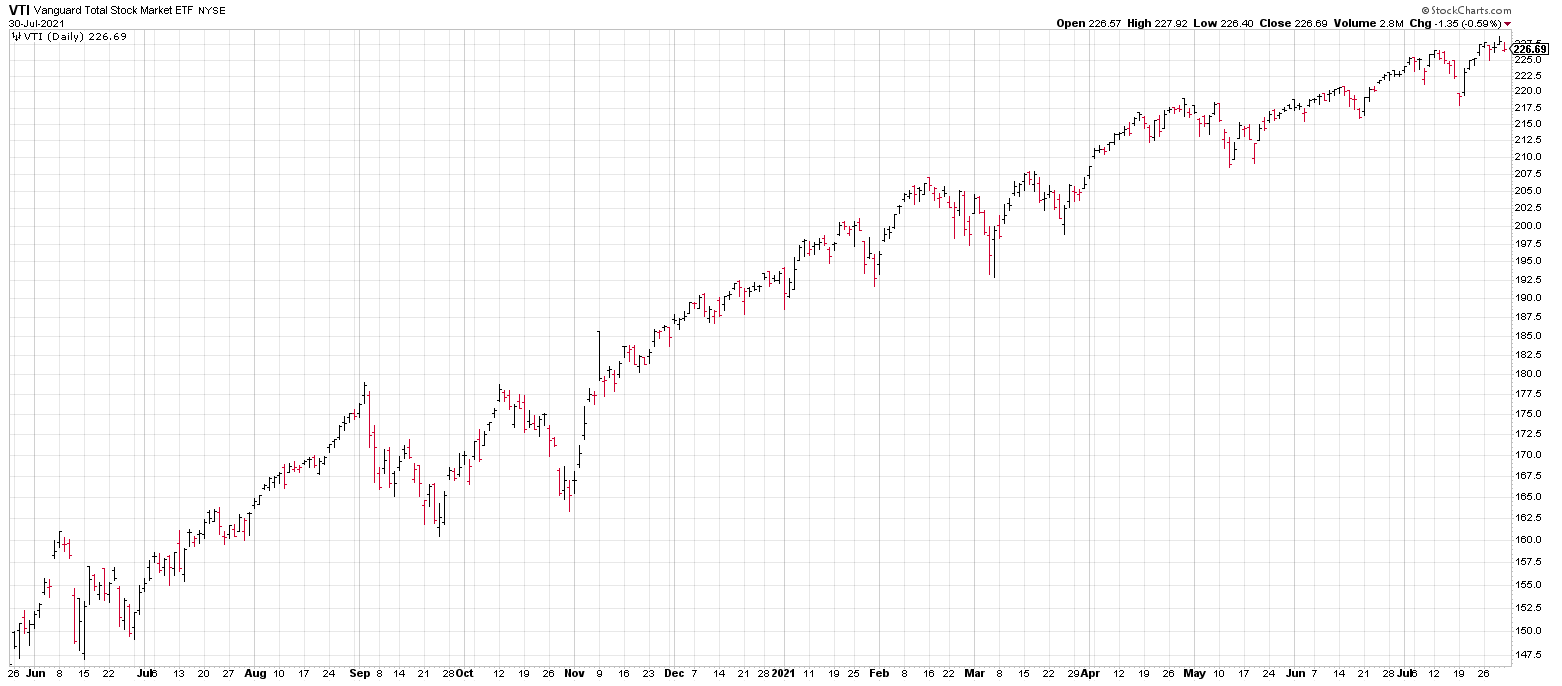

MARKET RECAP

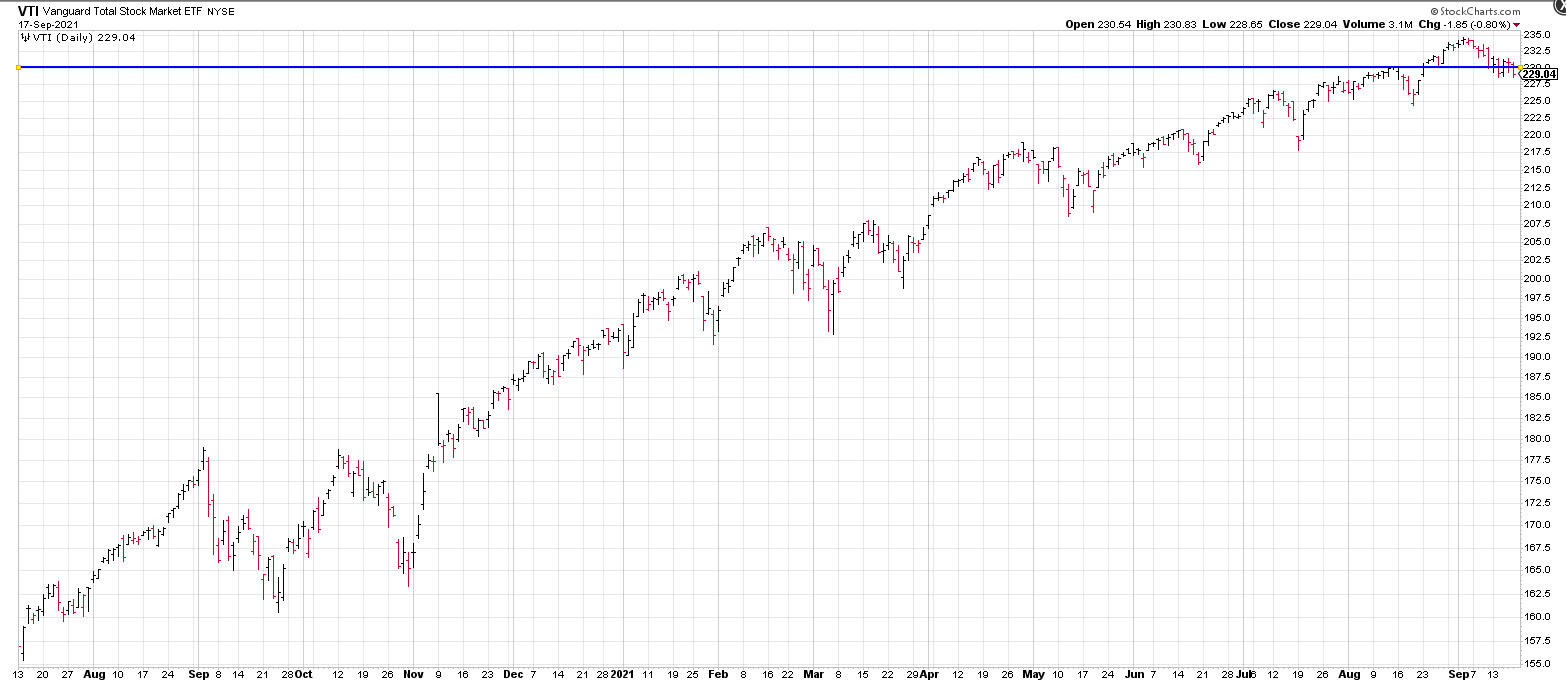

The market fell again this week, although not much, down by 0.45% in the US and 1.18% outside the US. High valuations, an economy that is still growing but slower than originally thought, inflation, proposed tax increases, and tapering around the corner have stalled the market out, at least for now. In what might be an ominous sign, the market did not hold support as we wrote about last week. Now stocks certainly didn’t collapse, but they finished the week just under the mid-August highs.

