No commentary this week due to the holiday. Below is our weekly scoreboard:

No commentary this week due to the holiday. Below is our weekly scoreboard:

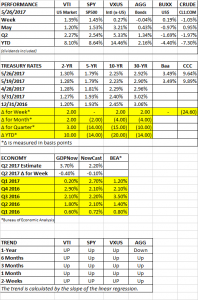

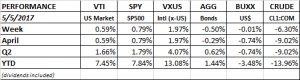

PERFORMANCE

The firing of FBI Director Comey remained in the news this past week. Markets headed south on Wednesday, dropping 1.8%, on news that Trump had asked Comey to “let it go” in regard to the FBI investigation of former adviser Michael Flynn’s ties Russia. That started talk of impeachment and the prospect of President Pence. Later in the week former FBI Director Robert Mueller was named as special counsel in relation to the Russia investigation. It is way too early to give a serious nod to the possibility of impeachment, but all of this political upheaval does reduce the chance of any of Trump’s initiatives getting passed.

As it was, the market recovered towards the end of the week and US equities were only down by 0.3%. International stocks were up 0.9%. Crude advanced by over 5%.

Bonds rallied as interest rates fell.

The spread between the 10 and 2-year treasury note fell to below 1% for the first time since October.

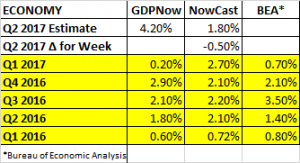

ECONOMY

The GDPNow forecast for Q2 growth increased by 1/2% to 4.1% and the Nowcast increased their growth estimate to 2.3% from 1.9%.

TECHNICAL CHART

The market still remains below the 2401 line we have been watching. It did go through it on Monday and Tuesday, but could not hold the gains.

In this article, written by the legendary Ben Graham in the spring of 1960, Graham warns of the unusually high valuation metrics in the early months of 1960. The article is based on a talk he gave on December 17, 1959. Graham writes about the high multiples like p/e, and the article is somewhat similar to the valuation arguments you hear today. Graham warns that there might be danger ahead.

In the first nine months of 1960, the market declined by about 15%. But after that it rallied by 26% through the end of 1961. From there, equities entered a bear market through the end of June of 1962 falling 23% and down 17% from their high at the end of 1959. After that, the market would rally through 1965.

Before the bear market began, some stocks like Texas Instruments and Polaroid were trading at p/e ratios of 115 times. The bear market even included a “flash” crash on May 28, 1962 where many stocks dropped 5 to 10% within minutes. The Dow fell 5.7% on that day.

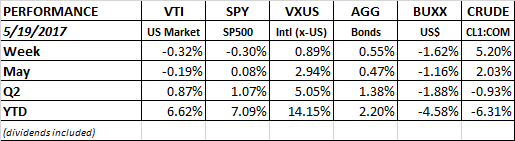

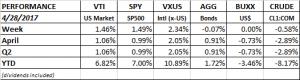

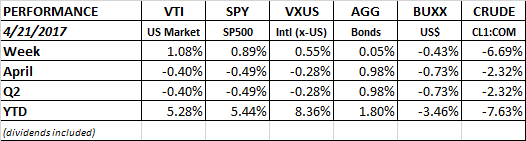

PERFORMANCE

The SP500 cracked through its all time high on Monday and Tuesday, but could not hold the gain and fell slightly through the end of the week. The index was down 0.3% while the NASDAQ managed a 0.1% gain.

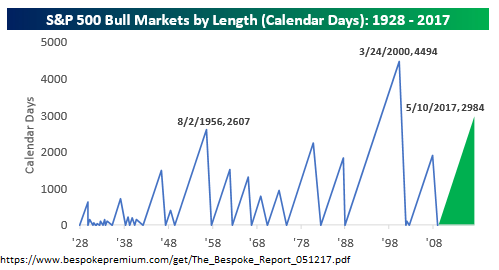

The US bull market is now 2,984 days old. That is the second longest bull run since 1928.

