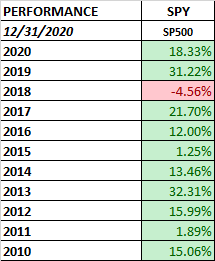

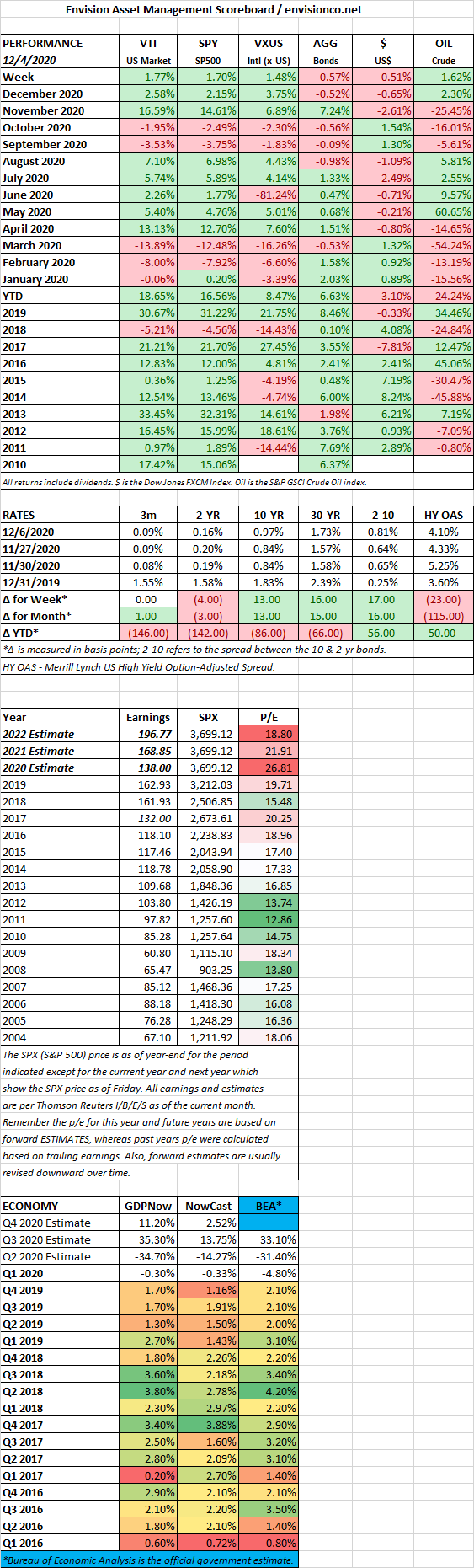

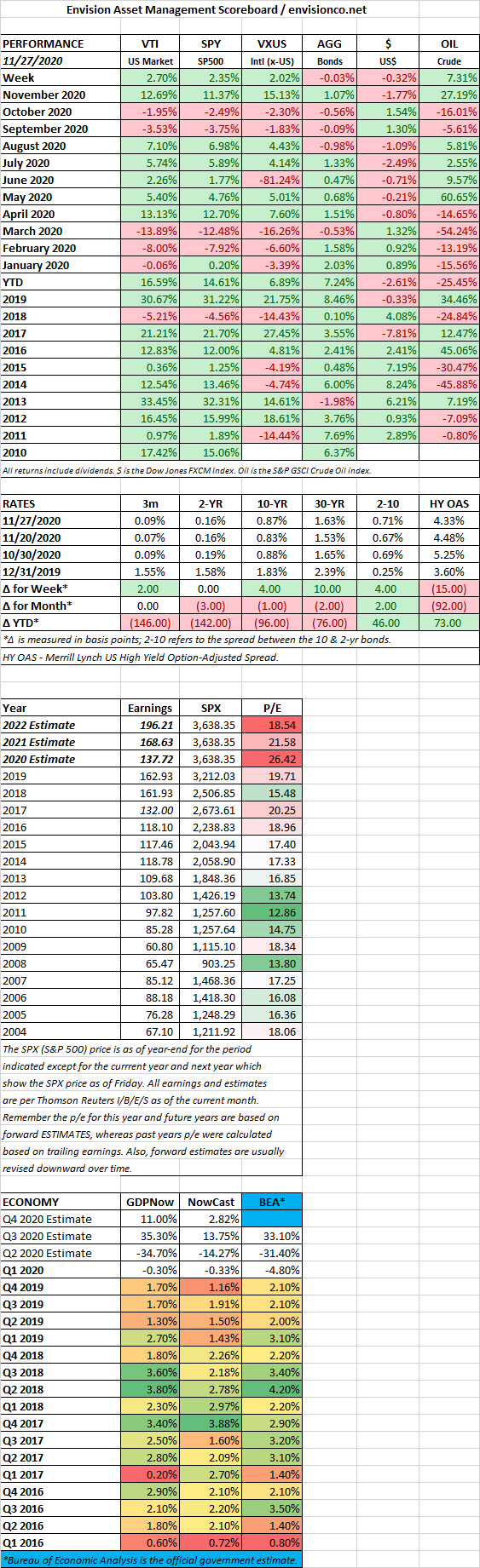

Scoreboard

Scoreboard

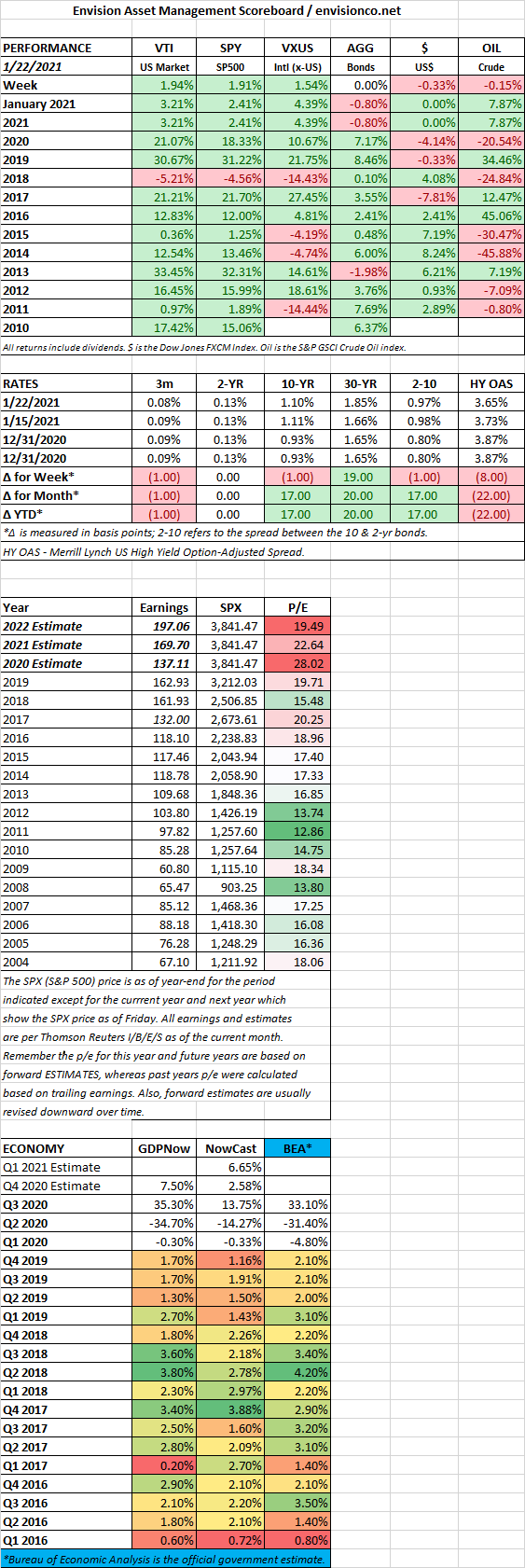

MARKET RECAP

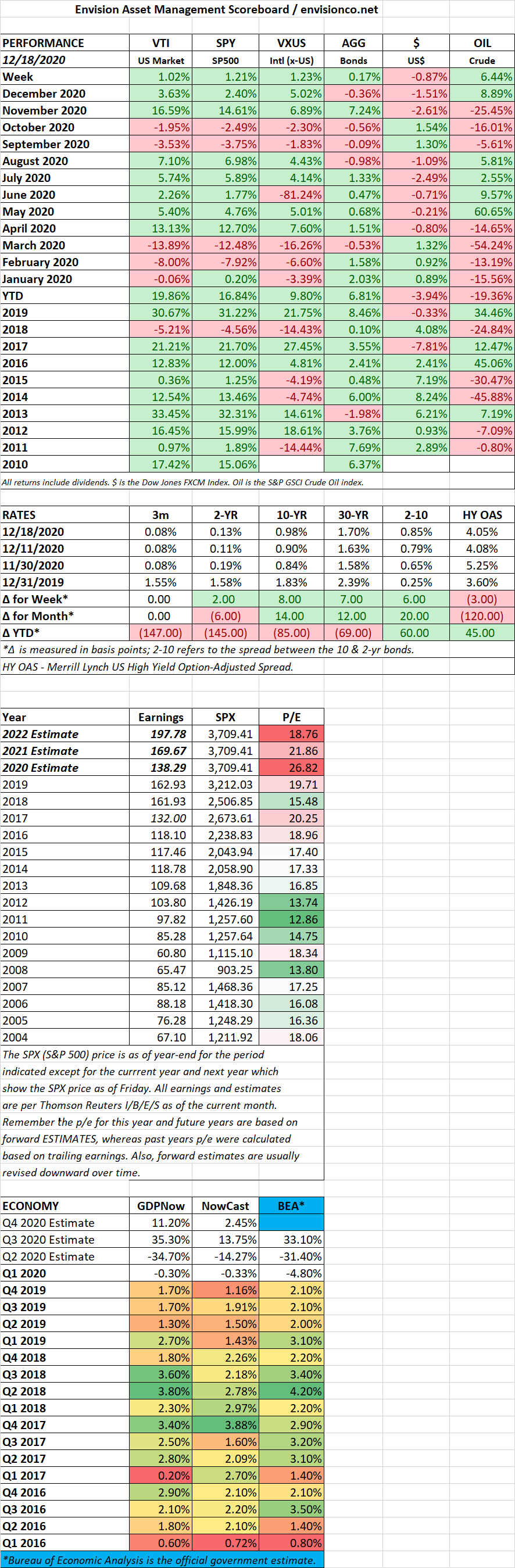

Stocks went up, what else is new, by 2.37% in the US and 4.36% outside the US. But that was not the big news this week, not close. In one of the saddest displays in US history, a Trump-inspired mob invaded/attacked the halls of Congress while the Senate was conducting its ceremonial duties of making the electoral college vote official. The proud US tradition of a peaceful turnover of power was briefly interrupted, and if Trump’s previous actions did not warrant it, his reputation will certainly be ruined forever by this act and deservedly so. We wrote back on September 25th that Trump would not commit to a peaceful transfer of power and that this was “another reason why he is unfit to be President.” He definitely deserves to be removed from office via the 25th amendment or impeached, although this is unlikely to happen with just days remaining in his term.

Trump’s actions earlier in the week probably cost the Republicans the US Senate. The two Georgia Senate seats went to the Democrats by narrow margins. Earlier in the week Trump was recorded asking Georgia officials to find another 11,000 votes so that he could suddenly and retroactively win Georgia. The Georgia officials would have none of it and made it clear it was a fair vote, both the Presidential contest and the Senate runoffs. However, Trump trying to fix the election, the very thing he has falsely accused the Democrats of, probably cost the Republicans the necessary margin to win one or both seats.

So now the Senate is 50-50, with Kamela Harris giving the Democrats the edge. Hopefully, the small 51-50 advantage will be enough to keep Biden’s policies more towards the center-left than the extreme left. Biden has already indicated he is going to go for lots of fiscal stimulus, thereby throwing the country deeper into debt. As they say, a trillion here, a trillion there, and soon you are talking about real money!

