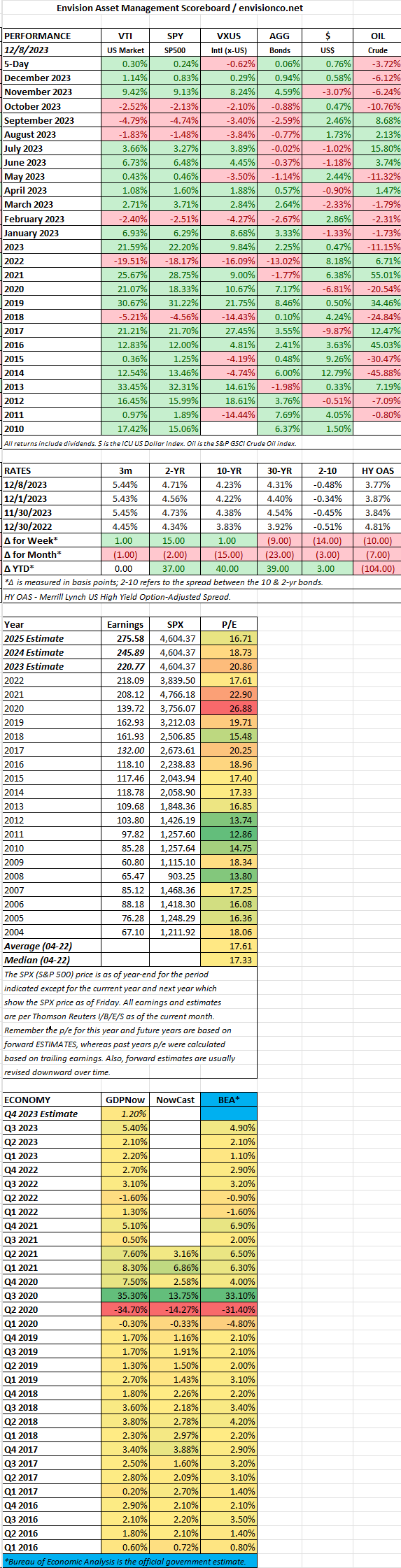

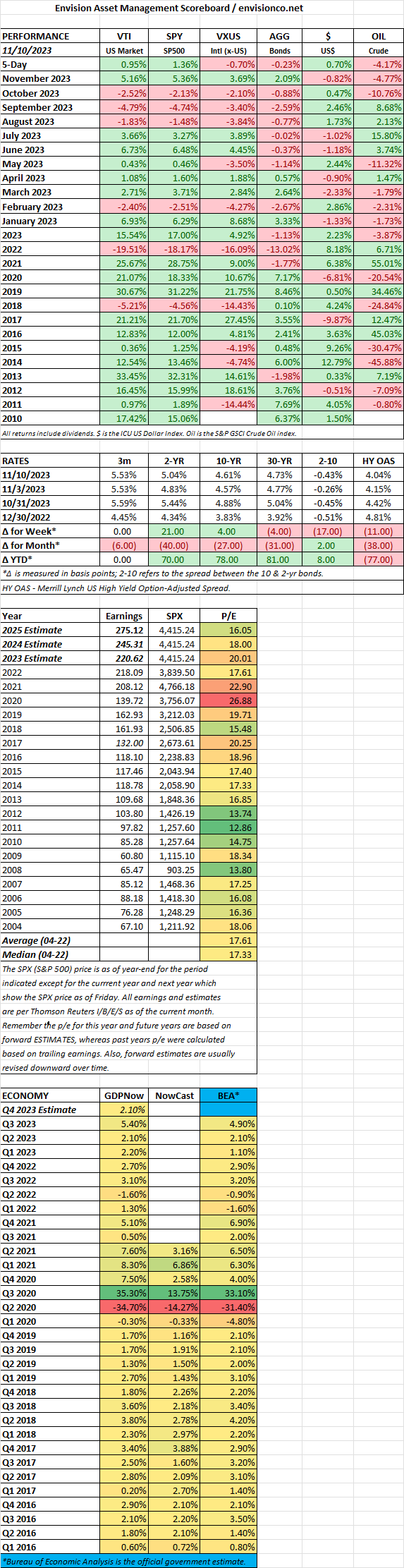

SCOREBOARD

