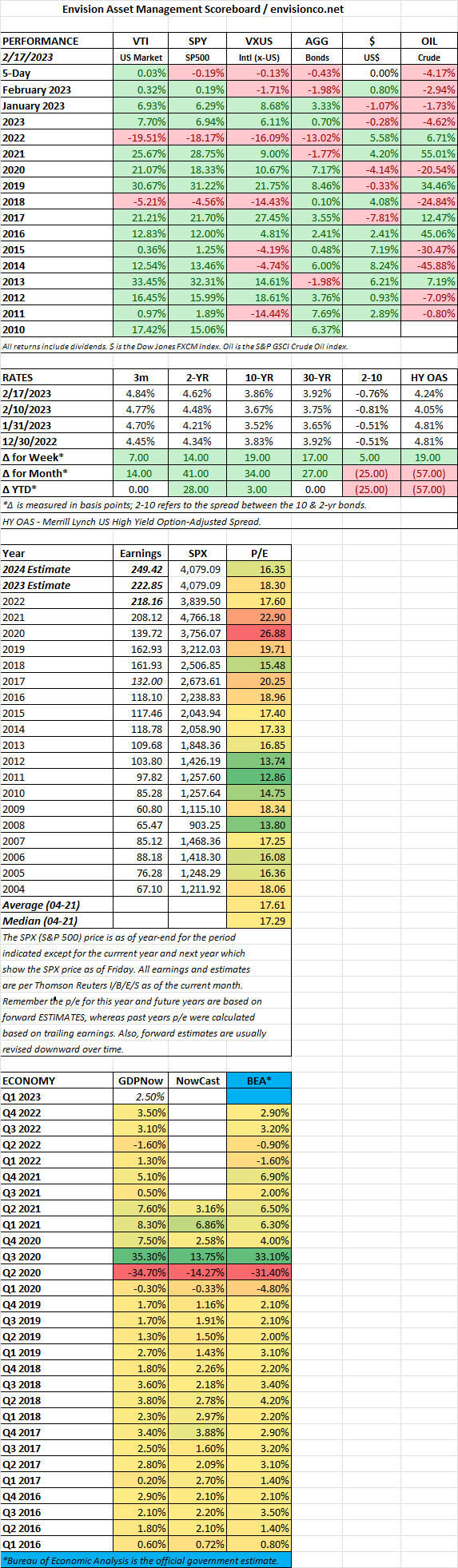

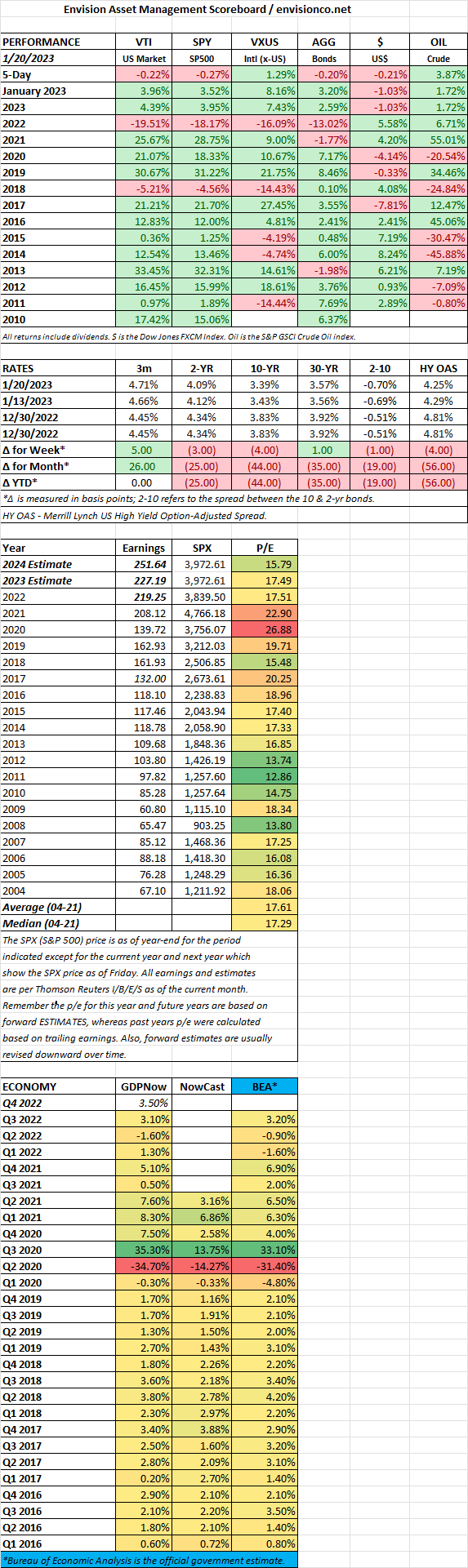

SCOREBOARD

SCOREBOARD

MARKET RECAP

US stocks rallied by 1.94%, while international stocks fell by 1.04%. Bonds were flat.

