillion at the end of February. And as we have shown in the past and below, there is a strong correlation between Fed assets and the stock market.

More than 25% of all investment-grade debt now yields less than zero. That has pushed investors into equities as well as riskier fixed-income investments like high-yield and leveraged loans. While the price of the riskier fixed-income products has risen, the fundamentals haven’t. The artificially low investment-grade yields are masking potential problems in these debt markets. A problem maybe not for now but probably for later.

SCOREBOARD

HIGHLIGHTS

MARKET RECAP

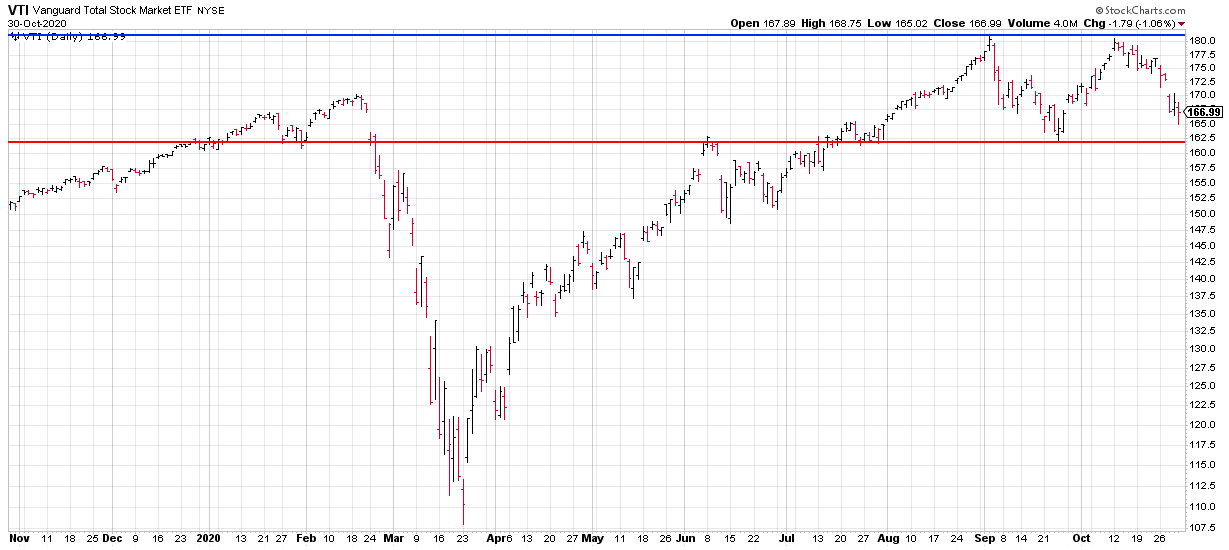

US stocks fell by the most since March, dropping 5.6%. It was the worst loss ever in the week preceding a Presidential election. While stocks fell, the ten-year yield reached its highest level since June, the exact opposite of how treasuries normally act in a falling equity market. High tech valuations, a fast-expanding virus in Europe and the US, and then throw-in election worries and you have what it takes to tilt the market way off balance.

US equities hit their high on 9/2 and then sold off by 9% through 9/24. A subsequent rally ended on 10/12 when stocks could not break through the September high. The market is now down 7.5% from the high.

The economic news for the week was good. GDP was up by a record amount in the third quarter. Jobless claims fell to a 7-month low, coming in at 751,000. Personal income rose in September by 0.9% and personal spending was up by 1.4%. Corporate earnings are down 12.5% from last year but 9% higher than was forecast, according to Lindsey Bell, the chief investment strategist at Ally Invest.

Real GDP shot up by a record 33.1% in Q3, which followed a 31.4% drop in Q2. Net, net, the US is down about 3.5% from the pre-crisis peak. To close the remaining gap, the service economy is going to need to get back to normal, and that will be almost impossible if the virus keeps impacting economic activity.

With the election just a few days away Biden leads by more than 8 percentage points based on recent surveys, but Trump is counting on inaccurate polling to pull the surprise victory. The pollsters, who completely miscalled the 2016 election, say don’t count on it, with the likely outcome being between a somewhat close contest with a Biden edge that can be disputed and spillover to the courts, to a Biden blowout win. The bigger question is can the Democrats take the Senate. Assuming a Republican victory in Alabama, the Dems will need to win four seats currently held by Republicans to gain control. With Colorado, Maine, and Arizona leaning to the Democrats, “North Carolina or Iowa could be the tipping-point states,” according to Jessica Taylor, editor of the Cook Political Report.

Germany and France implemented a new set of lockdowns to try to get the virus under control. France will lockdown for at least one month. People will have to remain at home, nonessential businesses will close. The German lockdown is less restrictive but will close restaurants, bars, gyms, and theaters. Here in the US, the surge of the virus is now at record levels.

A second wave in pandemics is common. The Spanish Flu of 1918 was marked by an initial breakout in the spring of 1918 followed by a second wave from September to November of 1918. The Asian Flu of 1957 had its initial wave in the US in October of 1957 and then the second wave in January and February of 1958. The Hong Kong Flu of 1968 started in July of 1968 and lasted into the winter of 1969 and then a second wave appeared late in the fall of 1969 and ending in the winter of 1970.

