Tracy Alloway from Bloomberg writes about the collapse of FTX, the comparison to the Beanie Baby phenomenon in the ’90s, and how when speculation collapses, all that is left is the utility value, and if there no utility value, that means $0.

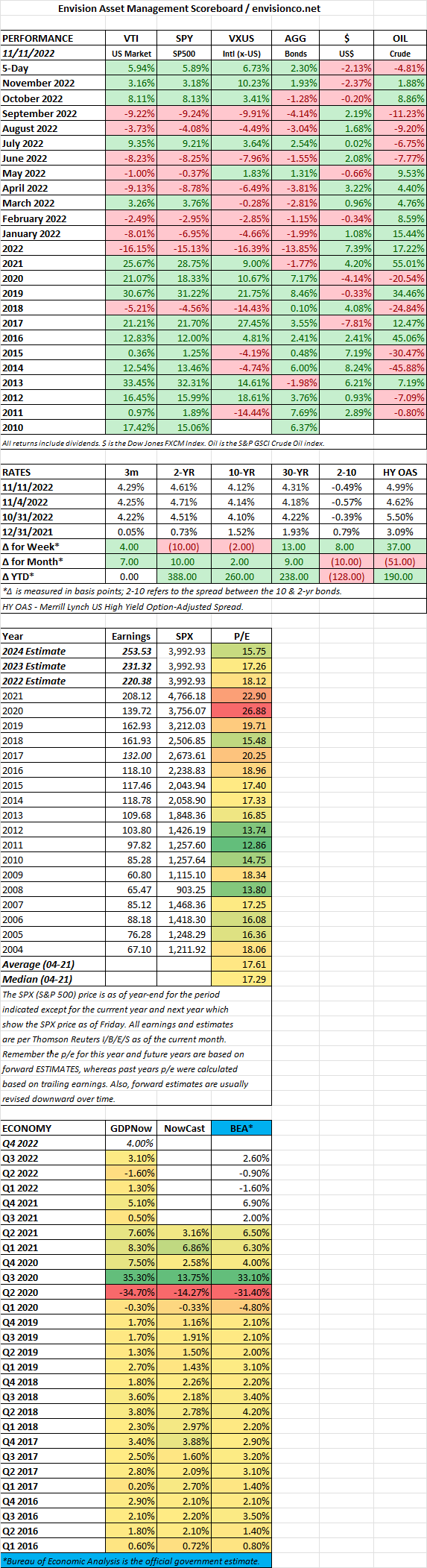

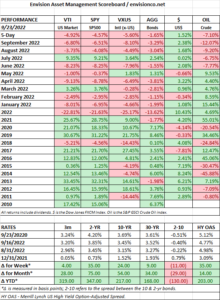

Week Ending 11/11/2022

MARKET RECAP

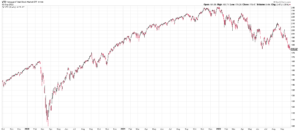

A big week for stocks worldwide as the inflation report came in slightly less than the consensus estimate. US markets were up by 5.94%, international stocks increased by 6.73%, and bonds rallied by 2.30% on lower interest rates. The October consumer price index was up by 7.7% compared to last year, below the estimate of 8%, and lower than the September print of 8.2%. Investors also will get a split government, as it looks like the House will slide just barely to the Republicans, and the Democrats will keep the Senate. That formula has generally worked out well for investors.

But the Republicans certainly were not happy with that outcome. It was a big underperformance given all the cards stacked up in their favor. At some point, the Republicans have to finally get the message, that Trump has been a disaster for their electoral hopes since he was elected back in 2016. In the 2018 mid-terms, despite a strong economy, the GOP lost 41 house seats. He lost the 2020 presidential election. When it was discovered that he was pressuring state officials in Georgia to turn the vote in his favor, his actions probably cost the GOP the Senate runoff. And then this past week, most of his endorsed candidates failed miserably in elections that would have been winnable with normal, sane candidates. Despite high inflation, high mortgage rates, the threat of a recession, and an unpopular President, it looks like the Democrats will only lose about 11 House seats, and they held on to the Senate, in what should have been a big year for the Republicans.

The Crypto world continues to fall apart. In an incredible turnaround from King of the block (chain) to bankruptcy, FTX disintegrated in five days, and CEO Sam Bankman-Fried, who was doing a good white knight impersonation of JP Morgan from 1907 just a few months ago, went from a net worth of $25 billion to $0 in a flash. So far the crash hasn’t spilled over into the traditional financial markets but time will tell.