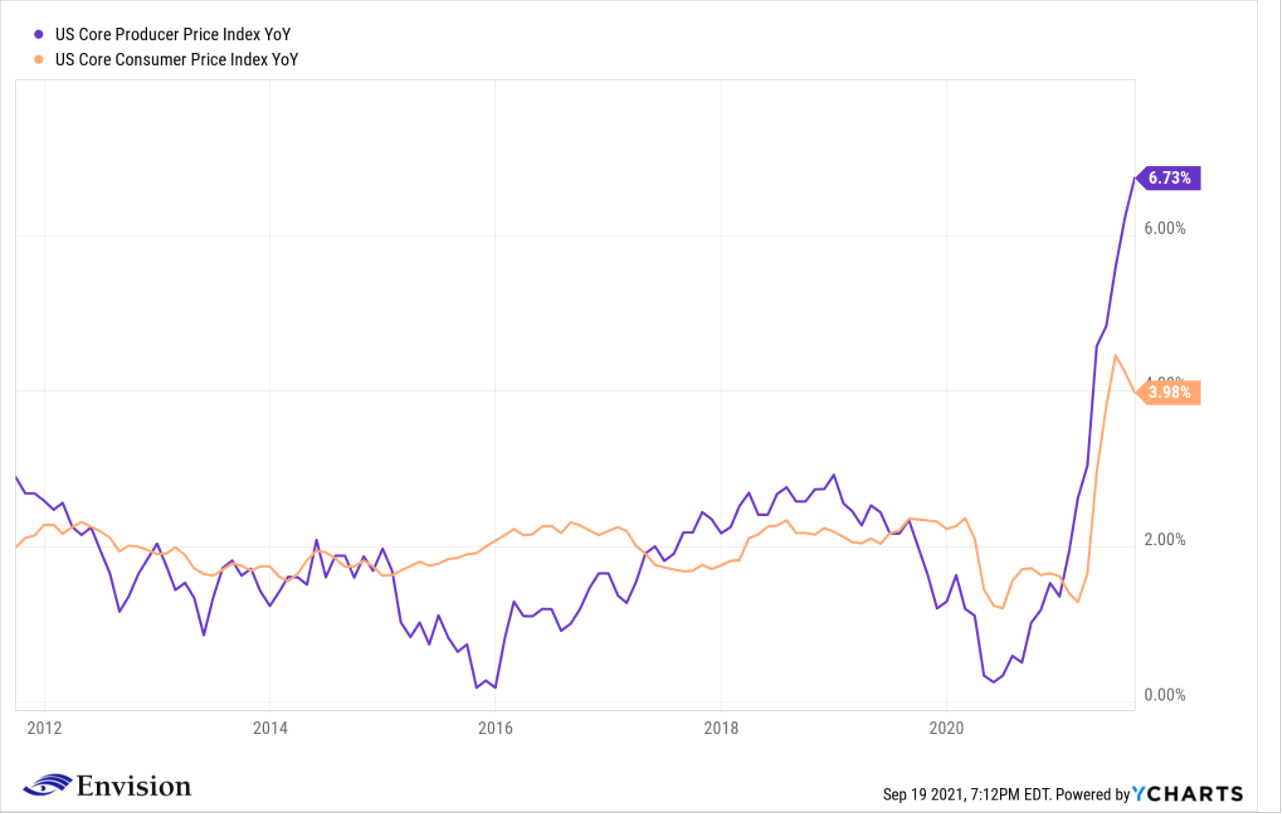

One problem is that producer prices (purple line below) have been rising much faster than consumer prices (orange line below), meaning that companies have not been able to pass on the rise in recent cost inputs. Should the higher inflation numbers turn out to be “temporary” than maybe the impact won’t be that bad, but if not, it will impact profits and growth.

Another issue is Evergrande, the huge Chinese property developer. With $300 billion in debt, the company is on the brink of default. For now, the Chinese government is playing hardball and has not indicated it will provide financial help, so there is the threat of a spillover into world financial markets.

