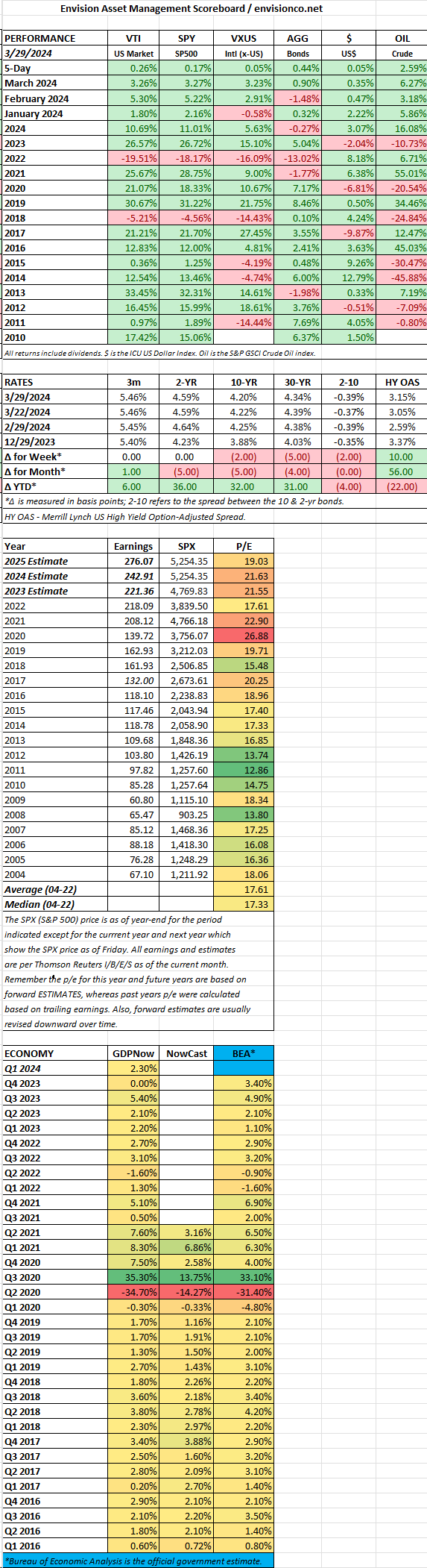

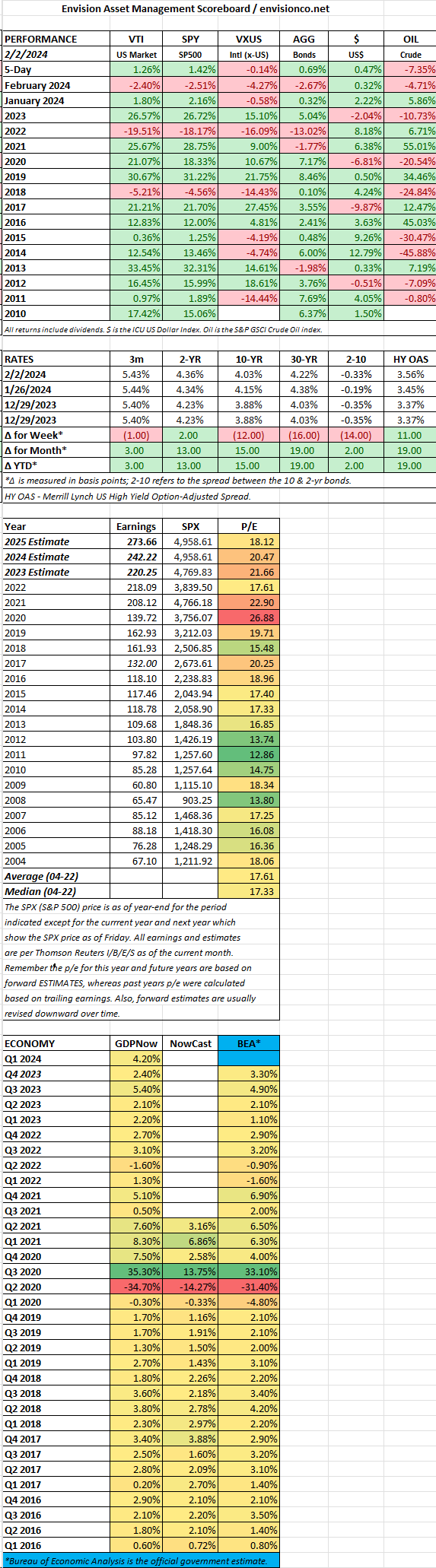

MARKET RECAP

- SPX +0.39%

- The SPX was up 10.2% for the quarter and managed 22 record closes along the way. It was the best performance for the first quarter since 2019. The market has been up more than 8% in Q1 16 times since 1950, the average gain for the rest of the year in those instances was 9.7% according to Dow Jones Market Data. Only one time did the market drop, and that was in 1987.

- The Personal Consumption Expenditures Price Index, excluding food and energy, was up 2.8% year over year and 0.3% for the month, matching estimates. Core PCE was up 2.5% and 0.3% compared to estimates of 2.5% and 0.4%.

- Consumer spending was up 0.8% for the month, beating the 0.5% estimate.

- The VIX closed at the ridiculously low level of 13.01, indicating no fear out in the equity market.

SCOREBOARD