The US added 517,000 jobs in January, way above estimates of less than 200,000, and in the process, dropped the unemployment rate to 3.4%, a 53-year low. Over the past year, wages were up by 4.4%, down from a revised 4.8% in December. The extra strong jobs report does not jive with other economic reports that show that consumer spending started to slow at the end of the year and that manufacturing activity declined. But new orders did increase, according to the Institute of Supply Management Business Activity Index, which increased to 60.4% from 45.2% in December. The Service Sector was also up, at 55.2 versus 49.2 in December.

The Fed raised its bench market interest rate to 4.75% from 4.5%. The strong jobs report led some investors to suspect that the Fed will continue for the time being on increasing rates and hold off cutting interest rates longer than expected.

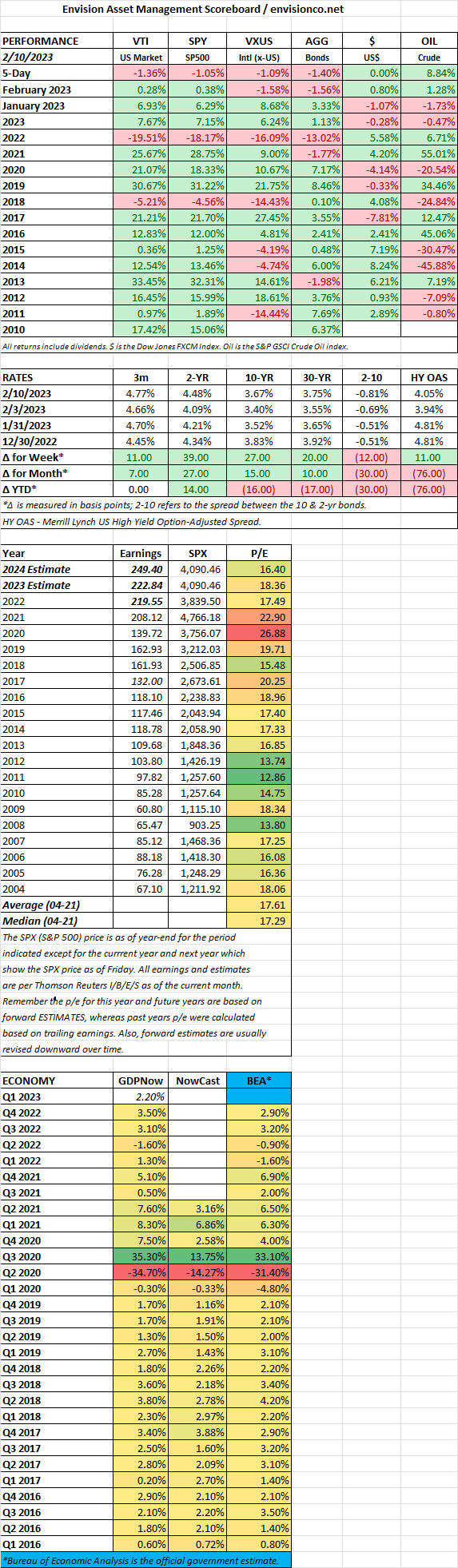

SCOREBOARD

MARKET RECAP

SCOREBOARD

MARKET RECAP

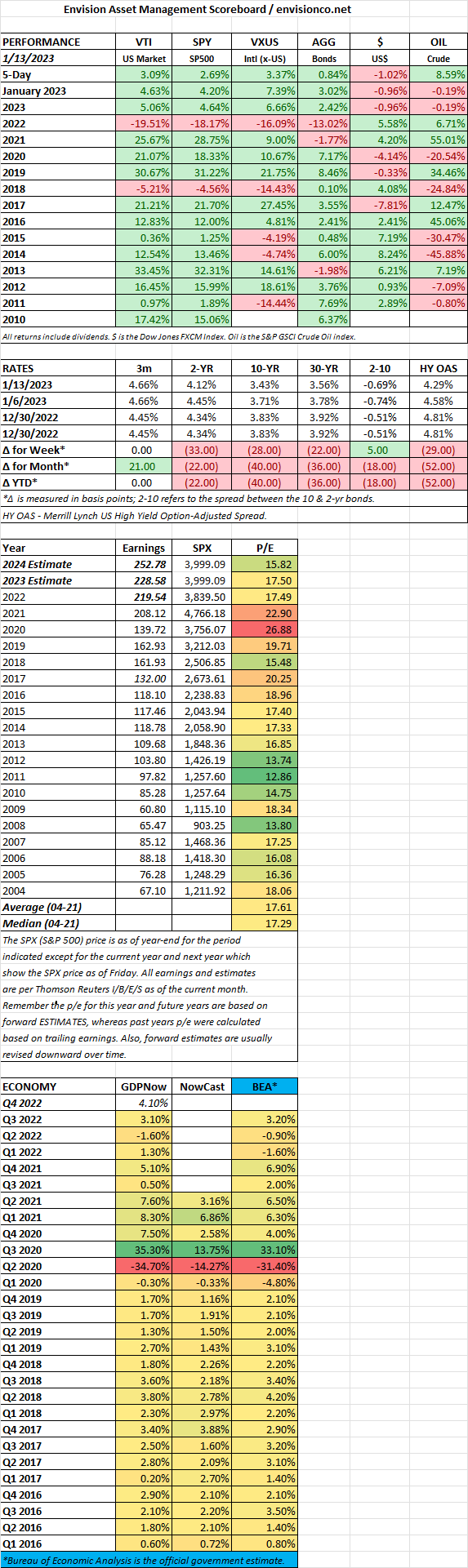

SCOREBOARD

MARKET RECAP

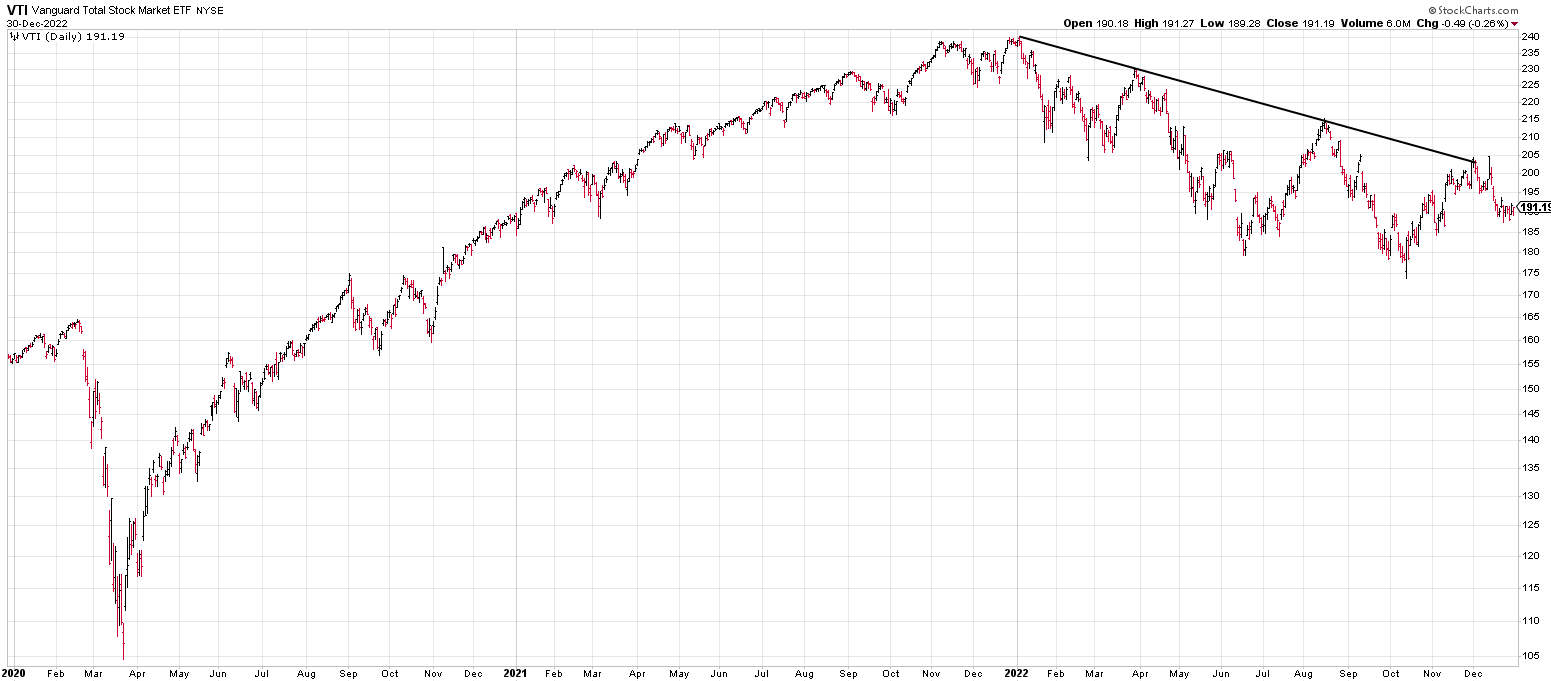

US stocks advanced by 3.09%, international stocks by 3.37%, and bonds were up by 0.84%. International stocks continue to outperform and appear on an uptrend now, while US stocks are close to breaking the declining trend line (see the two charts below).

2022 trends are reversing, helping investors; lower interest rates, a lower dollar, tech stocks, and crypto is rallying, and inflation is falling.

