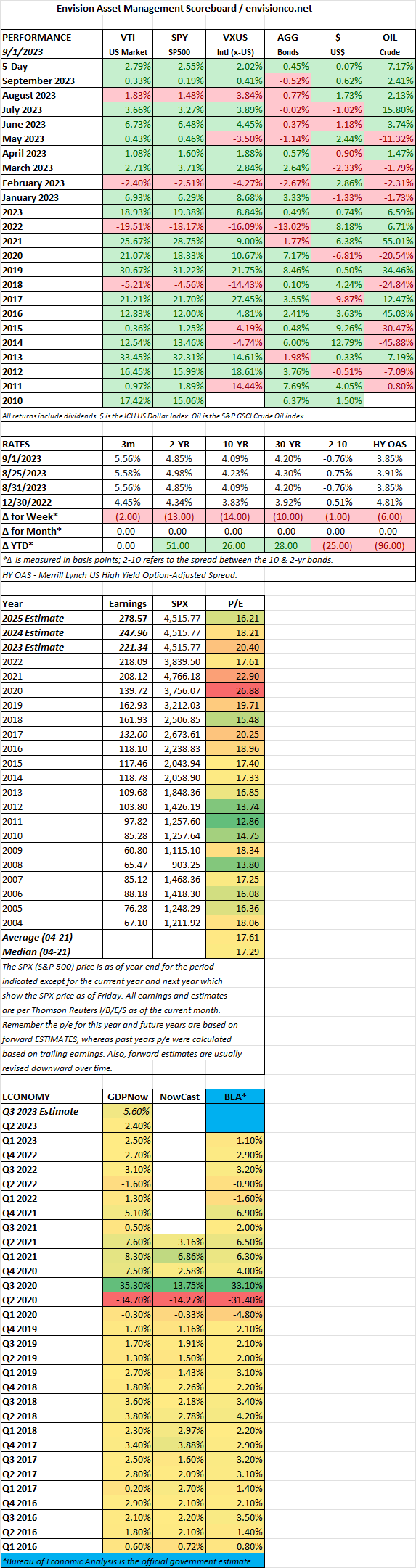

- SCOREBOARD

SCOREBOARD

SCOREBOARD

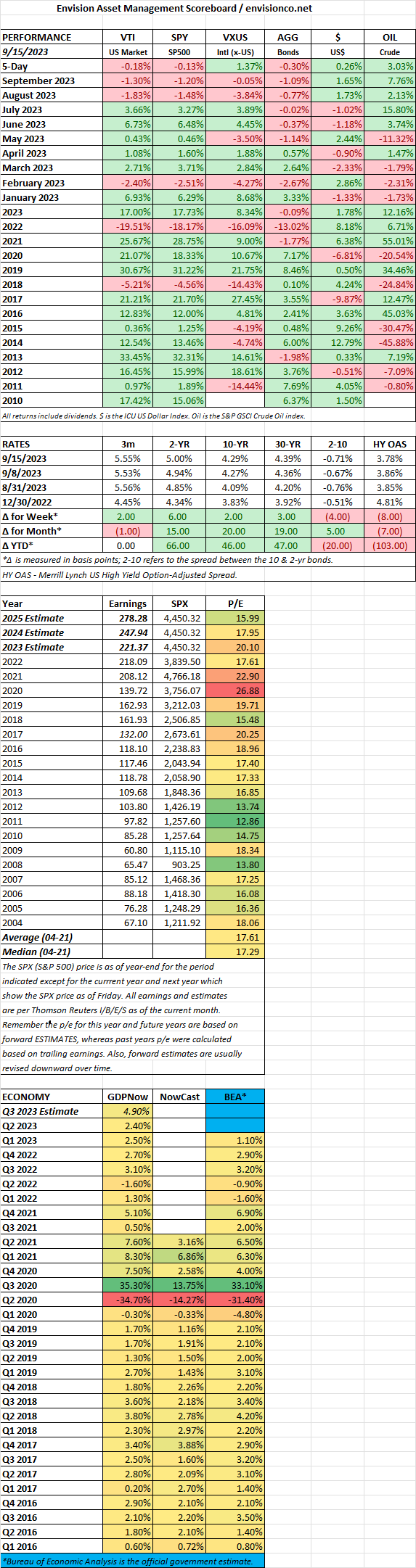

The summer heat wasn’t the only thing that cooled down in August. After a promising July, financial markets faced a reality check and retreated across most asset classes. Here’s a breakdown of the key themes:

Equity Market Tumble:

Rising Interest Rates:

Mixed Global Performance:

Economic Data Rollercoaster:

Other Notable Events:

Overall, August 2023 painted a picture of financial markets adjusting to a changing environment. The initial optimism fueled by easing inflation and strong earnings gave way to anxieties about rising interest rates, slowing economic growth, and geopolitical risks. The next few months will be crucial in determining whether this pullback is a temporary correction or a sign of a more extended downward trend.