Treasury yields generally fell by a few basis points out to ten years on the treasury yield curve, helping move the bond index higher by 0.20%. The dollar and crude were also up.

Retailers fell hard. Macy’s dropped by 17% on Thursday and Nordstrom was 11% lower on Friday. On-line commerce continues to hammer away at the brick and mortar retailers. Retail overall has been ok. Sales were up 0.4% in April and on-line retail was up 1.4%. Year over year, retail sales were up 4.7%.

The earnings story for the S&P 500 is positive. Q1 earnings might rise 14% year over year.

International equities were just above break even for the week.

TRUMP FIRES COMEY

Trump fired FBI chief James Comey which brought back memories of Nixon’s dismissal of Watergate special prosecutor Archibald Cox in 1973, in an event that became known as the “Saturday Night Massacre.” That, along with some really bad economic policies such as price controls, set off several years of economic hardship that included 9% unemployment, 12% inflation, a 13% fed funds rate and a GDP measure that sank by 3.2%. The economy is much different now and appears in better shape, but the memories are somewhat eerie.

One thing that might not be so different is that the stocks driving much of the market advance were part of a select group. Then, it was the “Nifty 50”, considered stocks that you could buy and hold forever. Today, we have the FANG, and even more exclusive set.

OIL

Oil has fallen 15% this year but rallied 5% in the last six days. Inventory fell more than expected. The international energy agency said that supply and demand are beginning to come into balance, and that inventories might begin to decline if OPEC extends production cuts beyond May. The recent drop in crude might have flushed out the remaining oil bulls. This might be laying the ground work for an advance in oil prices.

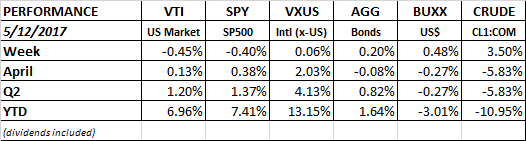

PERFORMANCE

The SP500 hit an all-time closing high on Friday, finishing at 2399.29. The index is now pushing up against its all-time intra-day high of 2400.98.

Overall US equities were up by about 0.60%. International equities continued to outpace US equities, +1.97%. Bonds fell as interest rates increased, the dollar was flat, and oil tumbled by over 6%. Volatility is ridiculously low, the VIX is at 10.97, close to a 10-year low. But investors are not overly optimistic. The AAII bullish sentiment is at 38.1%, less than the historical average of 38.5%. On the other hand, investors are also not pessimistic, the survey shows that bearish sentiment, expectations that prices will fall over the next six months, fell to 29.9%. The lowest reading since February 8.

GDP

The Atlanta Fed’s GDP model came out with their first estimate for Q2 growth on May 1 with a sizable increase over a weak Q1, projecting growth at 4.3%. That was revised down to 4.2% later in the week on light vehicle sales. The NY Fed’s Nowcast projects Q2 growth at 1.8%, down from 0.50% from last week on a weak ISM manufacturing report.

JOBS

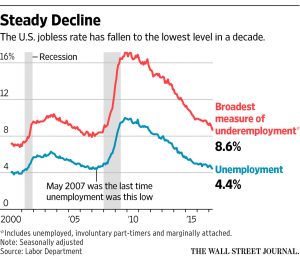

The unemployment rate fell to 4.4%, its lowest level since May of 2007. Non-farm payrolls increased by 211,000, a big improvement over the 79,000 increase in March. The hiring increase was broad-based but hospitality led the way adding 55,000 new jobs, 37,000 jobs were added in healthcare. Even retail managed to hire 6,000 new employees. The labor force participation rate remained low, at 62.9%, consistent with the past few years and just above a four-decade low. Average hourly earnings increased by 2.5% year over year, narrowly outpacing the 2.4% increase in the consumer price index.

FED

The Fed kept interest rates steady at their meeting this week. The Committee said that the slowdown in growth in Q1 “as likely transitory.” That means, at least for now, the Fed still considers itself on track for two more rate increase this year. There is a good possibility the Fed will raise rates in June.

