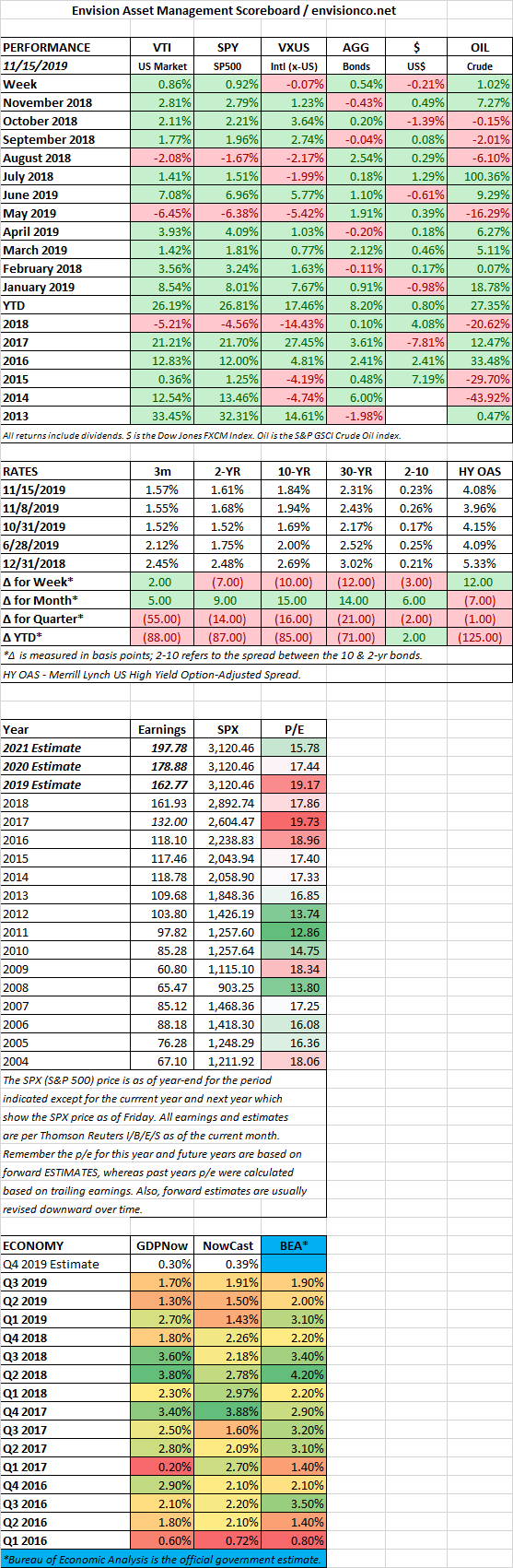

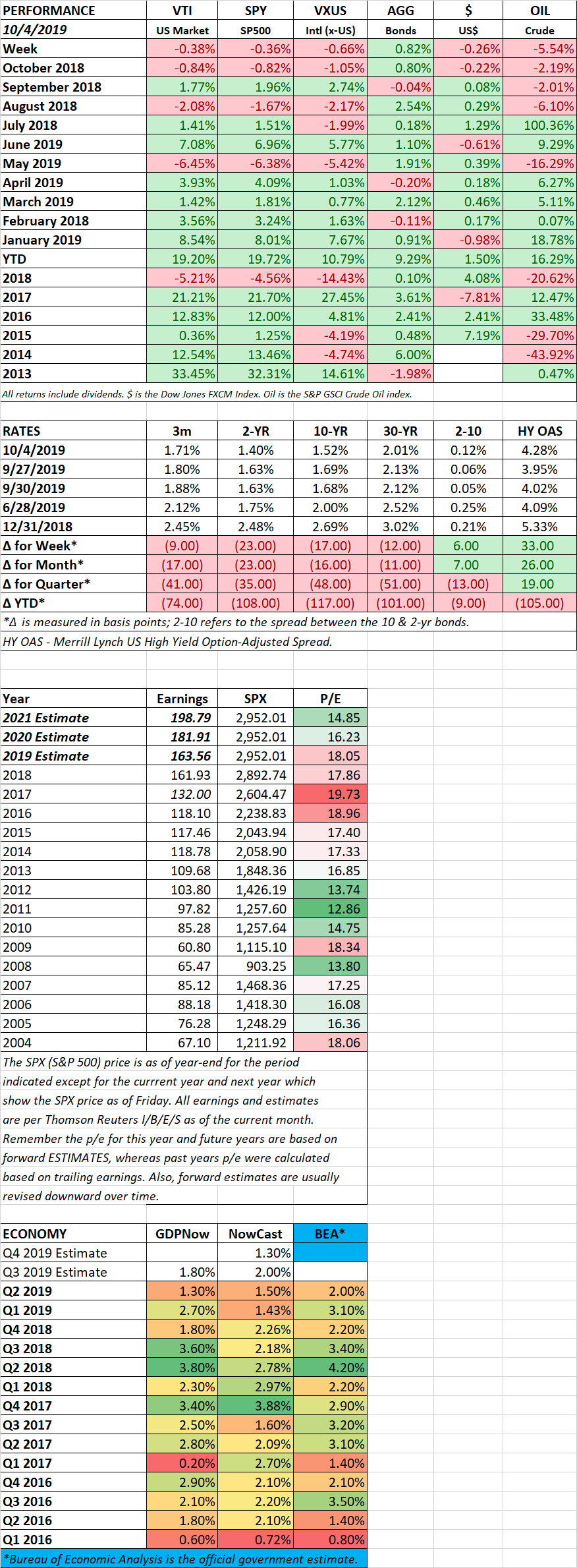

