SCOREBOARD

SCOREBOARD

MARKET RECAP

SCOREBOARD

MARKET RECAP

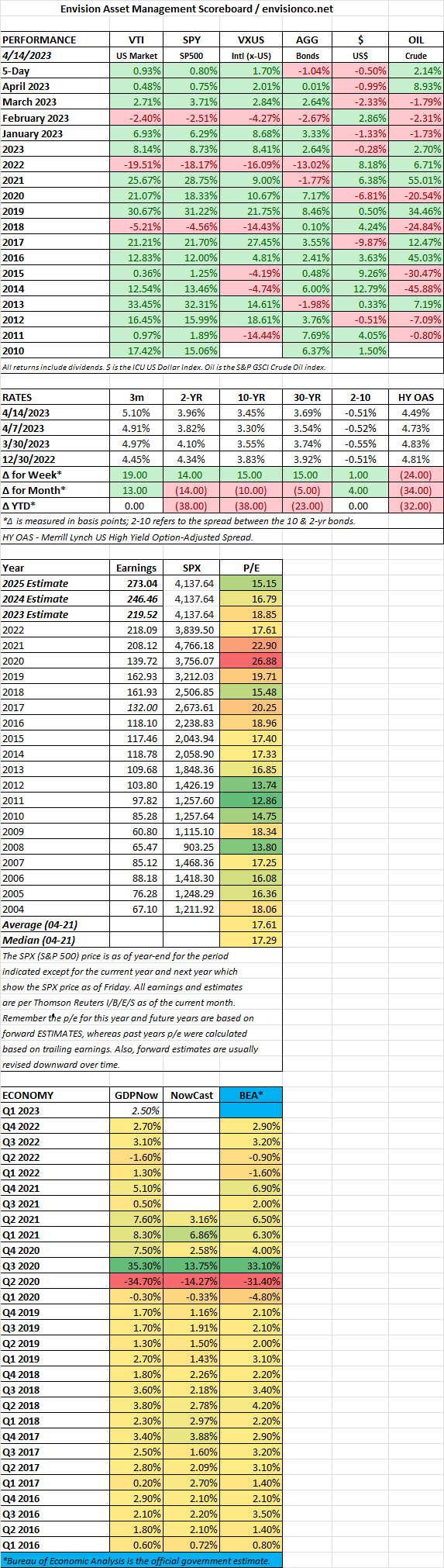

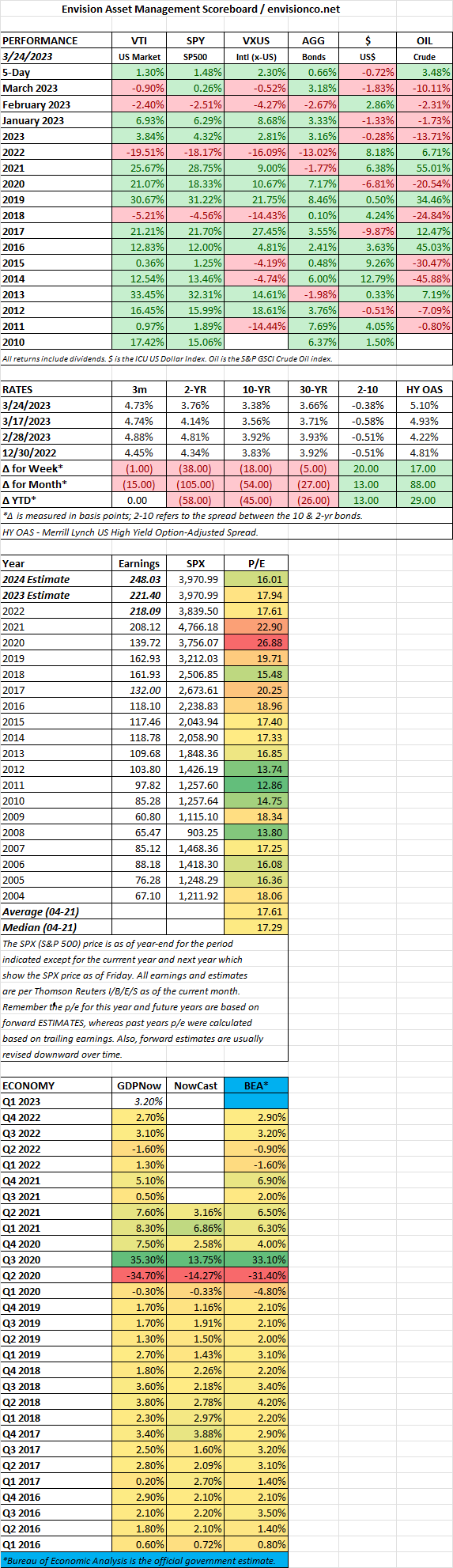

A big week for stocks as US markets rallied by 3.64% and international stocks by 3.37%. Bonds were off by 0.52%.