Well, real money it is, although the value of that real money is declining at a fast clip. The dollar is down 9.53% since March.

In fact, there is so much money around, that the market just goes up every day no matter what happens. When it looks like the Republicans will win the Senate, the market is up. Nope, the Democrats won, ok, that is a reason for the market to go up. Employments numbers go up, we get a higher market. Employment numbers down, which means more stimulus, the market goes up. A violent mob overtakes the Capital, no problem, stocks just continue to rise. If this isn’t stock market euphoria then what is? It just feels like the market will go up every day, which of course, is often when the market is most dangerous. But practically speaking, this can go on for much longer or it can end tomorrow, but every day the market rises futures returns are declining.

The stimulus that was just passed has not even fully been distributed yet. Applications for the PPP portion are not even available yet. And then you will have a second tidal wave of money with Biden’s new fiscal stimulus. So if the past is an indication of the future, equities will have plenty of fuel behind them.

Somewhat of an offset to an even higher stock market could be rising interest rates, higher taxes especially in the corporate sector, increased regulation, and the economy itself. When corporate tax rates were cut at the beginning of the Trump turn, stocks rallied as suddenly every dollar of revenue generated was suddenly worth a substantial amount more. And while Biden probably won’t increase taxes on corporations all the way back, whatever he does increase is coming right off the bottom line. That immediately raises p/e ratios unless prices adjust down. And then deregulation over the last few years has had a substantial impact on improving the fortunes of business. That now goes into reverse. And finally, the economy is slowing. The US lost 140,000 jobs in December, the first decline since April.

