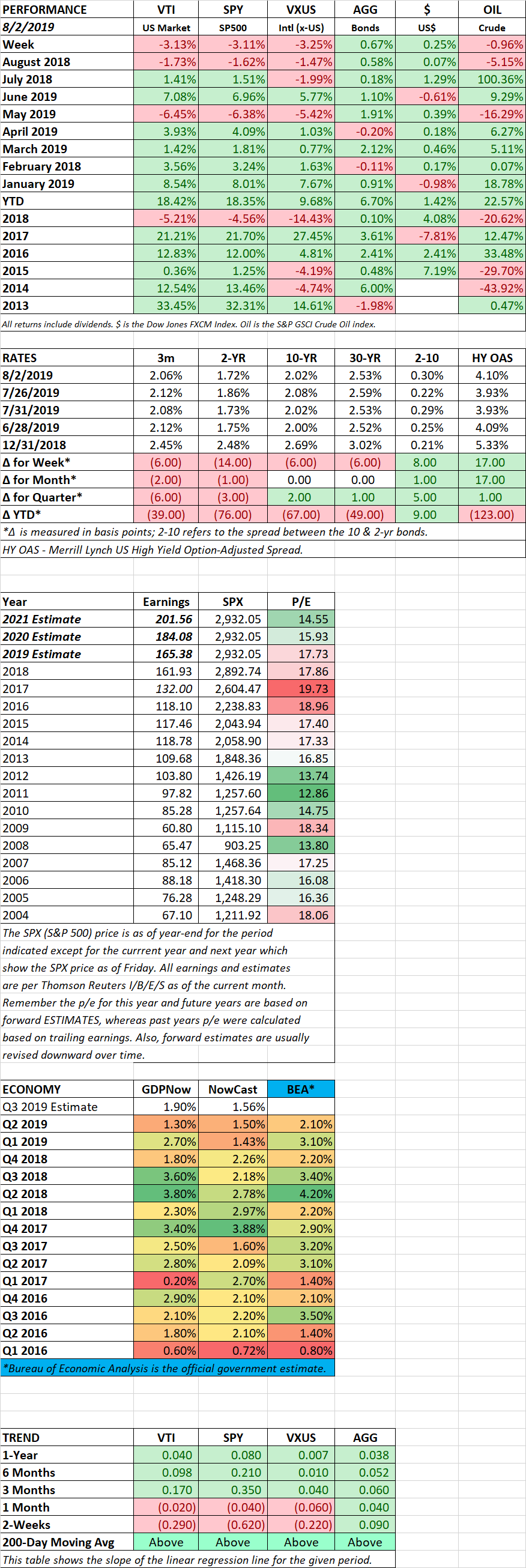

HIGHLIGHTS

- Stocks rally on word of a US-China meeting in October.

- Jobs are up but the pace is slowing.

- ISM falls into negative territory.

- Tariffs are cutting into US growth.

MARKET RECAP

US stocks rallied by 1.77% and international equities were up by 2.19%. Bonds were down by 0.18%.