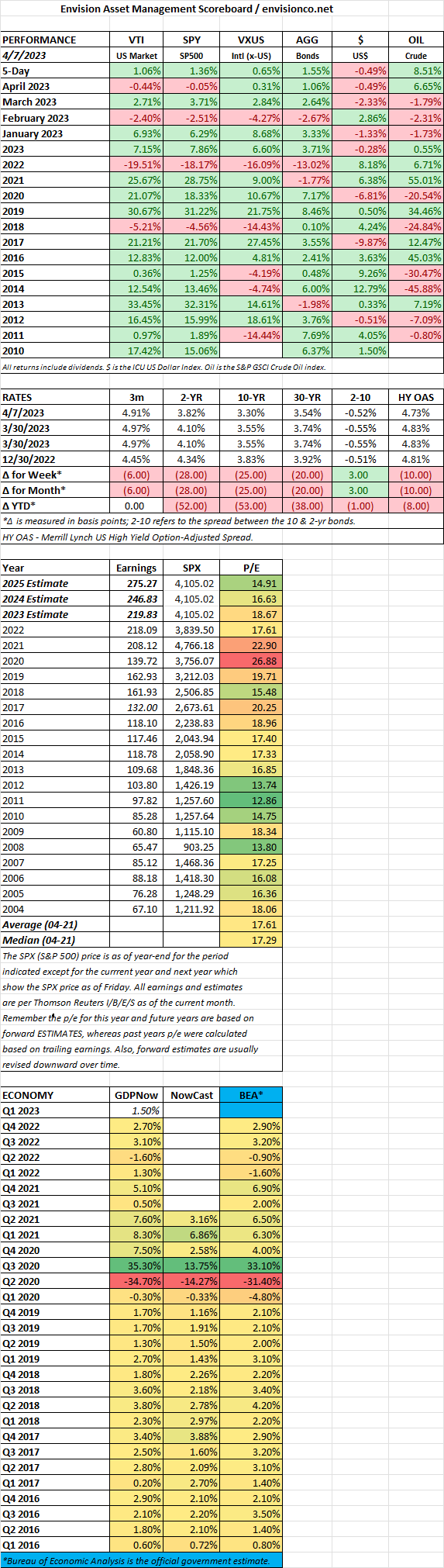

A winning quarter wrapped up on Friday, with US markets up by 7.2% and the Nasdaq up by 17%. Bonds also rallied for the quarter, up by 3.23%, as the 10-year yield fell from 3.826% to 3.491%. The much-feared recession has yet to arrive, and the labor market is still strong. The Fed has continued to raise rates, but that did not stop a winning quarter. Estimated earnings for the quarter just ended are expected to drop by 4.6%, following a 3.2% decline in Q4. But investors seem to be looking past all of that.