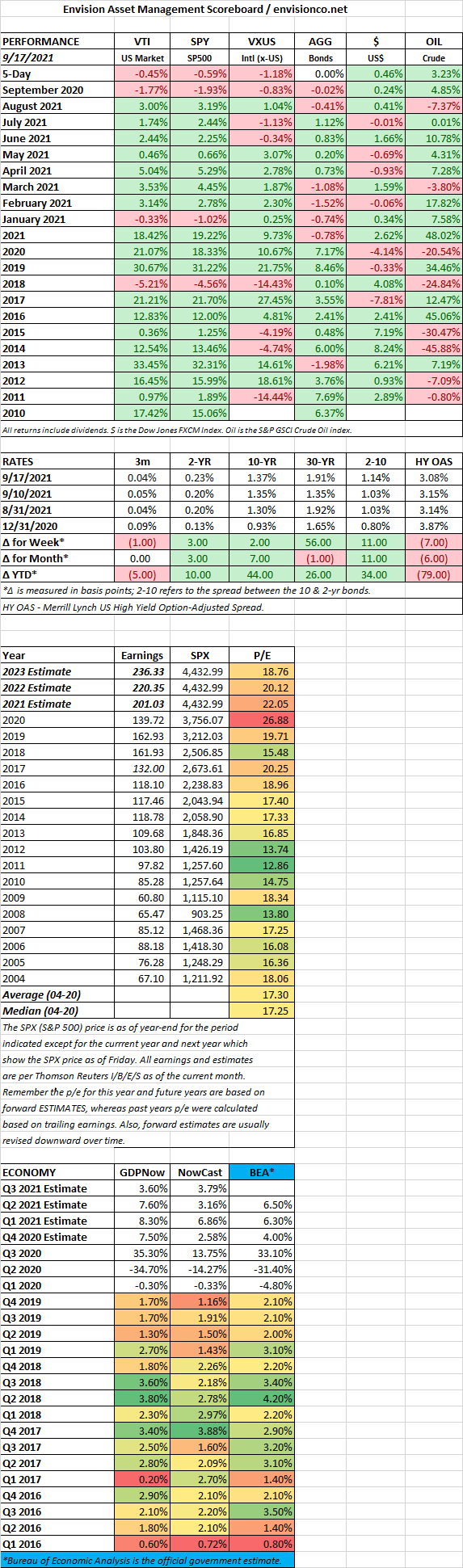

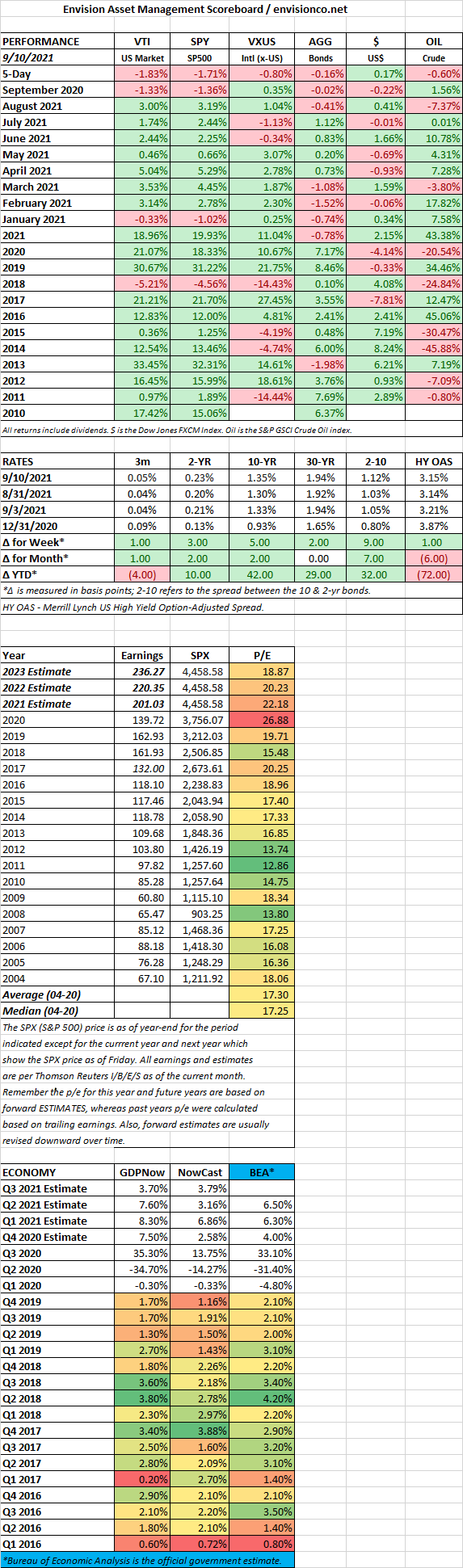