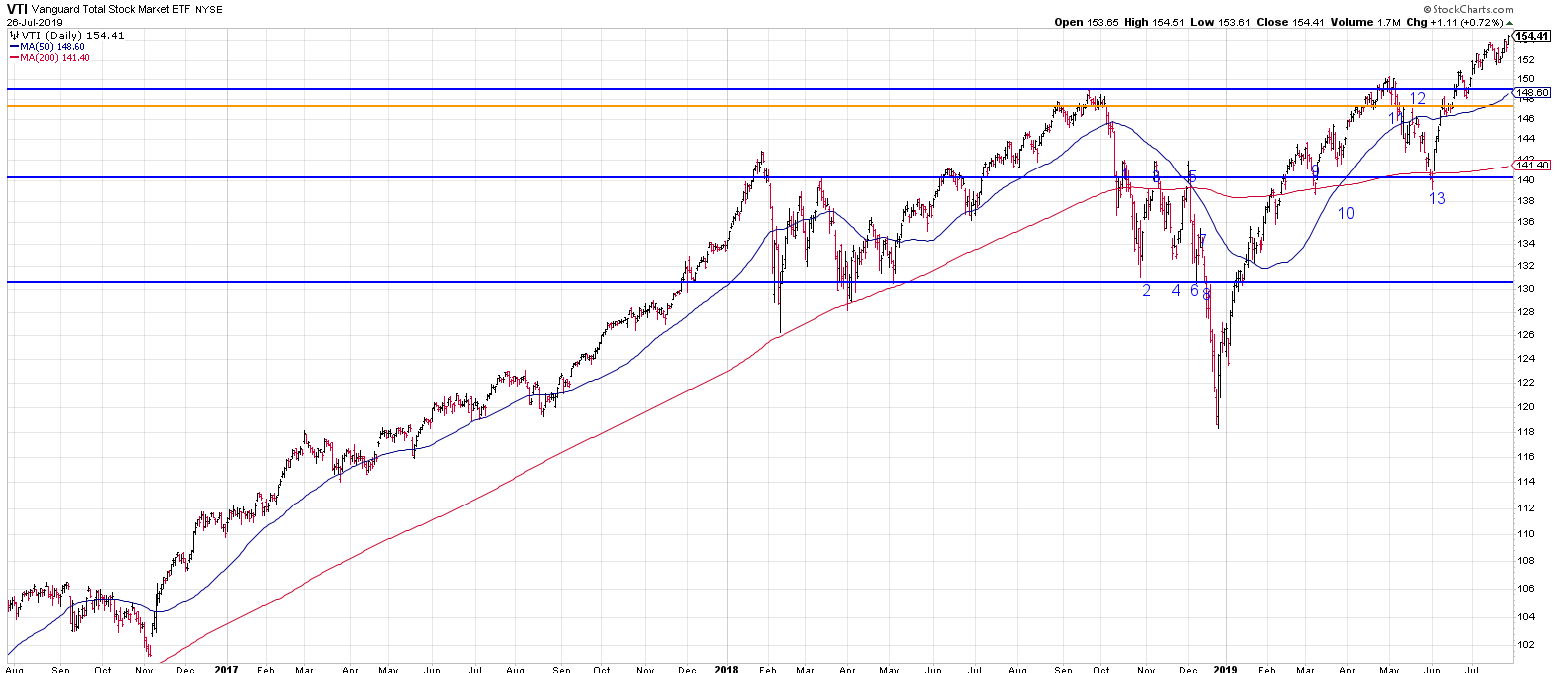

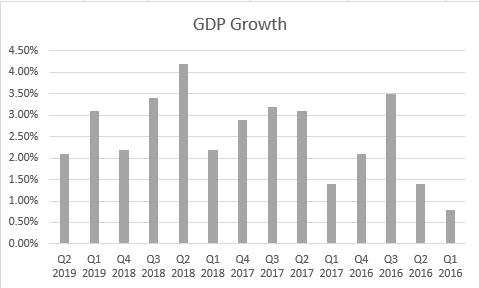

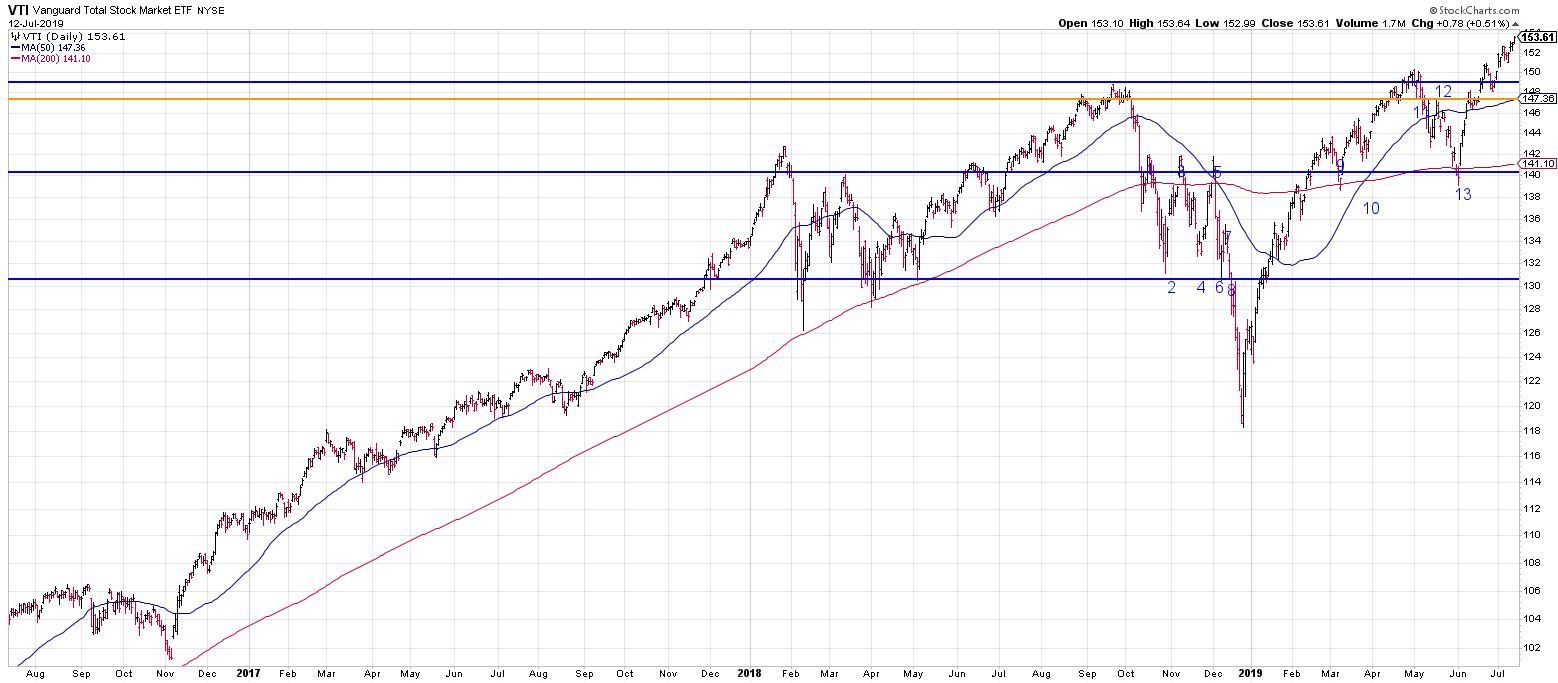

The market broke through recent resistance and is only 1.77% off of the all-time high set on July 26th. Stocks certainly didn’t rally on economic news. Manufacturing in the US is now contracting (see ISM below), the jobs report was tepid at best, and Q3 growth estimates are at about 1.5% for both the Atlanta Fed’s GDPNow model and the NY Fed Nowcast, all indicating a slowing economy.

Apparently news that the US and China would meet in October was enough for the market to move higher.

While the rate of growth in the US slows, $17 trillion in negative-yielding debt around the world is creating a wave of support for equities.

JOBS

The US added 130,000 jobs in August, and that included 25,000 census workers The amount of jobs being added has been falling the last few months. A bright spot, average hourly earnings were up by 3.2% and has now been over 3% for more than a year. The unemployment rate was unchanged at 3.7%.