SCOREBOARD

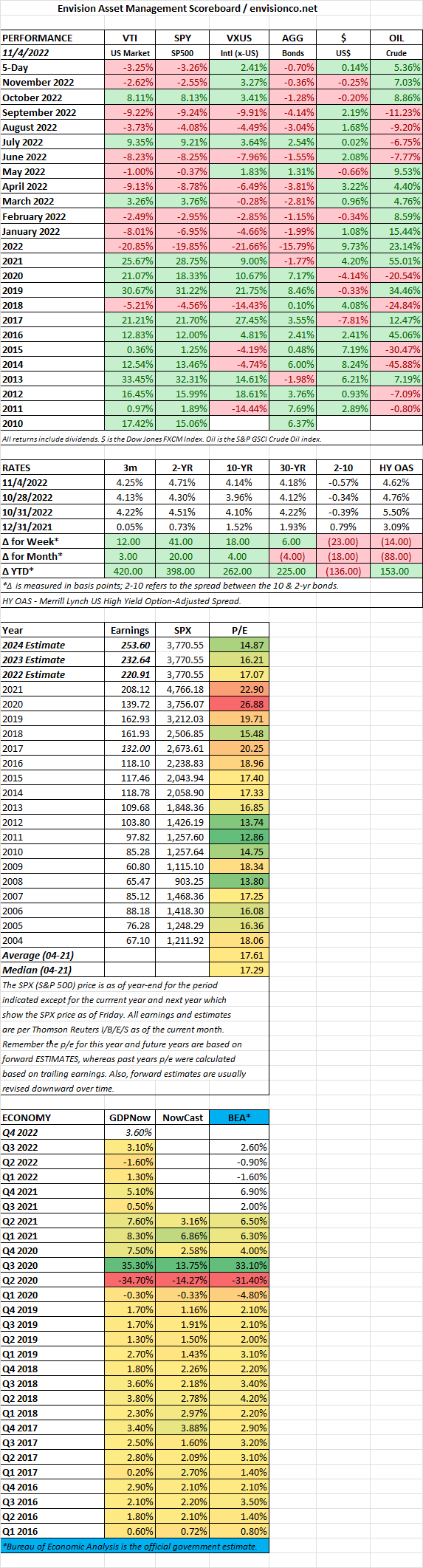

Week Ending 11/4/2022

MARKET RECAP

The S&P 500 fell by 3.35% and the Nasdaq was off by 5.65% on fears of more interest rate increases. The Fed doesn’t seem concerned that they might be overdoing it and is intent on increasing rates until inflation breaks, no matter what the damage. Similar to what they did on keeping interest rates at essentially zero for way too long, no matter what the damage.

The market has now retraced about half of the recent market gain.

Fed Chair Jerome Powell said, “We still have some ways to go, and incoming data since our last meeting suggest that the ultimate level of interest rates will be higher than previously expected.”

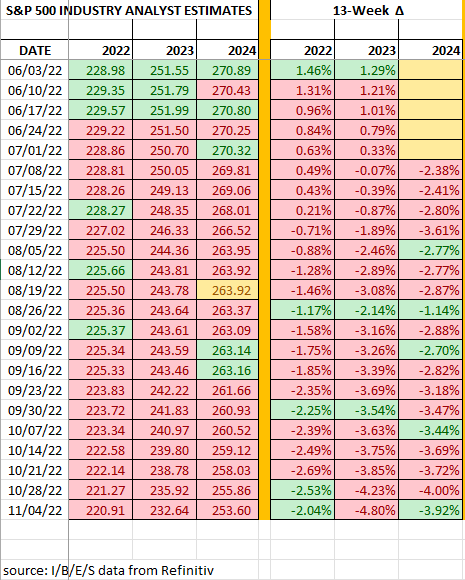

Projected earnings estimates have been dropping at an accelerating rate. The 2023 estimates have fallen by 4.80% over the last 13 weeks. But economic growth for Q4 is looking decent, the Atlanta Fed’s GDP Model has Q4 growth at 3.6%.

Employment increased by 261,000 jobs in October, the lowest amount since December of 2020, but still greater than the pre-pandemic average of 198,000. The unemployment rate increased to 3.7%. The report shows that the jobs market, while still positive, is beginning to lose momentum. Twitter, Lyft, and Stripe all announced layoffs this week. Average hourly earnings were up by 0.4% in October versus 0.3% in September. But year over year, the increase was 4.7% compared to 5% in October, both off from the 5.6% March high point.