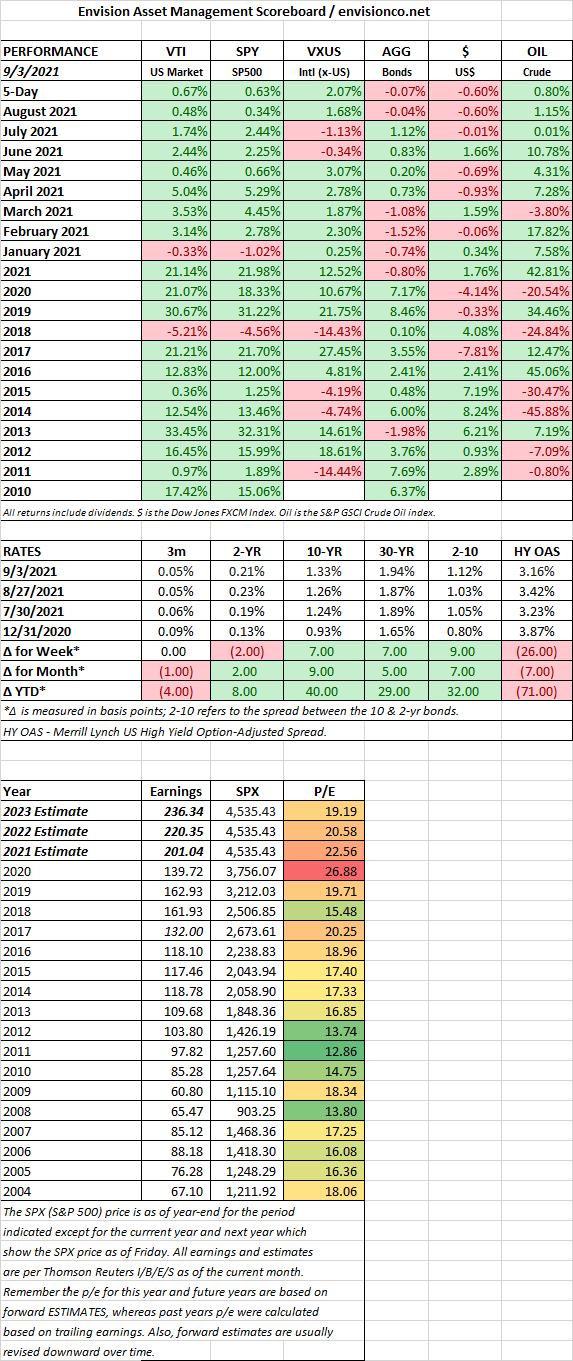

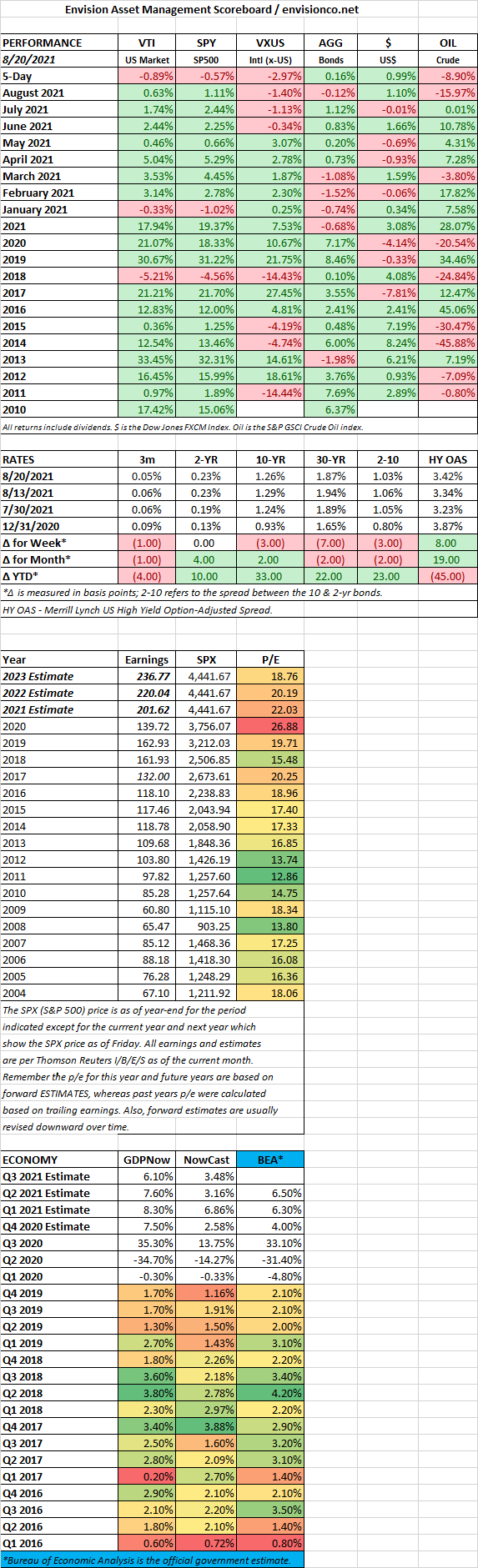