ISM

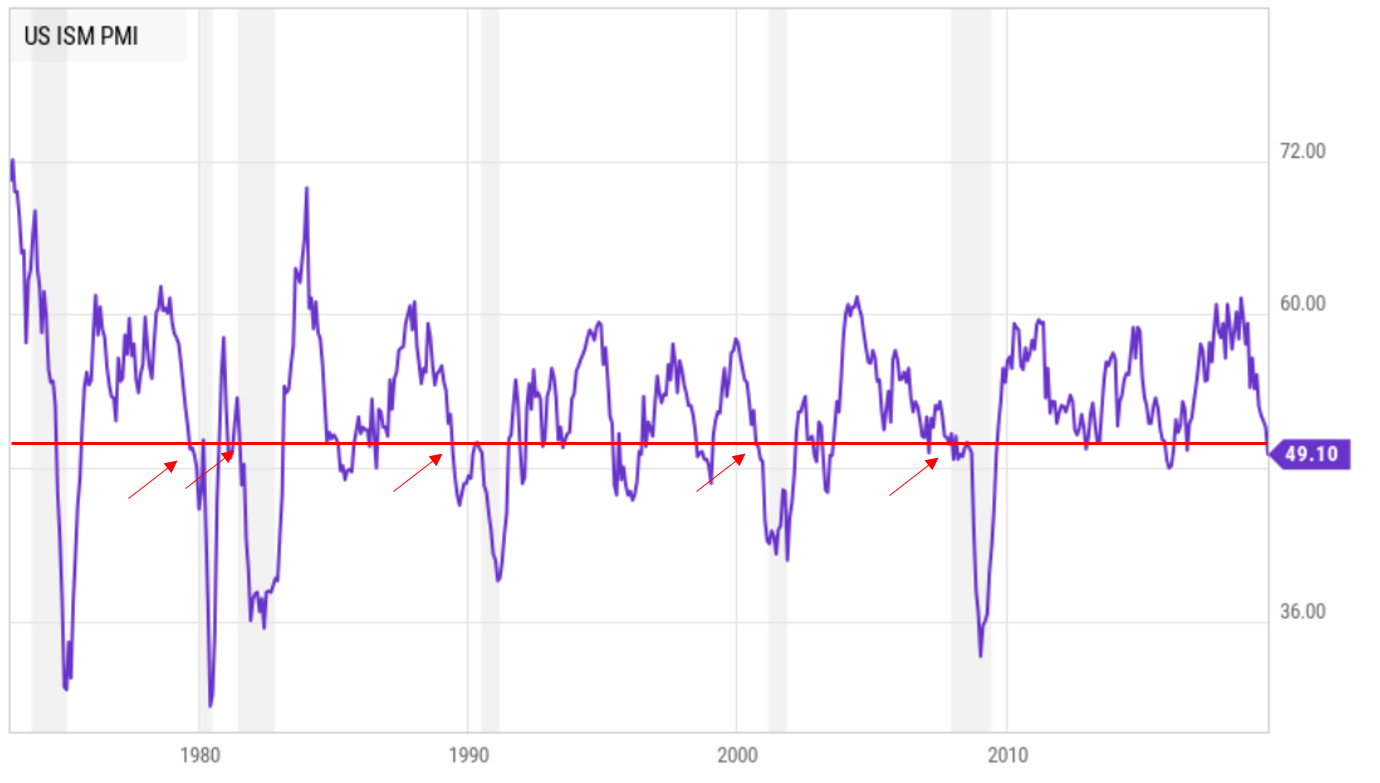

The Institute for Supply Management’s manufacturing index fell to below 50 for the first time since August of 2016. The reading came in at 49.1, below 50 is considered contractionary. Trade was cited as the biggest concern by executives.

Manufacturing only accounts for 11% of US output. So a weak reading does not necessarily measure the entire US economy. The overall job market continues to be solid and recent consumer spending numbers were strong. But this is a piece in the puzzle. In the past, when the ISM fell below 50, it has preceded a recession (shaded areas below) some of the time (see red arrows below) but not all of the time.

IMPACT OF TARIFFS

According to a new research report from economists at the Federal Reserve, the uncertainty created by trade policy has cut about 0.8% from US and global economic output in the first half of 2019. That number will increase to greater than 1% due to more recent developments.

