October 2023: Financial Markets Enter Octoberfest with a Dose of Reality

October 2023 saw financial markets navigating a mixed bag of anxieties and cautious optimism, much like the weather shifting between crisp autumn mornings and warm afternoon spells. Here’s a breakdown of the key themes:

Equity Market Pullback:

- Major indices retreated further, extending the downtrend from September.

- The S&P 500 lost 2.1%, the Dow Jones dipped 1.3%, and the Nasdaq Composite shed 2.8%.

- Small-cap and mid-cap stocks suffered even more, highlighting increased risk aversion among investors.

- Only Utilities and Technology managed to eke out small gains, the latter driven by specific company earnings surprises.

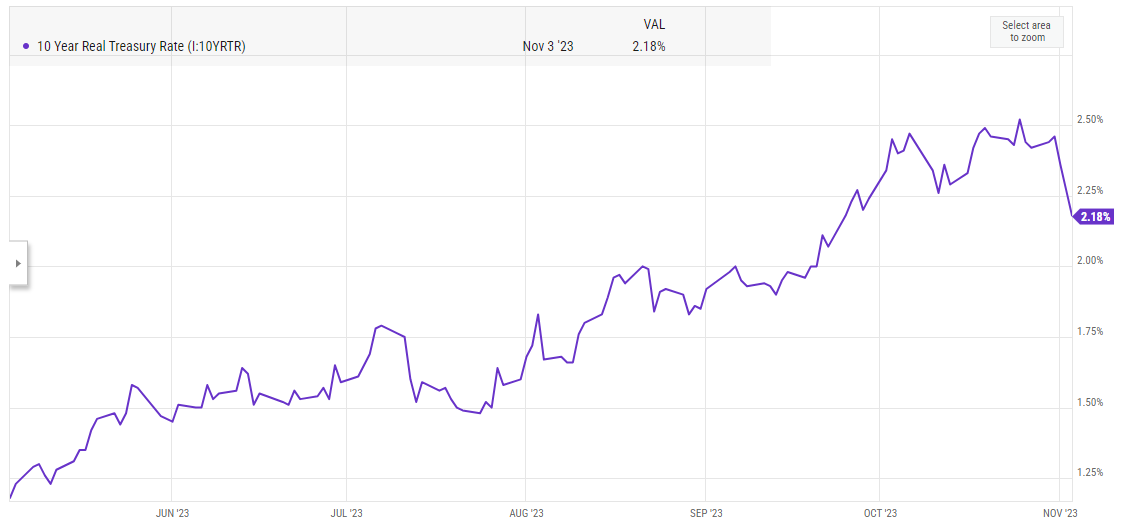

Rising Yields Bite:

- The long-held hope of Fed’s “pivot” towards a dovish stance faded as inflation stayed stubbornly high.

- The 10-year Treasury yield climbed from 4.58% to 4.79%, reflecting market expectations of further rate hikes.

- This put pressure on interest-rate sensitive sectors like technology and consumer discretionary.

Economic Resilience Fails to Buoy Markets:

- The US economy displayed surprising resilience, with a strong third-quarter GDP growth of 1.2%.

- However, this positive data was overshadowed by concerns about the sustainability of growth amidst rising interest rates and slowing global demand.

- Survey data pointed towards weakening consumer and business confidence, further dampening market sentiment.

Sector Rotation and Energy’s Rise:

- Investors sought shelter in defensive sectors like Utilities and Consumer Staples.

- Energy, benefiting from tight supply and geopolitical tensions, became the biggest laggard with a 5.8% decline.

- The strong dollar weighed on international investments, with emerging markets feeling the brunt of the pressure.

Other Notable Events:

- US government funding concerns briefly spooked the market before a temporary agreement was reached.

- Corporate earnings season commenced, offering mixed results with some companies beating expectations and others falling short.

- Geopolitical tensions remained prevalent, with the war in Ukraine and rising US-China rivalry influencing investor sentiment.

Overall, October 2023 proved to be a month of cautious adjustment for financial markets. While a strong economy provided some solace, rising interest rates and persistent inflation anxieties kept the bears in control.