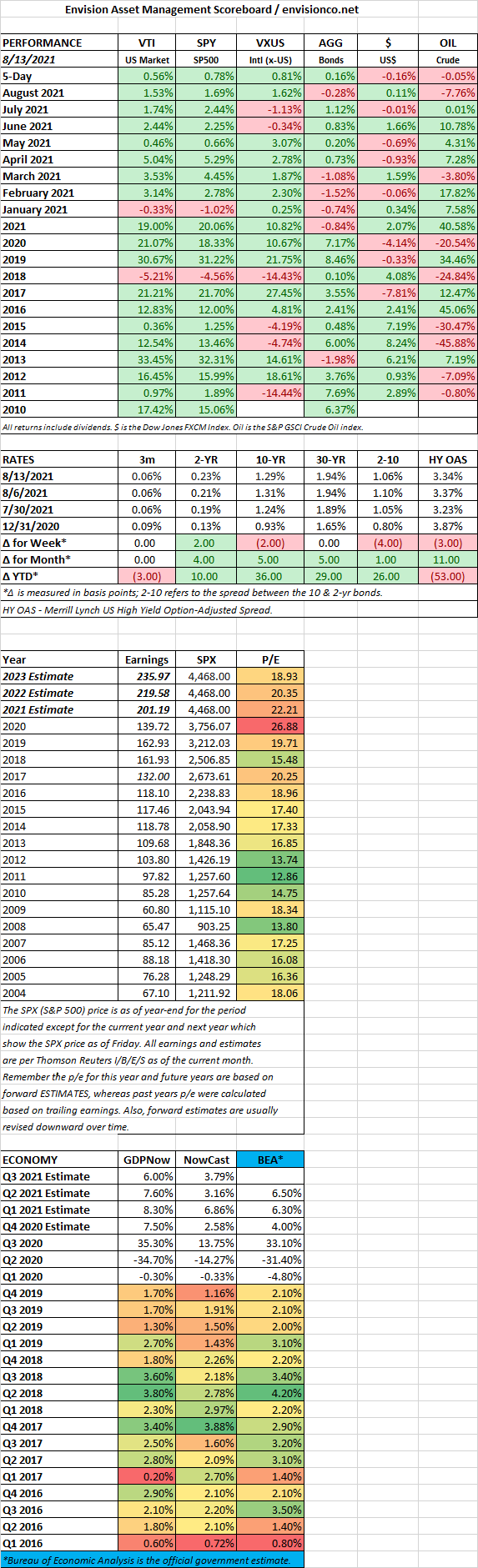

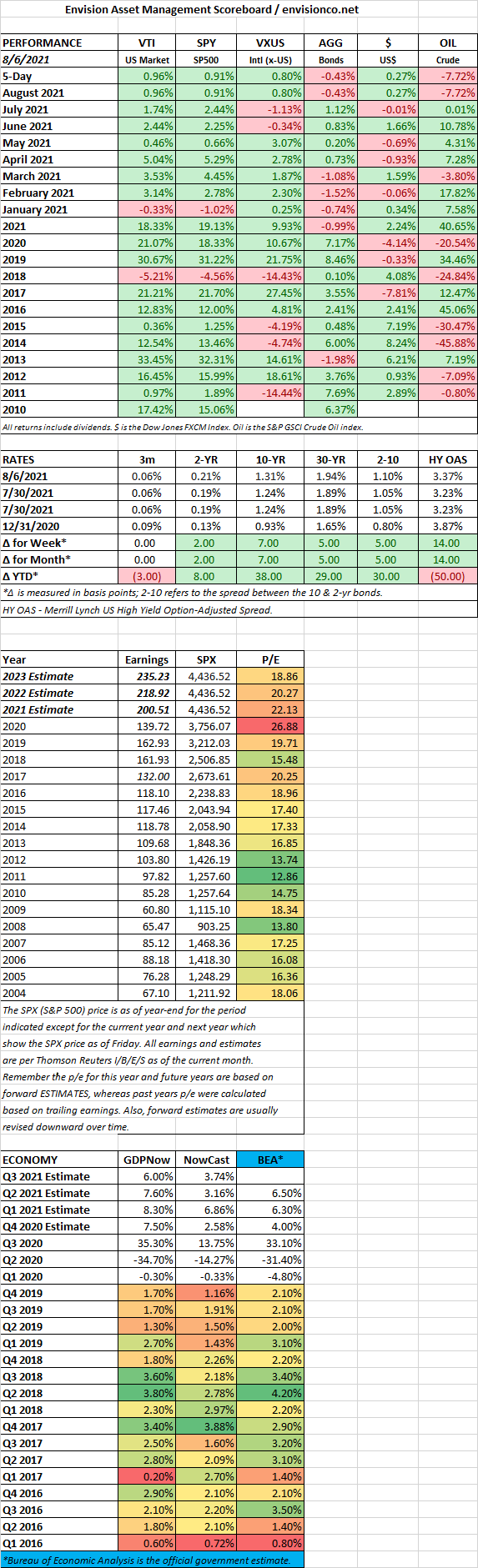