SCOREBOARD

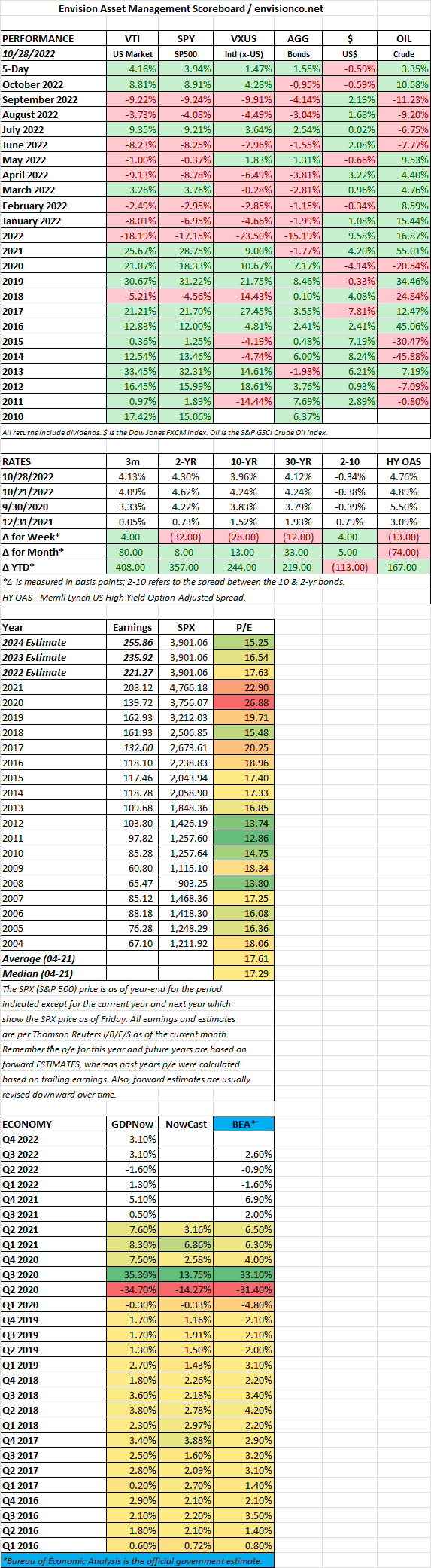

Week Ending 10/29/2022

MARKET RECAP

Another incredible week as US stocks rose by 4.16% and are now up 8.81% for the month; this is in the face of what is almost certainly another 0.75% increase in the fed-funds rate this week. Or maybe the market is looking ahead to what often is a market rally after the midterm elections. According to the Stock Traders Almanac, the Dow has averaged a gain of 46.8% since 1914 from the midterm low to the pre-election year high. But that metric will undoubtedly be tested by a Fed focused on slowing the economy until inflation fades.

The Dow is up 14.4% for the month, and assuming nothing crazy on Halloween, will turn in its best performance since January of 1976.

Except for Apple, big tech missed on earnings. Microsoft scraped by with a small beat, but disappointed investors with its outlook, Alphabet’s revenue fell short in the advertising category, and Meta missed on overall sales.

SCOREBOARD

Week Ending 10/21/2022

SCOREBOARD

Week Ending 10/14/2022

SCOREBOARD

Week Ending 10/7/2022

MARKET RECAP

Stocks managed to advance by 1.63% for the week. The market was strong at the beginning of the week on another hope that the Fed will pivot sooner rather than later, but as that became apparent that was more hope than real, the market fell hard at the end of the week.

Employers added 263,000 jobs in September, less than the 315,000 added in August and lower than the six-month average of 400,000, but more than the consensus estimate. The unemployment rate fell to 3.5% from 3.7%, matching a half-century low. The labor force participation rate declined. The stronger than expected report sparked another sell-off in the markets, worried that the slowdown in forthcoming interest rate increases in now further away. The S&P dropped by 2.8% and the Nasdaq fell by 3.8%.

Cracks continue to appear in the economy. AMD, Samsung, and Micron Technology have all issued weak forecasts.

SCOREBOARD

Week Ending 9/30/2022

MARKET RECAP

SCOREBOARD

Week Ending 9/23/2022

MARKET RECAP

Financial markets hit new 2022 lows and oil dropped by 5.7% on Friday to close out the week. Oil is now down 36% from its June high. Over the last two weeks, the S&P 500 has fallen by 9.2% and the Nasdaq by more than 10%. The 2-year treasury yield closed at 4.22%, the highest level in over a decade. The composite PMI in the US was in contractionary territory at 49.3, but that was up from 44.6 in August.

A Eurozone recession is pretty much a certainty now and the odds for a US recession seem to be rising by the day. And to make matters worse, Putin has doubled down on his so far losing strategy in Ukraine and called up 300,000 reservists and threatened nuclear strikes.

SCOREBOARD

Week Ending 9/16/2022

MARKET RECAP

US stocks fell by 4.80% and bonds were off by 0.95%. The 2-year Treasury yield increased by 29 basis points. International stocks dropped by 3.30%.

On Tuesday, the Bureau of Labor Statistics announced that CPI had increased by 8.3% since last year, higher than what was anticipated. The Core CPA, which excludes energy and food, was up by 6.3% compared to 5.9% in June and July, indicating that price pressures remain intense. The S&P fell by 4.3% after the news and the 10-year treasury yield increased to 3.42% from 3.297%. According to Ryan Sweet, senior director of economic research at Moody’s Analytics, the average household is spending $460 more each month to buy the same basket of goods and services as last year.

Markets are now anticipating a fed-funds rate of about 4.25% in December, implying 75 basis point increases in September and November, and then another 25 basis points in December. The terminal rate is anticipated to be 4.45% in April.

FedEx announced weak, very weak, preliminary earnings due to weak demand. The stock fell by 22%. Ray Dalio of Bridgewater writes that a 4.5% fed-funds rate could mean a 20% drop in equity prices.

SCOREBOARD