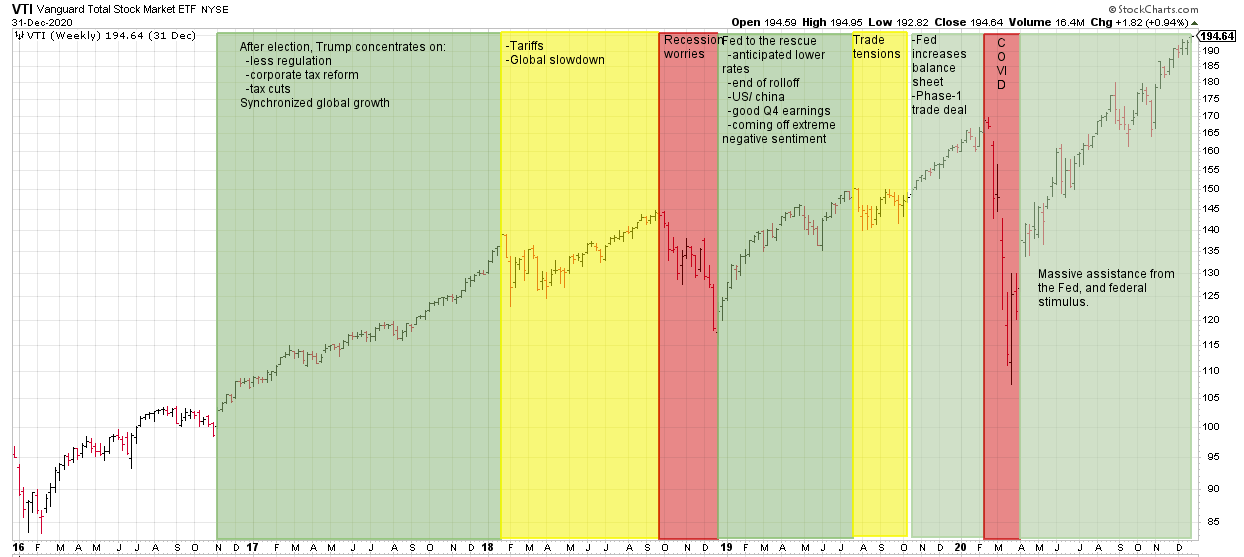

International markets seem to be overtaking the US recently in terms of equity performance. In the chart below, which compares the overall US stock market (VTI) versus outside the US (VXUS) when the solid black line is rising, the US is outperforming, and when falling, international is performing better. Over the last few months, the US seems to have topped in terms of relative strength and in recent weeks international stocks have outperformed. This might be reversing years of US outperformance.

Interest rates rose sharply during the week as the Democrats swept Georgia. The yield on the 10-year was up by 20 basis points.

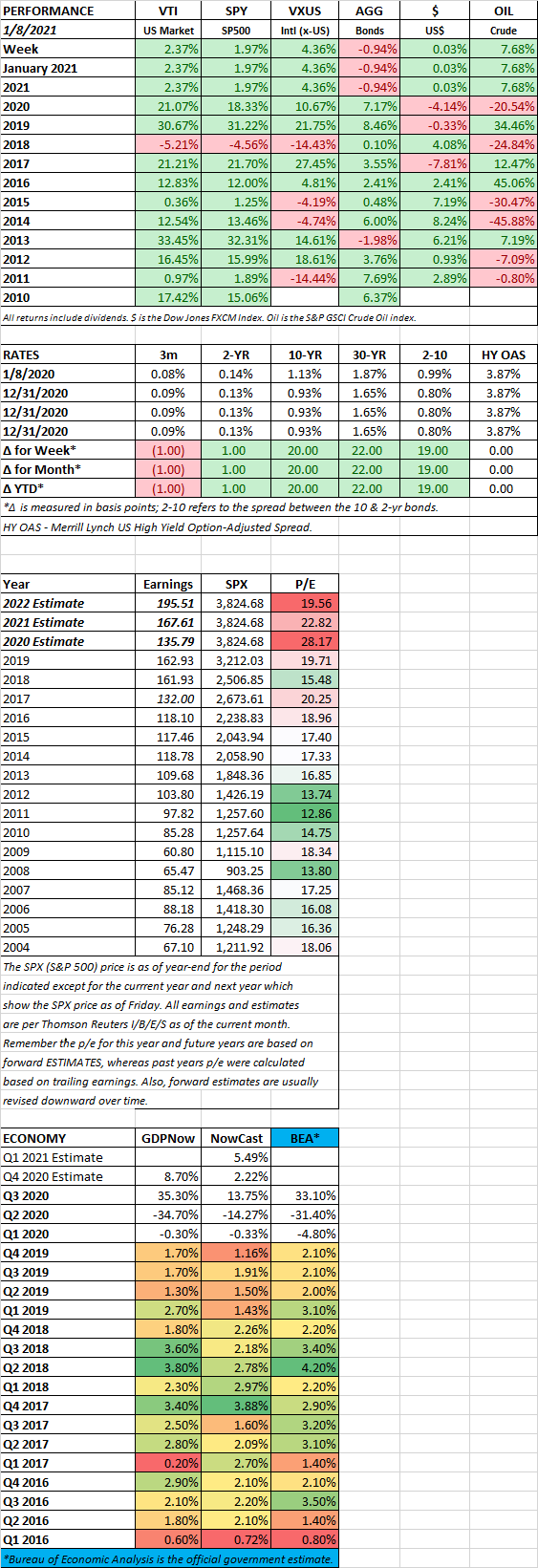

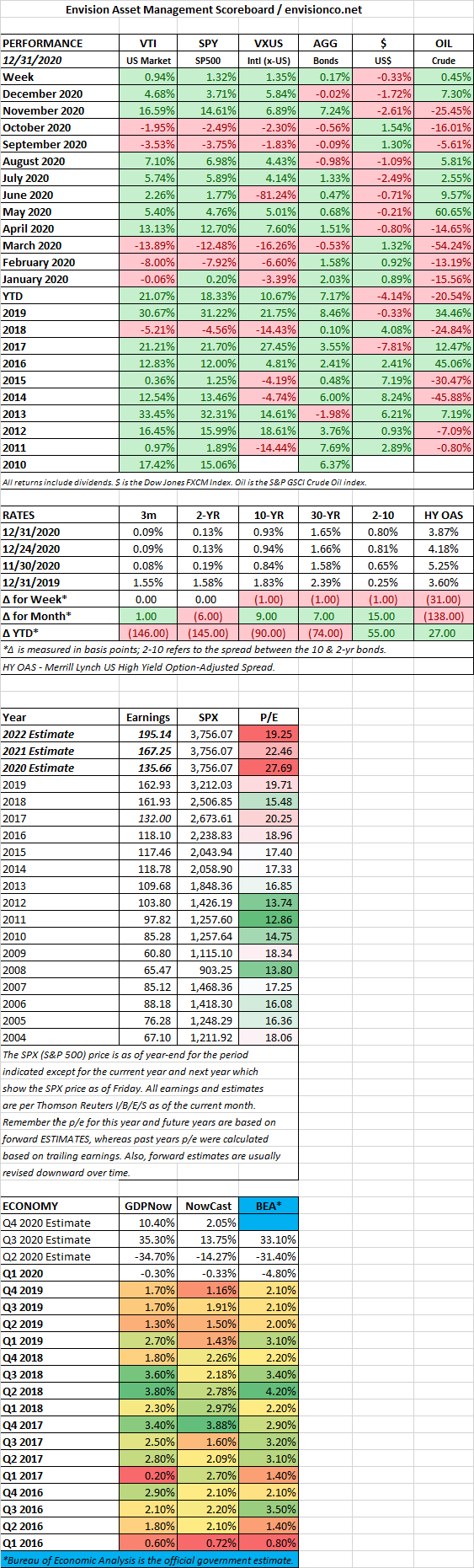

SCOREBOARD

MARKET RECAP

You can make a good case that the only good thing in 2020 was the stock market, that, and the triumph in science in quickly creating a vaccine. In a year marked by a global pandemic, a literal stop to the entire US economy, stocks turned in an amazing performance. The S&P 500 was up by 18.33% for the year. International stocks advanced by 10.67%. Massive government intervention, on a scale never seen before and in dollars never imagined, including dropping interest rates to nothing, powered equities here in the US and worldwide.

A lot of the gains in the index were powered by the technology leaders like Apple (+82%), Amazon (+76%), and Netflix (+67%). When looking at the S&P 500 and calculating on an equal-weight basis, the market was up by 12%, still very impressive.

US stocks have now been up ten times in the last eleven years and have put in double-digit gains two years in a row.

Needless to say, on an absolute basis, ignoring low-interest rates which might provide justification, valuations are high. The hoped-for and long-anticipated recovery is going to have to shift into high gear to catch up to current valuations.

