MARKET RECAP

It was a week like no other and one they will be talking about for the next 100 or so years, maybe more. A revolution of individual investors upended Wall Street and probably put an end to short-selling as we have known it for a long-time. It was Gamestop’s week and the story is further below.

But the entire GME episode certainly indicates that there is some wild speculation going on, and wild speculation in a raging bull market is often a sign that equities need to slow down or sell-off. Now maybe it happens and maybe it doesn’t, no one knows, but there are certainly lots of signs of crazy euphoria as we have been documenting for a while now.

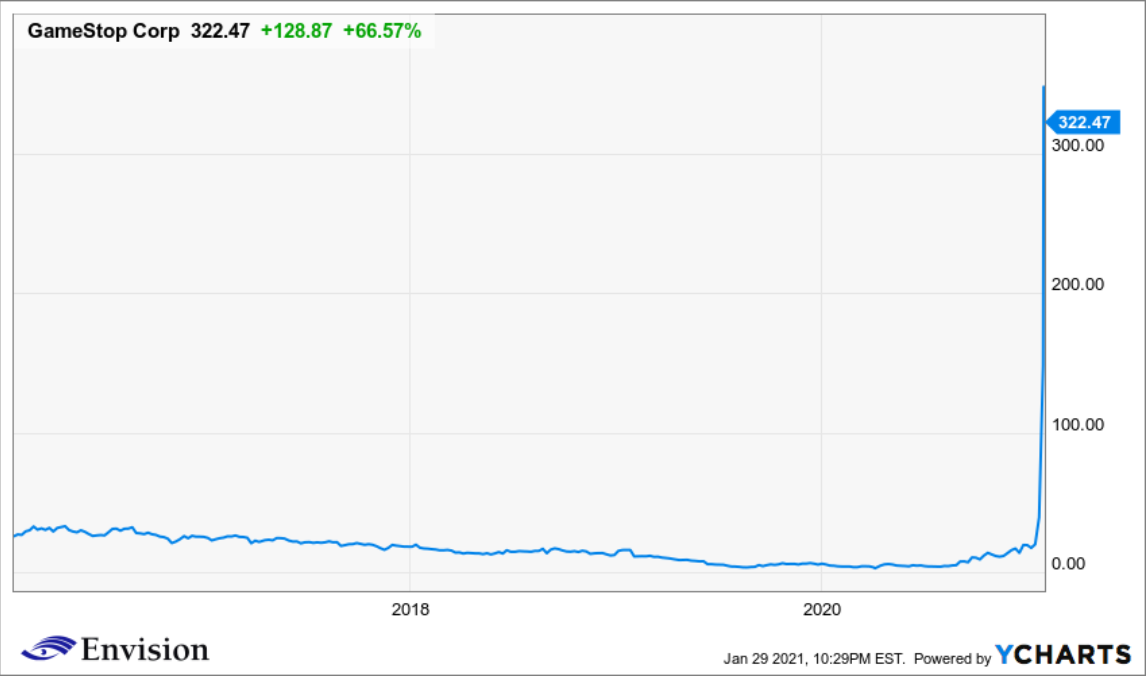

For the week US stocks dropped by 3.5% and international stocks by almost 4%. Gamestop was up 66% on Friday, 396% for the week, and is up by a factor of 76 over the last year.

GAMESTOP

This is the week when Gamestop took over the financial world. It might turn out to be the greatest long trade of all time. It was when an army of individual investors took on the hedge funds and won. It has been described as the younger generation against the older generation. It has been said that this has proved that value means nothing and the story means everything, but really, at its very core, what got this stock to move, were a few value investors who saw a fundamentally mispriced stock, kept telling their story, and believed in GME, until the Reddit army bought in and turned it into something else completely, and made the original believers incredibly rich. It was not an overnight get rich story. It was a few investors who believed for years until their story took on a completely unexpected life of its own.

HOW IT HAPPENED

Keith Patrick Gill, a 34-year old CFA and accounting major from Massachusetts seems to be the investor who started it all, at least on Reddit’s Wall Street Bets. Gill was an insurance advisor for Mass Mutual, but was let go. Don’t worry though, Gill probably pocketed 35-50 million from his investment in the last few days.

