HIGHLIGHTS

- Stocks were up around the world.

- Consumer spending remains strong.

- Foreign investment is flowing into the US due to negative interest rates.

- The next round of tariffs starts today.

- PMI reports later this week.

MARKET RECAP

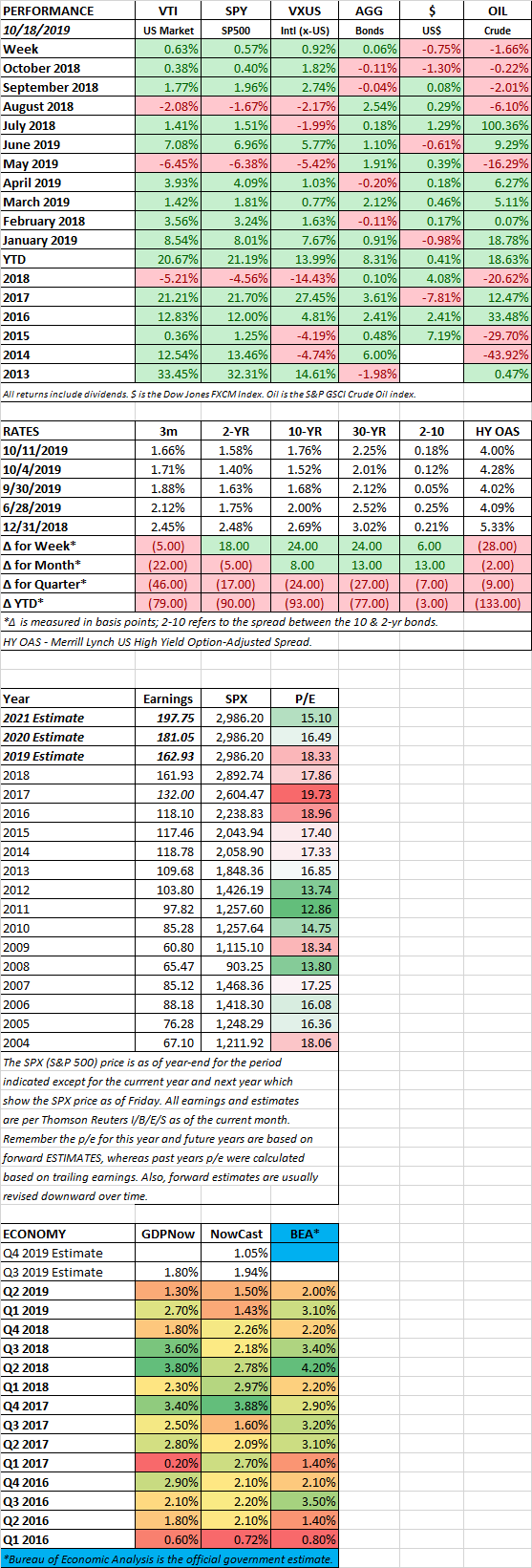

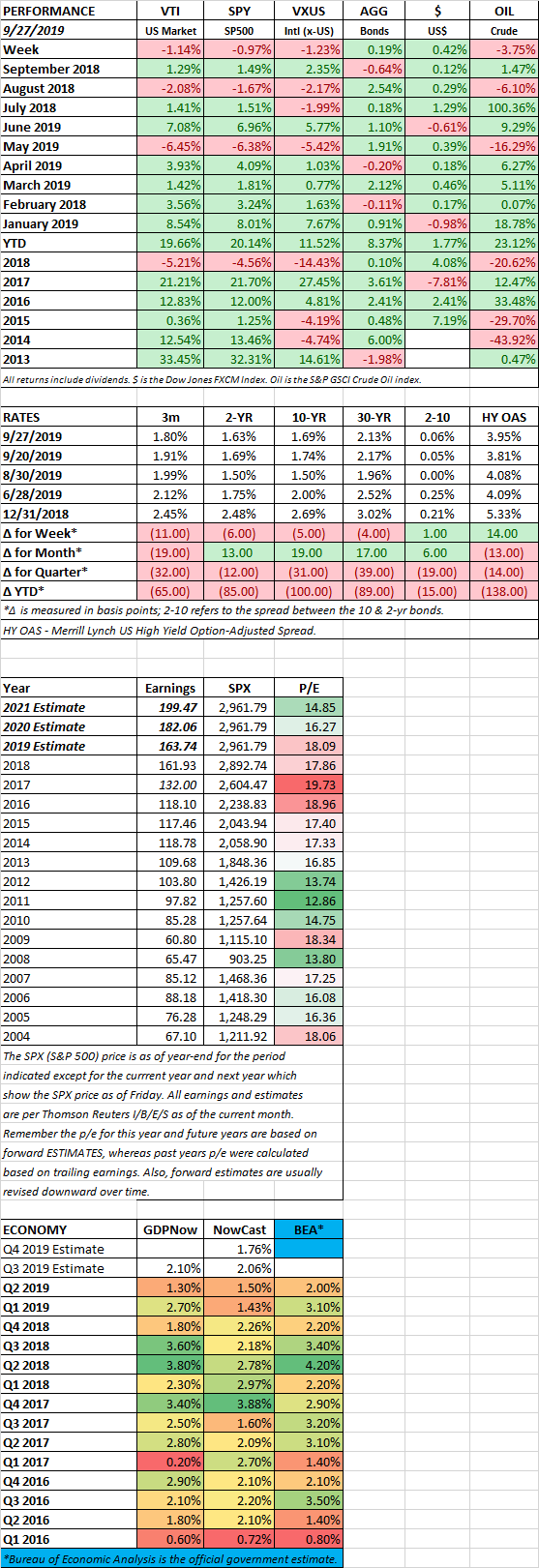

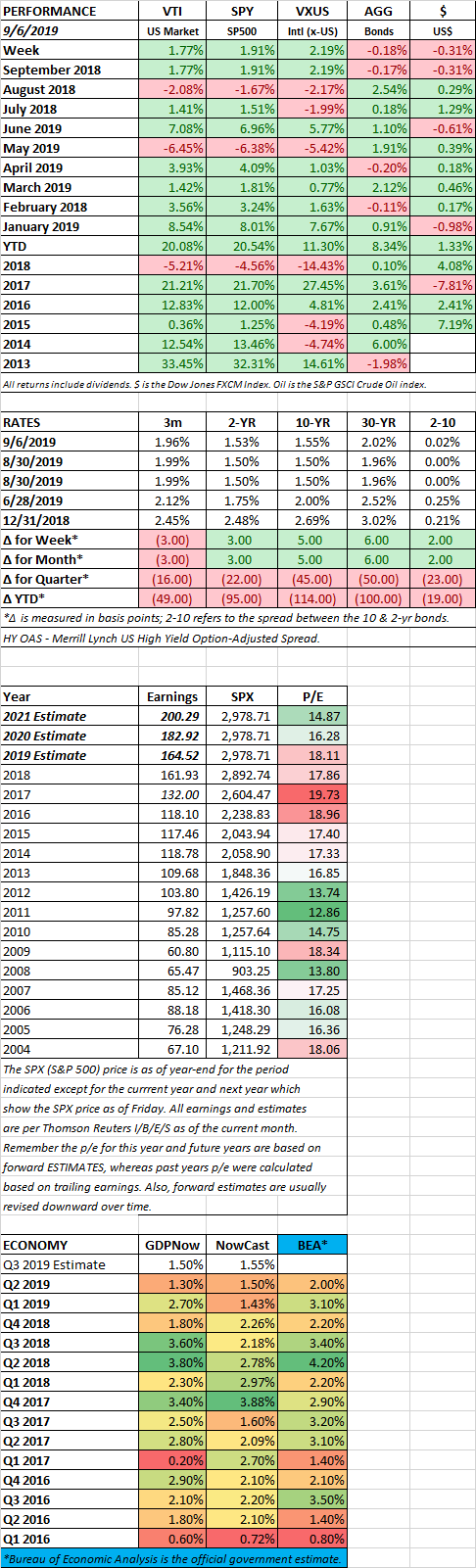

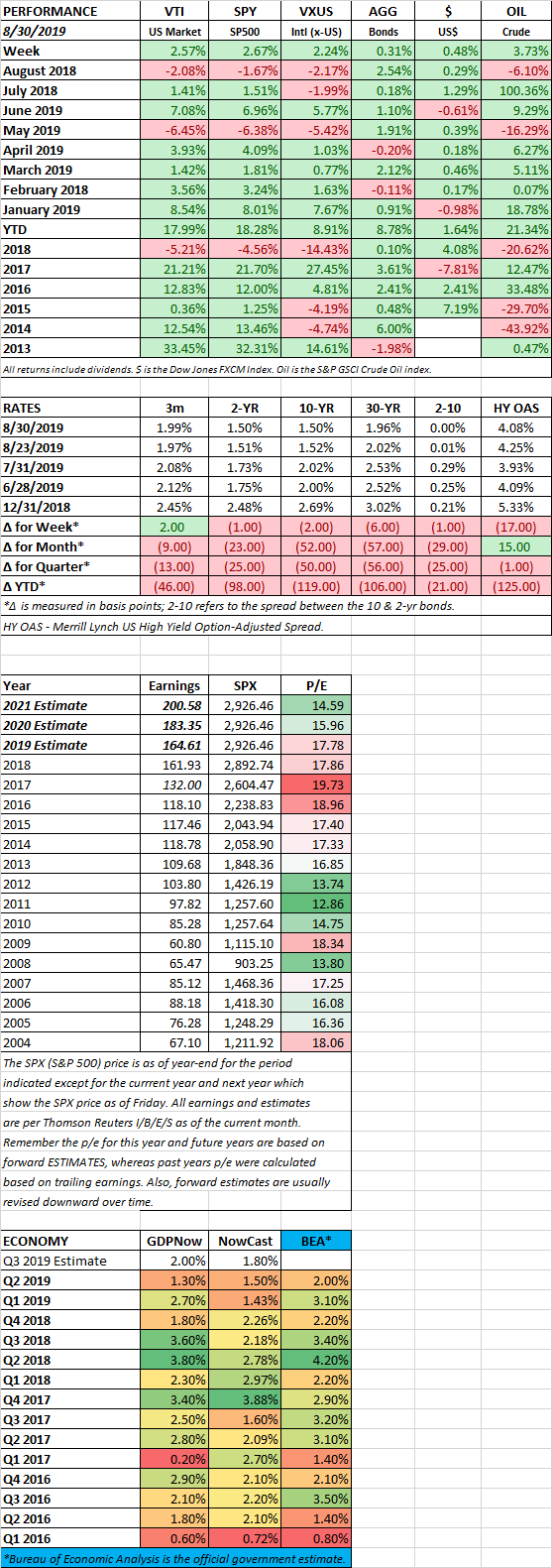