SCOREBOARD

MARKET RECAP

SCOREBOARD

MARKET RECAP

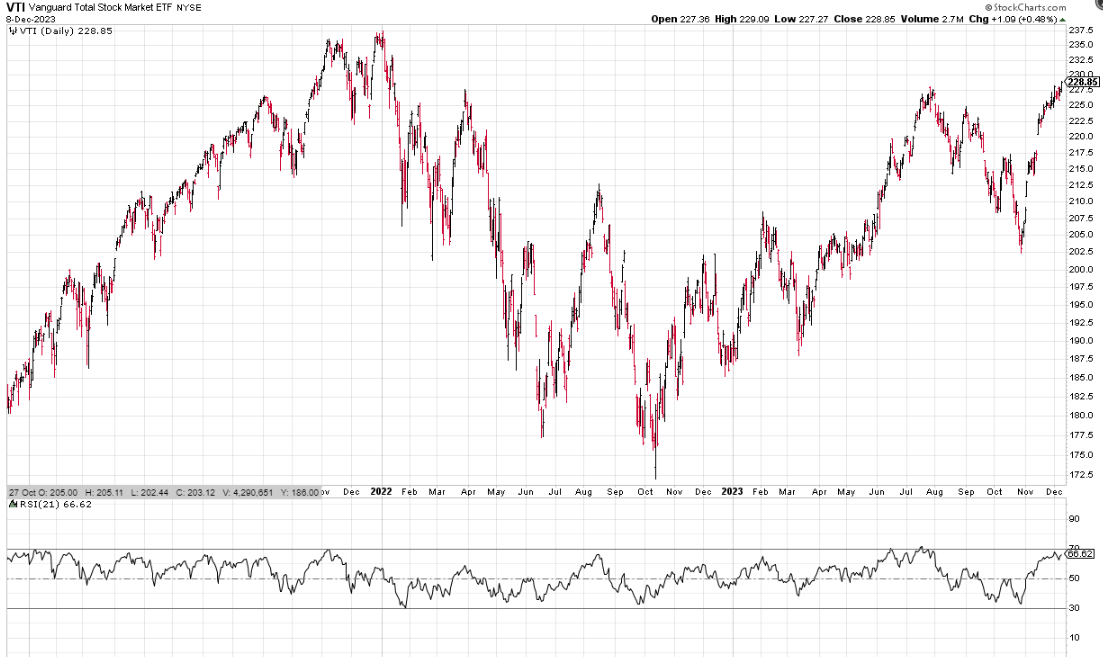