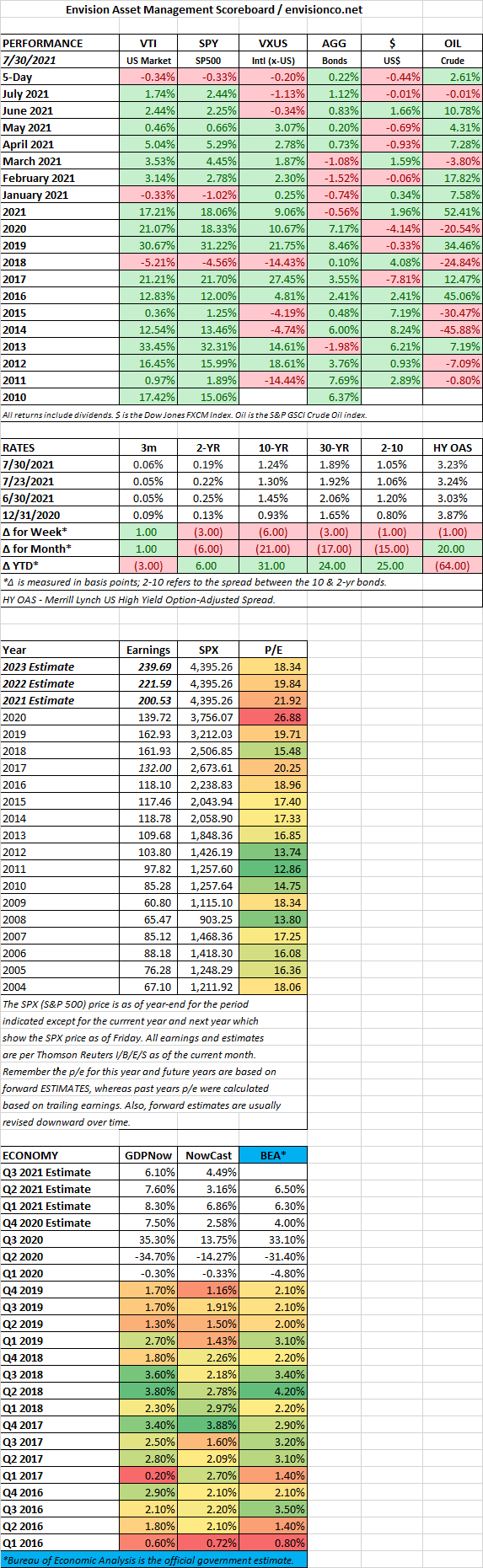