Give Gill extraordinary credit for doing the research. Gill actually believes in making money the old-fashioned way, by doing intense research and finding a story that others are missing. That is what got him interested in Gamestop. Gill started investing in GME long ago, in June of 2019, when the stock was trading around $5. Gill thought GME could turn around their fortunes with new customers and new technology. Gill also was aware of very high short positions in GME, which would be a potential fuel to fire the stock higher.

Gill did an amazing job publicizing his positions and slowly over time, he turned into somewhat of a legend in the Wall Street Bets Reddit forum. But Gill was not the only one, there was a loose coalition of individual value investors that saw a misunderstood company and kept telling their story. Rod Alzmann was one of them and started a website called GMEDD.com (the DD stands for due diligence) which laid out the fundamental argument for Gamestop. Alzmann had set a bull-case target price of $169.

The other part of this set-up were the professional investors on the other side who believed Gamestop was going to follow in the footsteps of the old video chain Blockbuster, it would only be time until GME went bankrupt and ended up with a terminal value of $0. So many investors believed this argument that there was short interest in the stock of 140%. Someone who is short the stock, borrows the shares from an owner (a “long” investor), and eventually has to buy it back. The idea is to short the stock at let’s say $20 a share, and then if the company is getting close to bankruptcy or has other problems, buy it back at a much lower price, and profit on the difference. But shorting a stock is a very difficult game for lots of reasons (this would require more detail than we have space for here, contact us if you are interested to learn more). But what it all means is that there was more than 100% of interest in this stock going lower, and that meant that at some point, those shares had to be purchased back. But if the stock price started going higher, and if it went much higher, then the shorts would have to start buying back the stock in big quantities in order to prevent further losses, and when this happens, and there is not enough supply, the stock can rocket higher. That is what happened in a big, big, way. This is called a short-squeeze, and what we saw with GME this week was one of the biggest short-squeezes ever.

Somehow, over the last few weeks, other investors (speculators) took the mantle and it morphed into a “rage against the machine” rally cry, the small guy against the big bad hedge funds, and this got millions of investors to buy GME and to stick with it as if it was almost a religious experience. Suddenly, the professional shorts were on the wrong side of this incredible short squeeze. And thus, GME went higher and higher and higher, until it topped out at $483.

In the end, this will most likely end up badly for most of the investors. The stock is trading at $322 right now and it is probably worth much less, and not everyone is going to get out at the top, it is just impossible. Lots of people will end up holding the bag, and those will be the losers. When that happens, who knows, maybe GME rallies another $500 from here, but sooner or later, I would say it ends up much, much lower.

THE REAL REASON BROKERS PUT RESTRICTIONS ON TRADES

On Thursday, Robinhood and other brokerages either stopped clients from purchasing more GME or put on restrictions. There were lots of conspiracy theories and politicians and others jumped on that theme to push their individual agendas, and to put their followers into more of a rage, but the truth is, during extreme periods of market volatility, brokers often have to put an end or at least slow down the party. This was not the first time and it won’t be the last.

Here is why, when someone buys stock through Schwab or TD or Robinhood or anyone else, they are buying on credit. The client owns the stock they just bought instantly, but they don’t pay until two days later. This is what is known as “T+2 settlement.” The seller is exposed to credit risk for two days. Someone who bought GME for $150 on Tuesday may not show up to pay for the stock on Thursday if GME had dropped to $10. Normally, this is not a problem as stocks don’t fluctuate that wildly, and volume is not so overwhelming in any one particular issue. But in this case, GME, and others like it, were being traded at ridiculous levels of volume and potentially could have dropped to almost zero just like that. After all, this was a stock with lots of pretty smart people thinking that $0 is where it would eventually end up.

Most stock trades go through a clearinghouse for processing. The brokerage firms are members of the clearinghouses and they effectively guarantee the trades. The clearing brokers have to post collateral to make sure they can honor these trades, this would be similar to a margin account for a regular customer. With all of the volume and all of the volatility, the collateral was getting way too high and risky for some of the individual brokers, and they simply had too much risk on the table. They needed to slow down the trades to put a temporary tap on their downside exposure until they could recalibrate. The brokers were actually doing what was needed to prevent a systematic breakdown of the system in the event of a disaster.