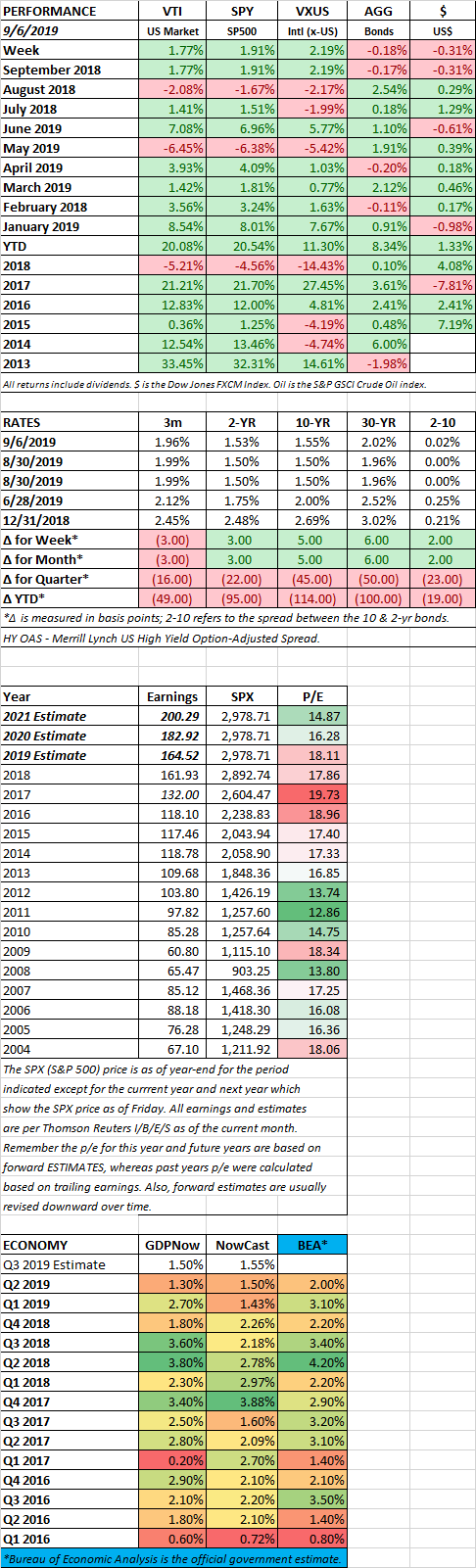

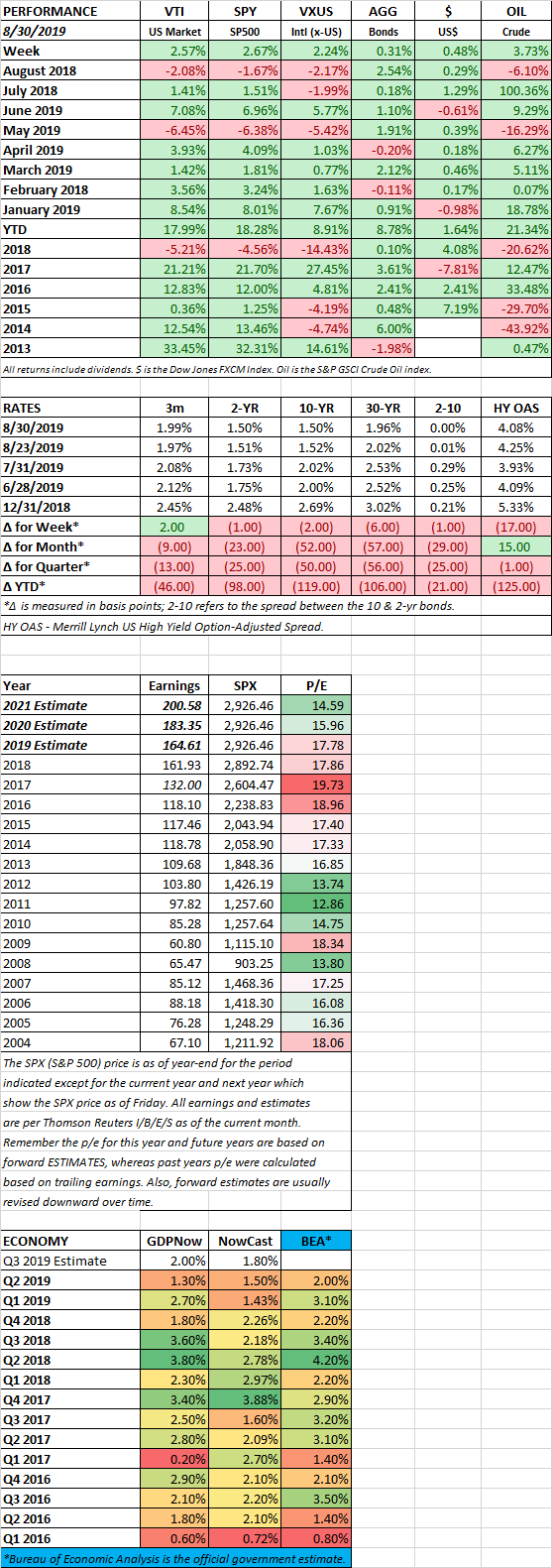