SCOREBOARD

HIGHLIGHTS

MARKET RECAP

Stocks fell by 0.40% in the US as hopes for a stimulus package wavered up and down during the week. Overseas, the markets did better, advancing by 0.60%. Earnings so far have been positive, 83.7% have beaten forecasts and the average earnings have topped expectations by 17%, this is compared to 65% and 3.5% on average, respectively.

The size of the labor force fell in more than half of the 30 states that showed a decline in unemployment rates last month. That is a signal of a weakening labor market. The unemployment rate is a function of people finding new work, those who cannot find work, and others who left the workforce entirely. When people stop looking for work, it pushes the unemployment rate down, even though it is actually indicative of weakness, not strength.

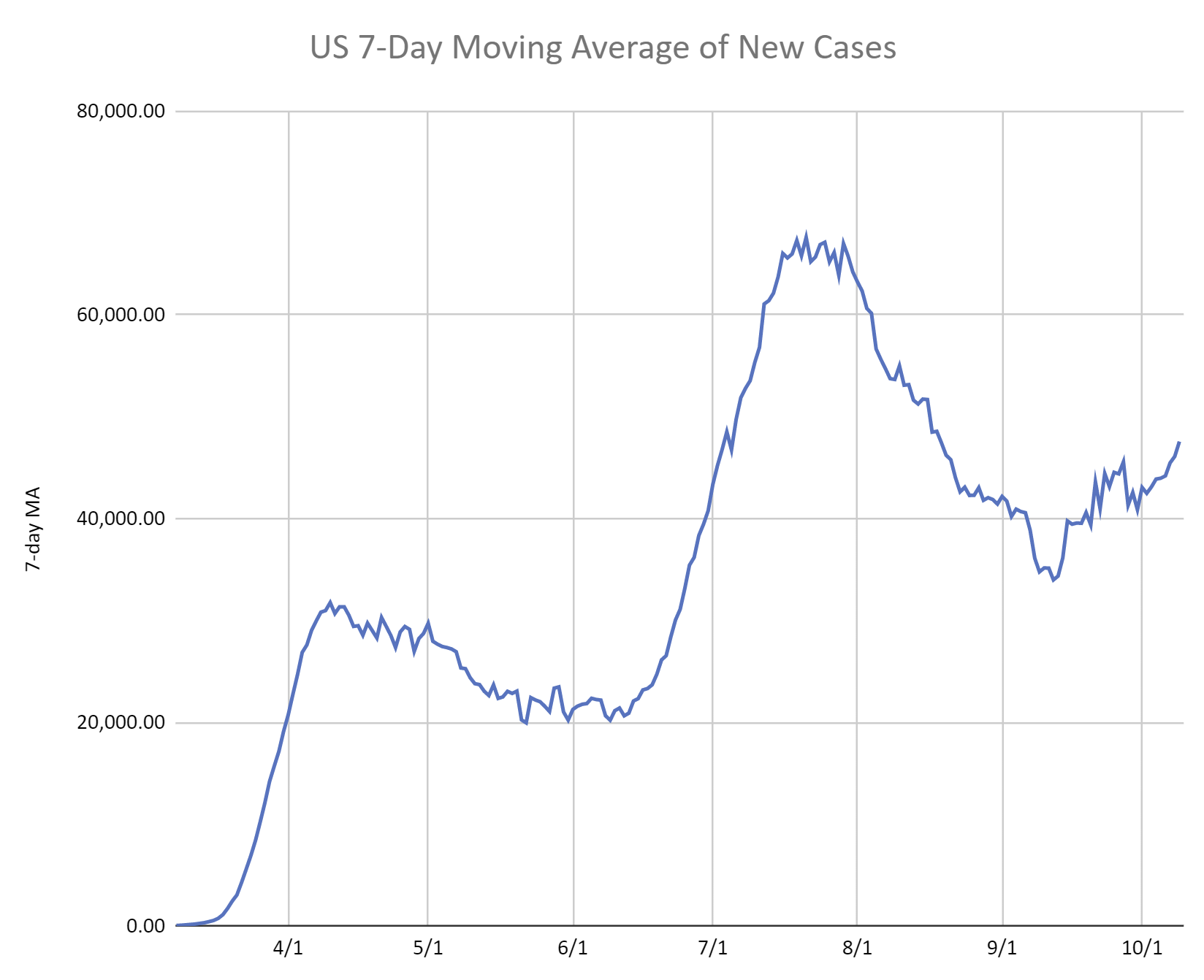

The Covid virus is back at full strength in the US, reaching the highest level since July as communities across the country open up. The virus is now beginning to circulate in higher numbers in rural type areas and people in their 30s and 40s are the main age group, compared to 18-24 in the previous peak. The surge is arriving earlier than was expected. The numbers are also surging in Europe.

