MARKET RECAP

US equity markets posted solid weekly gains for the week ending July 2, 2026 (with markets closed July 3-4 for the holiday), driven by a softer-than-expected June jobs report that eased rate-hike fears and supported a rotation into cyclical sectors.

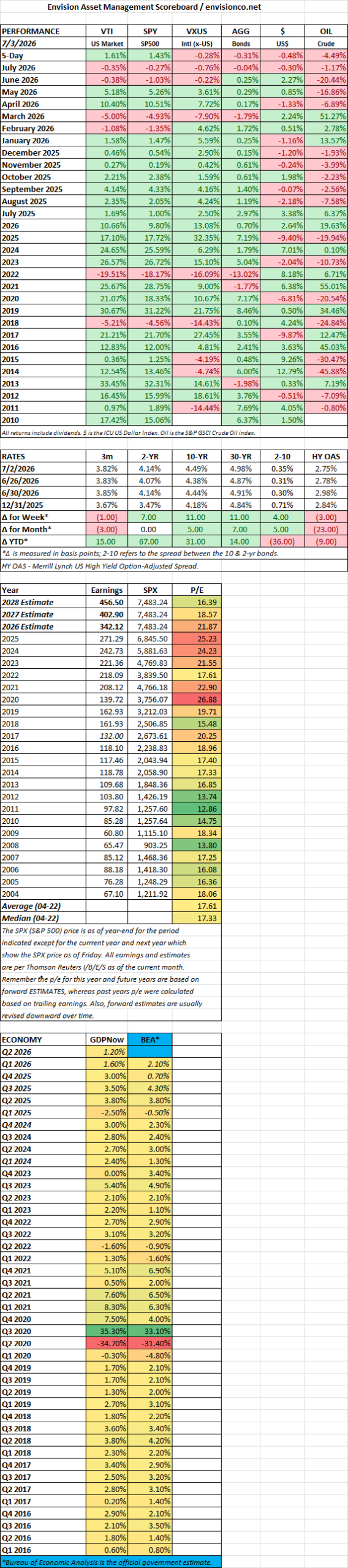

The S&P 500 rose from approximately 7,354 on the prior Friday to close at 7,483.24, a gain of roughly +1.8%. The Dow Jones Industrial Average climbed from 51,876 to a record 52,900.07, up about +2.0% for its fourth straight weekly advance. The Nasdaq Composite advanced from around 25,298 to 25,832.67, gaining roughly +2.1% despite some intraday tech weakness on July 2.

International stocks, as proxied by the Vanguard Total International Stock ETF (VXUS), showed modest gains. VXUS closed the week at approximately 84.84 (up from around 84.48 the prior Friday), for a weekly advance of roughly +0.4%. This reflected mixed global performance amid U.S. data spillover effects and varying regional economic signals.

In fixed income, the 10-year Treasury yield edged higher. It rose from 4.38% on June 26 to close the week near 4.49%, reflecting some recalibration after the jobs data tempered extreme dovish bets while still supporting overall risk appetite.

Bitcoin and gold both advanced. Bitcoin moved from around $60,000 mid-to-late June to the low-to-mid $63,000 range by early July, posting a solid weekly gain on risk-on sentiment. Gold climbed over 2% for the week, trading near $4,170–$4,200 per ounce after four weeks of declines, as weaker U.S. employment data reduced near-term Fed tightening expectations.

Overall, markets ended the shortened week on a constructive note with broad participation and record highs for the Dow, though rotation away from mega-cap tech and upcoming data will likely keep volatility in focus.

SCOREBOARD