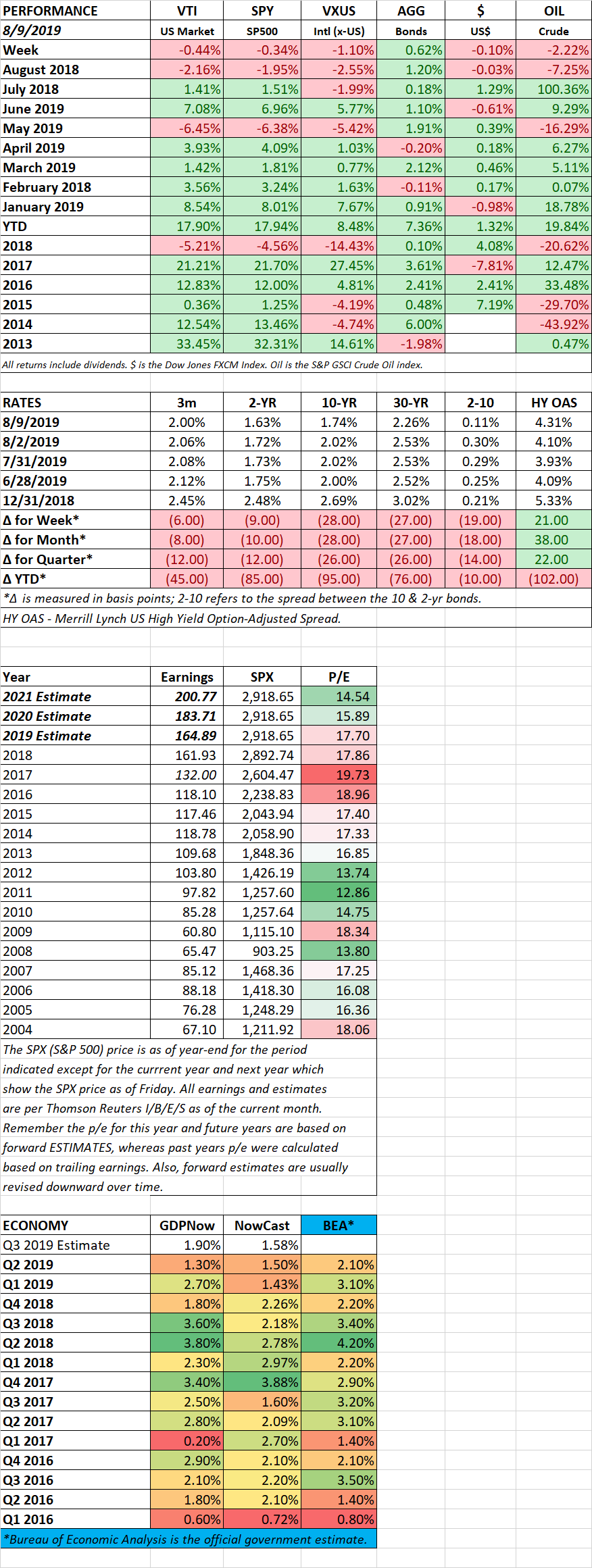