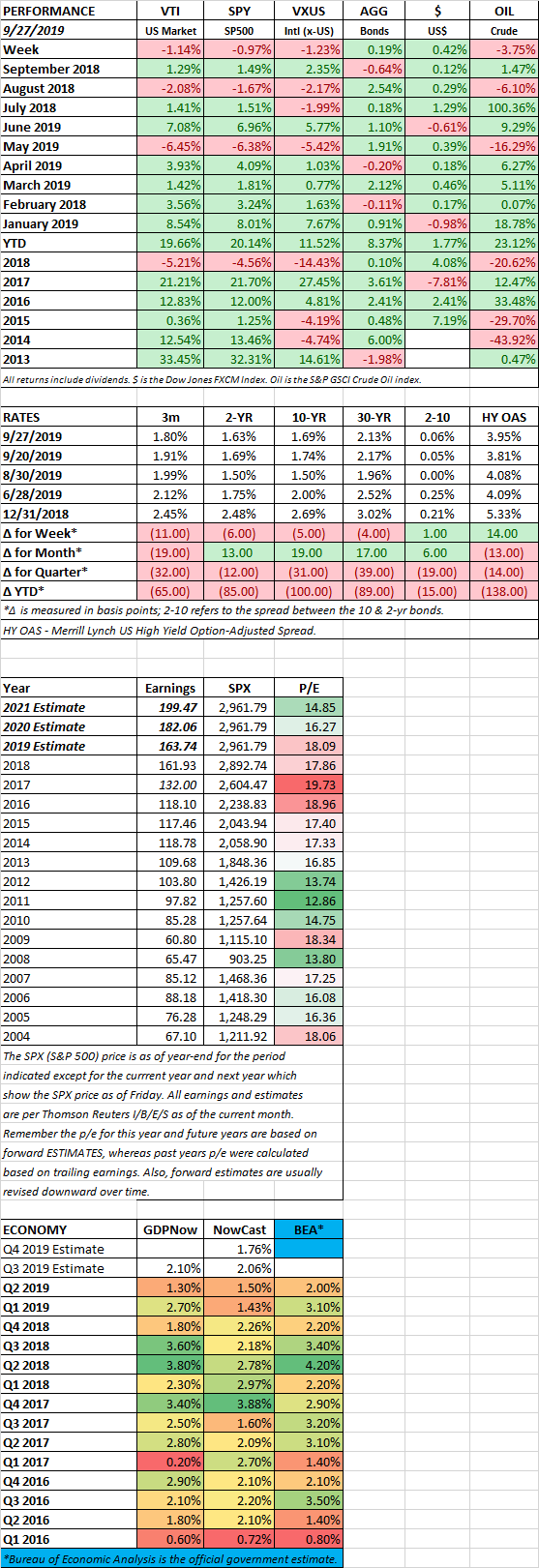

HIGHLIGHTS

- US stocks are up by 0.86% as the indexes hit a new record.