The Depository Trust & Clearing Corp (DTCC), which operates the clearinghouses for U.S. stock trades, said that the trading in GME (and others) had “generated substantial risk exposures at firms that clear these trades” and that the trades were “predominantly on one side of the market.”

That is why Robinhood had to quickly raise $1 billion.

Had they not put on restrictions, and had a worst-case scenario ensued, the brokers would have gotten ripped by politicians and regulators for letting the situation get out of control and putting the entire economy at risk. Instead, they did what was probably the prudent action to safeguard the system, and are now getting attacked and ripped by the regulators and the politicians for a different reason. So they were damned if they do and damned if they didn’t. But they probably did the right thing given the risk.

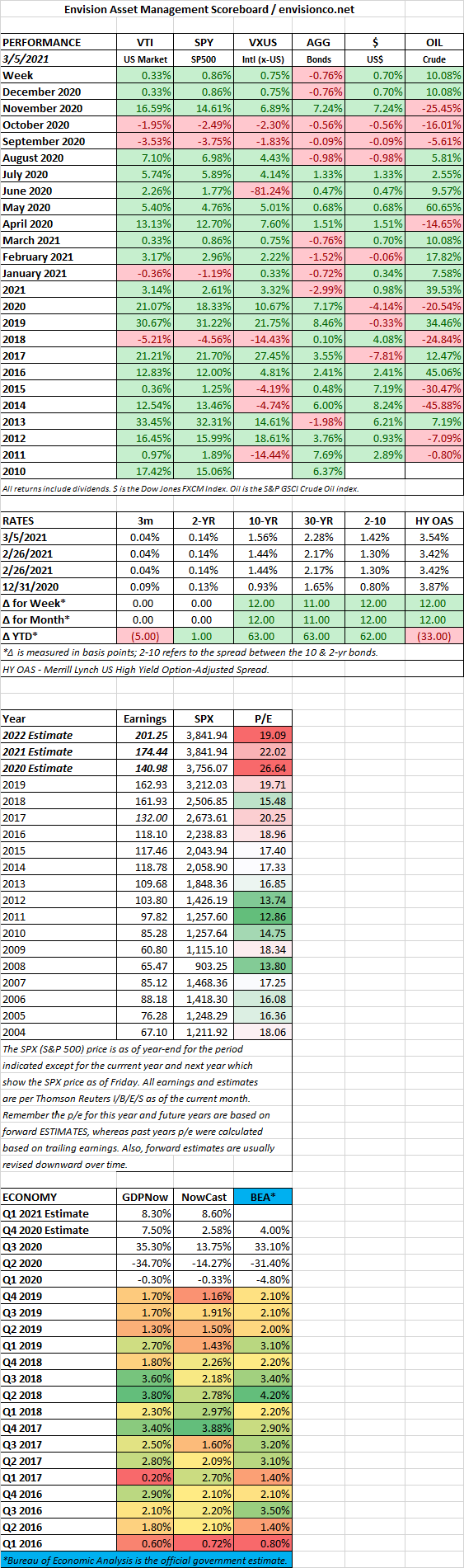

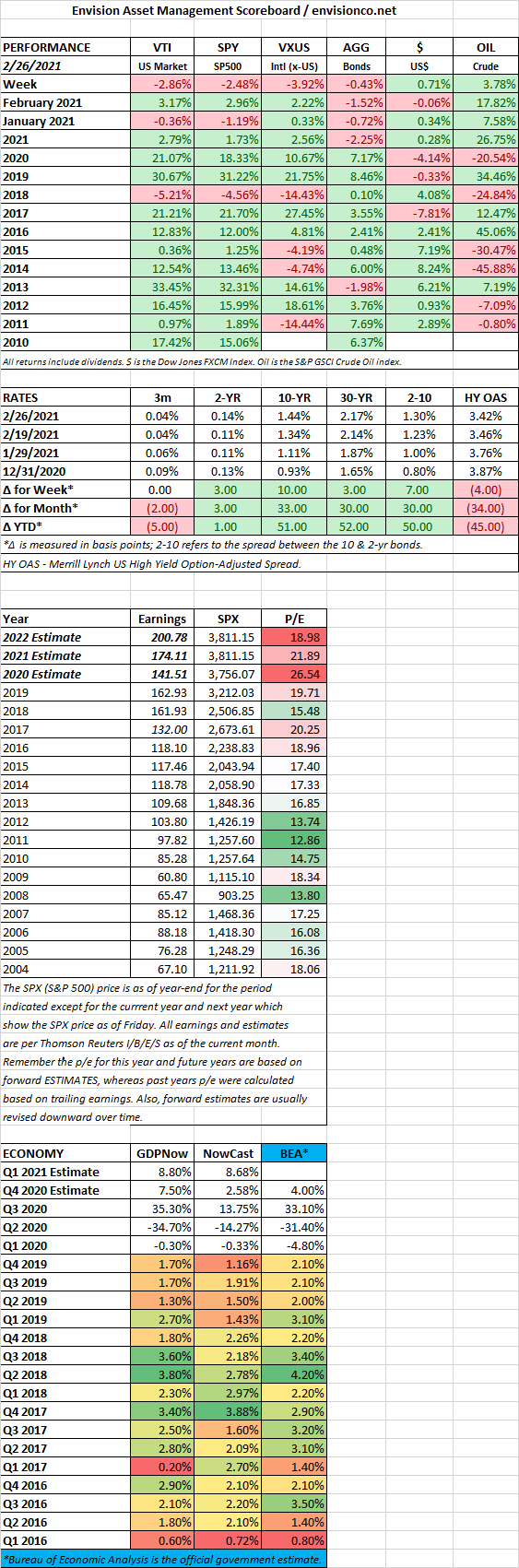

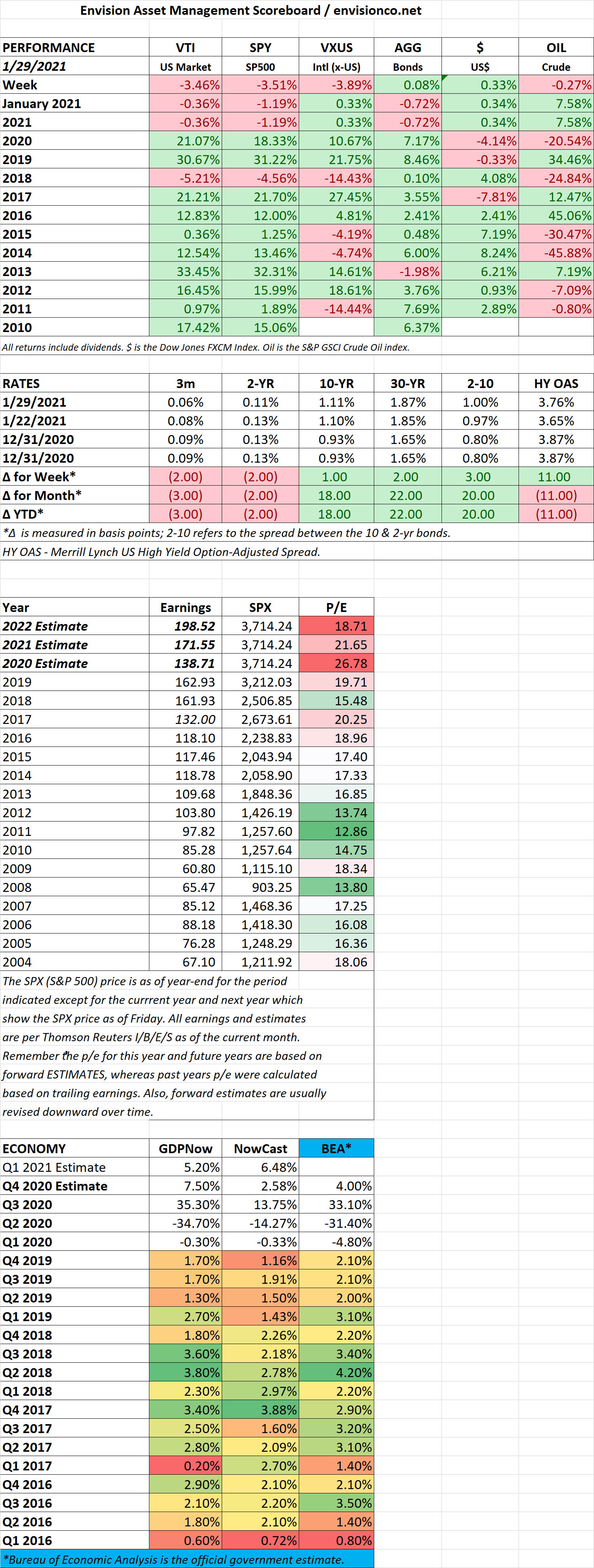

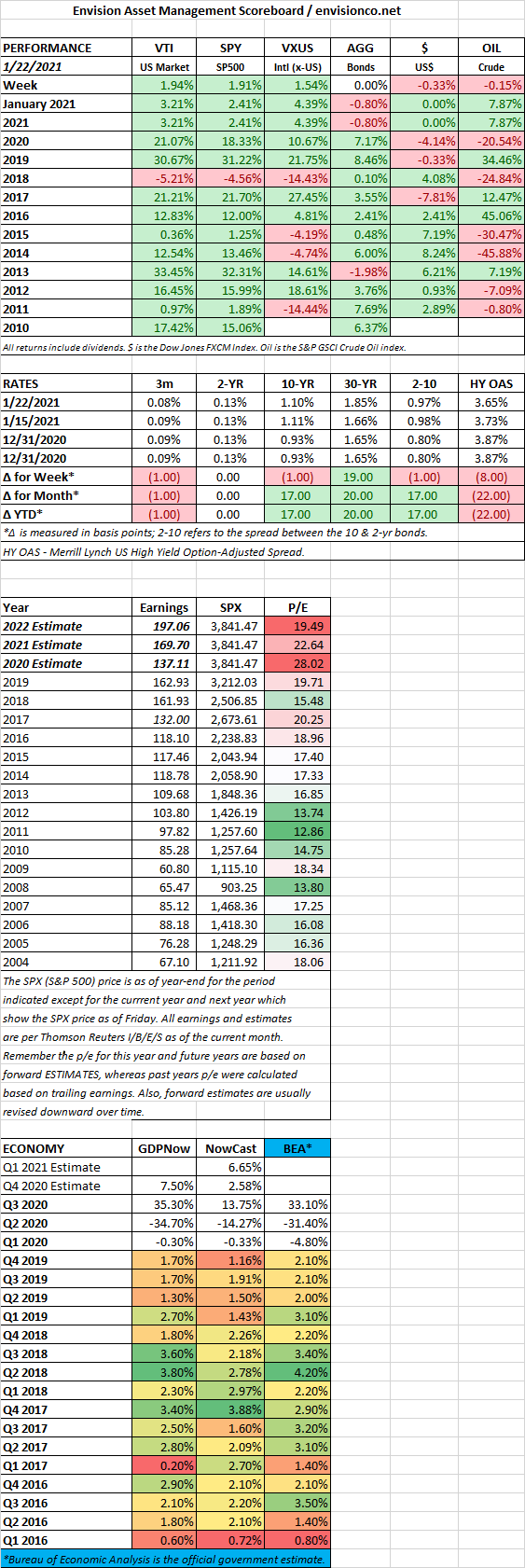

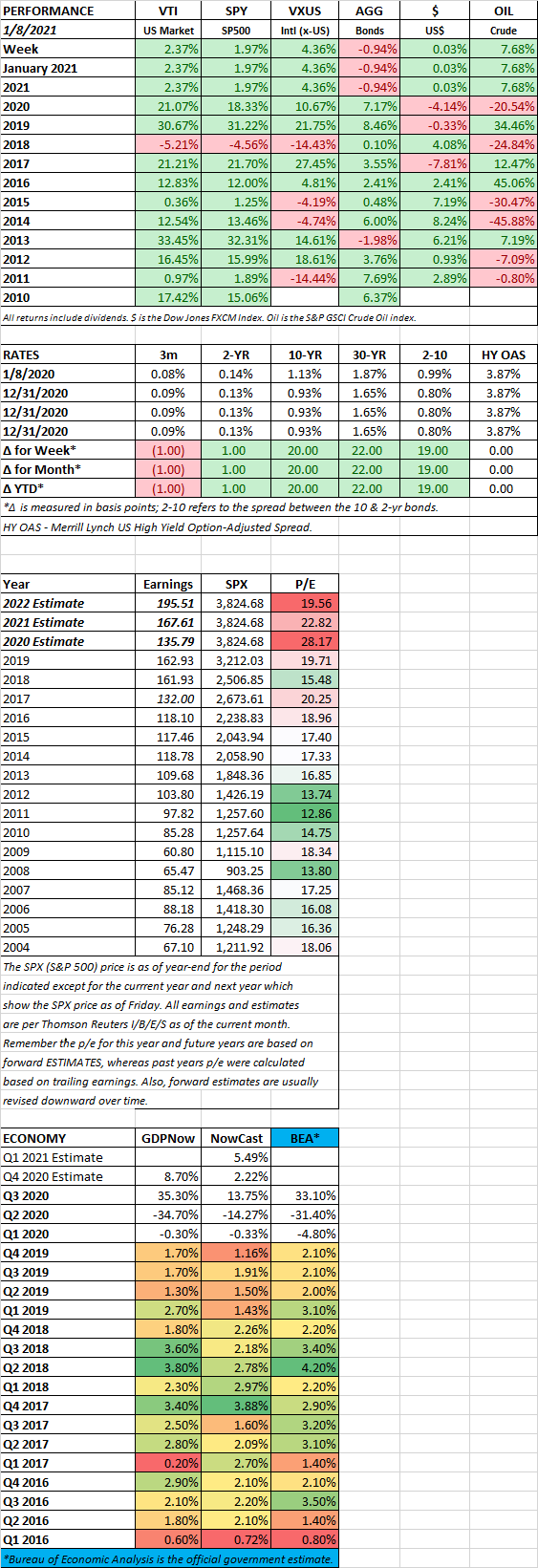

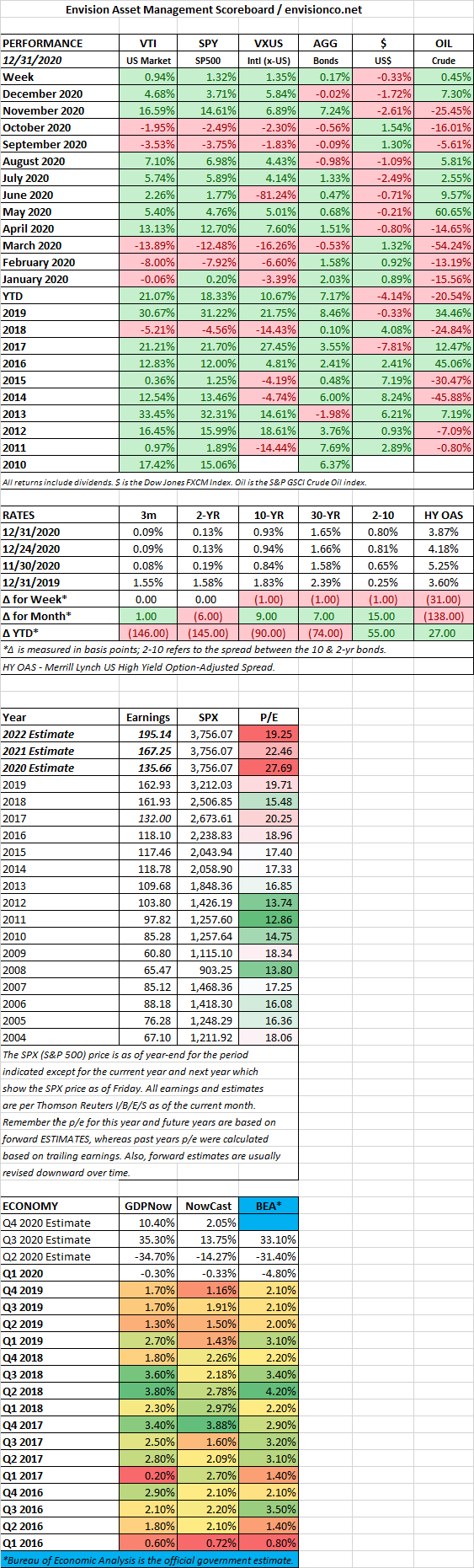

SCOREBOARD