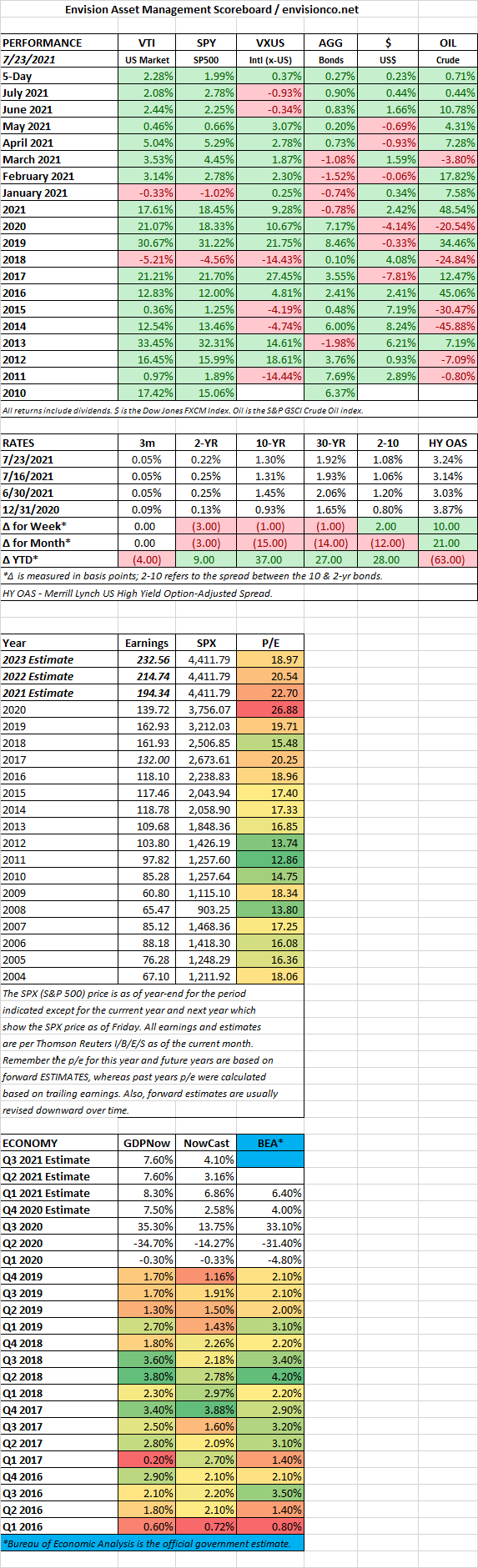

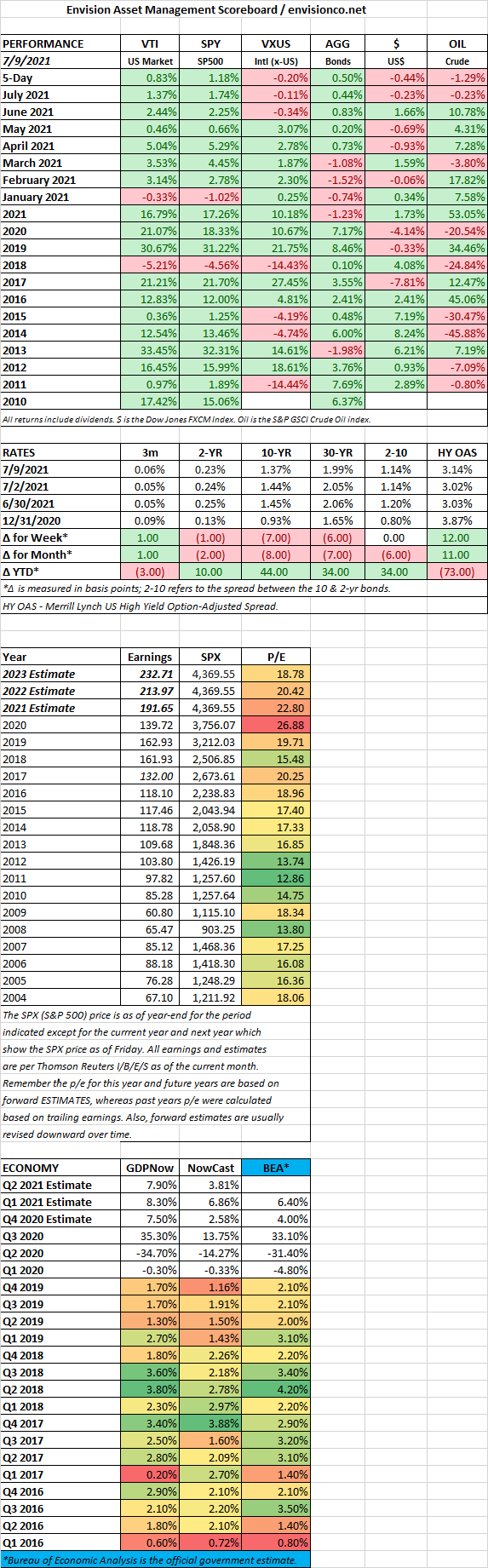

SCOREBOARD