Looking forward at 2021 earnings estimates, stocks sell at a price-earnings ratio of 22.46. That is high. The median stock in the Morningstar coverage universe now sells at 109% of fair value, which is the second-highest amount going back to 2007. But as we said above, with interest rates at incredibly low rates, there is some justification for elevated valuations based on traditional metrics.

There are signs of euphoria in the market. IPOs that soar to ridiculous heights (DASH and ABNB), Tesla up by 743%, Bitcoin is at $31,882, up by 354% since August. SPACs (special purpose acquisition companies) or blank-check companies proliferated in 2020, there were 248 that went public last year. Here you have investors buying in on the hope that the SPAC can find something worthwhile to purchase. You are not buying an income-producing or revenue earning business, just a hope that your SPAC can find one.

As far as the economy, the US continues on the rebound path but has slowed of late due to the surging virus. Vaccines by Moderna and Pfizer are slowly being rolled out, and everyone in the US should be able to receive a vaccine by September if they want one. With or without the vaccine, the growth of the virus should begin to taper down within a few months, at least based on past pandemics.

Retail sales were up by 2.4% between November 1 and December 24 compared to the same period a year prior. Online sales soared by 47.2%. The National Retail Federation had been expecting an increase of at least 3.6%. There were winners and losers. Department store sales fell by 10.2% while furniture was up by 16.2% and home improvement by 14.1%.

Between trade issues with China, and Covid, companies have been evaluating their supply chains. Some businesses are considering bringing factories closer to home, others spreading out factories around the world so they don’t have to rely on just one facility. In either case, the net result is going to be less efficient supply-chains, which would be a contributing factor to higher inflation down the road.

High inflation down the road, from a declining dollar, from the government dropping money everywhere, from less efficient businesses, wherever it might come from, represents a threat. That would mean higher interest rates in a world where the US deficit has simply grown way out of control. Or, if the Fed suppresses interest rates, the possibility of runaway inflation and a plunging dollar. Counterbalancing higher inflation is a population that is getting older, that will save more than it spends, and improved productivity from better technology.

In the meantime, the market continues to move higher. That can change on a dime, but momentum is currently positive.

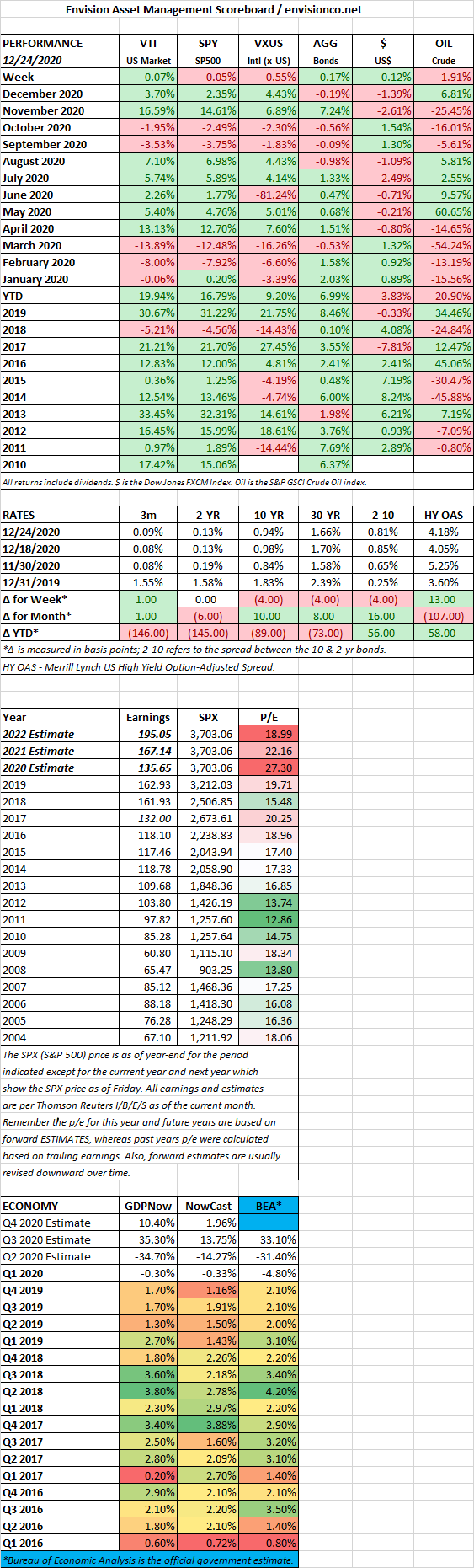

SCOREBOARD

MARKET RECAP

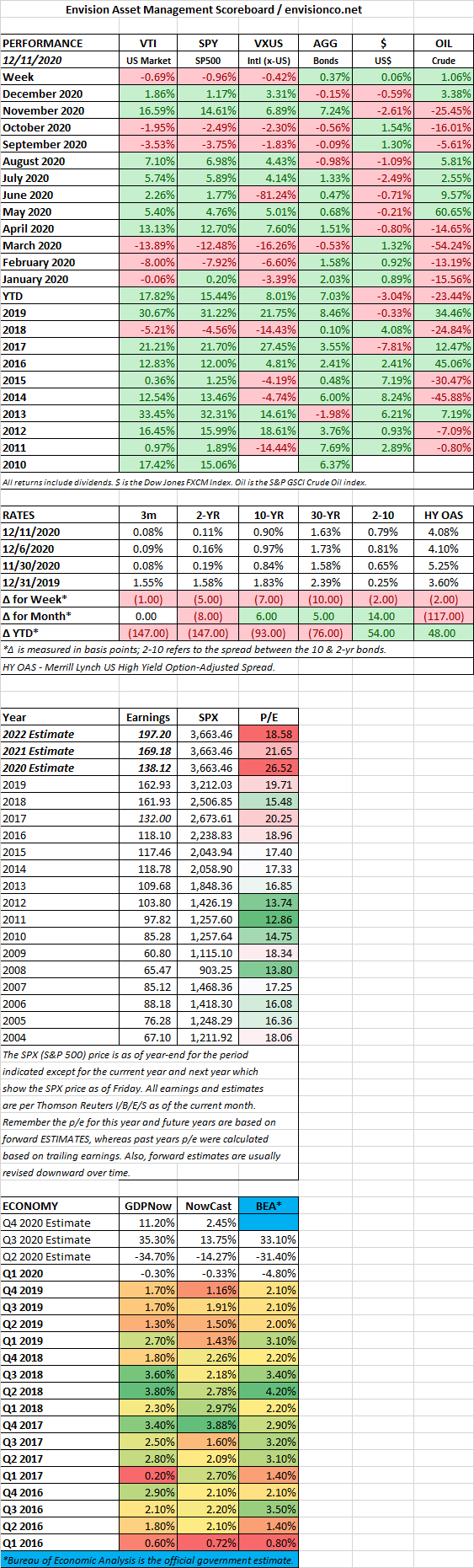

Stocks were basically flat in the US and down 0.55% outside the US. The action has been in small stocks, which are at a record and are up by 25% since November 5.

After months of negotiation and congressional approval, Trump suddenly decided he didn’t like the stimulus bill, but the market wasn’t disappointed, figuring congress will now come back with an even bigger package. Trump wants $2,000 in direct payments instead of $600. In a world where debt doesn’t seem to matter, why not (according to Trump)?

Household spending fell in November for the first time in seven months, down 0.4%, more evidence that the virus is taking its toll. Household income dropped by 1.1%, the third decline in four months. Consumer confidence is falling, down by 4.3 points, according to the Conference Board. However, income is up 2% since February, and savings rates are at historically high levels. So whenever the virus gets under control, there is the possibility of pent-up demand will increase economic activity. The Atlanta Fed’s GDPNow model is projecting Q4 growth at an annualized rate of 10.4%.