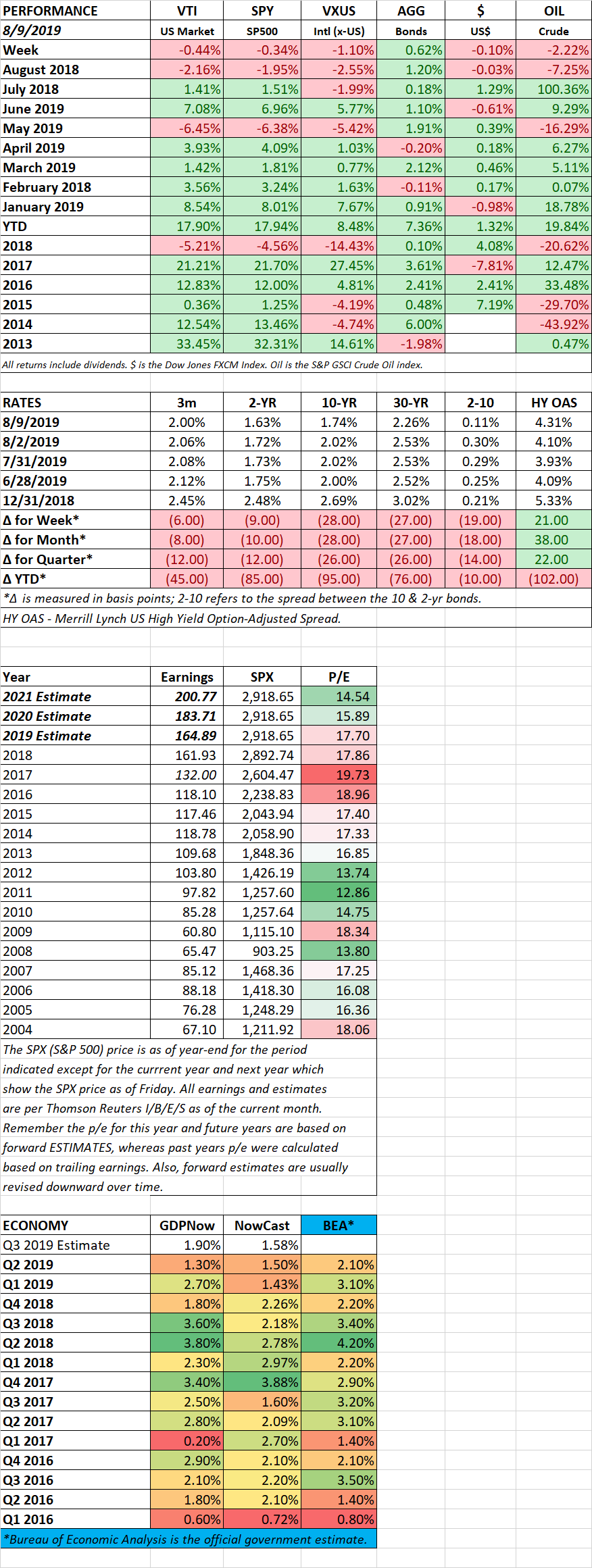

US stocks rallied during the week advancing by 2.57% while international stocks followed with a 2.24% advance. Bonds were up by 0.31% as rates fell slightly.

