MARKET RECAP

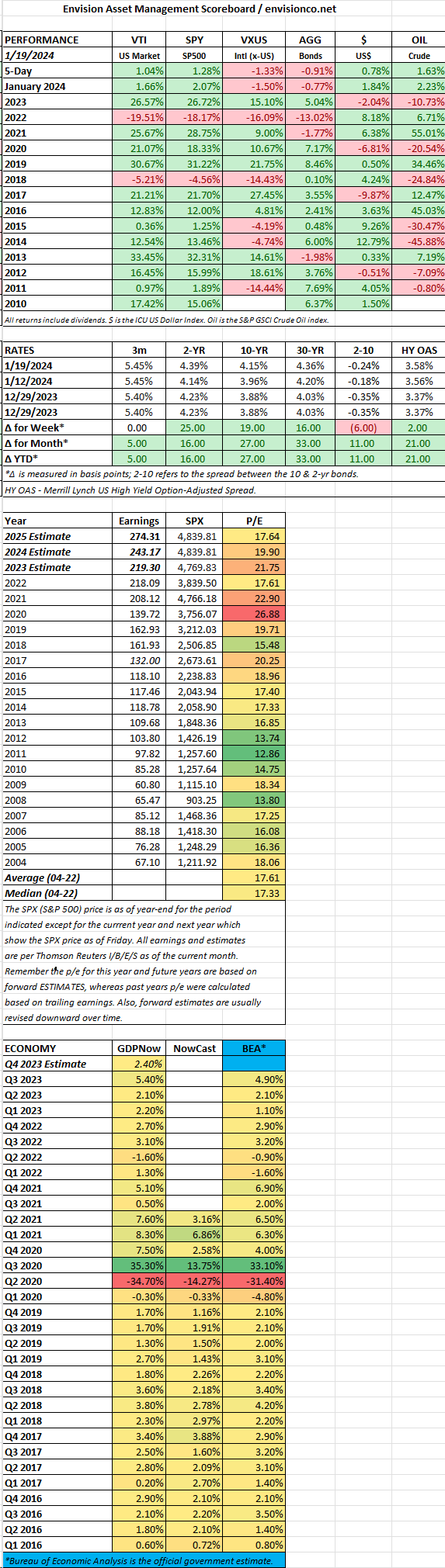

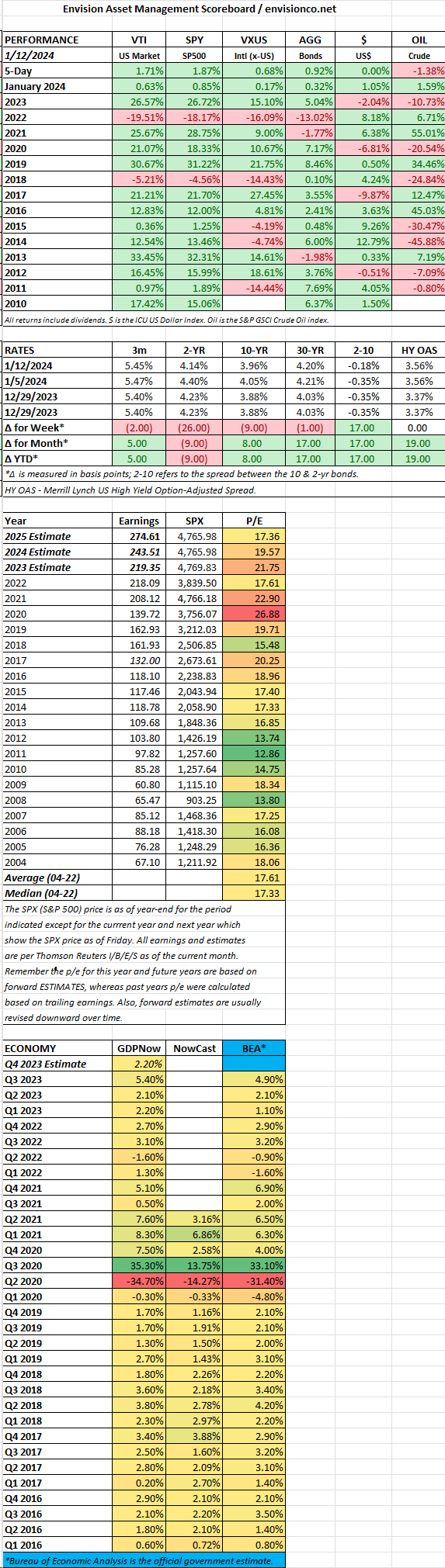

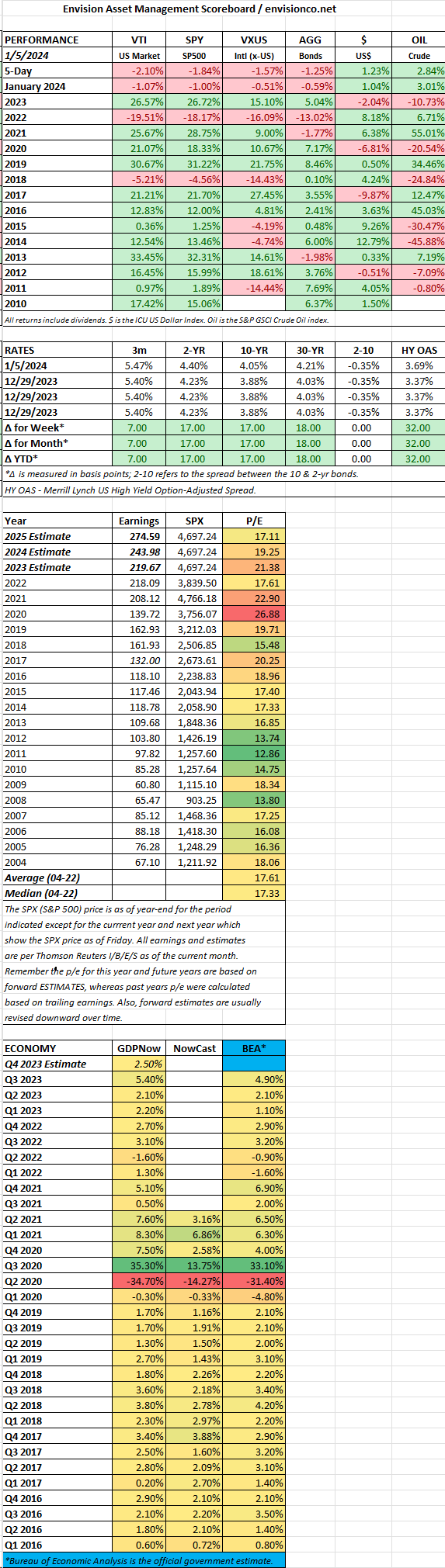

- US stocks are up by 1.04%, the Nasdaq by 2.3%, international stocks are down by 1.33%, and bonds fall by 0.91%. The yield on the 2-year treasury increased by 25 basis points to 4.39%, and the 10-year yield increased by 19 basis points to 4.15%.

- Expectations for Feb rate cuts, in terms of starting in March and in total number for 2024, are declining.

- Bitcoin, which had a recent peak on January 11th at $49,102, is now down almost 16% to $41,347. A classic example of sell on the news, as a bunch of bitcoin spot ETFs became available last week.

- Jobless claims are closing in on historic lows again, coming in at 187,000 this past week.

- University of Michigan consumer sentiment improved by the most since 2005, up by 9.1 points to 78.8.

- The Philadelphia Fed Manufacturing Index fell to -10.6, showing declining activity in that region.

- According to Barron’s, the Wall Street consensus is for S&P 500 earnings growth of 11% this year. But management is talking more conservatively.

- There is an estimated $8.8 trillion in money market funds. Part of the bull argument is that some of those funds will flow into equities if interest rates fall.

- Jacob Sonenshine writes in Barron’s that the earnings yield on the SPX is 5.3%, only 1.3% greater than the 4% 10-year treasury yield. Investors are optimistic and short interest is low, some of the reasons the market might be set for a correction.

SCOREBOARD