OIL

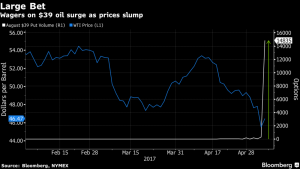

We said at our quarterly webinar that one risk to the market would be a collapse in oil prices. That was a contributing factor that led to the big market selloff at the beginning of 2016. Oil is down to about $46 per barrel from just north of $50 only a few weeks ago. Worries about weakening Chinese demand has hurt the pricing on all commodities. Options traders are starting to bet on fall below $40. The big spike in trades could be a sign of a peak in fear, and a contrarian would say this would be the time to get long for a recovery. But if oil continues to fall, especially if is breaks $40 to the downside, it might drag the market with it.

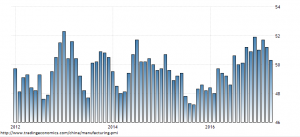

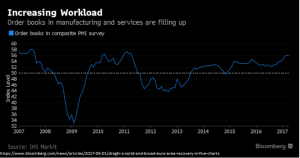

MANUFACTURING

In the US, the ISM Manufacturing Index fell by 2.4 points to 54.8, the biggest drop since August. The decline indicates a small slow-down in manufacturing activity, but still up from last year.

The Chinese Caixin Manufacturing PMI fell to 50.3 from 51.2. The reading was the weakest since September of 2016, although a reading above 50 still indicates expansion, although very slight. New export orders fell, there was weakening business confidence and employment fell the most since January.

PMI readings were much more positive in Europe.

Sweden 62.5

Spain 54.5

Switzerland 57.4

Italy 56.2

France 55.1

Germany 58.2

Overall, 87% of countries reported growth.

PERFORMANCE

The US equity markets turned in another solid week, gaining about 1.5%. International markets did even better, +2.34%. Bonds fell slightly, the dollar was even and crude was off boy 0.6%.

Very strong earnings are moving the markets higher. According to FactSet, as of Friday, the blended earnings growth rate is 12.5%, above the 9% estimate at the beginning of earnings season. This would be the first time since Q4 of 2011 when the SP500 companies reported a double digit earnings increase.

The market is still trading in a range of between 2280 and 2400, and it will have to crack the 2400 line (orange line above) to possibly begin another leg up.

TAX PLAN

Trump proposed an outline for an aggressive tax plan. He is leaving it up to Congress to fill in most of the details. The plan would cut tax rates on corporations from 35% to 15%. There would be a one-time “amnesty” rate of 10% to encourage repatriation of about $2 trillion in profits that US companies have been keeping overseas. The proposal to get those dollars back into the US is a good idea and both parties should support that. The plan also taxes only domestic profits, another smart proposal.

The tax cut would also apply to “pass-through” entities like Sub-S corporations. That would give the pass-through entities a big tax advantage over regular corporations since income on corporate profits is eventually taxed two times, while a pass-through is taxed one time.

A corporation is taxed on its income, and then its shareholders are taxed at some future point on dividends and taxable gains. The tax proposal calls for a 15% corporate tax and a 20% dividend/capital gains tax. For $100 of income, the corporation will pay $15 in tax. That would leave $85 in the business. Let’s assume that $85 is paid out as a dividend, it will get taxed on the personal level at 20%, resulting in another $17 in tax for a net of $68. Meanwhile, the same pass-through entity investor would net $85.

One of the main ideas of reforming the tax system is making it equitable and easy to understand. The pass-through advantage does not do that. That needs to be corrected.

The other huge issue is that the plan would result in trillions in lost revenue. Of course, the argument is that the economy would grow faster, and that would eventually result in most of the lost revenue being recovered. The proposed cuts are too deep and too risky given the country’s fiscal situation.

In sum, the plan won’t pass as proposed but it is a starting point.

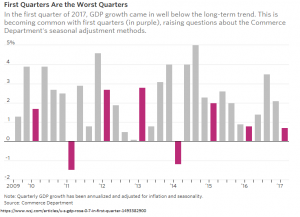

GDP

The Commerce Department reported that GDP growth in Q1 was 0.70%, the lowest reading in three years, and not a good start to the Trump era. This is the initial reading and it will be revised down the line, but it continues the string of weak Q1 growth that we have seen over the past several years.