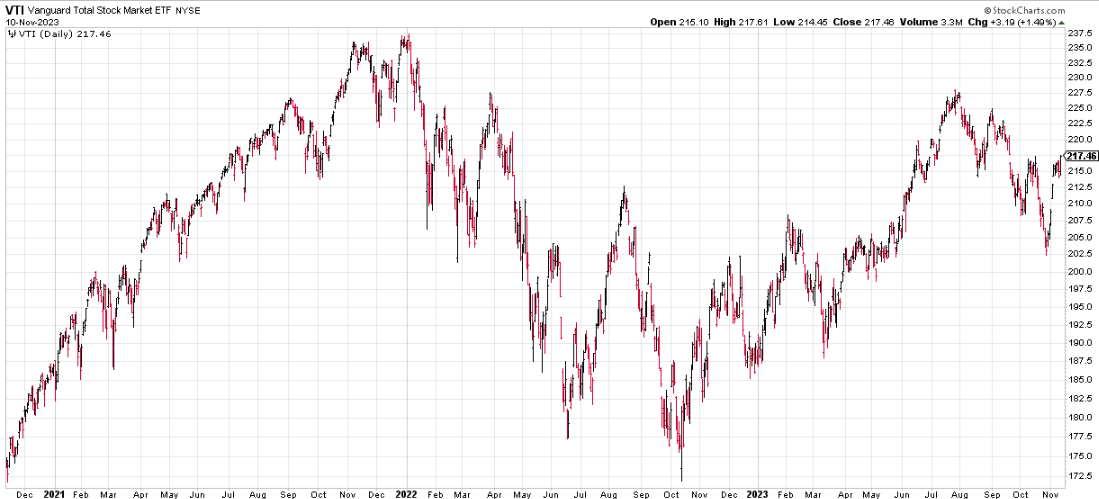

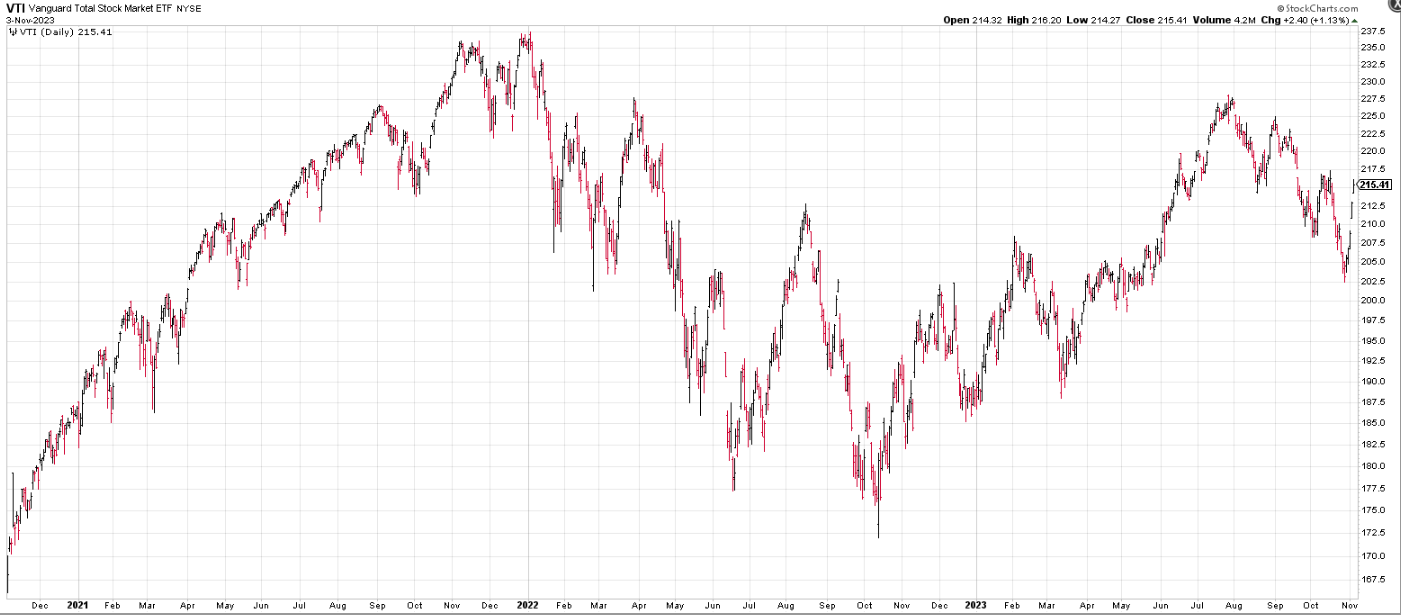

US STOCK MARKET (VTI)