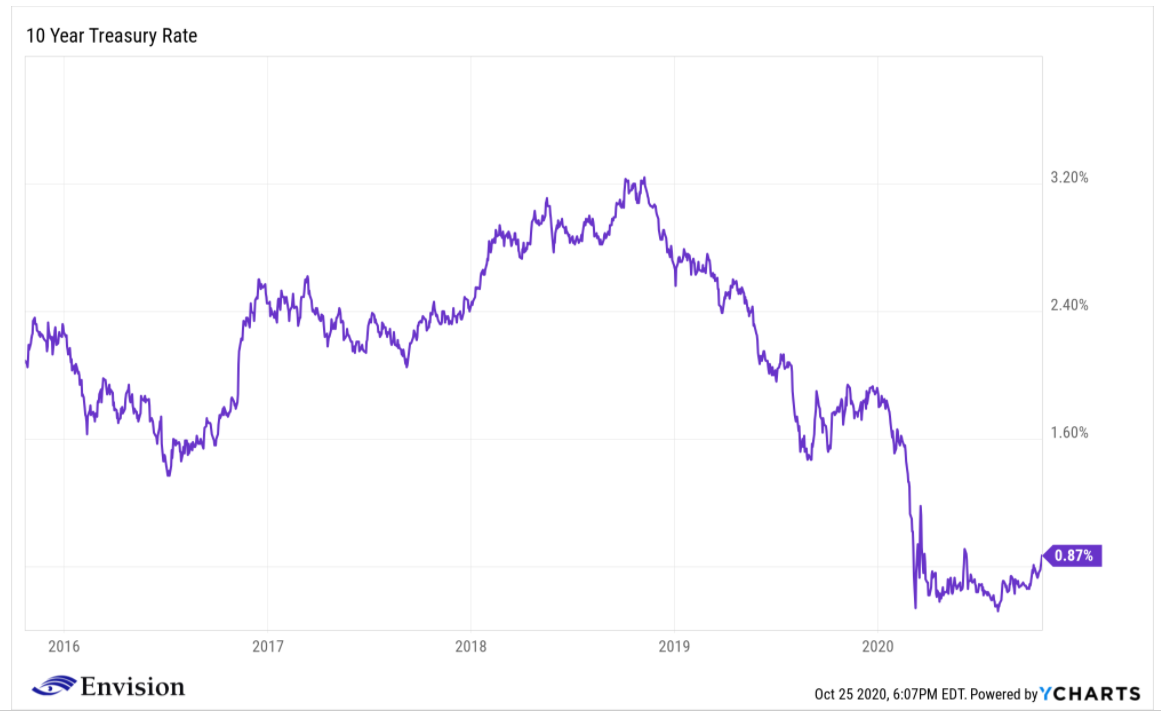

The 10-year yield has ticked up to 0.87%, which is the highest yield since June, as the bond market begins to anticipate a Democratic sweep and a massive stimulus bill. The deficit could expand by $5 trillion-plus under such a scenario. The difference between the 10-year and 2-year yields reached 71 basis points on Thursday, which is the most since February of 2018.

China posted 4.9% growth in the third quarter, slower than what was expected but still good relative to the rest of the world. Its growth rate continues to catch up with last year. China is the only major economy to grow this year.

SCOREBOARD

No commentary this week, below is the scoreboard.

MARKET RECAP

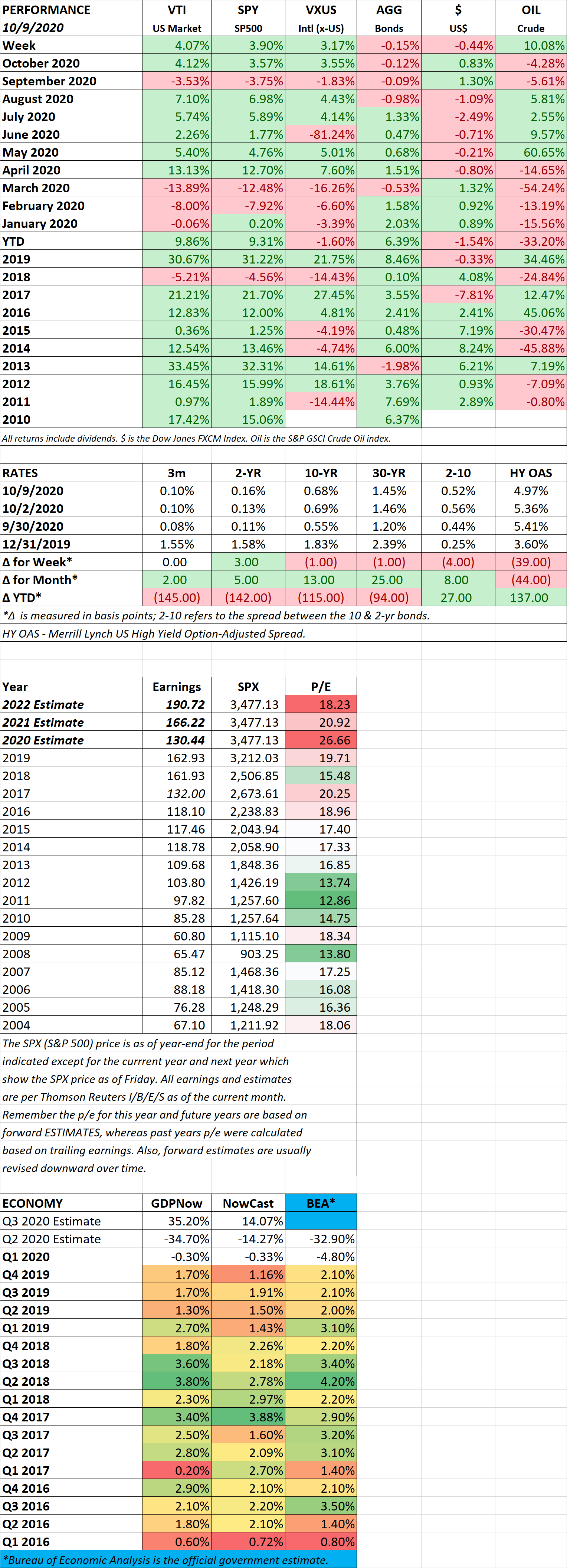

The market had its best week in three months as US markets increased by 4.07% and international stocks advanced by 3.17%. Investors were cheered by Biden opening up a bigger lead on Trump, hoping that minimizes the chances of a contested election. The consensus is also moving in the direction that a Democratic win will be good for stocks, as it would probably mean big fiscal spending.