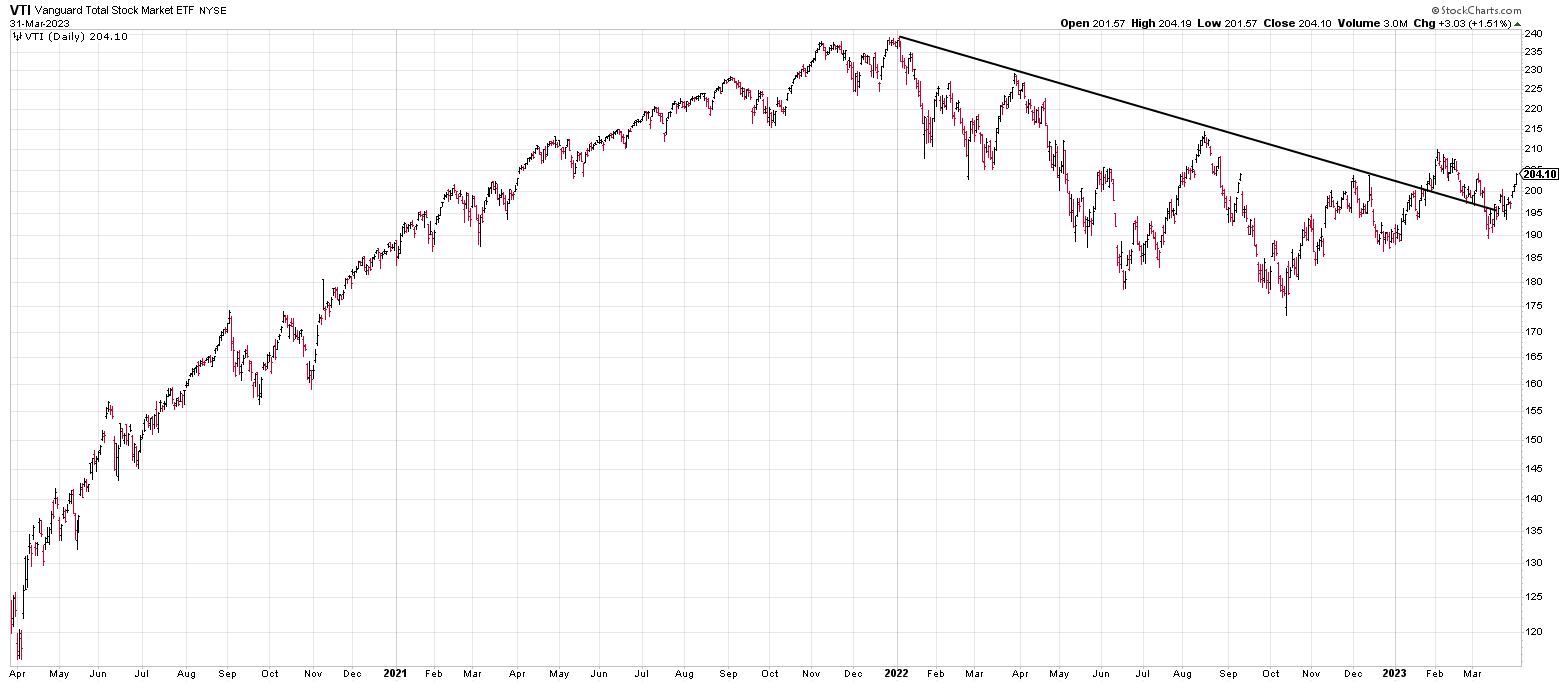

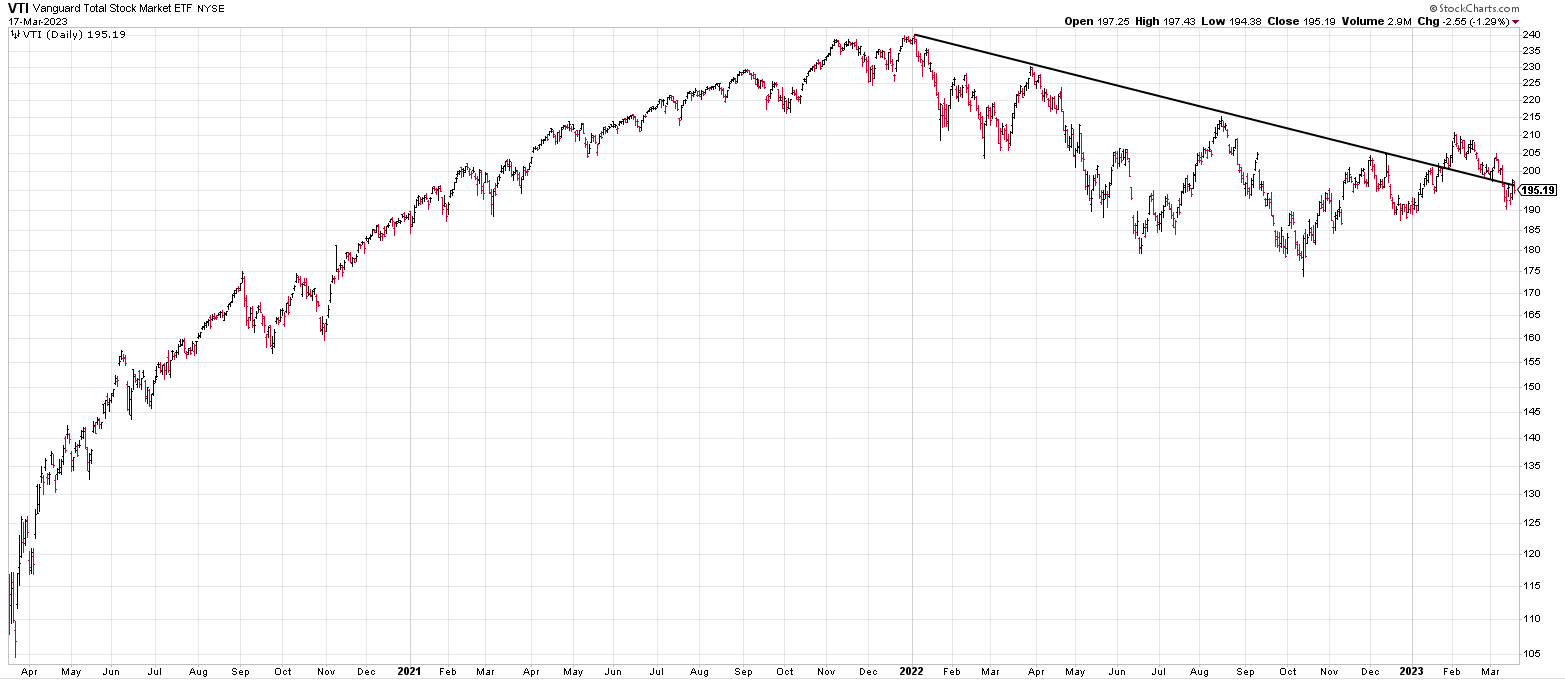

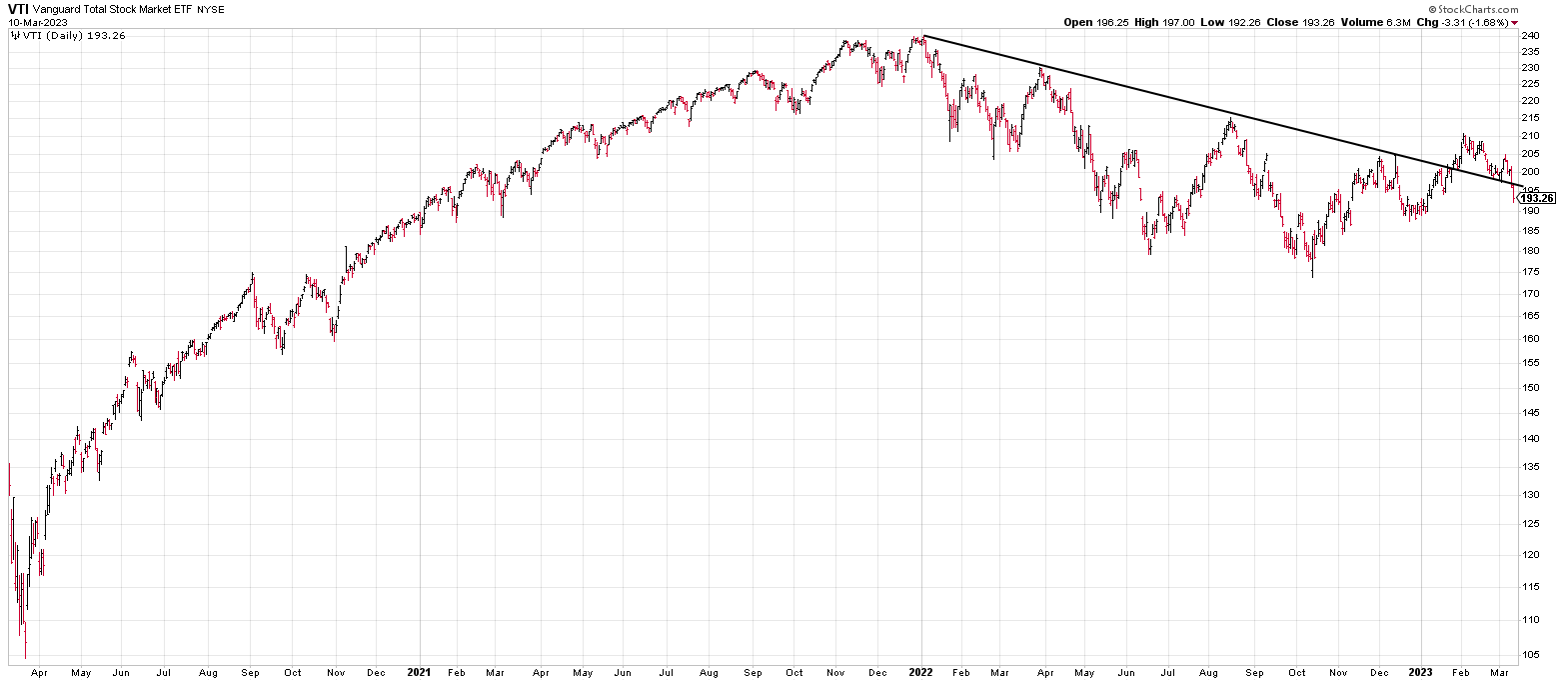

For all the predictions by the “experts” that the market will turn down with all of the bad news, stocks have taken a near-term turn upwards and are back up the declining trend line.

SCOREBOARD

Following February’s pullback, March saw a rebound in sentiment for financial markets, albeit amidst new concerns. Here’s a breakdown of the key highlights:

Equity Market Bounce:

Fading Concerns Over Inflation:

Central Bank Tightrope Walk:

Banking Sector Stress:

International Markets Uptick:

Other Notable Events:

Overall, March was a month of renewed optimism for financial markets. The fading threat of inflation and cautious central bank actions allowed for a rally, despite the temporary shock of the banking crisis. However, uncertainty remains regarding the sustainability of the uptrend, with factors like geopolitics and potential economic headwinds playing a role.