With a Republican-controlled house, and the recent shenanigans in electing a speaker, don’t count on a smooth increase in the debt ceiling. We have already seen congressmen (and women) operate in their own perceived best interests, even when the well-being of the country is at stake. The Treasury should be good until early June.

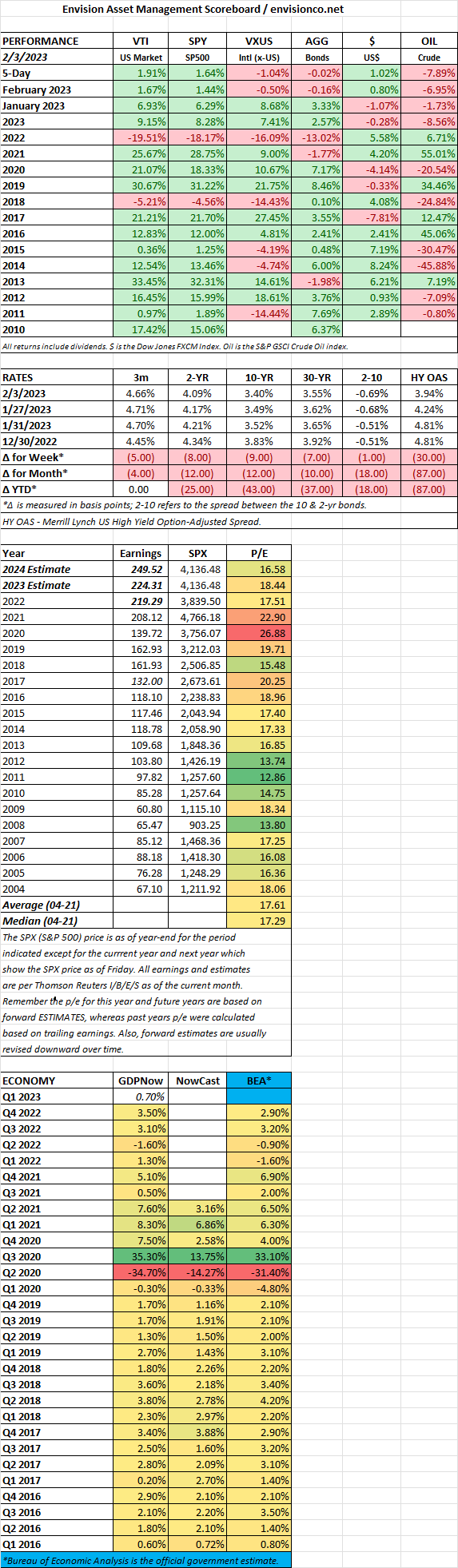

SCOREBOARD

MARKET RECAP

SCOREBOARD

MARKET RECAP

Stocks closed the year with a slight loss of 0.1%. The overall US stock market returned -19.51% for the year, the S&P 500 was down by -18.17%, international stocks were off by -16.09%, and bonds were down -13.02%.