MARKET RECAP

SCOREBOARD

MARKET RECAP

SCOREBOARD

MARKET RECAP

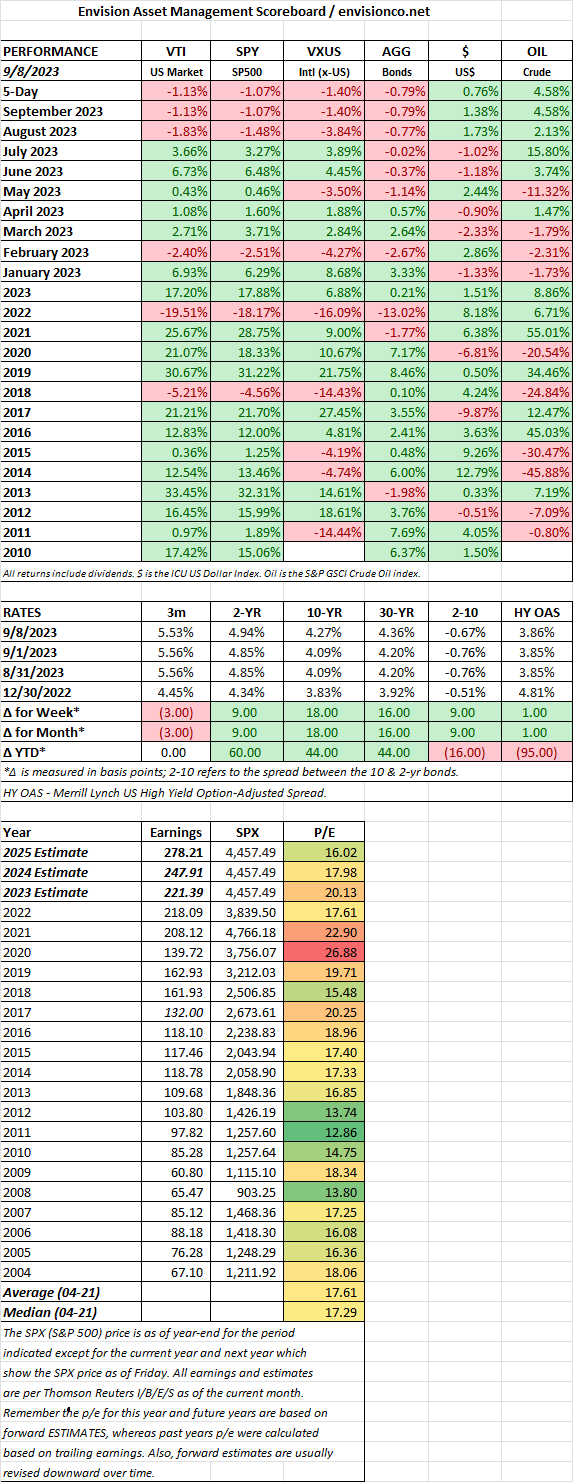

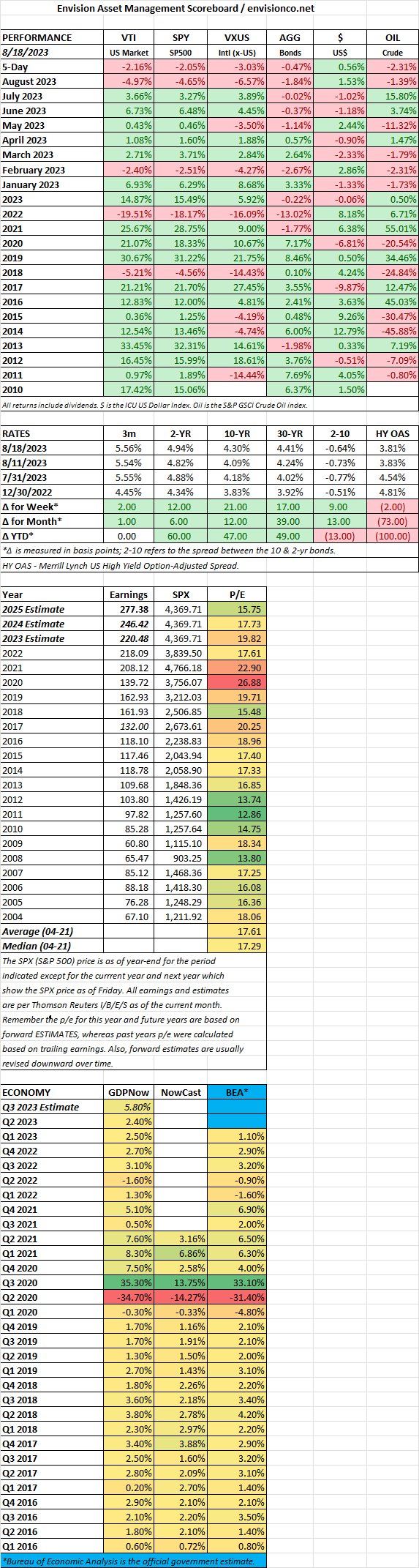

Fitch downgraded US debt to AA+ from AAA a couple of weeks back. Fitch said the downgrade was due to an “erosion of governance” in the US compared to other top-tier economies over the last two decades. The Biden administration and many “experts” said the downgrade was undeserved and nonsense. Treasury Secretary Yellen said, “The change by Fitch Ratings announced today is arbitrary and based on outdated data.” But in all seriousness, who can argue with the downgrade?

Look what is going on in this country:

So the downgrade was well deserved and should probably have been deeper.