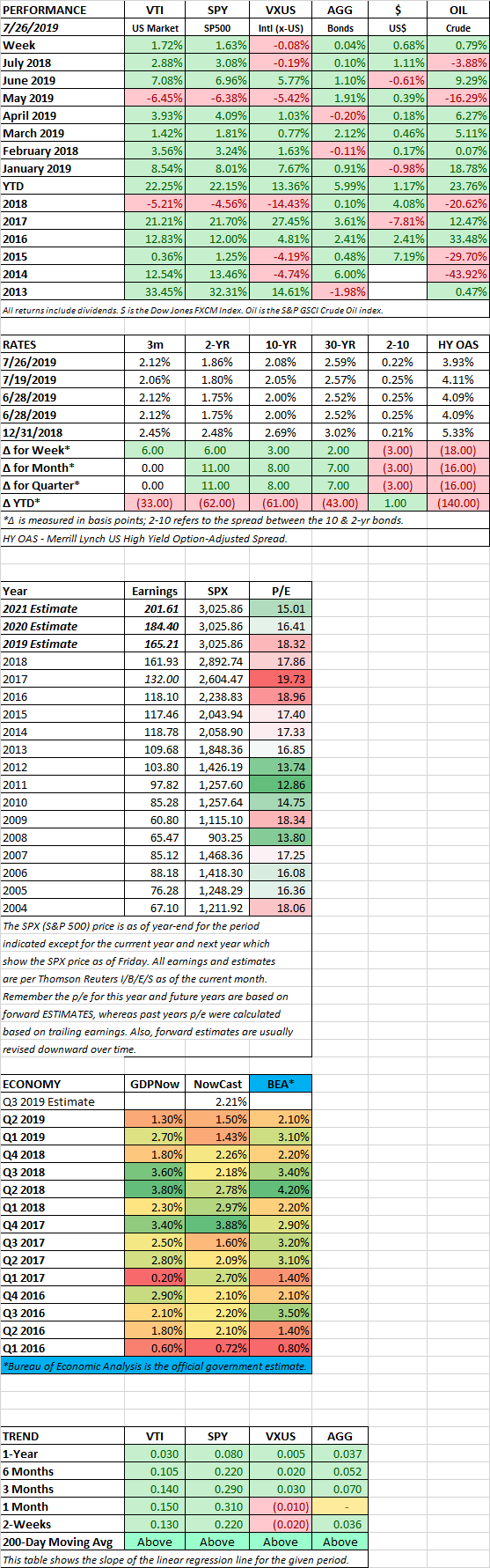

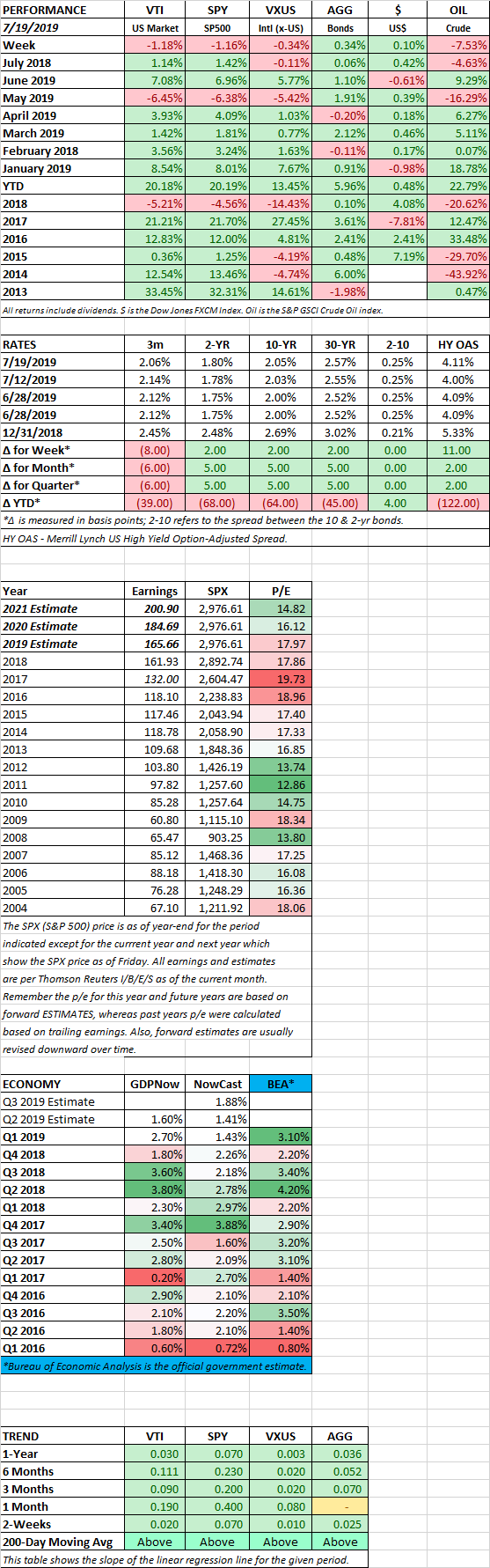