After four years the finishing touches are being put on a Brexit deal that would govern trade, totaling almost $900 billion, between Britain and the EU. The deal, for the most part, would allow tariff-free trade between the two sides and reduce paperwork at the border. It would also allow Britain to sign free trade deals with other nations.

SCOREBOARD

MARKET RECAPS

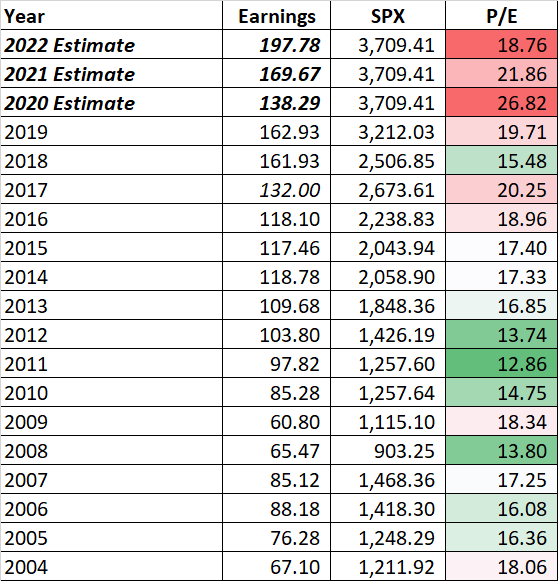

US stocks were up by 1.02% and international stocks by 1.23%. As the market continues marching higher, signs of excessive optimism are all around. A recent Bank of America survey of professional money managers are underweight cash for the first time since May of 2013, holding only 4%. Individual investors are piling into speculative stocks with outsized best on call options. Bitcoin has broken out to new highs, now over $20,000. Value Line, a long-time investment research firm, calculates an 18-month target price range for the companies that it follows, the projection for the average stock is now 4%, the lowest number ever. At one point this year, when stocks were at their low, it was 72%. Speculation is running high in the IPO market. In this week’s Barron’s 2021 Outlook article, experts say stocks will gain 10% next year. More government stimulus and a faster-growing economy will provide the fuel for higher equity prices. The consensus is for the fastest economic growth in the US since 1984, +5%, and S&P earnings of about $170.

At a news conference this week, Fed Chair Jerome Powell did say that price/earnings ratios were on the high side but said that the equity risk premium was reasonable given low Treasury yields. Right now, the forward p/e based on 2021 earnings would be the highest p/e ratio since at least 2004 (see below). The problem is what happens when yields begin to rise. That may be a long way off, or maybe not, if the vaccine puts an end to the crisis and consumer spending explodes, setting off inflation, forcing rates higher, which would require a reset to lower p/e ratios.

Growth on the virus stalled out for a couple of weeks pre-Thanksgiving, but as the experts predicted, the holiday put in motion another huge surge in cases. The Pfizer vaccine began its initial rollout this week, and the Moderna vaccine was approved on Friday. So, as the vaccines slowly rollout, the economy is getting closer to a return to something close to normal.

The surging virus is cutting into economic activity. Retail sales were down by a seasonally adjusted 1.1% in November from October, and October was revised down from +0.3% to -0.1%. Restaurants, department stores, and car dealerships were all down while groceries and building materials were higher. First-time unemployment claims were 885,000 last week, the highest level since September.

The electoral college declared Joe Biden the next president of the United States. Trump’s lawsuits challenging the election were all dismal failures. Congress still has not agreed on a relief plan, the two sticking points are aid to state and local governments, and business liability protection.

A recent ruling in a US District Court is sending shivers through the leveraged buyout industry. Judge Jed S. Rakoff ruled that creditors of retailer Nine West can file a lawsuit for $2 billion in damages against the company’s board of directors. The ruling stated that the board acted “recklessly by failing to adequately assess an LBO-buyers post-transaction solvency.” Brian Quinn, a corporate law professor at Boston College says “It could be a game stopper for the private equity business.” Basically, the Board sold off important Nine West brands leaving the remaining entity as a much weaker unit, with too much debt, which led to bankruptcy. Because of that, they are now liable. The ruling can be overturned on appeal, but for now, this can impact private equity going forward.

SCOREBOARD

MARKET RECAP

Stocks were down by 0.69% in the US and 0.42% outside the US. Stimulus talks, which are on a constant stop and go, were in stop mode most of the week so that hurt stocks. Plus, the virus has been ramping up significantly since Thanksgiving and that is raising concerns of more restrictions on economic activity. As an example, indoor dining in New York was halted.

Despite the slight decline in the overall US market, the IPO’s were flying high, bringING back memories of 1999. DoorDash was up 86% and Airbnb 113% on their first day of trading.

Another sign signaling overvaluation, US investment-grade corporate bonds now yield less expected inflation. As of last Friday, the expected inflation rate over the next decade was measured at 1.89% (the difference between nominal and inflation-adjusted yields on 10-year US bonds), greater than the 1.85% yield on investment-grade corporates. This is the first time that has happened and it is mainly driven by negative real yields on US Treasury’s pushing investors up the risk scale, such as into these bonds, thereby pushing their yields down.

The European Central Bank ramped up its bond-buying program by more than a third and will introduce new low-cost loans for banks, in an effort to help governments and businesses as they fight through the current tidal wave of the virus. With this effort, the ECB has now poured in $3.62 trillion into the eurozone economy.

Unemployment claims jumped significantly higher, up by 137,000 to 853,000, last week. Consumer spending was up in October for the sixth straight month, according to the Commerce Department. And the Institue for Supply Management reported that the manufacturing and services sectors expanded in November.

The government reported a record deficit for the first two months of the fiscal year, up 25% from last year to $429 billion. Federal spending was up by 9% while revenue was down by 3%.

Net worth of U.S. households hit a record, a Federal Reserve report showed. Most of the benefit has gone to wealthier Americans who are invested in equities.

SCOREBOARD

MARKET RECAP

Stocks advanced again last week, with US markets up by 1.77% followed by international markets at 1.48%. For November, stocks rallied 16.59%. It was the best November since 1928. Bonds declined by 0.57% for the week as the yield on the 10-year Treasury rose by 13 basis points.

91% of S&P 500 companies are trading about their 200-day moving average, the highest percentage since July of 2013.