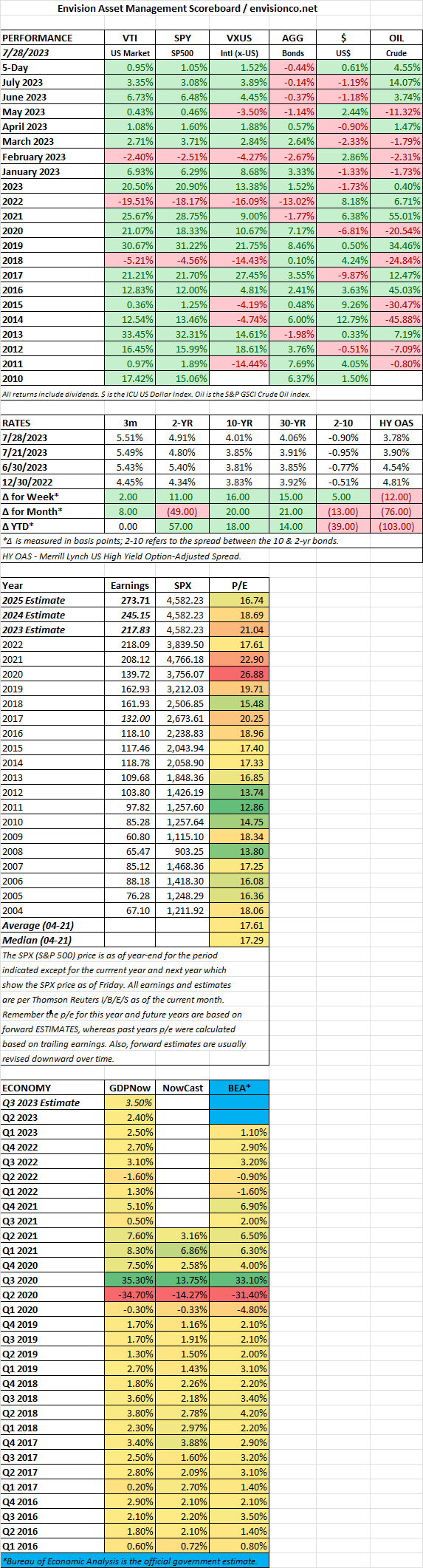

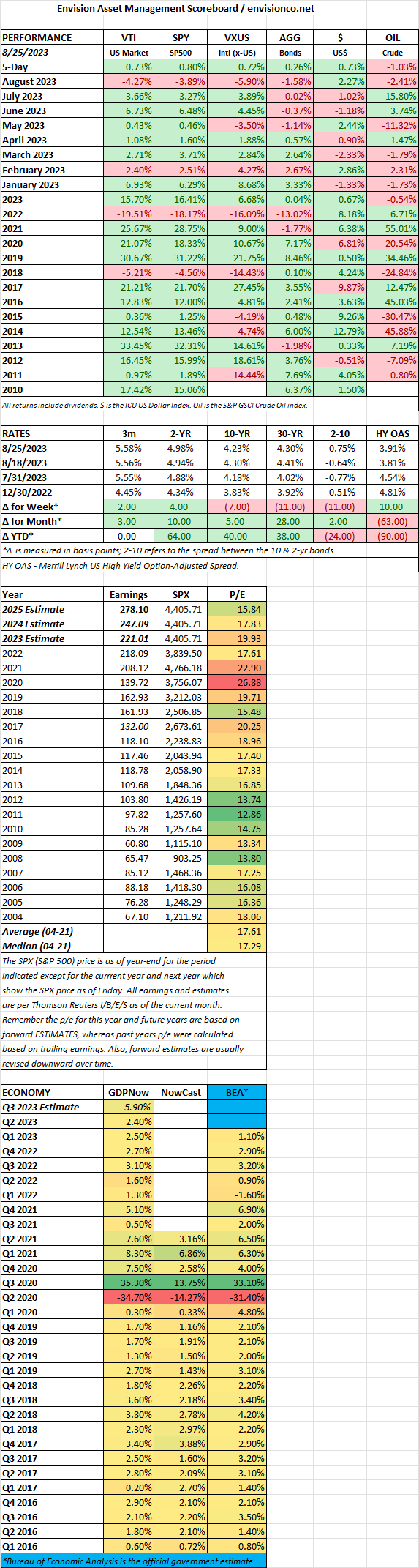

SCOREBOARD

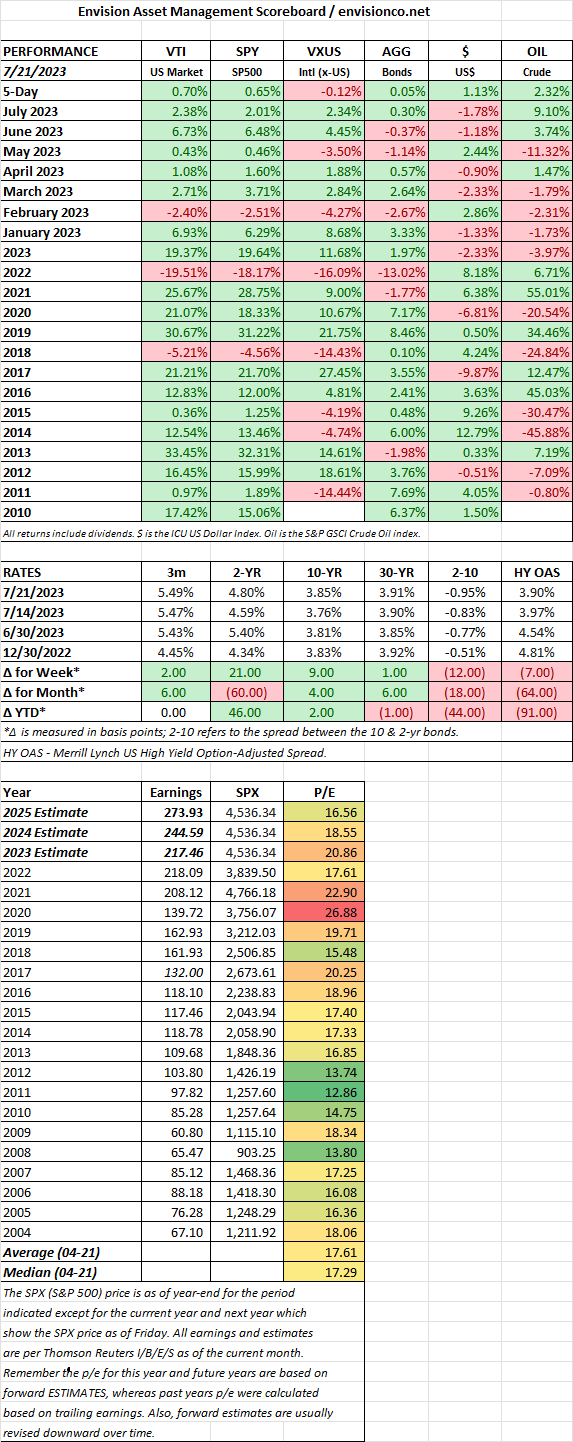

July 2023 brought continued sunshine to financial markets, extending the gains of June, but whispers of cooler autumn winds started to ruffle investor confidence. Here’s a closer look at the key themes:

Equity Market Resilience:

Earnings Beat and Economic Data Uptick:

Shifting Risk Appetite:

Sector and Regional Differences:

Other Notable Events:

Overall, July 2023 was a positive month for financial markets, but the optimism was tempered by concerns about future Fed actions and potential headwinds in the second half of the year. The upcoming months will be crucial in determining whether the summer rally can hold its heat or if the whispers of autumn chills become a reality.