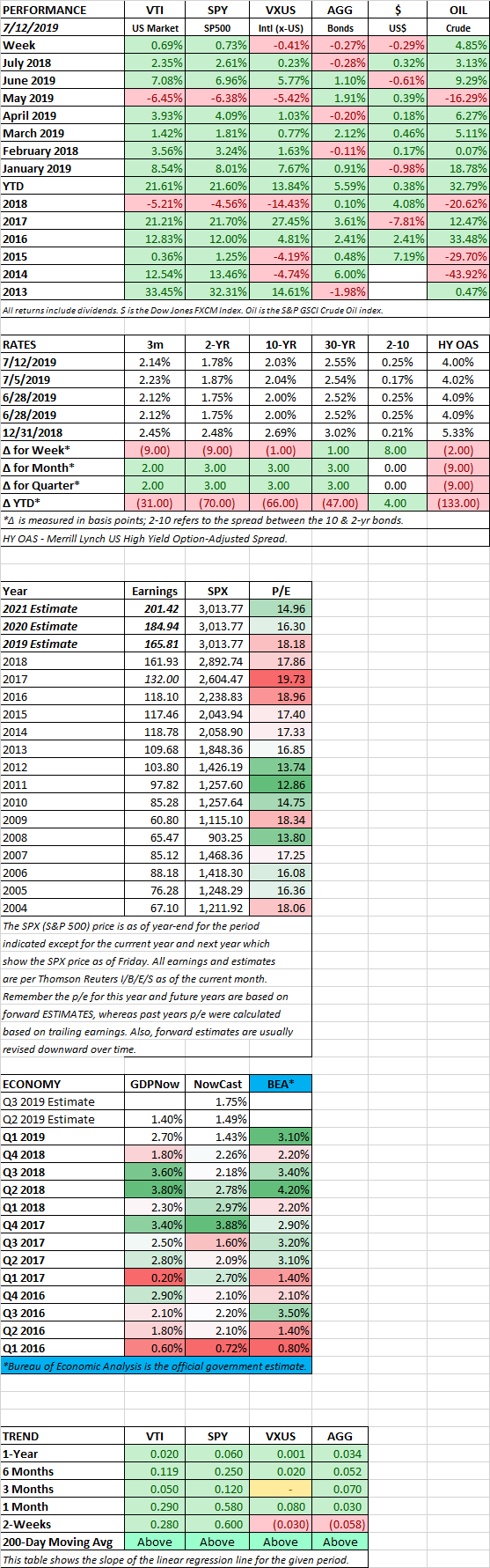

SCOREBOARD