The Republicans and Democrats appear to be getting closer to a coronavirus relief package, after Trump shutdown negotiations earlier in the week, only to change his mind a day or so later. Treasury Secretary Mnuchin upped the ante to $1.8 trillion on Friday, while the Democrats have proposed a $2.2 trillion dollar package. There are some Republican Senators who are opposed to a large spending package, so there will still be obstacles to overcome.

SERVICES

The Institute for Supply Management reported that its nonmanufacturing index, a survey which measures services activity, increased to 57.9 in September from 56.9 in August. In Europe, the purchasing-managers index fell due to a rising coronavirus. In Spain, the index fell to 42.4 from 47.7.

COVID

The virus is definitely on the rebound in Europe and the US. Eight US states are up 10% week over week. New cases in France are up to 18,000/day. The UK is up 20% from the prior week. The numbers in Spain are also way up. The good news is that we are getting closer to the initial launch of vaccines, probably in December. And there could be emergency approval of a couple of antibody drugs by Lilly and Regeneron that could help bridge the time gap between now and future vaccines. Of course, the rollout of these products will take a while, but we are getting pretty close to the initial launches.

SCOREBOARD

HIGHLIGHTS

MARKET RECAP

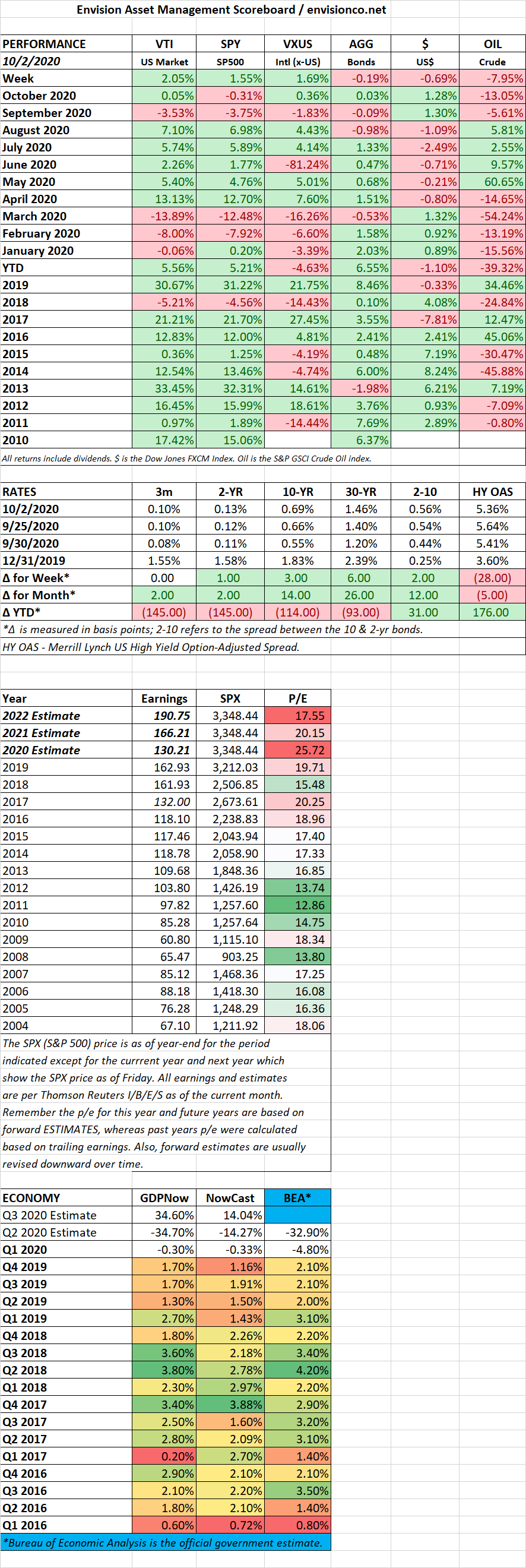

US stocks were up by 2.05% and international stocks were 1.69% higher on hopes for a stimulus bill. Oil slumped by 7.95% on fears of a slowing economy.

Trump and Biden faced off in the first Presidential debate on Tuesday and let’s just say there was nothing presidential about it. It was a new low in presidential politics as Trump just talked over and through the moderator and Biden. Then on Friday, it was announced that Trump had tested positive for Covid. Analysts seem to think this increases the odds of a stimulus bill.

Payrolls were up by 661,000 in September. Leisure and hospitality began to come back to life, adding 318,000. Construction was also strong, plus 26,000. But the total number was 200,000 lower than the consensus estimates. The unemployment rate fell to 7.9% from 8.4% last month, but a lot of that was driven by the fact that 700,000 people left the workforce. Payrolls are still 10.7 million less than the February numbers.