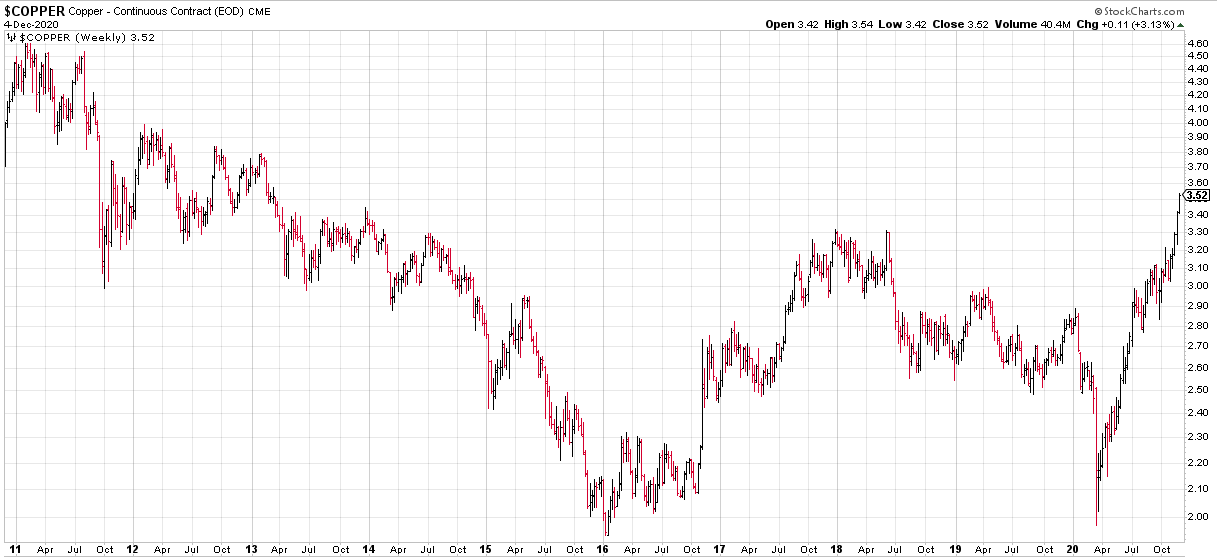

Super-low interest rates and hopes for a spectacular recovery are fueling the rally. Industrial metals are anticipating a surge in activity, copper is at a seven-year high, and the other industrial metals are all way up in price.

But the anticipated slow-down in the labor market that we have written about in the last couple of months appears to be here. Non-farm payrolls were up by only 245,000 in November, down from 610,000 jobs in October. The unemployment rate did fall to 6.7%, but that was due to 400,000 people leaving the workforce. The weak report might spur Washington to move quicker on a stimulus plan. The latest proposal centers on a $900 billion stimulus package.

22 million jobs were lost at the beginning of the pandemic, and the US has regained 12 million of those. Government payrolls were down by 100,000 while hiring was up in transportation and warehousing, reflecting e-commerce, which has been the big beneficiary of the virus.

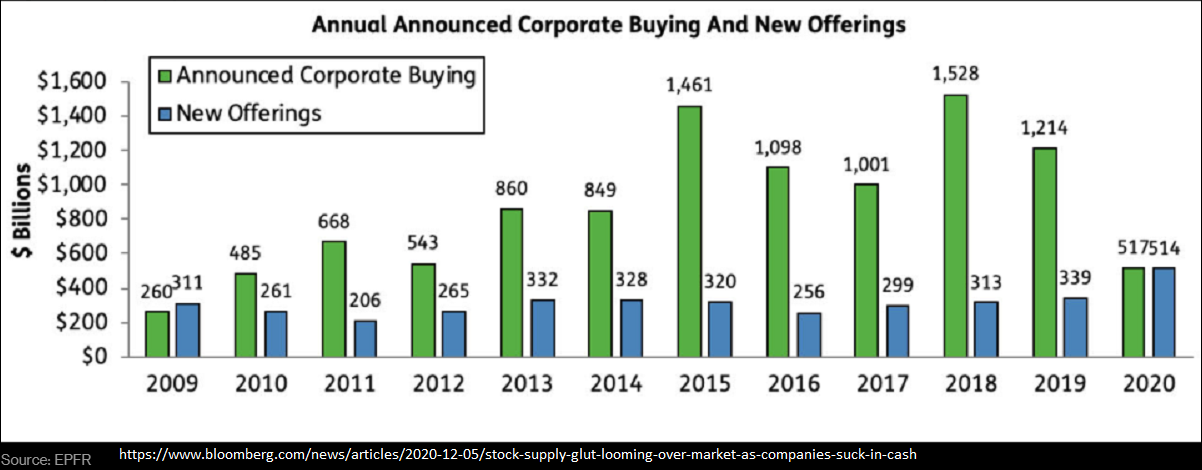

Over the last decade, equity taken out of the stock market, mainly via stock buybacks and takeovers, outpaced equities issues, via initial and secondary stock offerings, by a 3 to 1 ratio. But this year, the numbers have evened out. That makes the stock rally this year even more impressive, as stocks are up 18.65% without that tailwind. But it might be giving a message on valuation, with companies selling stock into the market to “sell high” and holding back on buybacks given high prices and valuations.

SCOREBOARD

HIGHLIGHTS

MARKET RECAP

The Dow broke the 30,000 barrier on Tuesday for the first time and is now up about 60% since the March low. In the last couple of weeks, positive vaccine news gave the market a possible end date on the pandemic, and Trump announced on Tuesday he would cooperate with Biden on the transition, those were enough reasons for investors to move stocks to the historic highs.

This is a market that can really do no wrong. It continues to move higher, counting on a booming recovery when the virus ends, while simply ignoring a virus that seems to be everywhere and its economic fallout.

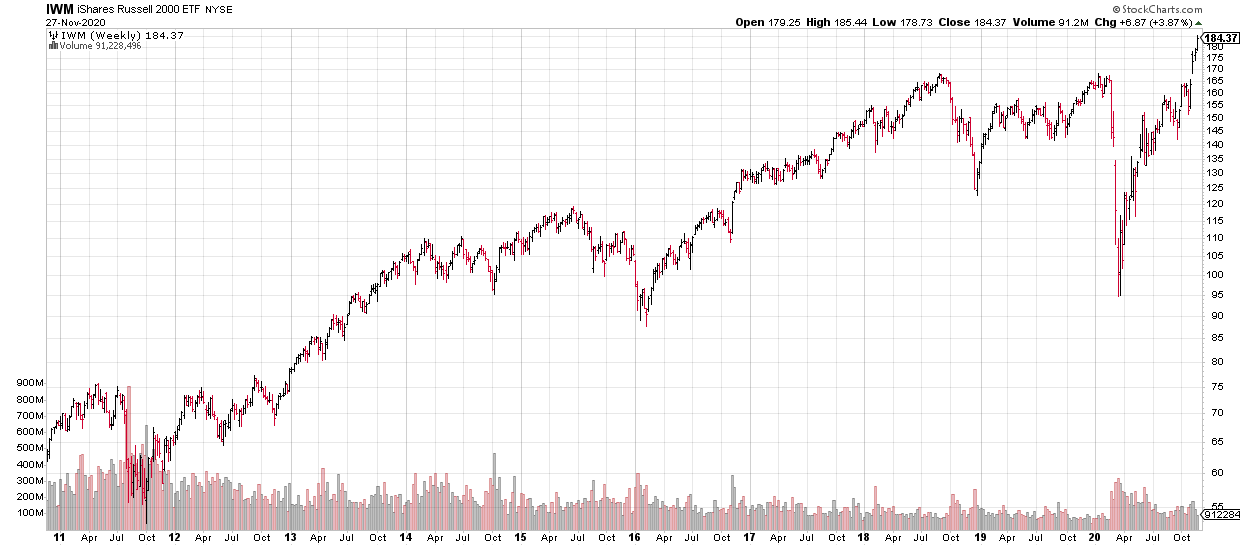

The rally has been broadening as more stocks are joining in. The Russell 2000 index small-cap companies reached a new record and international stocks are close to topping their 2018 peak.