SCOREBOARD

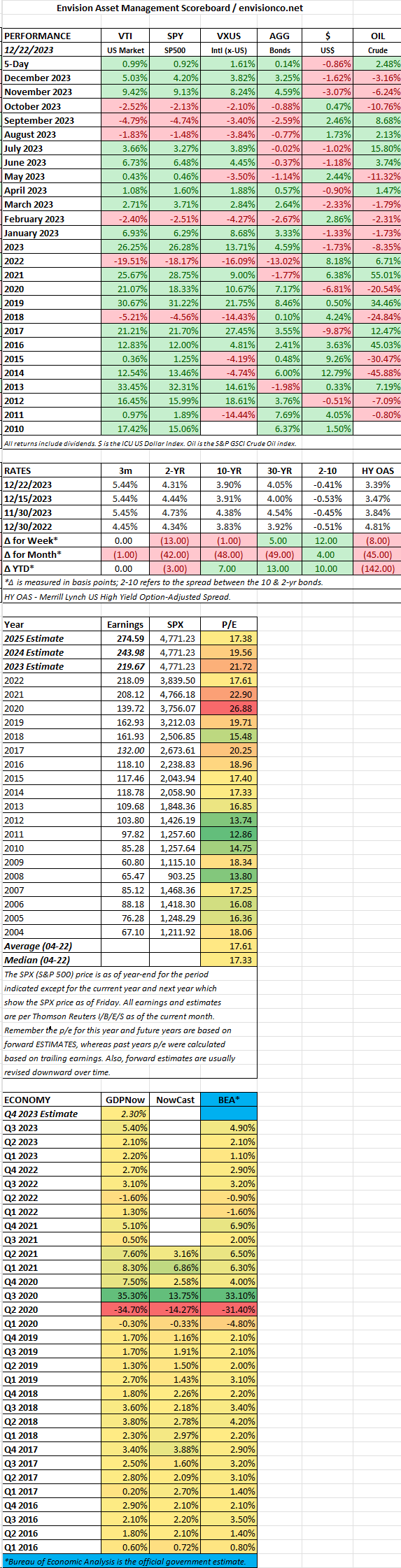

November 2023 painted a rollercoaster picture for financial markets, offering a welcome glimpse of sunshine amidst lingering anxieties. Here’s a breakdown of the key themes:

Equity Market Uptick:

Shifting Sentiment:

Sector Rotation and Winners:

Global Markets Join the Party:

Other Notable Events:

Overall, November 2023 was a month of remarkable financial market resilience. The fading threat of inflation, cautious optimism regarding Fed policy, and strong corporate earnings combined to fuel a broad-based rally. However, some underlying uncertainties remain, including the trajectory of economic growth, geopolitical tensions, and the future pace of interest rate hikes.