The Conference Board reported that consumer confidence jumped to 101.8 in September from 86.3 in August. It was the biggest increase since April of 2003 and brought the index to the highest level since March. Consumer confidence had dropped in the two previous months due to Covid outbreaks in several states like Florida and California.

A record number of retail stores are closing and will set a record by year-end. Through mid-August, more than 10,000 stores have either closed or there have been announcements that they will close, and that number could shoot up to 25,000 by year-end according to market-research firm Coresight Research. That tops the 9,500 from last year. Six thousand of those closings were due to bankruptcies. That translates into 130 million square feet of space. More than half of that is due to JC Penny, Stein Mart, Bed Bath & Beyond, and Pier I Imports.

US household income fell by 2.7% in August due to a drop in unemployment benefits. Despite the drop, household spending was up by 1% in August, down from 9% in May, 7% in June, and 2% in July. Initial jobless claims fell by 36,000 to 837,000 for the week ending September 26. American Airlines and United plan to proceed with 32,000 job cuts, other job cuts announced were 3,800 by Allstate and 28,000 by Disney.

The long-term growth forecast for the US, released last week by the Congressional Budget Office, is dreary at best. The CBO projects economic growth to average 1.6% over the next three decades. The lowest number since the 1930s. The slow-growth is a result of demographics, productivity, and national debt. Covid has impacted birth rates this year and probably going forward. That, combined with less immigration, and already falling birth rates, means less young Americans to help grow the economy in the future. Productivity is projected to slow due to less business investment and an older population. Exploding national debt will crowd out private investment. The CBO projects that in 2049 debt will be 189% of GDP, from 79% last year.

SCOREBOARD

HIGHLIGHTS

MARKET RECAP

Stocks declined for the fourth consecutive week as the US market was off by 0.86% and international markets fell by 3.09%. Worries about rising coronavirus numbers and the subsequent economic impact, high valuations, as well as a volatile presidential race, have impacted prices. However, some of the tech stocks that were leading the decline rebounded this week, Amazon was up by 4.8% and Apple finished 5.1% higher. Fed Chair Powell has called on Congress to provide additional fiscal assistance to the economy. Estimated growth for Q4 will come down markedly if Washington cannot agree on a deal.

International stocks had a big fall, down by 3.09%, as Covid numbers continue to spike substantially higher in Europe and pressure increased to take aggressive steps to slow the spread. Numbers are also increasing in parts of the US. The Midwest appears to be getting the surge in cases that had previously hit other parts of the country. But even New York, which has been well under control since July, reported more than 1,000 new cases on Friday. Numbers in Florida have stayed flat recently at substantially lower levels from the peak, but will be getting a test soon as Florida Governor Ron Desantis has lifted all restrictions in the state.

Initial public offerings are setting up for the biggest year since 2000, having already raised $95 billion so far this year, almost matching the 2014 number and there are still three months to go.

The economy is improving, although not at the rate that many had hoped. However, there are some pockets of strength. Durable goods orders were up for the fourth consecutive month, increasing by 0.4%. New orders for nondefense capital goods excluding aircraft were up by 1.8%. Andrew Hunter, an economist at Capital Economics, said “business equipment investment staged a V-shaped recovery in the third quarter.”