Trump has promised to get growth to 3% plus. That is a tall order. But Q2 growth is expected to improve. The NY Fed’s NowCast currently has Q2 growth estimated at 2.3%, plus 0.20% on the week on positive news on manufacturing and housing data.

On a positive note, wages grew at the fastest rate since Q1 of 2007.

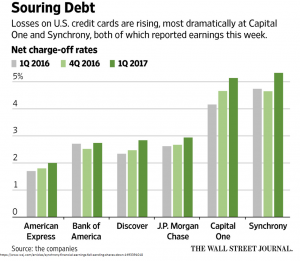

CONSUMER DEBT

We spoke about this at our quarterly webinar (click to view), trends in consumer debt are turning negative. Credit card lenders are reporting more losses. This is probably the result of leaner credit standards and overspending by consumers. The subprime market is where the hits are being taken and the threat is if there is a spillover effect.

NORTH KOREA

The market has been ignoring North Korea but the heat is rising. Secretary of State Rex Tillerson addressed the U.N. on the need to step up pressure on North Korea. A U.S. nuclear submarine has arrived at a South Korean port. On Saturday, North Korea launched conducted another missile test. Like the one prior, it failed. Trump would not rule out the use of military force in an interview on “Face the Nation” on Saturday.

GOLD

One investment that might benefit from a major geopolitical event like North Korea would be gold. The Gold Miners ETF (GDX) is off 8.2% from its recent peak in mid-April.

PERFORMANCE

The US equity markets advanced by about 1%, and in the process, at least for now, broke the recent downtrend. International equities were up 0.55%, bonds were about even, the dollar declined and crude fell by 6.7%.

This week will start on a positive note as France’s pro-growth candidate Emmanuel Macron finished first in the Sunday election and advances to the runoff with nationalist Marine Le Pen. Macron is favored and a win will keep the Eurozone intact.

The market has been advancing in a stair step fashion. It trades in a sideways manner, breaks out, then enters another consolidation phase, and then breaks higher again. That might be continuing.

Earnings appear to be on target for an approximate year over year increase of about 11%. Excluding energy, about 7.5%. Improving earnings will work down some of the excess valuation in the traditional ratios like price to earnings, price to sales and price to book.

GOVERNMENT FUNDING

Trump just complicated the process of keeping the government operating. The government runs out of money on Saturday and a deal must be passed to keep the US in business. Trump is now demanding that the legislation include funds for a border wall with Mexico. That is a deal-breaker with the Democrats and will make it more difficult to avoid a government shutdown next weekend.

ECONOMY

Initial jobless claims came in at 244k, a low number. Existing home sales were up 5.7% year over year. Industrial production rose by 1/2% month over month. The flash PMI composite estimate fell to 52.7 from 53.2 That is down but still above 50, indicating growth.

