HIGHLIGHTS

- Stocks explode higher on dovish comments by Powell.

- Trump and Xi to meet on Saturday, with hopes that a deal can be made.

- Initial jobless claims hit a six-month high.

- GM announces job cuts.

- Economic Surprise Index has fallen to a six-month low.

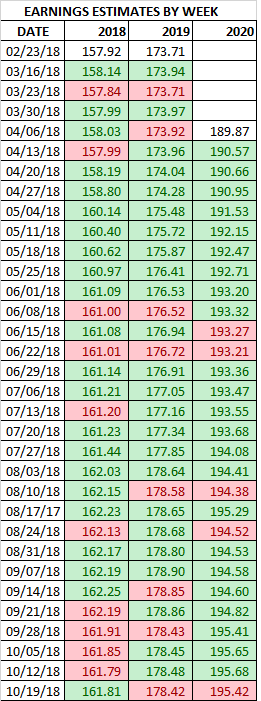

- 2019 earnings projections have declined for seven straight weeks.

MARKET RECAP

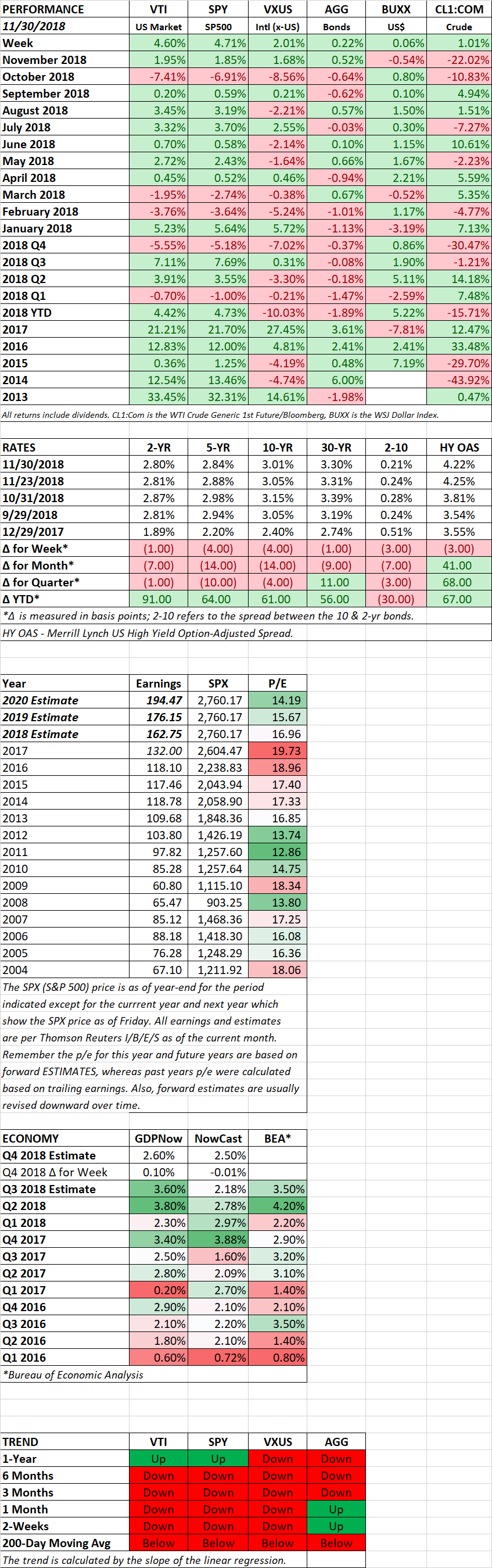

The market exploded higher, US stocks surged by 4.60% and international stocks were up 2.01%. It was the best week in seven years. Stocks were helped by comments from Fed Chair Jerome Powell, and hope that President Trump and Chinese Leader Xi will reach a deal of some sort to forestall the next set of scheduled tariff rate increases. With the rally, equities were up by 1.95% for November and are now up 4.42% for the year.

Back in October, Fed Chair Jerome Powell set a hawkish tone when he said that the Fed was “a long way from neutral.” That set the perception that the Fed was dead set on a series of interest rate increases every quarter.

On Wednesday, Powell, speaking at the Economic Club of New York, shifted to a more dovish position, stating that interest rates are just “below neutral” and that there “is no preset policy path” regarding future interest rate increases. Powell went on to say that the Fed’s decisions would be based on economic data. That is just what the market wanted to hear, and equities burst higher, closing up by 2.3% on the day.