- The Dow breaks 28,000.

- Kudlow says progress on trade talks.

- Fed says rates to remain steady.

- Retail sales up 0.3%.

- Q4 growth is barely above breakeven according to two Fed bank models.

MARKET RECAP

US stocks managed another advance, +0.86%, but international stocks were unable to follow, declining by 0.07%. Bonds advanced by 0.54% as interest rates fell slightly. The Dow Jones Industrial Average closed above 28,000 on Friday for its eleventh record high of the year. There continues to progress in the US/China trade talks according to White House economic adviser Lawrence Kudlow and the Fed said rates would remain steady for now. US retail sales were up by 0.3% in October, showing that the US consumer is still going strong.

Outside of the markets, the impeachment investigation of President Trump went public this week, with hearings in the House. Bolivian President, and socialist Evo Morales resigned and fled the country.

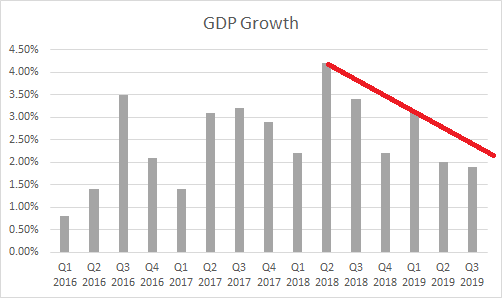

GDP FORECASTS

Stocks have been going up, but GDP forecasts have been headed in the other direction, down. The Q4 forecast for GDP growth comes in at 0.30% for the Atlanta Fed’s GDPNow model, and the NY Fed’s Nowcast registers a gain of 0.39%, both barely above zero.

FED

Federal Reserve Chairman Jerome Powell does not see the need for further rate cuts, in testimony to lawmakers this week. “We see the current stance of monetary policy as likely to remain appropriate as long as incoming information about the economy remains broadly consistent with our outlook of moderate economic growth.” Powell went on to state that the Fed, at this time, does not have the ammunition it did in the past to fight a future recession given that interest rates are so low.