MARKET RECAP

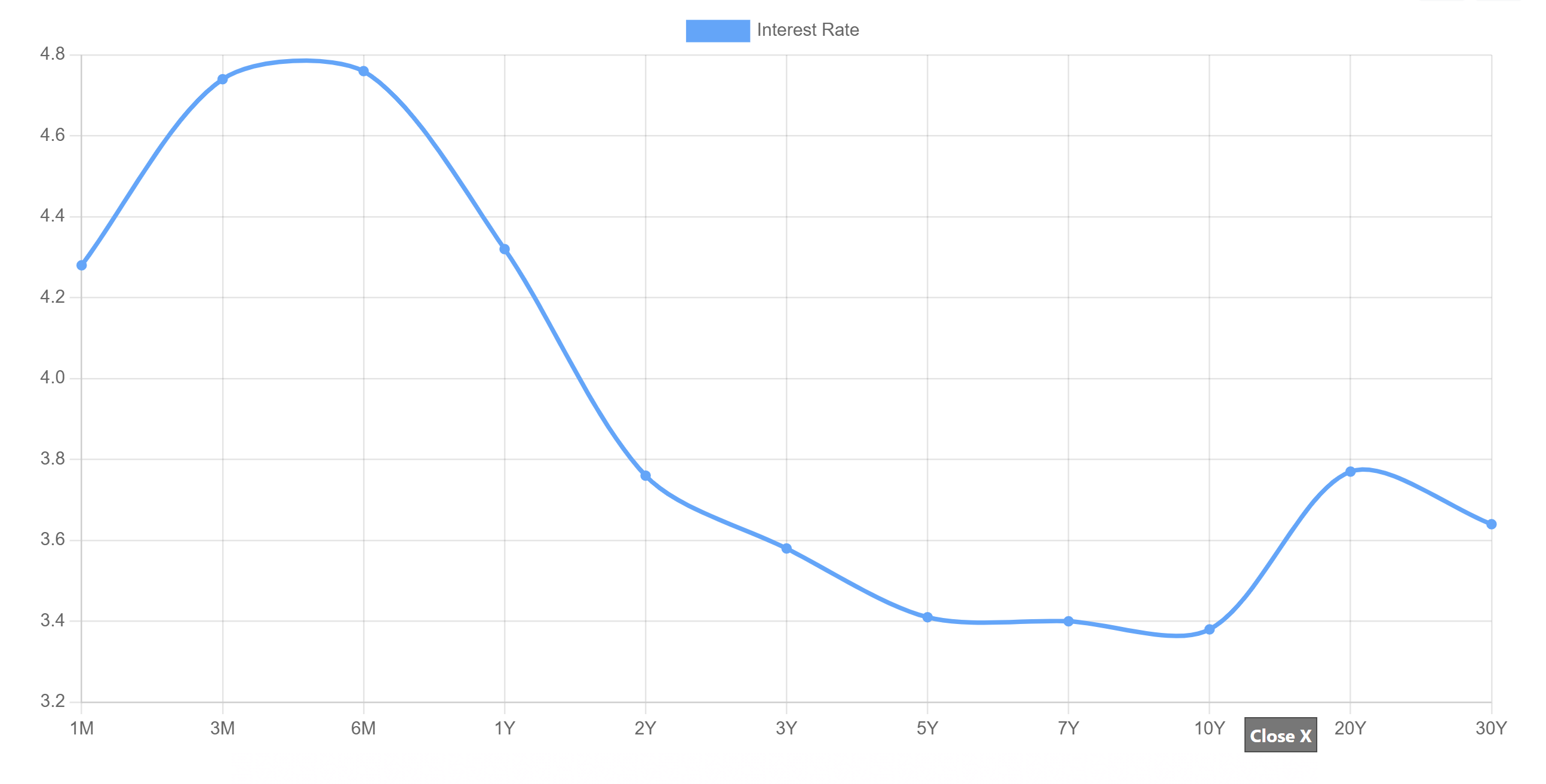

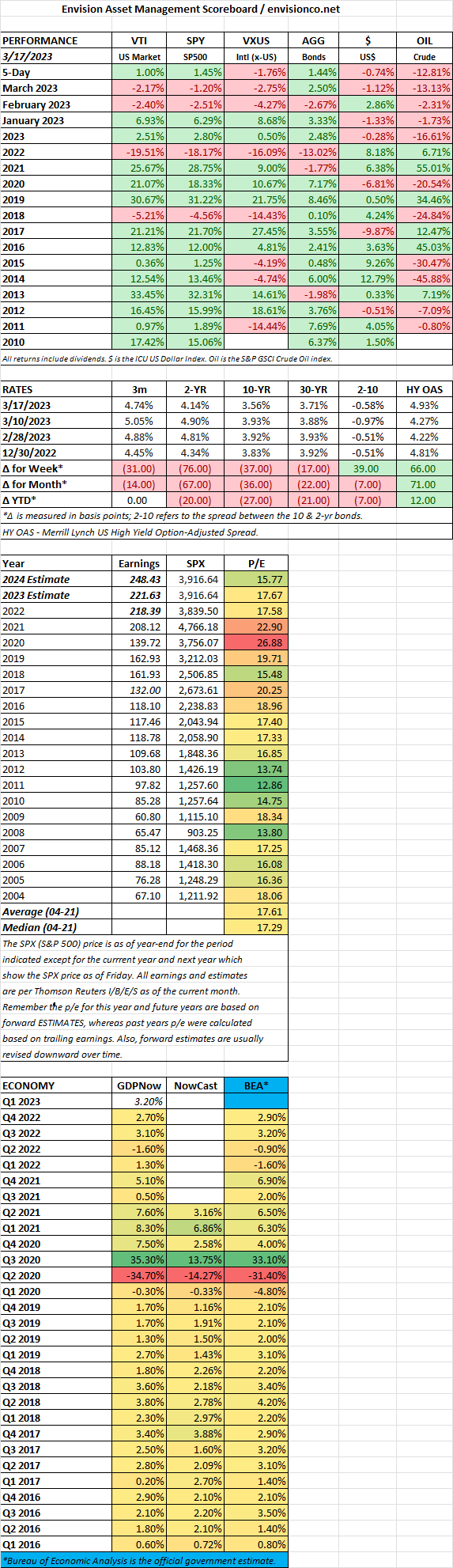

US stocks managed a gain for the week as the S&P 500 finished up by 1.48%. Bonds also were up as yields fell slightly. The 2-year yield fell five basis points to 3.76%. The peak on the curve is about 4-5 months out at 4.8%.

The scare in banking is hurting financing. No investment-grade credit has been issued since the collapse of Silicon Valley Bank. In the high-yield market, the percentage of distressed issues yielding 10% or more compared to equivalent Treasuries’ increased to 10.6% from 7.8% seven trading days prior. Some economists estimate the hit to the economy would be the equivalent of raising rates by 1/2 point to 1.5 points. Even with that, the Fed went ahead this week and raised rates by 1/4 point.