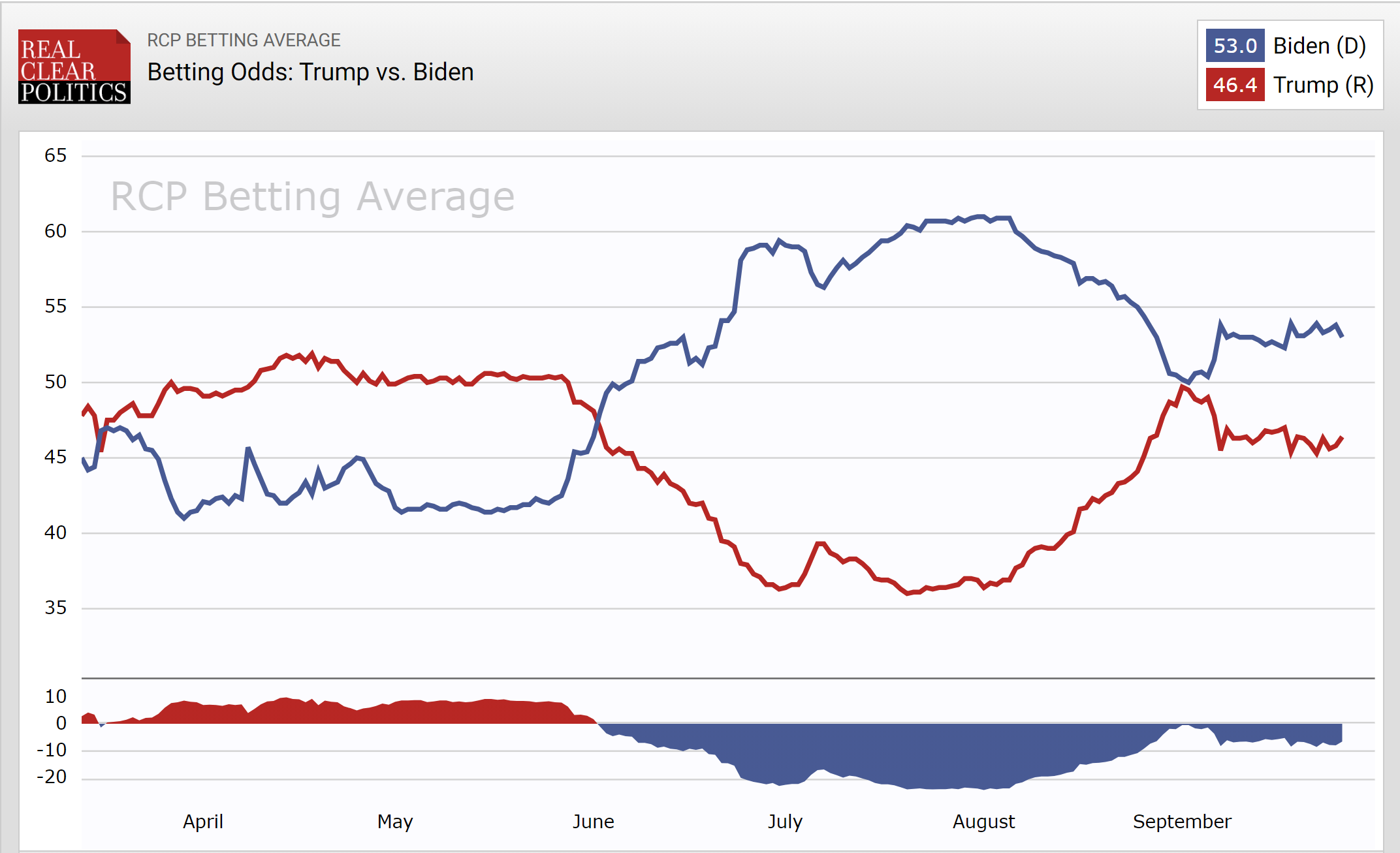

Trump said he would not commit to a peaceful transfer of power. “Well, we’re going to have to see what happens,” Trump said. Basically threatening to usurp one of the most hallowed traditions of the United States. Another reason why he is unfit to be President. The betting odds still favor Biden.