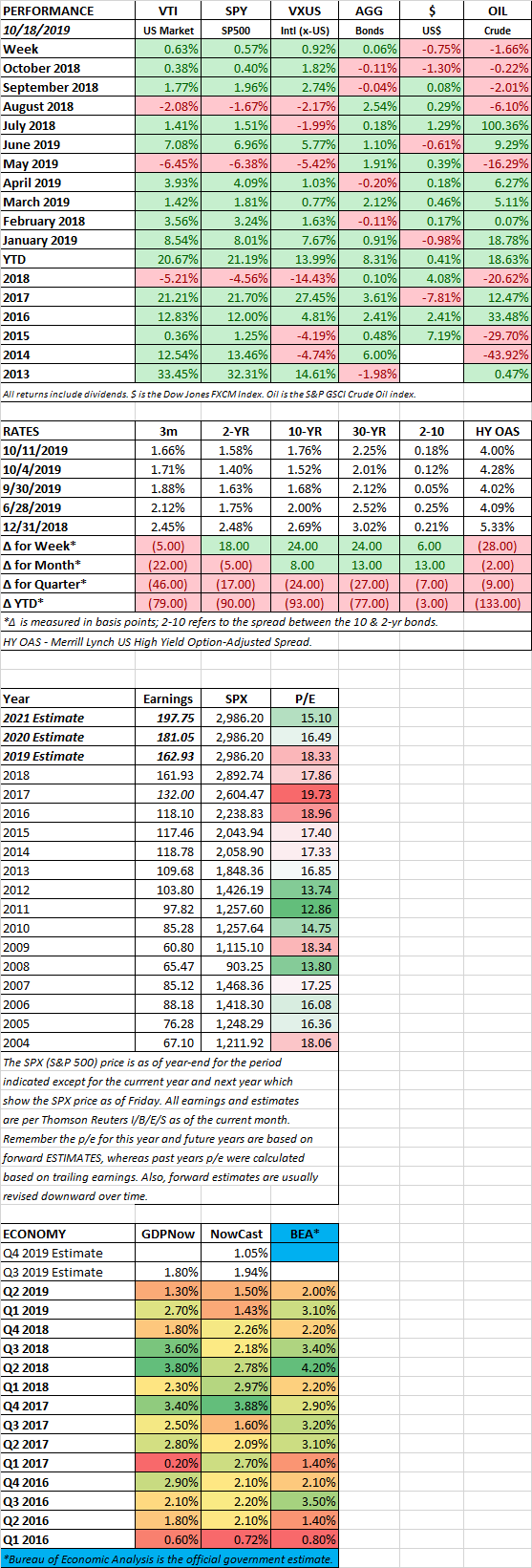

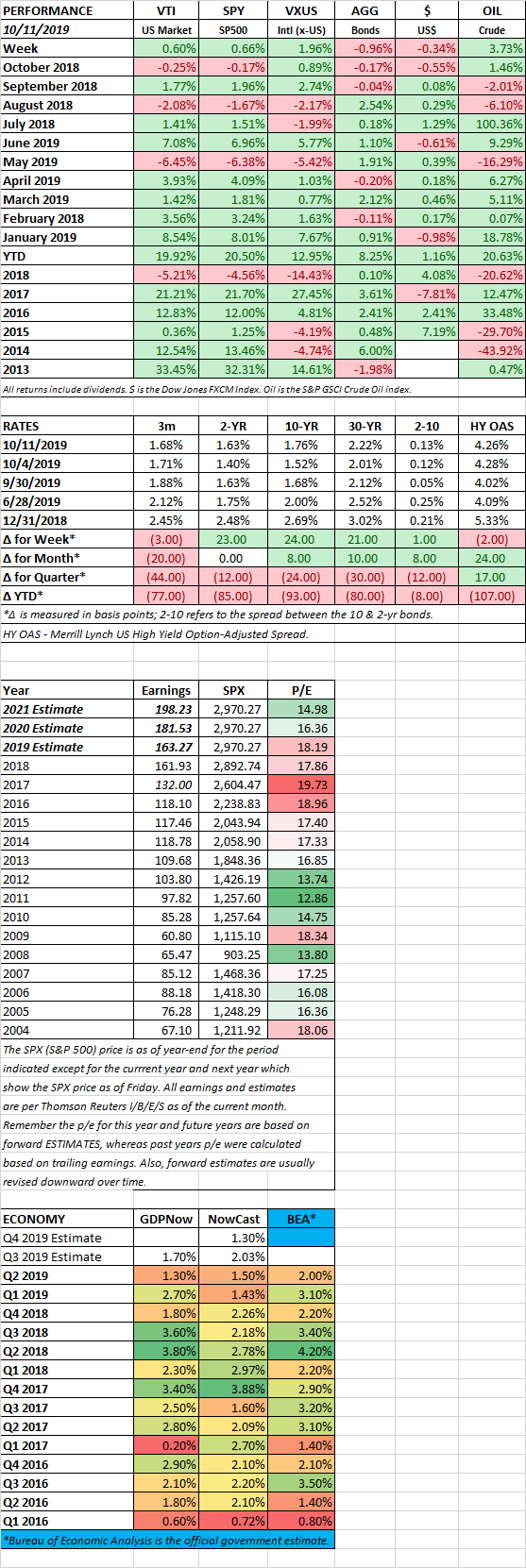

SCOREBOARD