The rally was also good for the market from a technical perspective. Stocks did not put in a lower low (see the red line below) and broke through the high from the two-day rally a couple of weeks back (see the blue line). However, we would not give the all clear yet, there is still economic data out there that is mixed at best.

JOBLESS CLAIMS HIT A SIX-MONTH HIGH

It is too early to say this is the start of a trend, but, initial jobless claims came in at 234,000 this week, the highest reading in six months. Over the past several years, whenever there was a hint of a slowing economy, the fallback was that the labor market was extremely tight and that jobless claims were ridiculously low. At 234k, jobless claims are still very low historically, but the number does represent a recent high in initial unemployment claims.

GM ANNOUNCES JOB CUTS

GM announced that it will cut up to 14,800 North American jobs due to weak sedan sales. This is the first set of large job cuts since the last recession for the company. GM CEO Mary Barra said she wanted to take action ahead of the next downturn, “The industry is changing very rapidly. We think it’s appropriate to get in front of it while the business and the economy are strong.”

President Trump was not happy. He threatened to take away electric-vehicle and other subsidies that benefit GM. Those subsidies shouldn’t be there in the first place but that is another issue. Trump is of the belief that GM has an obligation not to cut jobs due to the government’s help in saving the company during the last recession. While heartbreaking, Barra is making these moves to keep the company financially secure so that they won’t have a repeat of a near-death experience the next time the auto industry falls into a major slowdown.

SURPRISE INDEX

The Citigroup Economic Surprise Index for developed markets has now fallen to a six-month low. The Index measures whether economic statistics are meeting the consensus projections. The index has been falling consistently since September.

EARNING PROJECTIONS

Stocks are selling at a reasonable valuation based on forward-looking earnings. The S&P 500 is priced at 15.67 projected 2019 earnings. The problem is that earnings projections for 2019 have now been revised lower for seven consecutive weeks. Per Refinitiv, earnings for 2019 are now projected at $176.15, down 1.53% from the high on September 7 of $178.90.