An aggregate M-Score for almost 2,000 companies shows the probability of fraud in the group is at the highest level in 40 years. The M-Score, developed by Messod Beneish from Indiana University, worked with several co-authors to measure the aggregate score. The M-Score received prominence for spotting problems with Enron three years before its collapse. It measures if companies are getting too aggressive with their accounting and/or committing fraud. The metric often rises rapidly before a recession.

All in all, the probability is increasing that a recession is coming.

One big winner is gold; GLD is up by 9.5% year-to-date.

SCOREBOARD

MARKET RECAP

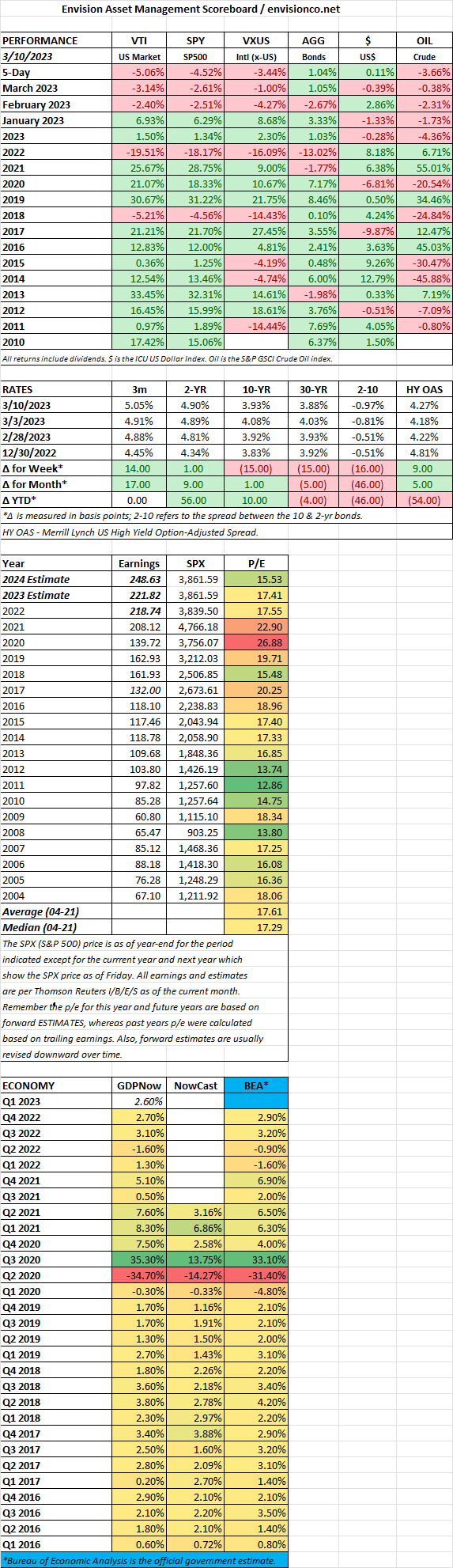

In the midst of the continuing bank chaos, gold hit an 11-month high, and bitcoin rose to over $27,000 from about $20,000 last week. The S&P was up 1.4% for the week but down 3.2% over the past two weeks. The Nasdaq is up by 4.4%.

