MARKET RECAP

US stock markets posted modest gains over the past week, rebounding from earlier volatility amid hopes for geopolitical progress and stabilizing oil prices.

1. Shift in the Credit Intensity of US GDP Growth

A significant shift has emerged in how debt is fueling US economic output. According to the Federal Reserve’s Flow of Funds report, domestic debt expanded at a 12.3% annualized pace in Q1, pushing federal debt to nearly 110% of GDP. Outside of the 2020 pandemic anomalies, nonfinancial corporate leverage marked its second-largest quarterly increase relative to GDP since 2008, driven heavily by AI infrastructure borrowing. This structural shift suggests that the private sector’s multi-year deleveraging process has reversed into a tailwind, meaning the Federal Reserve may need to remain aggressive to reliably curb sticky inflationary pressures.

2. High-Profile SpaceX Public Debut Captures Market Attention

The financial markets were dominated by the massive public debut of SpaceX (SPCX) on secondary markets. After being co-led by Goldman Sachs and Morgan Stanley, institutional book-building closed out a healthy four times oversubscribed and priced at $135 per share. Shares surged to close just above $160, valuing the company at over $2 trillion and cementing it as the sixth-largest publicly traded US corporation. While the blockbuster listing energized market sentiment, it triggered a severe “sell-the-news” rout for other space equities, which plummeted by an average of 10.5% during the session.

3. Mixed Consumer and Producer Price Pressures

The latest government data presents a complicated, mixed picture for inflation. May Consumer Price Index (CPI) advanced 0.5% month-over-month and 4.2% year-over-year, though Core CPI came in a notch softer than expected at 0.2% (+2.9% YoY). Constructively, core consumer goods ex-used-autos dropped at a 1.5% annualized rate, hinting that tariff pass-through costs are cooling. However, wholesale metrics remain incredibly sticky; the May Producer Price Index (PPI) beat expectations by rising 6.5% year-over-year, while “supercore” PPI jumped to 5.1%—marking some of the highest wholesale input pressures seen outside of the pandemic shock.

4. Preliminary Diplomatic Breakthrough Shakes Up Energy Markets

Geopolitical friction in the Middle East eased substantially following a surprise announcement by the Trump administration of a preliminary diplomatic settlement with Iran. Front-month Brent crude oil futures tumbled roughly $3 per barrel to close near $87, their lowest level since military strikes began in February. While regional agencies note that the finalized text still requires full ratification, the core draft framework involves lifting the naval blockade and suspending primary energy sanctions within 30 days in exchange for systematically reopening the Strait of Hormuz. This potential resumption of oil flows has rapidly deflated the geopolitical risk premium embedded in energy assets.

5. AI Capital Expenditures Reshape US Trade Dynamics

The fundamental structure of US international trade is undergoing a massive transformation fueled by the ongoing artificial intelligence buildout. While the headline April trade deficit arrived roughly as expected at $55.9 billion, import categories explicitly tied to AI—such as semiconductors, advanced computing machinery, and accessories—surged to a record 16.5% of total inbound goods. This represents a vertical 237% increase since late 2023. Without this massive technology investment boom, counterfactual analysis indicates that the current goods trade deficit would be sliced exactly in half from $84 billion to $43 billion.

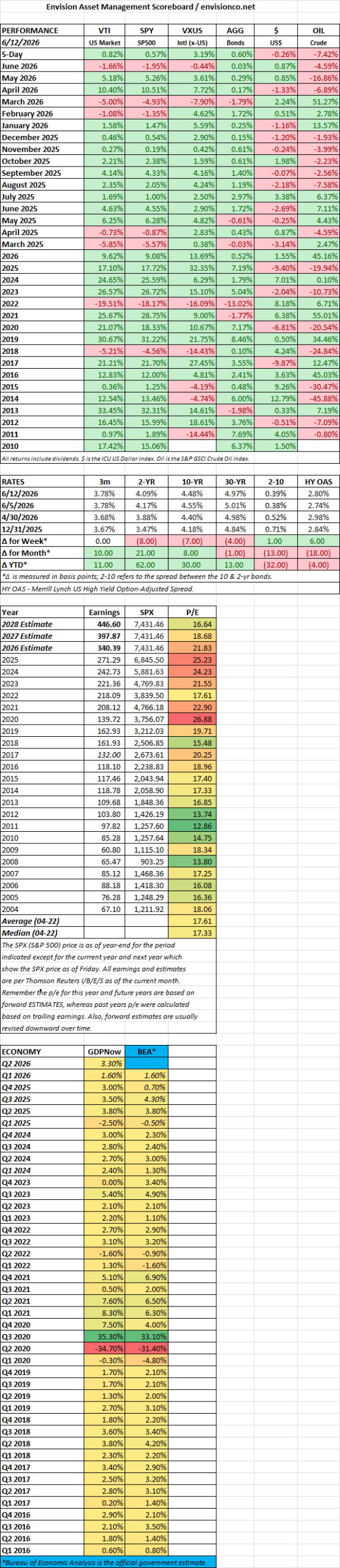

SCOREBOARD