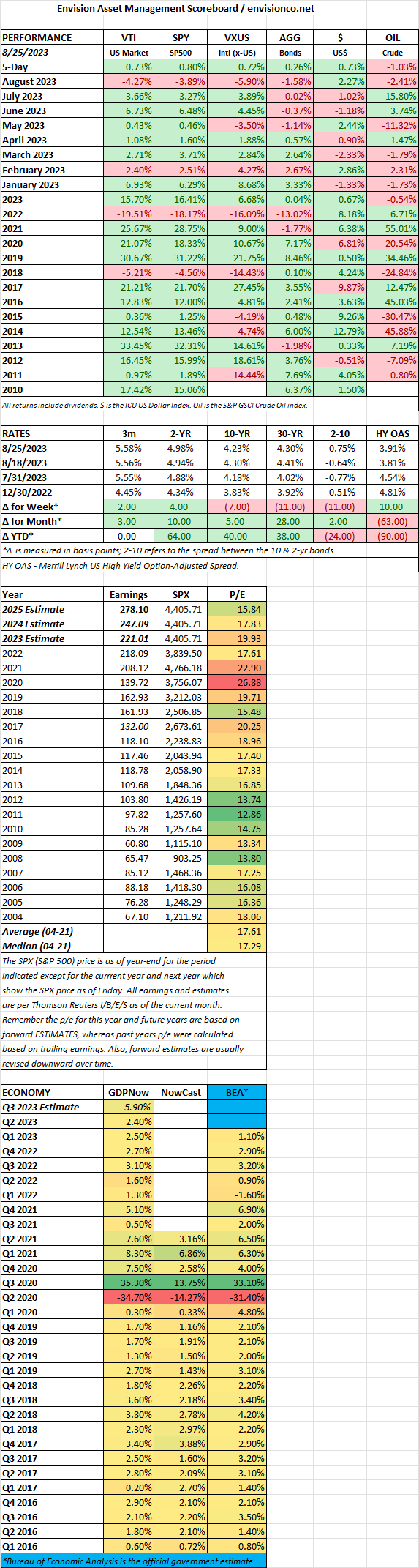

MARKET RECAP

- US stocks were up by 0.73%, international +0.72%, bonds +0.26% but for August, US equities are down by 4.27%.

- The 2-year yield is now at 4.98%. The 10-year is at its highest level since 2007 at 4.34%.

- Earnings estimates have been trending up for the last three weeks.

- The GDPNow estimate is ripping up at +5.9%, but two retailers, Macy’s and Dick’s, indicated some problems, higher theft, and credit card delinquencies. Dick’s missed estimates.

- Powell spoke on Jackson Hole and left open the possibility of a September increase.

SCOREBOARD