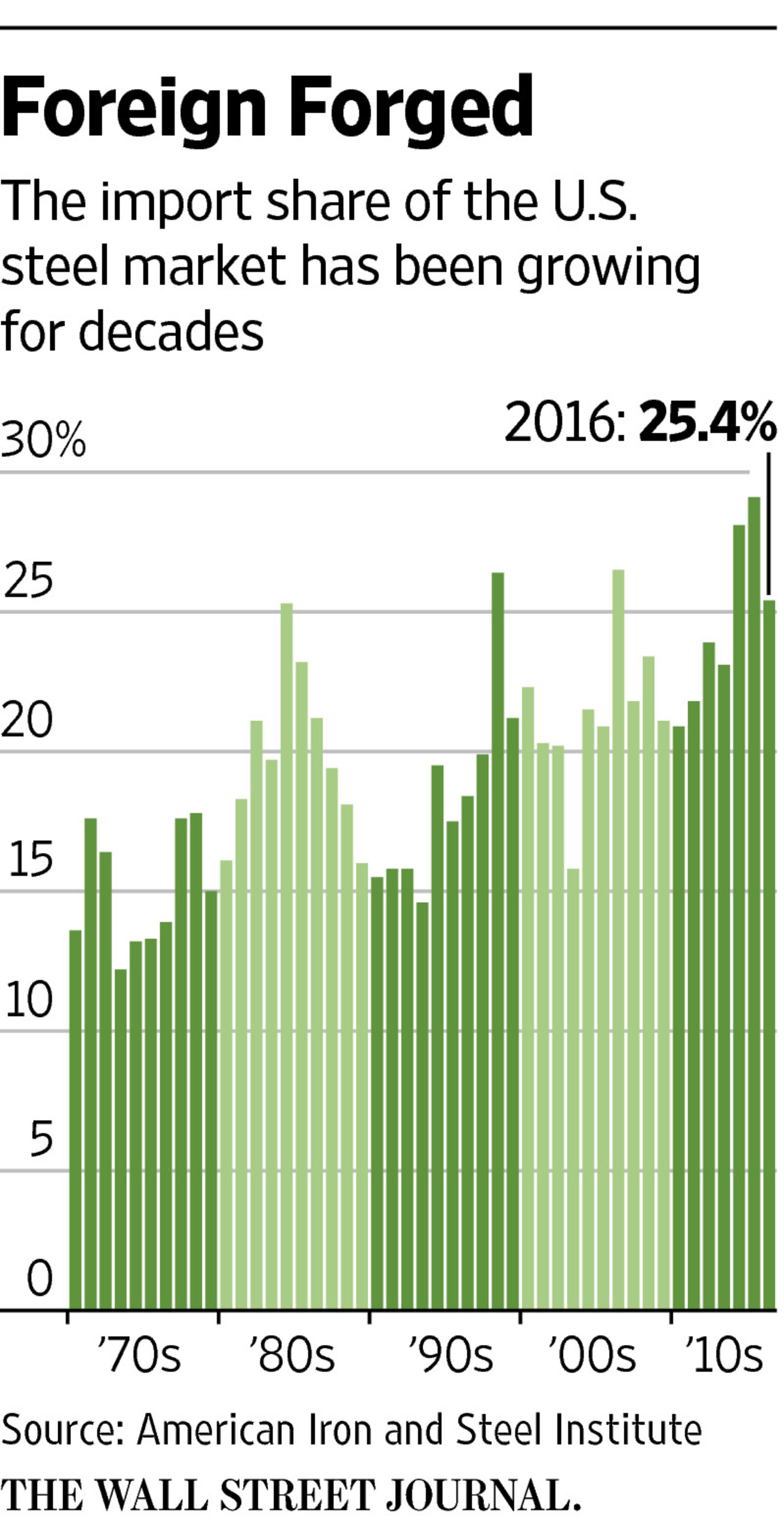

STEEL IMPORTS

The Trump administration announced that it is opening up a probe into steel imports, indicating that national security might require a cut in imports. The trade law cited to justify the cut in imports requires a study that will be submitted to the Commerce Department that assesses the legitimacy of the national-security claim.

It is one thing to retaliate against a company that is “dumping” product with the help of government subsidies, it is another to implement across the board cuts that impacts even those that compete fairly. Such an across the board cut would possibly result in retaliation against other US manufacturers.

Cutting imports would allow US manufacturers to increase steel prices even further. Manufacturers ramped up prices last year after the government imposed duties on imports from some companies in China and elsewhere. US steel prices are already among the most expensive in the world and impact a wide range of businesses that are the consumers of steel. There are about 60 workers in steel using industries for every steelworker in the US. A mismatch which shows that such an across the board cut might not past a true cost/benefit test.

TAX PLAN

Trump officials plan to release a tax overhaul plan soon. The plan would concentrate on business first (corporate and pass-through entities) and leave individual tax reform for after.

These articles explain the concept of positive skew and how it makes beating a benchmark so difficult.

Why indexing beats stock picking.

Do stocks out perform treasury bills?