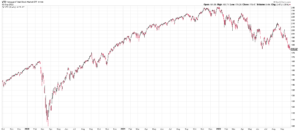

MARKET RECAP

Stocks managed to advance by 1.63% for the week. The market was strong at the beginning of the week on another hope that the Fed will pivot sooner rather than later, but as that became apparent that was more hope than real, the market fell hard at the end of the week.

Employers added 263,000 jobs in September, less than the 315,000 added in August and lower than the six-month average of 400,000, but more than the consensus estimate. The unemployment rate fell to 3.5% from 3.7%, matching a half-century low. The labor force participation rate declined. The stronger than expected report sparked another sell-off in the markets, worried that the slowdown in forthcoming interest rate increases in now further away. The S&P dropped by 2.8% and the Nasdaq fell by 3.8%.

Cracks continue to appear in the economy. AMD, Samsung, and Micron Technology have all issued weak forecasts.

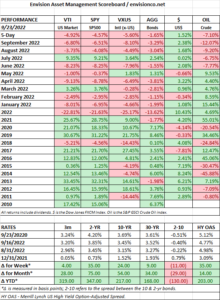

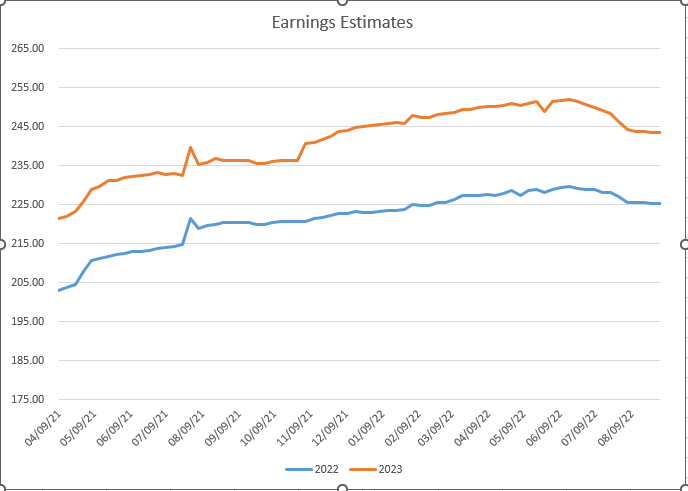

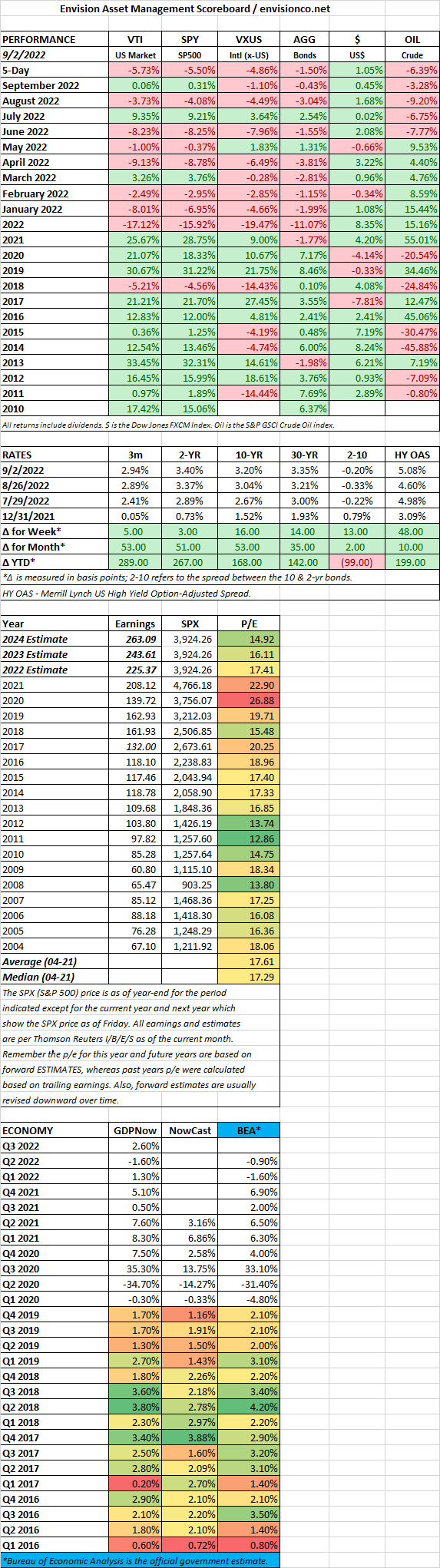

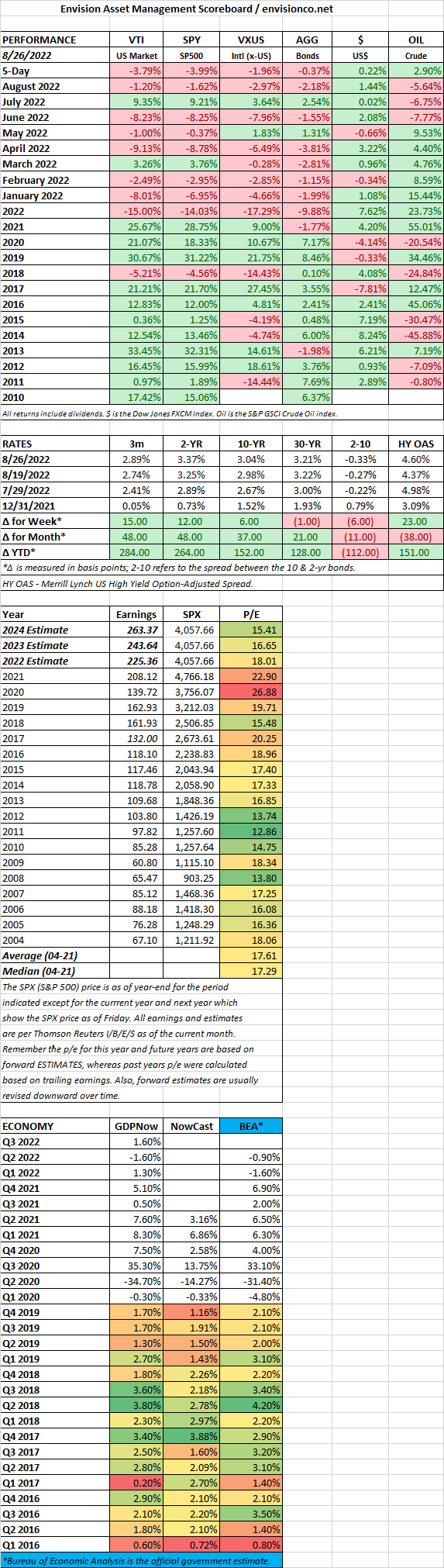

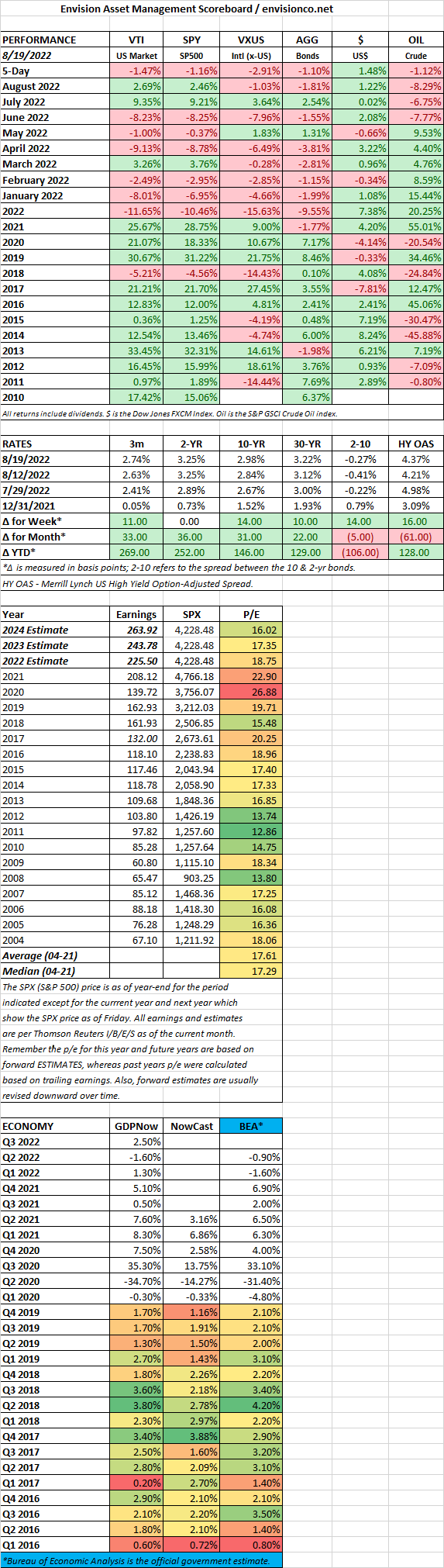

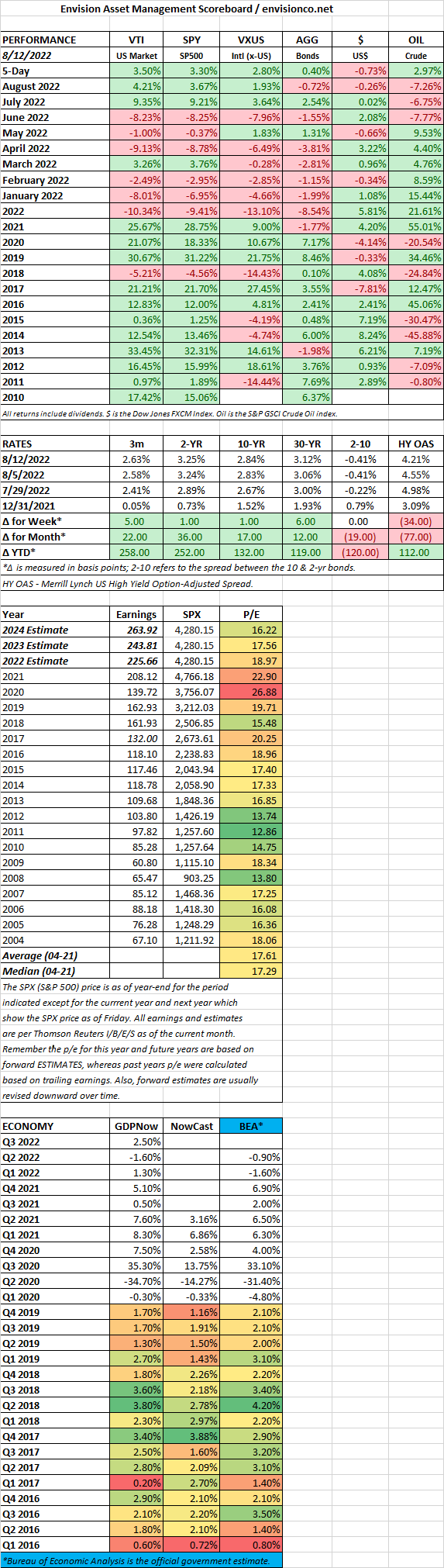

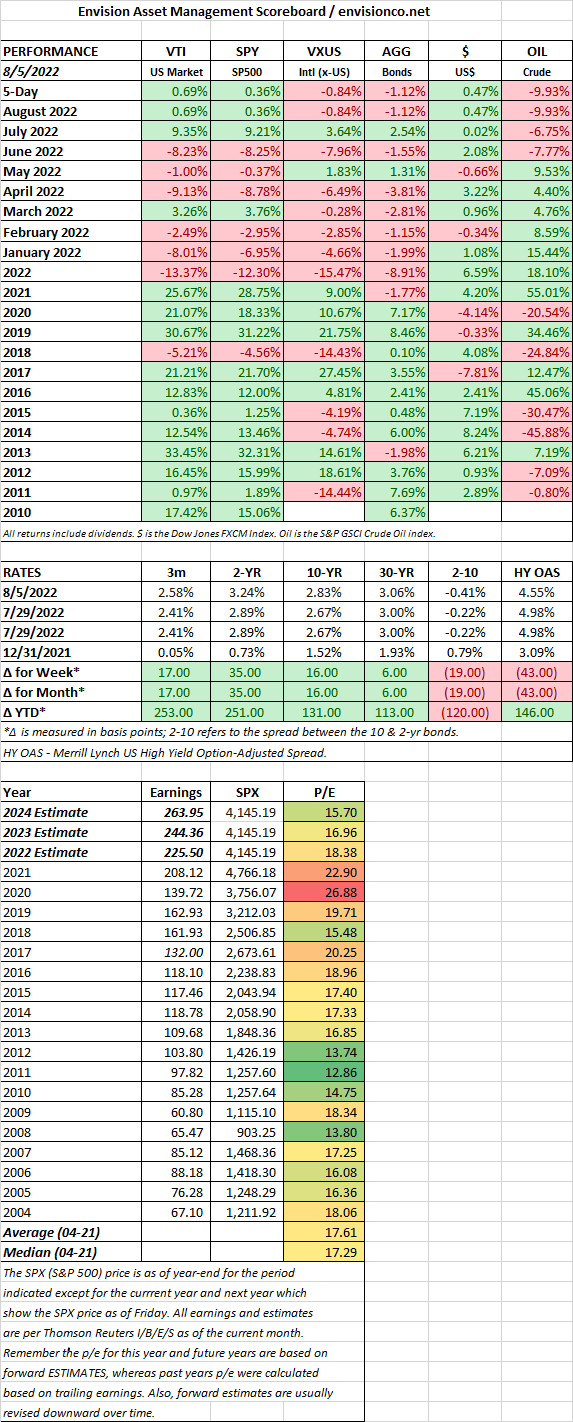

SCOREBOARD