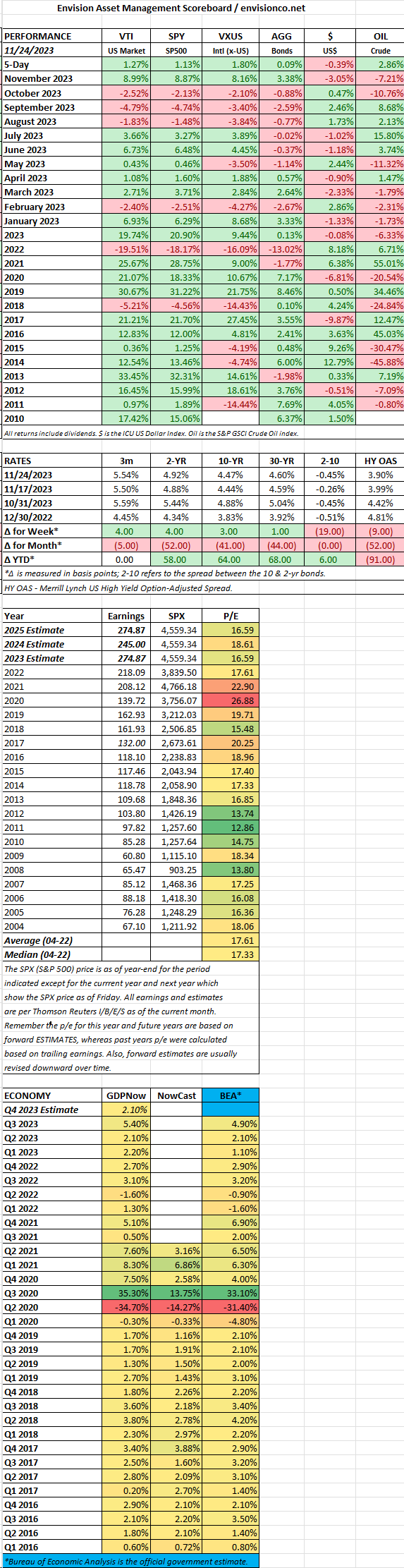

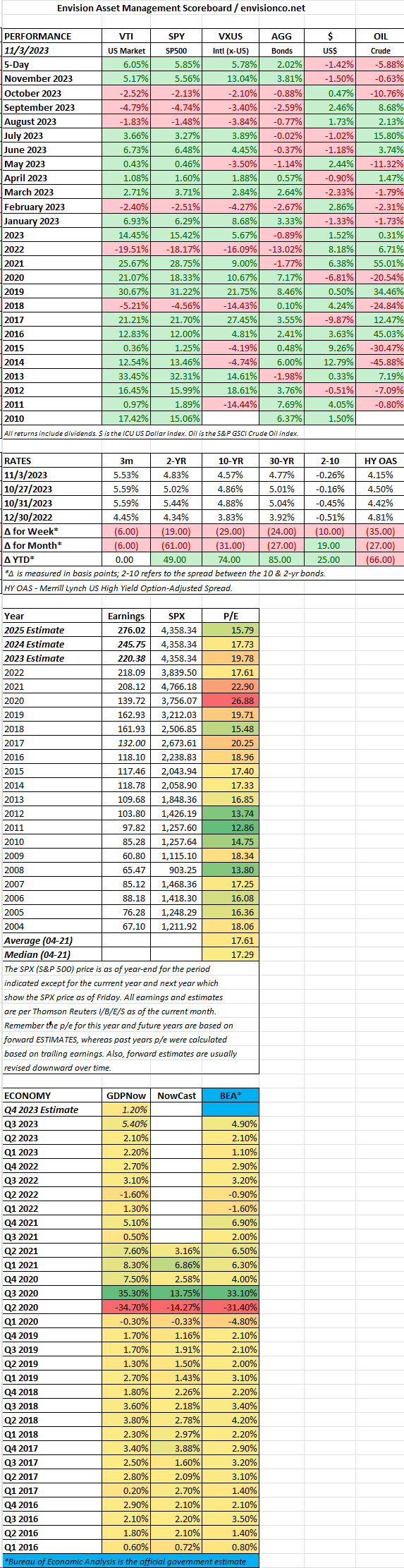

MARKET RECAP

SCOREBOARD

MARKET RECAP

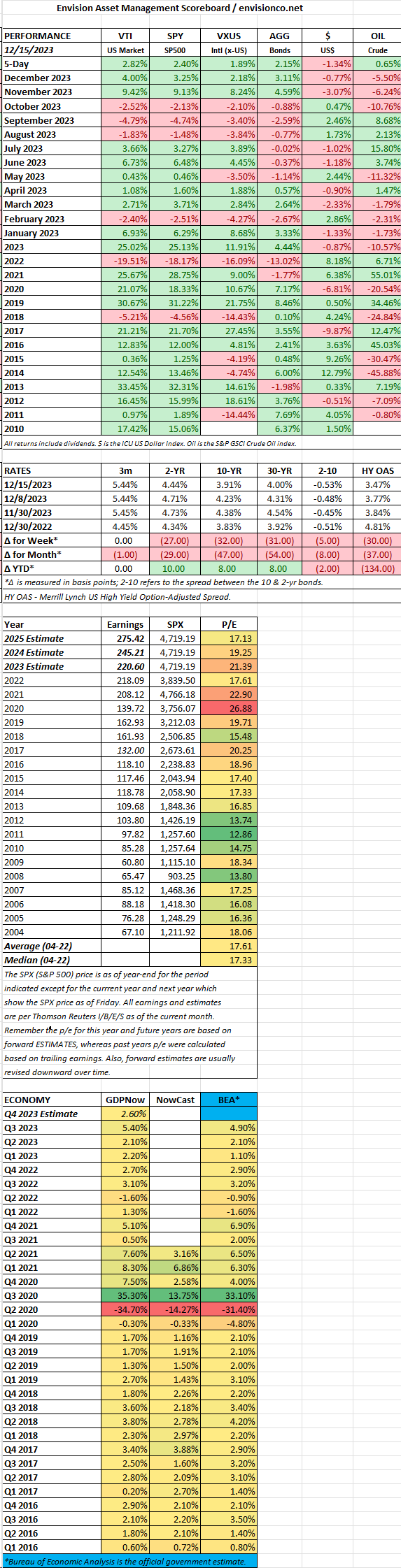

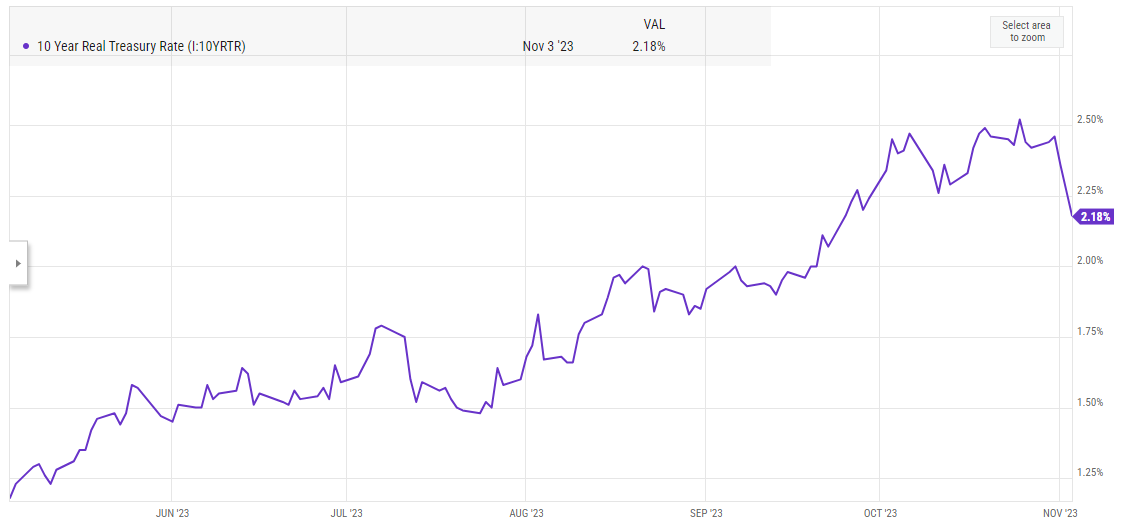

The S&P 500 continues to tear higher, up 10% since the October low. For the week, US stocks advanced by 2.60%, international stocks by 3.52%, and bonds by 1.37%. The yield on the 10-year treasury fell by 13 basis points to 4.44%.

Investors figure that inflation is sinking, interest rates have dropped, and Fed cuts are coming. The CME Fed-Watch site says the market is pricing in four 25-basis point cuts by the end of next year. That seems contrary to the “higher for longer” theme that Fed officials preach.

MARKET RECAP

MARKET RECAP

US STOCK MARKET (VTI)