The Feds were active this week in trying to keep bank depositors calm to stem a run on the small banks. Signature Bank was taken over, and 11 major banks deposited $30 billion in First Republic Bank to help keep the bank afloat. A program was put in place to lend money to banks in need. Then the Swiss central bank had to back Credit Suisse Group to the tune of $53 billion. Treasury Secretary Janet Yellen said, “Americans can feel confident that their deposits will be there when they need them.” The overall turmoil increases the odds of a recession.

At least for now, the bank problem is one of liquidity, not solvency.

As quickly as bank stocks were selling off, there was wild demand for Treasuries. Since March 8th, the yield on the 2-year treasury has fallen by 124 basis points from 5.05% to 3.81%. The 10-year has dropped from 3.98% to 3.39%. The three-month t-bill is now at 4.52% from 5.06%. Gold is up 8.4% and oil is down 13.4% in the last eight days.

But the overall market is not in panic mode. The VIX is at 25.5 and junk bonds trade in a normal range.

Commercial real estate might be the next big problem. They make up 24% of all bank loans, and many are at risk of default.

SCOREBOARD

MARKET RECAP

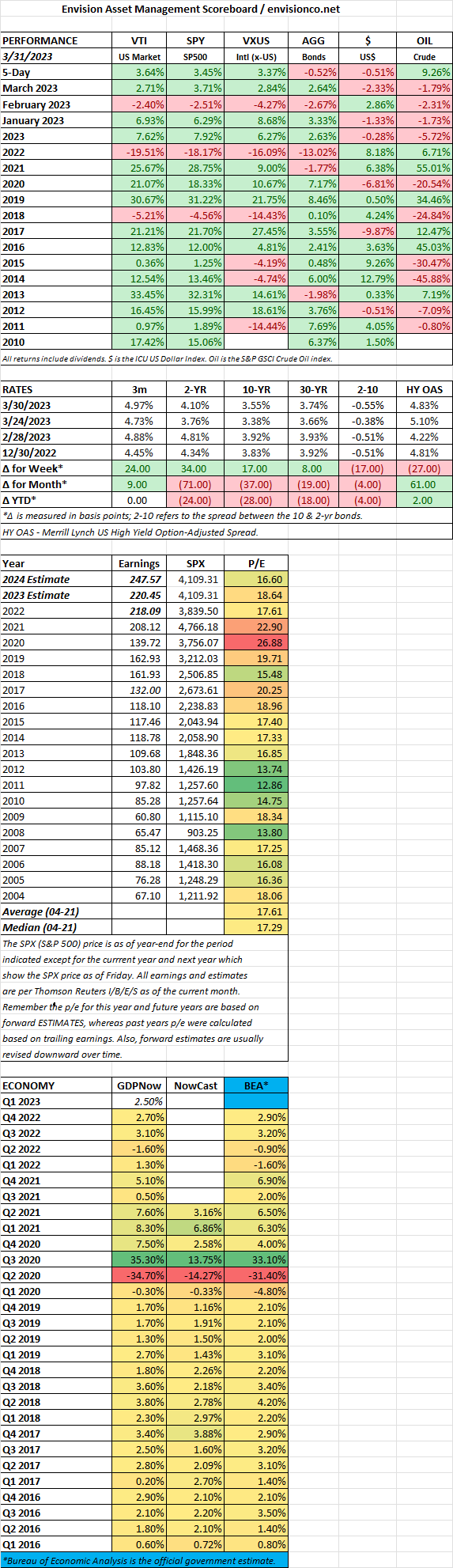

Stocks took a big hit, falling by 5.06% in the US and 3.44% outside the US. Bonds rallied on lower interest rates. The fall in US markets put equities back below the declining trend line and lower than the 200-day moving average. On Tuesday, Fed Chair Powell’s comments indicated a chance of a 50 basis point increase at the next Fed meeting, a hawkish stance. Then, on Friday, the Silicon Valley Bank (SIVB) failed.