SCOREBOARD

MARKET RECAP

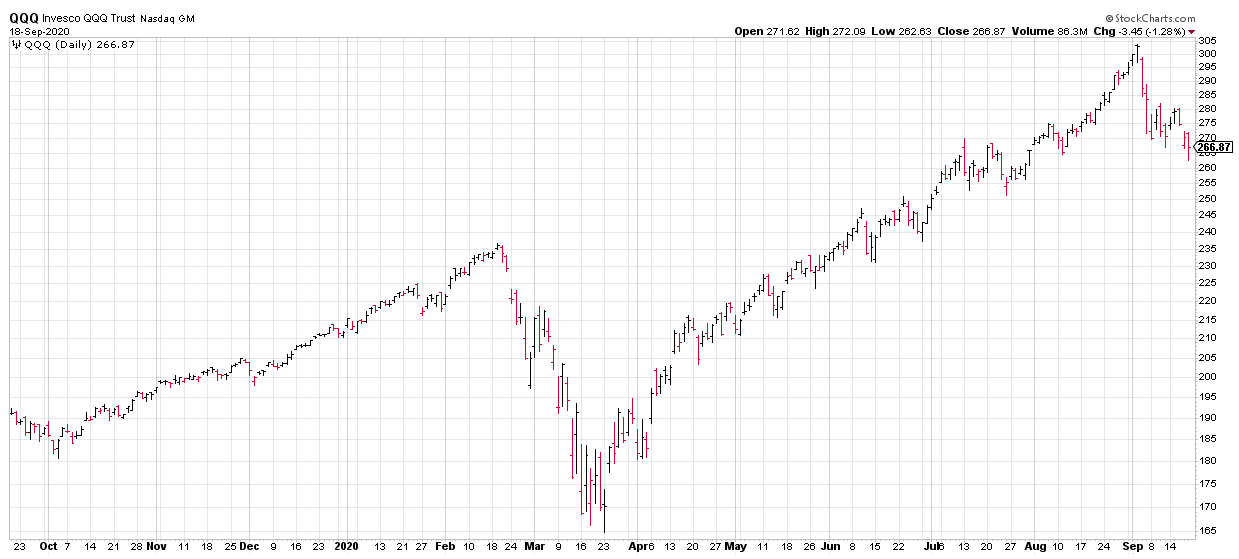

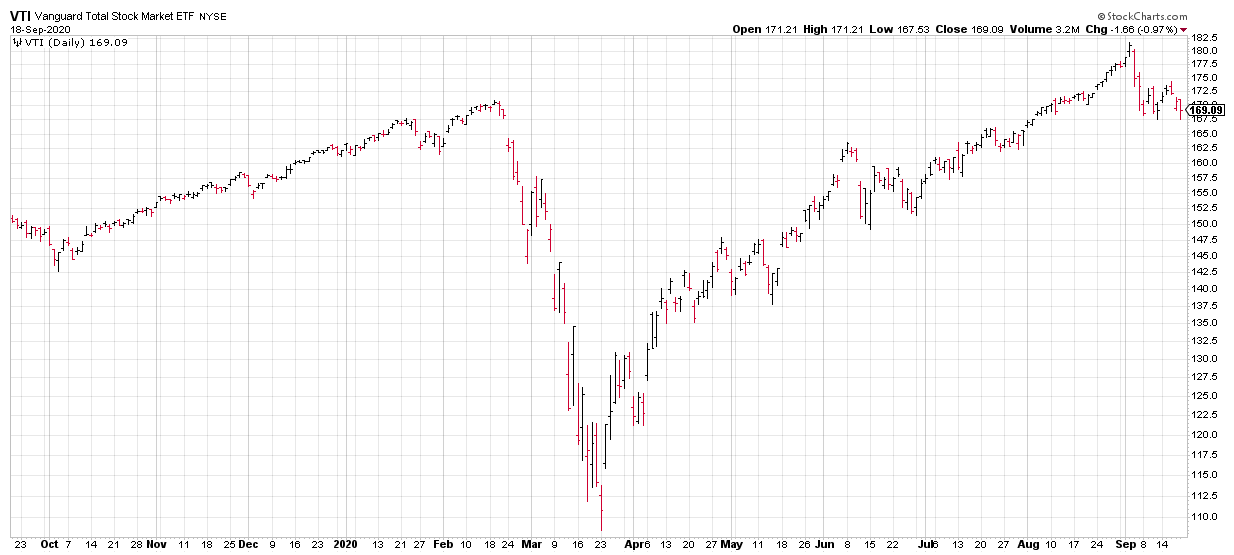

Stocks fell for the third straight week as technology stocks continued their fall from grace. Amazon dropped 5.2%, Facebook 5.3%, Apple was down 4.6% and Google lost 4%. Since the September 2nd closing high, the overall US market as measured by the VTI is down 6.7% and the Nasdaq as measured by QQQ is down 11.9%.

The VTI (total US stock market) hit a new low on Monday, rallied slightly during the week, and then touched the low again on Friday before bouncing to close off the low. The Qs (Nasdaq 100) was not so fortunate, breaking down to a new low on Friday, in what might indicate further downside.

Despite the recent fall, there are still signs of excess in the market. Snowflake (SNOW) went public in what was the biggest initial public offering of a software company ever. Priced at $120, the stock soared to $245 in the initial trade, giving the company a market value of $68 billion or 110 times revenue.

The Fed said during the week that the economic outlook is highly uncertain and said they would keep interest rates at close to zero for three more years and would continue to buy $120 billion of agency mortgage-backed securities and treasuries each month. The Fed also updated their guidance and said the Fed would need to see evidence of a tight labor market and that inflation will “moderately exceed 2% for some time” before considering raising rates. Paul Volker must be rolling over in his grave.

US retail sales increased for the fourth straight month but the pace was slower than earlier in the summer. August sales were up by 0.6% over July and were above pre-pandemic levels. The retail sector has recovered well, unlike other parts of the US economy, which still trail pre-pandemic numbers. Meanwhile, in China, retail sales have rebounded to pre-pandemic levels. Q2 growth was up 3.2% compared to a 6.8% decline in Q1. China has had the pandemic more or less under control since its initial outbreak.

Mortgage data firm Black Knight Inc. says about one million homeowners are behind on their mortgages and could be in danger of losing their homes when restrictions on evictions and foreclosures expire.

Initial claims for unemployment fell by 33,000 to 860,000 last week.