CONSUMER SPENDING / LOW GAS PRICES

Personal-consumption expenditures increased by a seasonally adjusted 0.6% in July, an indication that US households remain strong. Jack Kleinhenz, the chief economist at the National Retail Federation, said: “As long as we see a strong job market…the direction of the economy continues to be on track: positive but slowing.” Low gas prices have buoyed the spirits of consumers. A gallon of regular gasoline is down $0.30 from one year ago according to the price-tracking firm Gas-Buddy. The low prices are providing a tailwind to the economy, helping offset some of the negative impacts of the trade war.

FOREIGN INVESTMENT FLOWING INTO THE US

The barrage of negative yields around the world is one factor that has been helping support US markets. There is now $17 trillion in negative-yielding debt around the world. 10-year German Bunds have a -0.7% yield, while Italy, which has a barely functioning government, yields less than 1%. Thus, US debt, yielding around 1.5% or so, is attracting an avalanche of overseas investors. Foreigners bought $64 billion of US stocks and bonds in June, the largest amount since August of 2018, according to Treasury Department data. This has lowered yields on debt and kept equities close to their highs, despite a more threatening economic outlook.

ANOTHER ROUND STARTS TODAY

The newest round of tariffs kicks in today on about $110 billion in Chinese goods. This will be a 15% tariff that hits consumer products like footwear, apparel, home textiles, and some technology products like the Apple Watch. Another round that will impact $160 billion in goods is scheduled for December 15.

Not to be outdone, China rolled out their own tariffs today on about $75 billion of US goods, impacting factories and farms across the Midwest and the South.

In an August report, the non-partisan Congressional Budget Office estimated that by 2020, the tariffs/trade war will lower US GDP by 0.3% and reduce the average real household income by $580. JP Morgan wrote that the cost to the average US household will be $1,000 per year.