SIVB was taken over by regulators. The bank had $200 billion in assets and was the second biggest bank failure of all time, trailing Washington Mutual ($300 billion) in 2008. The bank relied on private equity funding as compared to regular deposits while at the same time having a very high level of loans. The vast majority of the assets the funds held were classified as “hold-to-maturity,” which means the bank did not have to mark the bonds to market. Given the dramatic increase in interest rates, the bonds had substantial unrealized losses. It wasn’t that the bonds were not creditworthy, just that the duration mismatch (holding long-term assets while having short-term liabilities) left SIVB susceptible to a bank run, and that is what happened. Even before the “run,” customers pulled money from SIVB to get higher interest rates elsewhere. What happens now remains to be seen. But the first casualty might be the Circle stablecoin, which had $3 billion of its $40 billion in reserves at the bank.

The failure sent yields plunging. The 2-year treasury yield fell by 31 basis points on Friday to 4.59% and 45 basis points over two days.

The February jobs number outpaced estimates. Nonfarm payrolls were up by 311,000 compared to the estimate of 215,000. The rise in average hourly earnings was only 0.2%, less than expected. And there was higher participation. Overall a good report, but the bank failure entirely overshadowed this.

SCOREBOARD

MARKET RECAP

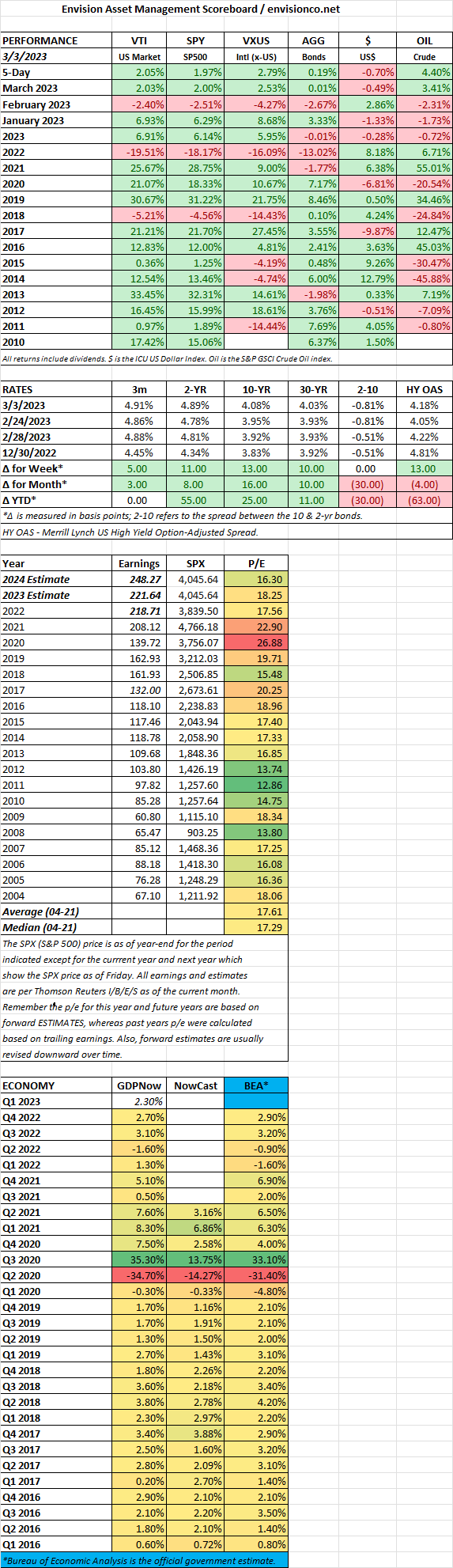

Stocks moved ahead for the week, in the US at +2.05% and outside the US at +2.79%. The market is still trading at a somewhat high level, given where interest rates are. The 5.3% earnings yield on the S&P 500 is barely above the almost 5% that treasuries yield going out up to 2 years. This is a divergence that, over the long run, likely won’t hold.

The market expects rates to top out at 5.25% to 5.5%, with the next hike to be 25 basis points. But with a hotter-than-expected economy, there is now a push to go for 50 basis points.

The economy, so far, is still advancing. The Atlanta Fed GDPNow shows Q1 GDP at 2%+, and the ISM services index stayed at 55.1, indicating an expanding economy. At the same time, though, the ISM manufacturing index is 47.7, indicating a contracting economy. Global PMI is now north of 50.

Warren Buffet took a direct shot at President Biden when he said in his annual letter, “We you are told that all [share] repurchases are harmful to shareholders or to the country, or particularly beneficial to CEOs, you are listening to an economic illiterate or a sliver-tongued demagogue.”

SCOREBOARD

After a strong January, February shifted sentiment for financial markets. Key themes for the month included:

Equity Market Pullback:

Rising Interest Rates:

Economic Resilience:

Global Market Performance:

Other Notable Events:

Overall, February was a month of adjustment for financial markets. The rally fueled by disinflationary hopes gave way to concerns about higher interest rates and the sustainability of economic growth.

Scoreboard