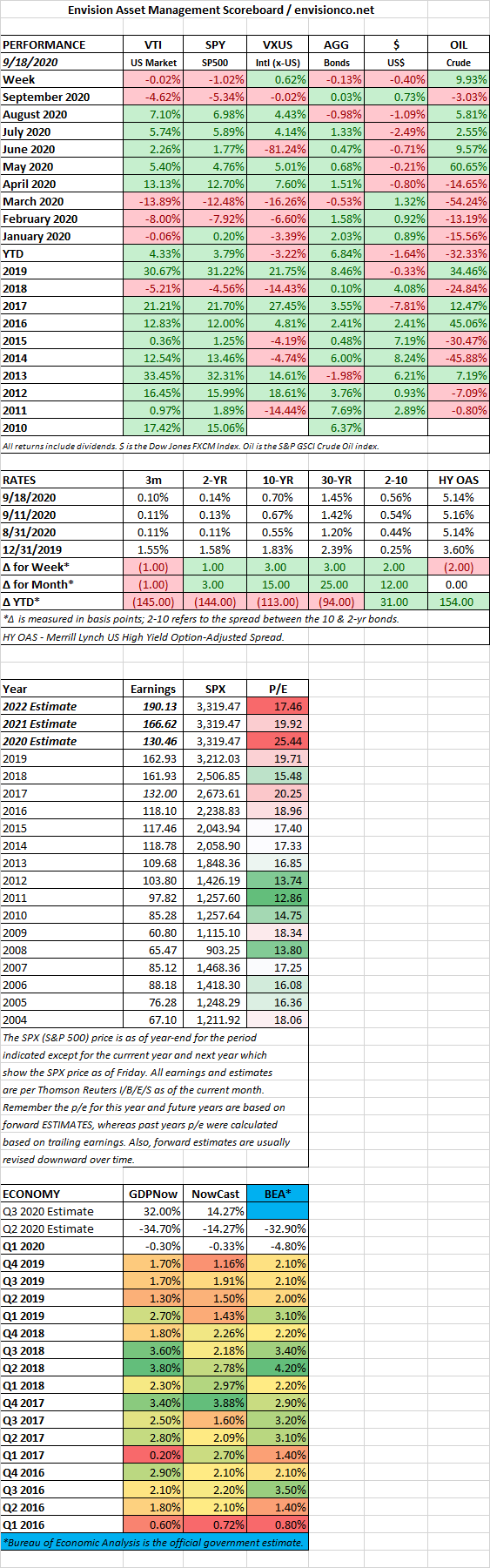

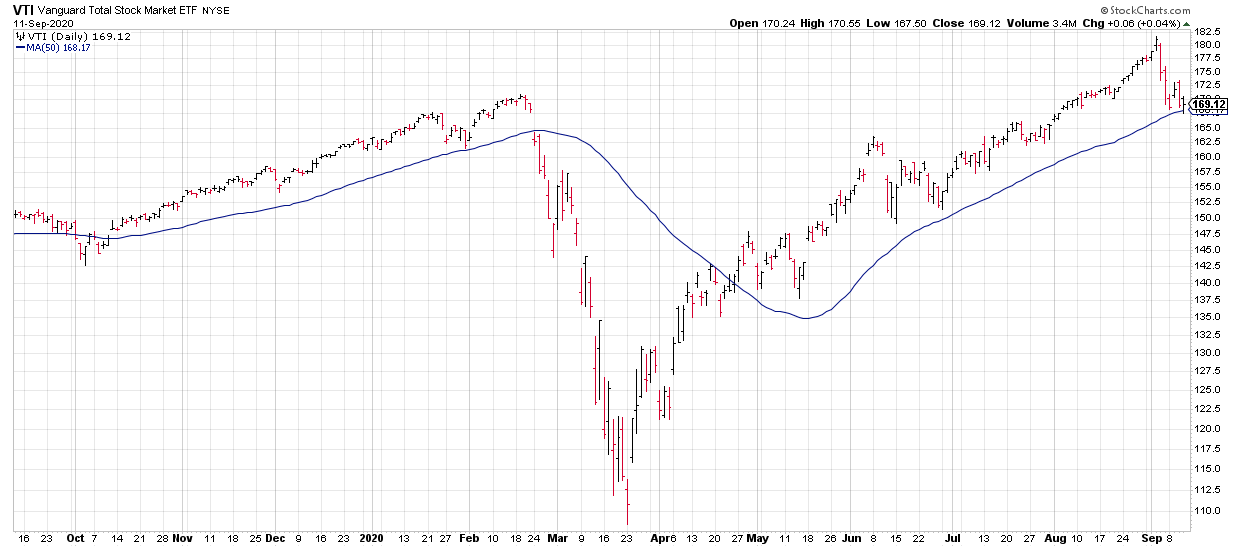

SCOREBOARD

MARKET RECAP

For the week, US stocks fell by 2.5% while the Nasdaq composite was off by 4.1%. The VTI (the total US stock market) has sustained some technical damage, and is barely above its 50-day moving average, after recovering from earlier in the day on Friday when it fell below. A break below the 50-day straight from here, or a failed rally to new highs followed by a break below the 50-day, could signal a bigger drop ahead.

Tech stocks have been up and down all week in volatile trading. The Nasdaq 100 had a 3% span from high to low on Friday and is down 11% since September 2. That decline was after a 58% run from late March. Apple is down 16% from its high but is still up almost 100% since its March 23 low. Tesla dropped by 21% after it was not selected to join the S&P 500. The overall US market is down 6.8% from September 2 closing price.

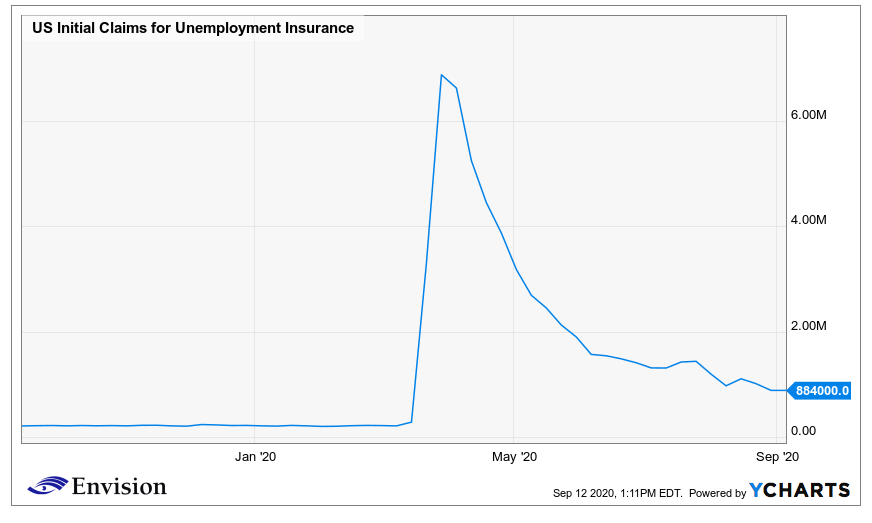

The easy gains in economic output coming off Q2 are beginning to slow down. The Federal Reserve Bank of Atlanta estimates the US will expand by 7% in Q3, up from a 9.1% contraction in Q2. But they are only looking for a Q4 expansion of 1.25%. Unemployment claims came in at 884,000 last week. The pace of the decline is beginning to flatten out at a level that still exceeds the prepandemic record or 695,000. The number of job postings is at levels 20% below last year according to Indeed.com. Washington’s inability to agree on a new stimulus package and restrictions that still remain on many businesses such as restaurants and bars in parts of the country are also holding back the economy.

SCOREBOARD