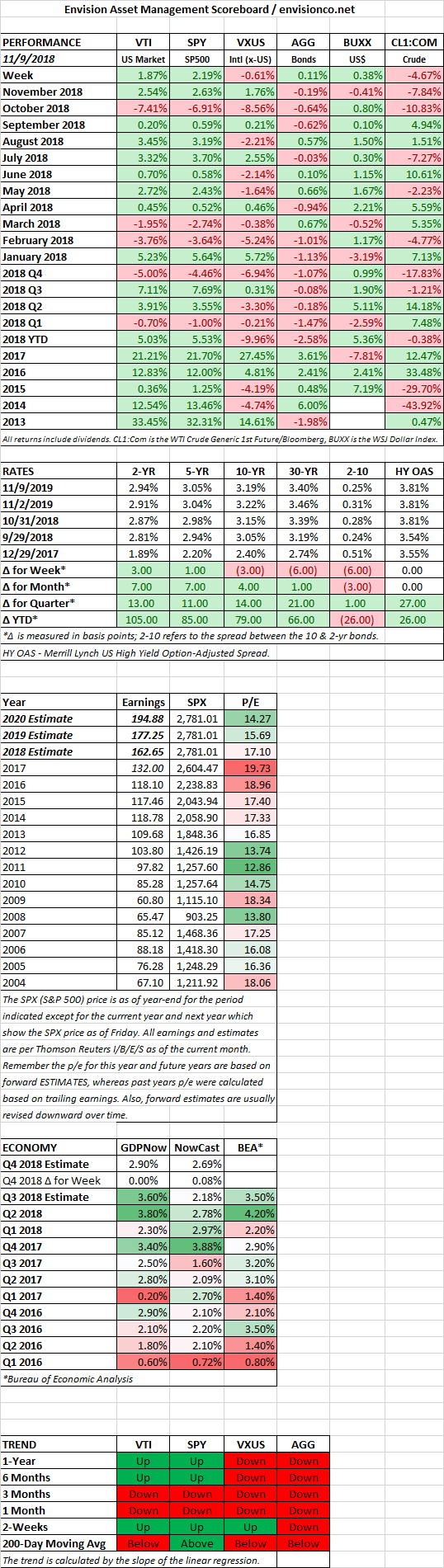

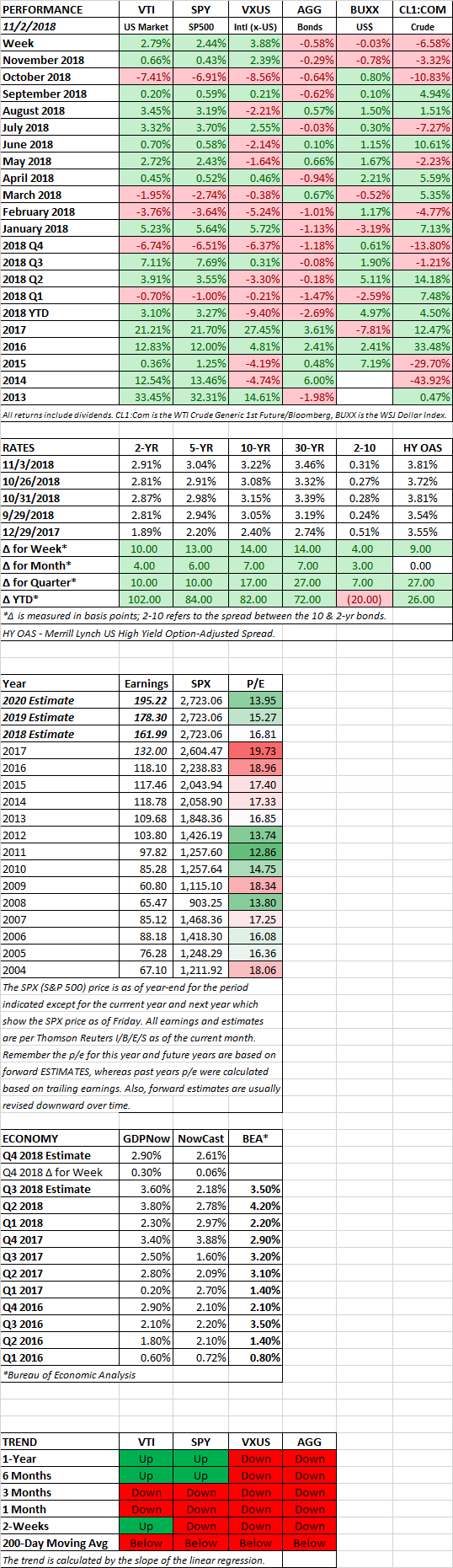

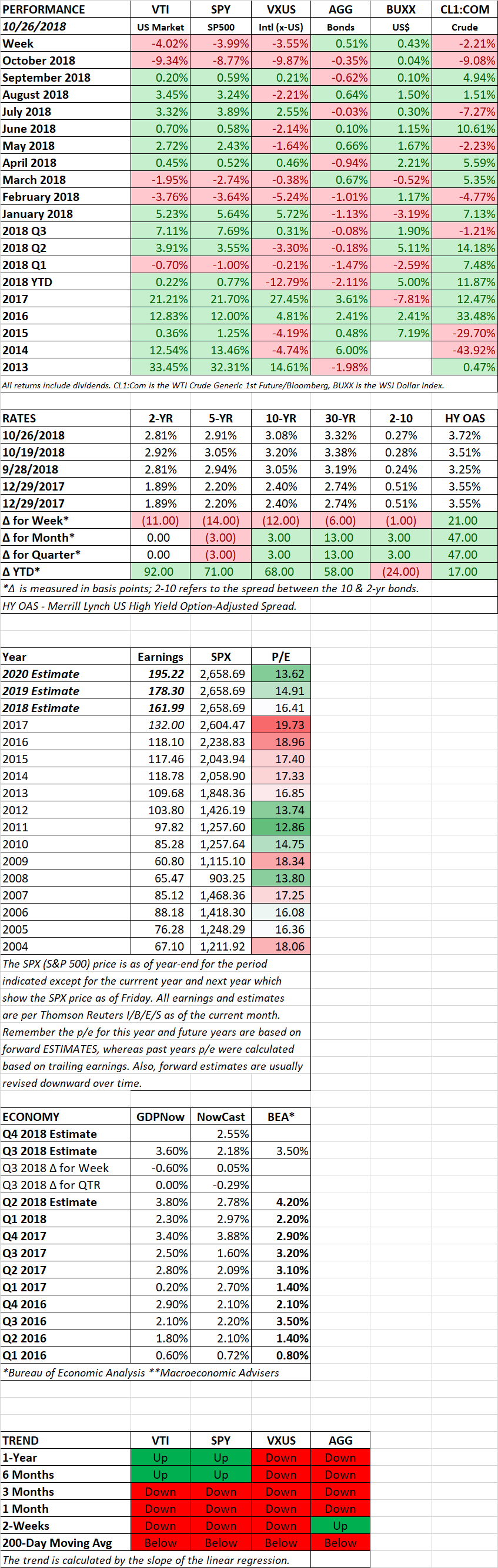

SCOREBOARD