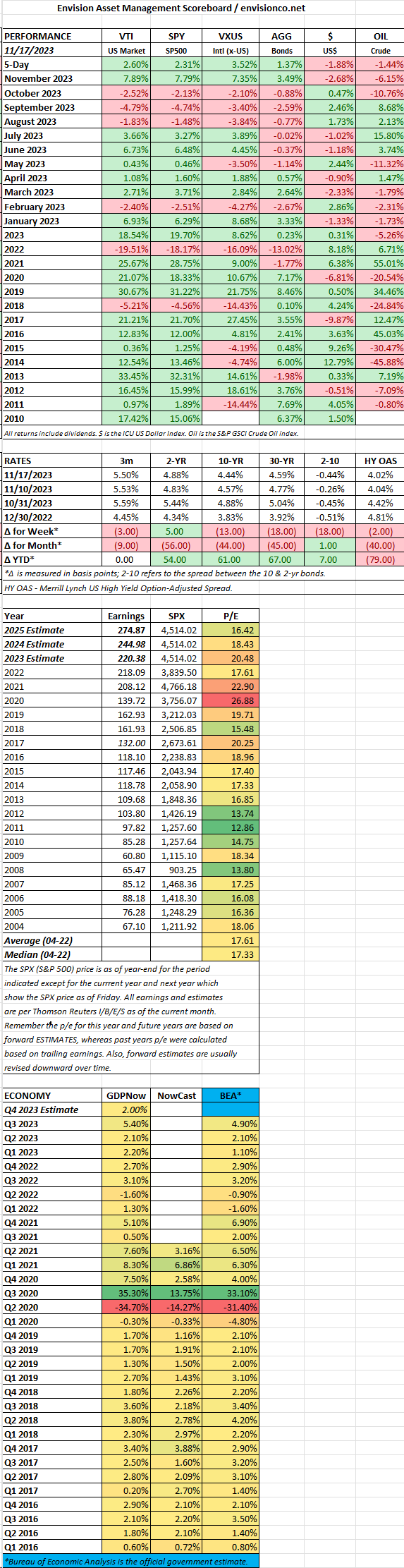

SCOREBOARD

MARKET RECAP

Equities had a monster rally worldwide; US markets jumped by 6.05% and international stocks by 5.78%. Bonds rallied by 2.02% as the 10-year yield fell by 27 basis points. Markets rallied when the Treasury announced that long-term debt auctions would be smaller than anticipated. In addition, economic data came in softer than expected. Interest rates dropped like a rock in response.

During the week, the Fed announced they would hold interest rates steady. Investors are assuming that interest rates are near their peak. Also, job growth was only +150,000 in October, half of the September gain. All of this news combined set up a “Goldilocks” scenario, at least that is the way the market reacted.

SCOREBOARD

October 2023 saw financial markets navigating a mixed bag of anxieties and cautious optimism, much like the weather shifting between crisp autumn mornings and warm afternoon spells. Here’s a breakdown of the key themes:

Equity Market Pullback:

Rising Yields Bite:

Economic Resilience Fails to Buoy Markets:

Sector Rotation and Energy’s Rise:

Other Notable Events:

Overall, October 2023 proved to be a month of cautious adjustment for financial markets. While a strong economy provided some solace, rising interest rates and persistent inflation anxieties kept the bears in control.

MARKET RECAP

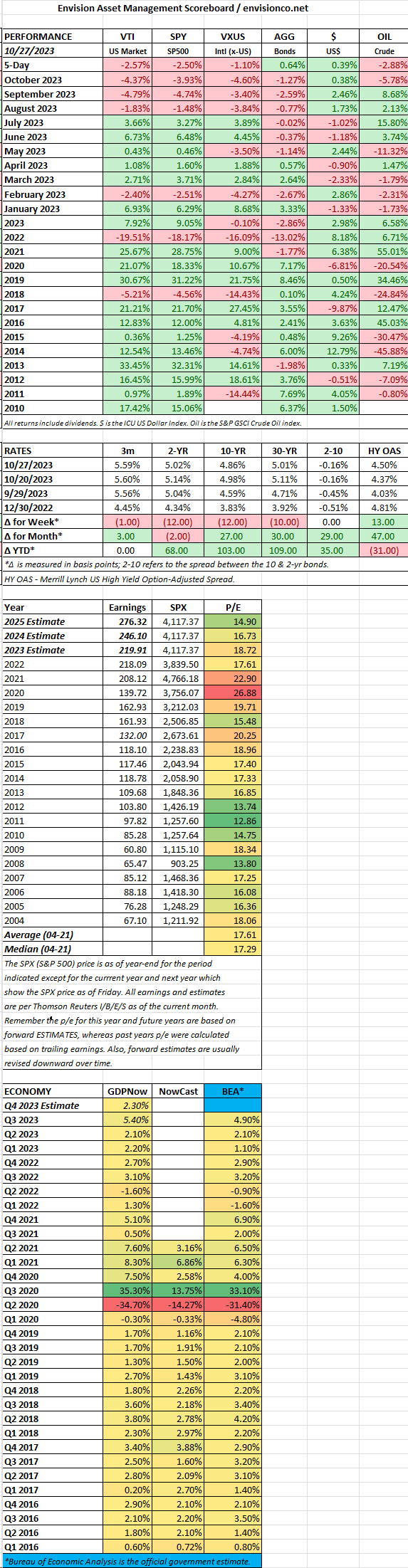

US stocks fell by 2.57% and international stocks by 1.10%. US stocks are now in correction territory, down 11.05% from their July high. Bonds managed a 0.64% rally. The US economy grew at a robust 4.9% in Q3, up from 2.1% the quarter prior. The GOP elected a speaker, Mike Johnson, after a couple of weeks of going through a series of nominees.

SCOREBOARD