The Dow did the best, dropping by 8.8%, while the NASDAQ fell by 33.1%. Investors will watch how stocks perform during the first five days of the year. According to the “Stock Trader’s Almanac,” “the last 47 up First Five Days were followed by full-year gains 39 times.” That equates to an 83% accuracy ratio with an average return of 14%.

Analysts did a good job predicting earnings for 2022. According to Bloomberg, the consensus was for $221 per share in S&P 500 adjusted earnings, and right now, it looks like that estimate will close to the target. But they were way off on the price of the index. The forecast was for the S&P 500 to end the year at 4,950, which was way higher than the 3,821.62 closing price. For 2023, the average estimate is 4,078. So you can probably assume that estimate is the one number the index won’t be close to; only seven times in 23 years of data has the forecast been within 5% of the consensus.

Economists expect a recession in 2023.

Q3 GDP was revised up to 3.2% from 2.9%. According to the Case-Shiller index, home prices fell for the fourth straight month, down by 0.3% in October.

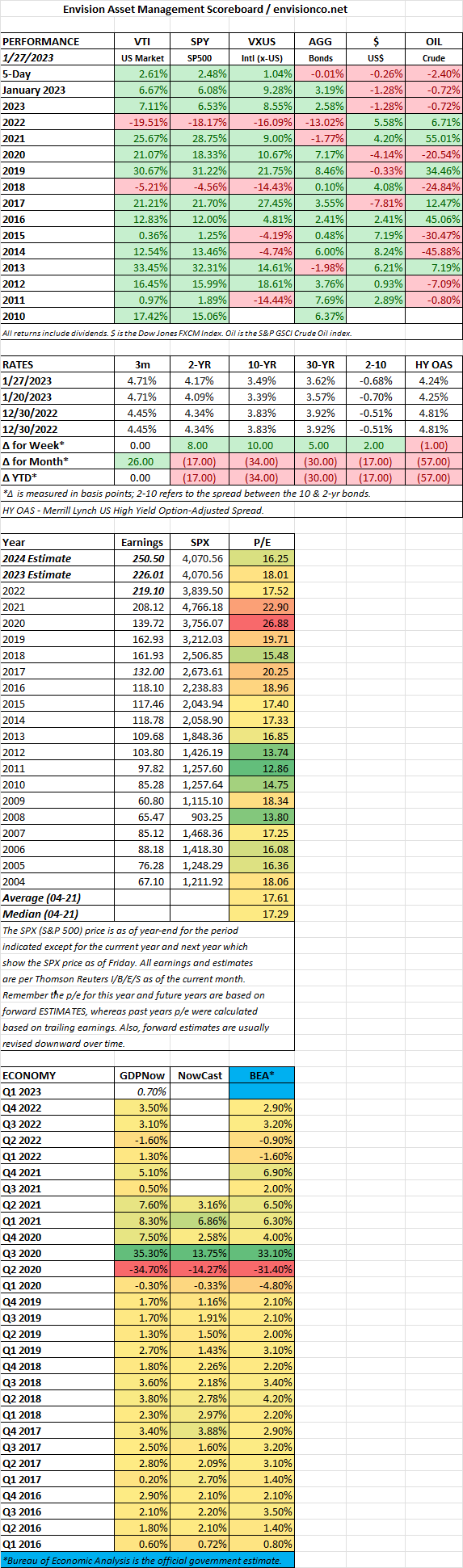

SCOREBOARD

MARKET RECAP

US stocks fell slightly, down 0.17%, while international stocks managed a 0.60% advance. Bonds dropped by 1.39%.

Personal spending was up by 0.1% in November, down from 0.9% in October, indicating a slowdown in consumer spending. At the same time, the personal consumption expenditures price index increased by 5.5% year over year in November, down from 6.1% in October. Month to month, the increase was only 0.1%, compared to 0.4% in October. So, inflation seems to be dropping at a decent pace.

Caroline Ellison and Gary Wang, two senior executives at FTX/Alameda, pleaded guilty to fraud and to cooperate in the government’s investigation. In the meantime, ringleader Bankman-Fried was bailed out of jail on a $ 250 million bond.

SCOREBOARD

SCOREBOARD