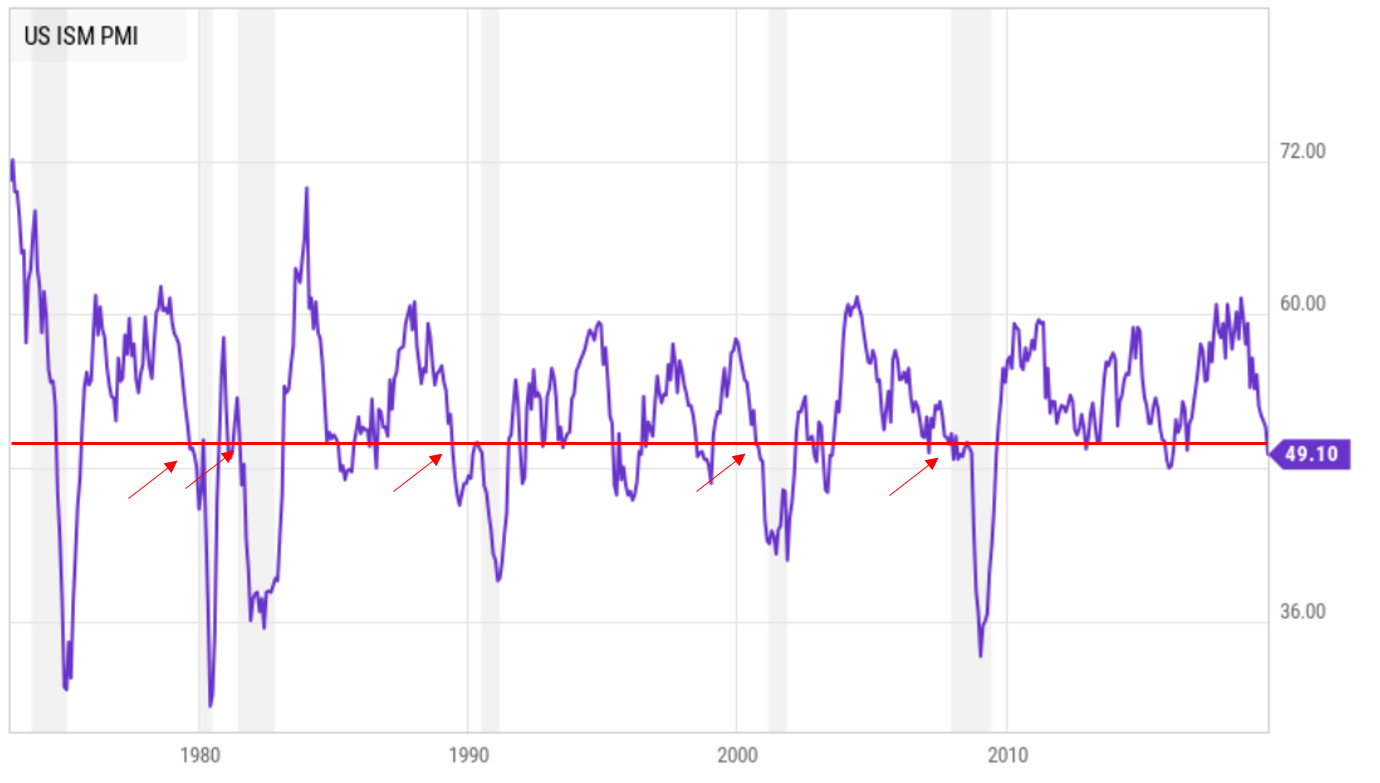

PMI’s This Week

The purchasing managers’ index reports from around the world will be released later this week. That will give a hint as to the direction of the world economy and what the impact of the trade war has been and likely to be.

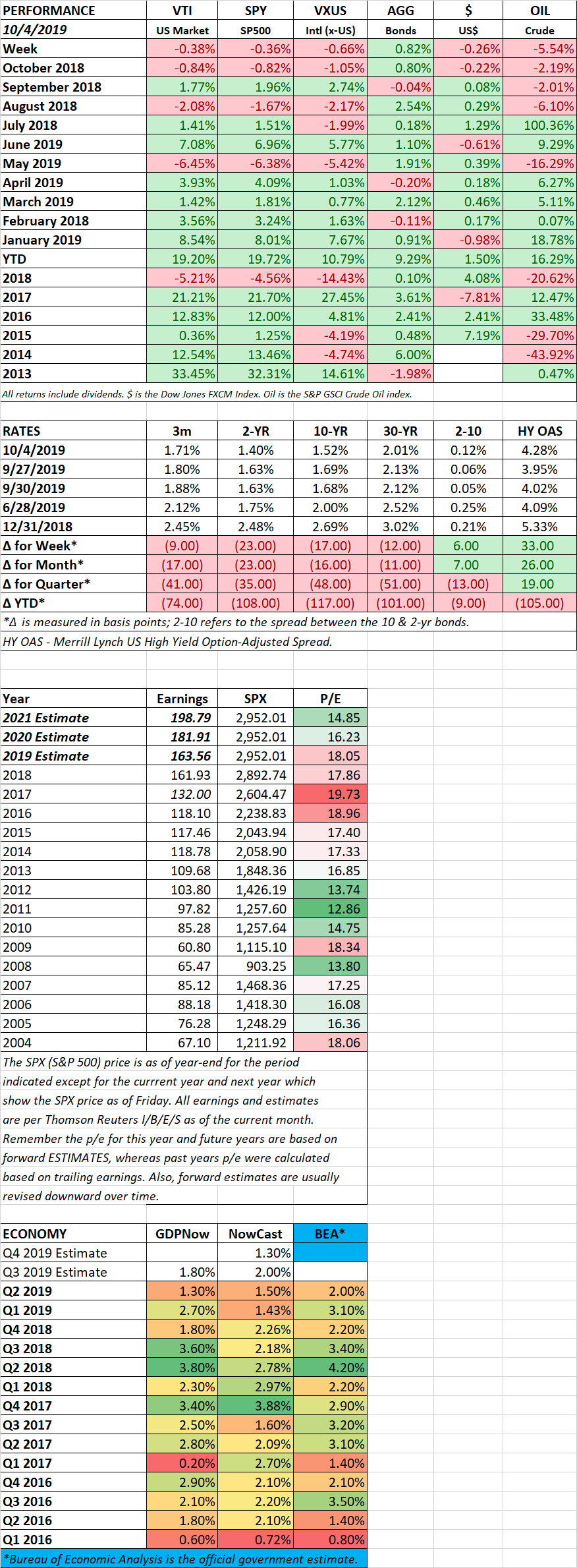

SCOREBOARD