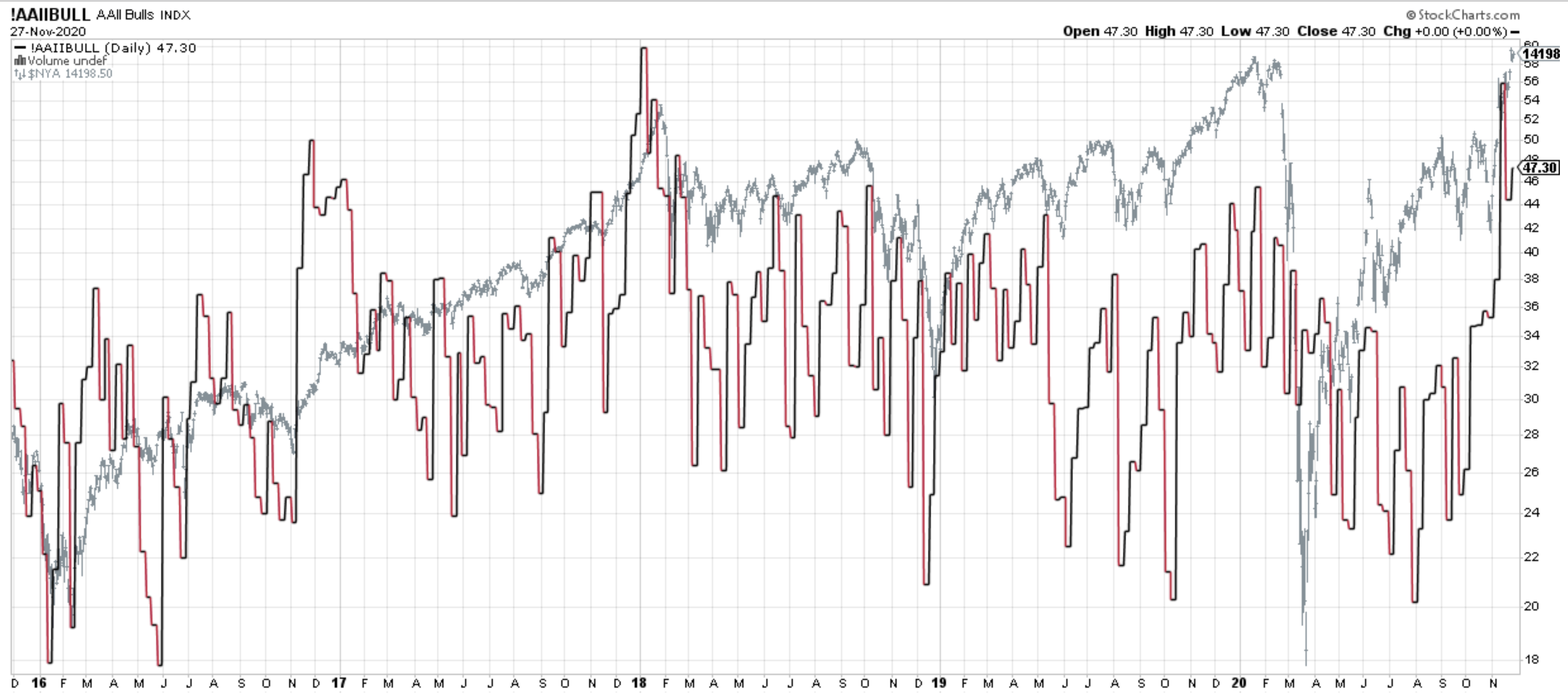

Bullish sentiment is everywhere, and in the past, that has sometimes been a precursor to either underperformance or a decline. The chart below shows bullish sentiment as measured by the AAII (American Association of Individual Investors) versus the S&P 500. Bullish sentiment hit very high levels two weeks back.

Likewise, CNN’s Fear and Greed Index came in at 92 this week, indicating extreme greed.

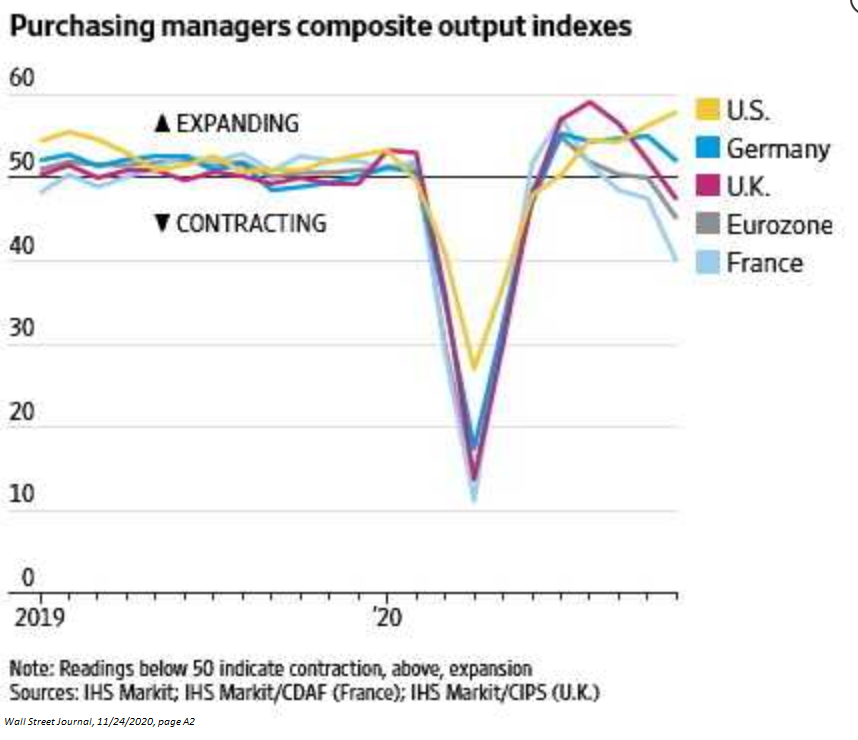

There is some good news in the economy, even in the face of rising virus numbers. The IHS Markit composite index of US business activity increased to 57.9 in November, up from 56.3 in October. The increase, which is a preliminary estimate, would be the fastest pace of growth since March of 2015 and represents a positive divergence from Europe, where their measure has been sinking.

But there is also more negative news. Jobless claims rose for the second week in a row, now at 778,000 from 758,000 last week.

As for the virus itself, the pace of growth seems to have slowed, but there is the threat of another ramp up coming off the Thanksgiving holiday.

