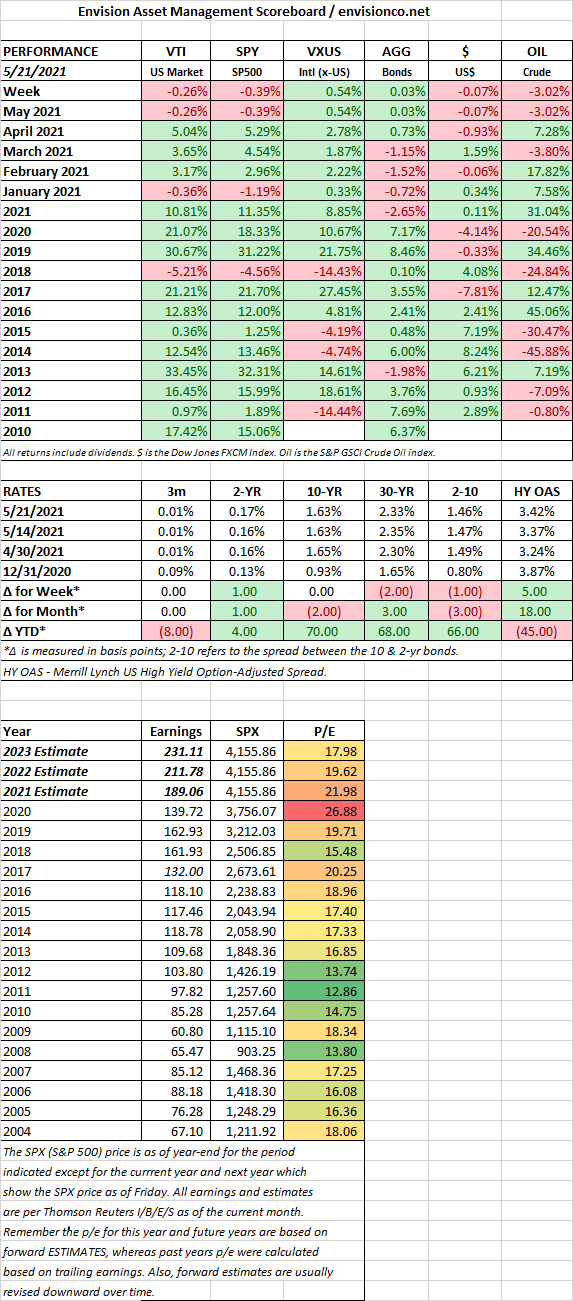

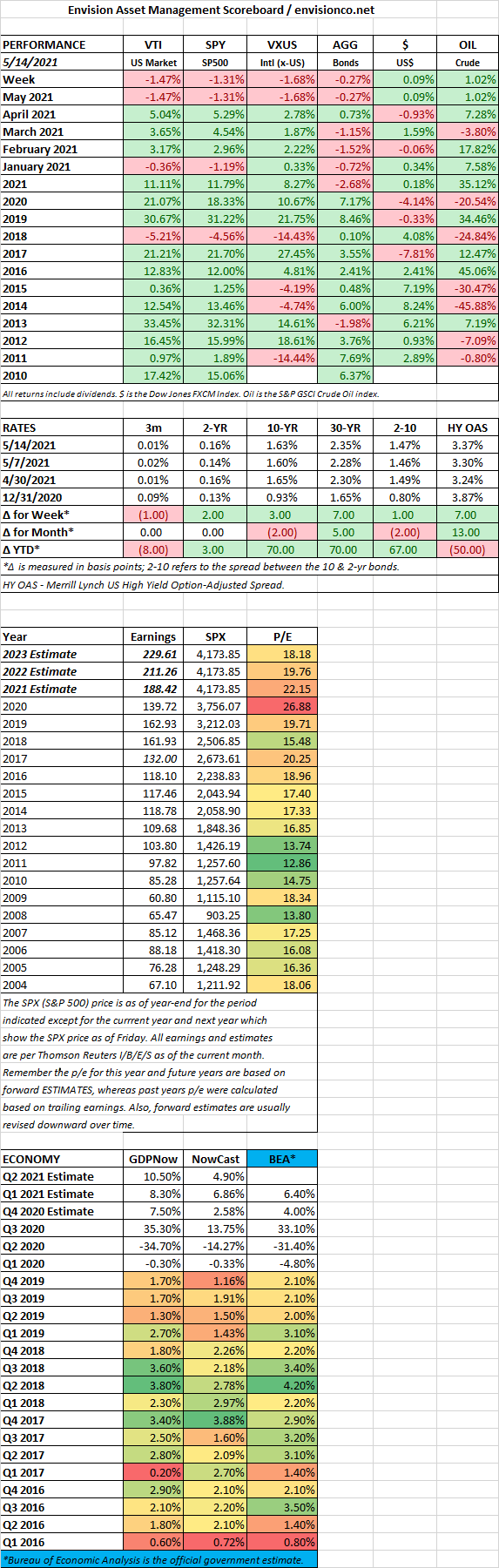

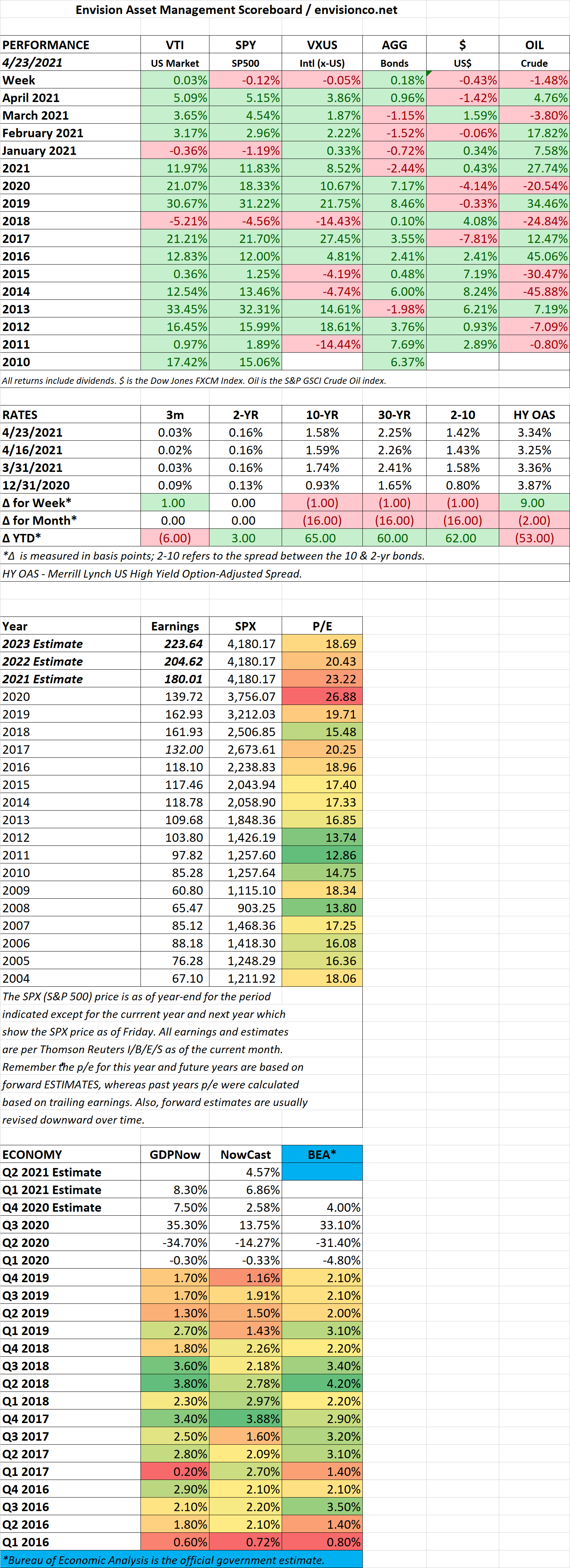

MARKET RECAP

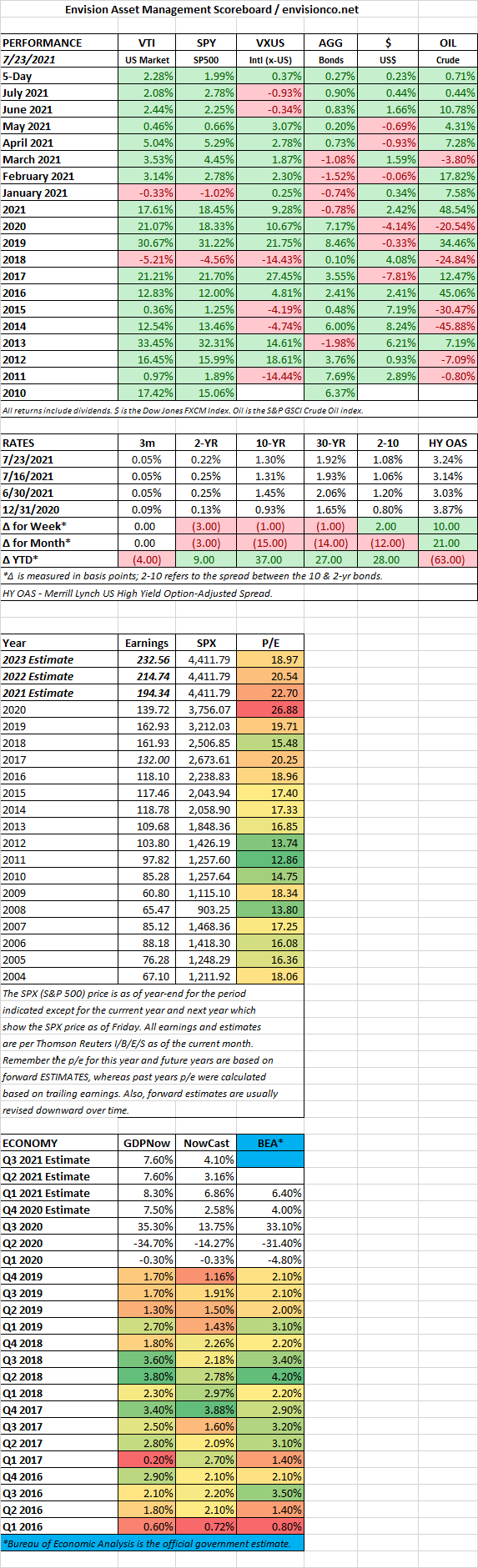

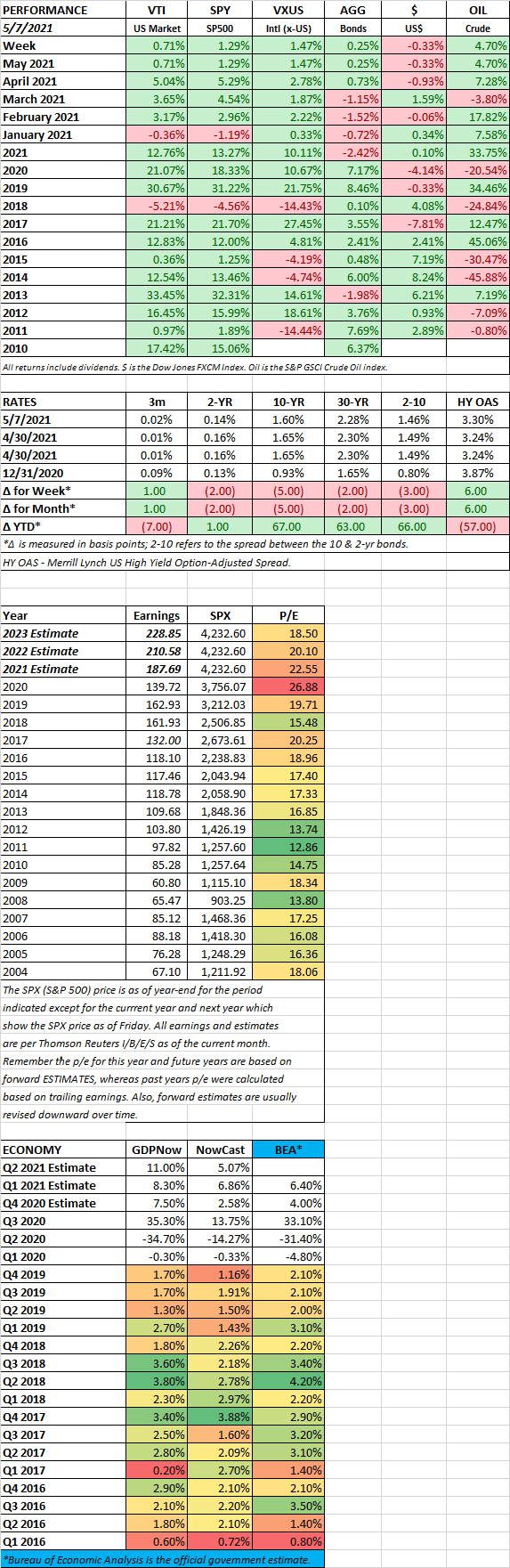

The market fell hard on Monday, dropping over 2%, but after that the bulls took control. The market was up by 2.28% for the week and closed at another high. The Dow broke the 35,000 barrier. The market scare on Monday was due to fears of a spreading Covid Delta variant and its potential slowdown of the economy. The virus tripled in case count over the previous two weeks. The 10-year yield dropped to a stunning 1.13% yield.

But then the “buy the dip” investors got to work, investing about $7 billion in ETFs. That stock market rally coincided with the 10-year returning to where it closed the week before, at a 1.30% yield, just off by one basis point. Strong earnings also helped. 85% of the 110 companies that have reported earnings have beaten forecasts.

The IHS Markit US manufacturing purchasing managers index hit a record high, powered by a surge in new orders. On the job front, the reports were mixed. On one hand, the number of people receiving jobless payments hit a post-Covid low, but new applicants rose by 51,000. The increase in new applicants was blamed on the auto industry due to supply constraints, mainly chips.

SCOREBOARD