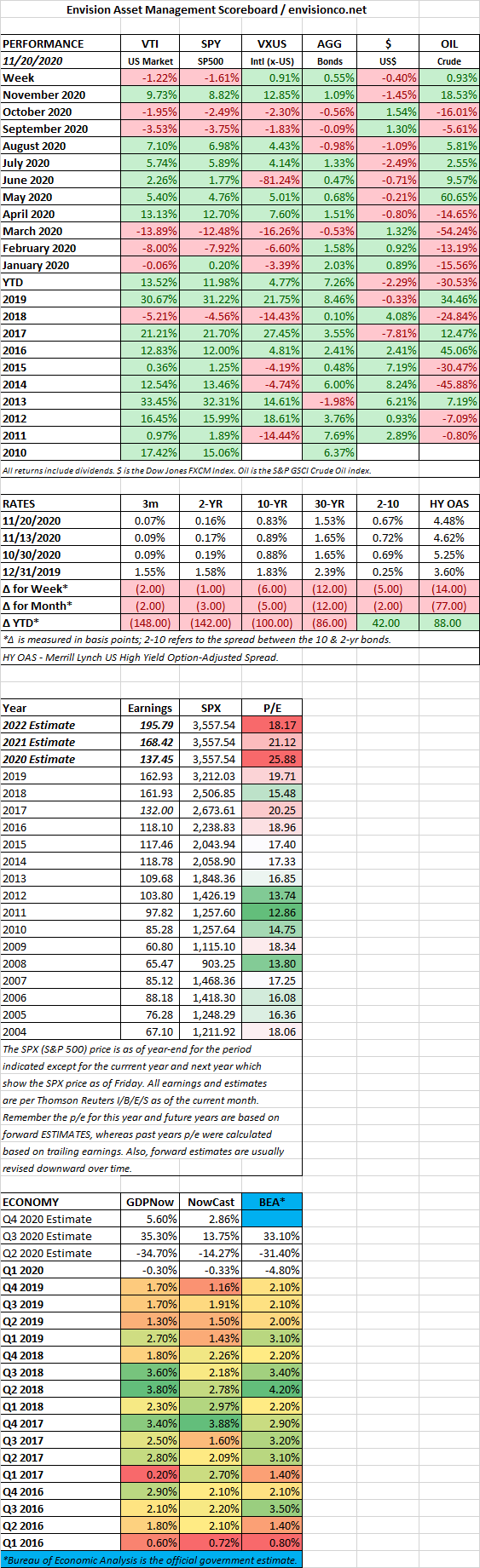

SCOREBOARD

MARKET RECAP

US stocks were down by 1.22% while international equities finished 0.91% higher. Good news from Moderna was offset when the Treasury Department announced it would not continue five special lending facilities, as well as a JP Morgan projection that it sees the economy contracting in Q1 of 2021. Fed Chair Jerome Powell said the next few months will be challenging and asked for more fiscal support, but that does not seem likely until the Biden administration takes power.

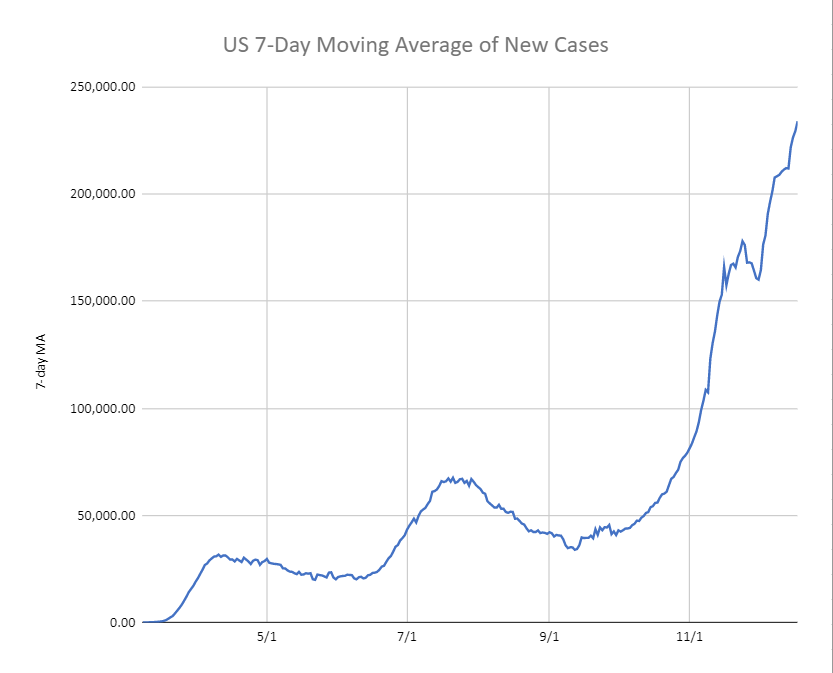

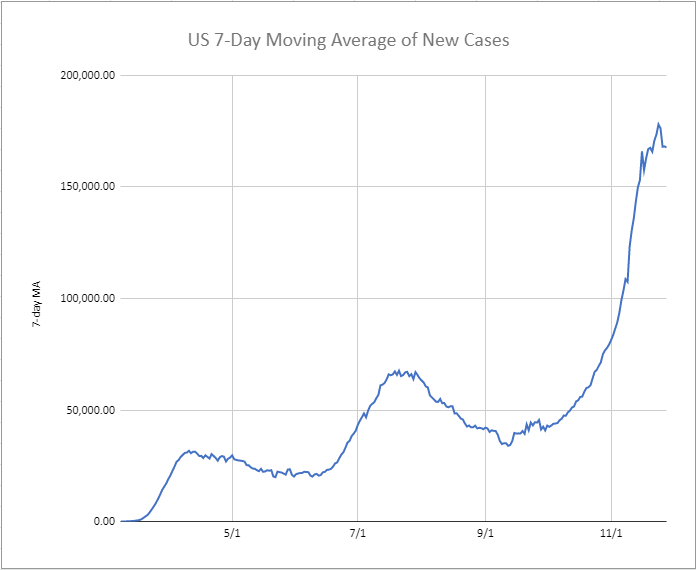

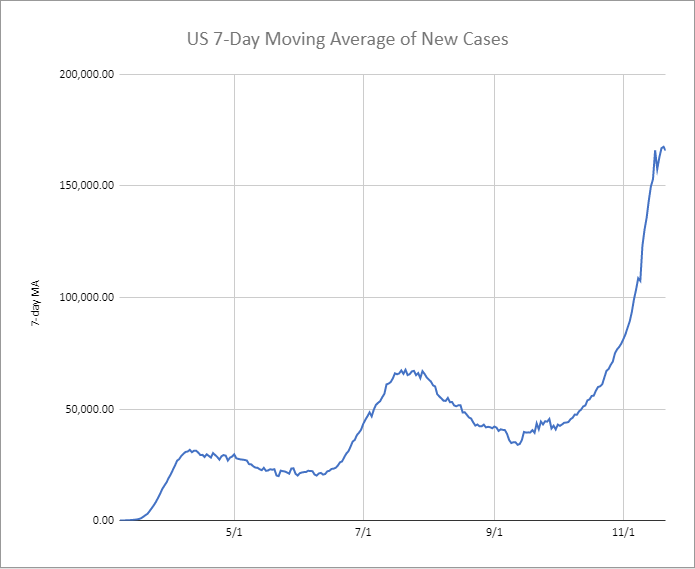

Following up on the Pfizer announcement from one week prior, Moderna announced on Monday that its Covid vaccine is 95% effective based on early trials. That is a huge win for science and puts a rough end date on the epidemic of 9-months to a year, but in the meantime, the virus is just exploding. Maybe, hopefully, the growth of the virus is beginning to slow in the USA, the 7-day moving average has stayed at about 165,000 for five days. Of course, it might just be a pause but the trend has been relentlessly higher since the beginning of October until now.

Home sales hit a 14-year high in October as sales increased for the fifth straight month. After years of disappointments, home sales have been the bright spot in the Covid economy, as ultra-low interest rates and a desire to get into individual homes have driven purchases.

October retail sales were disappointing, rising just 0.3% in October, lower than the 0.5% consensus estimate. Jobless claims increased by 32,000 last week. 742,000 were filed last week. More increases might be on the way as Boeing, Disney, and Exxon have recently announced job cuts.

Running out of legal options, Trump’s lawyers are making even more bizarre allegations, claiming the election was stolen via a massive conspiracy involving Democrats and foreign governments, including some help from Hugo Chavez who died in 2013! To date, there is no evidence of any kind of widespread fraud, and many of Trump’s lawyers have said they do not believe there was widespread fraud. Trump fired the official who was in charge of election integrity after he said there was no fraud. Jeffrey Engel, a presidential historian at Southern Methodist University said that other candidates have challenged election results in the past when there were clear and legitimate circumstances, but “all of them recognized that the unity of the country was more important.”

SCOREBOARD