MARKET RECAP

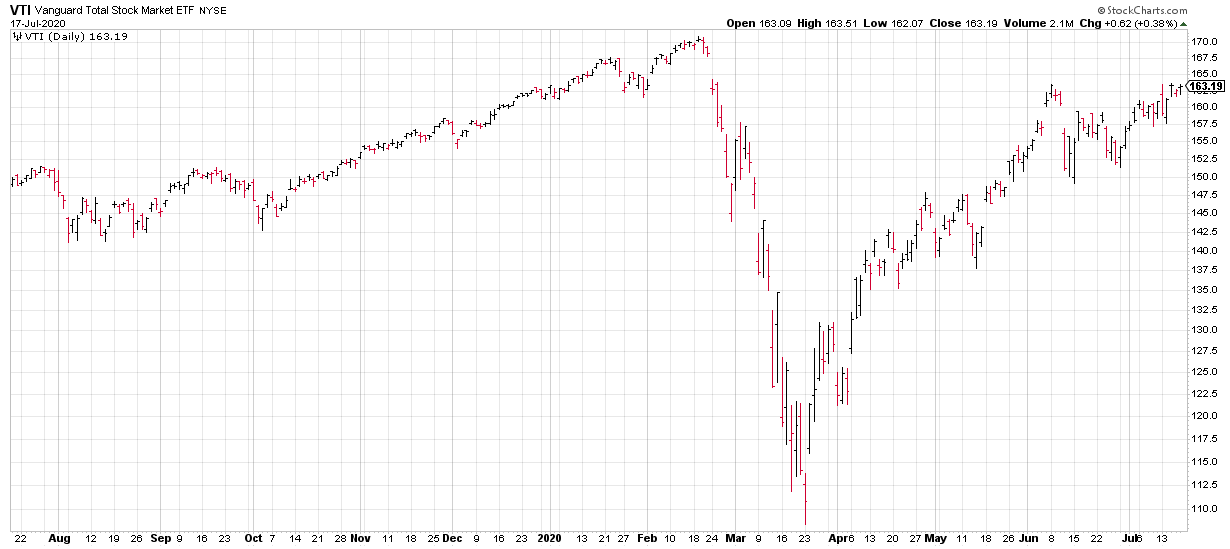

Stocks advanced around the world with the US up by 2.59% and international stocks by 2.23%. Bonds were flat.

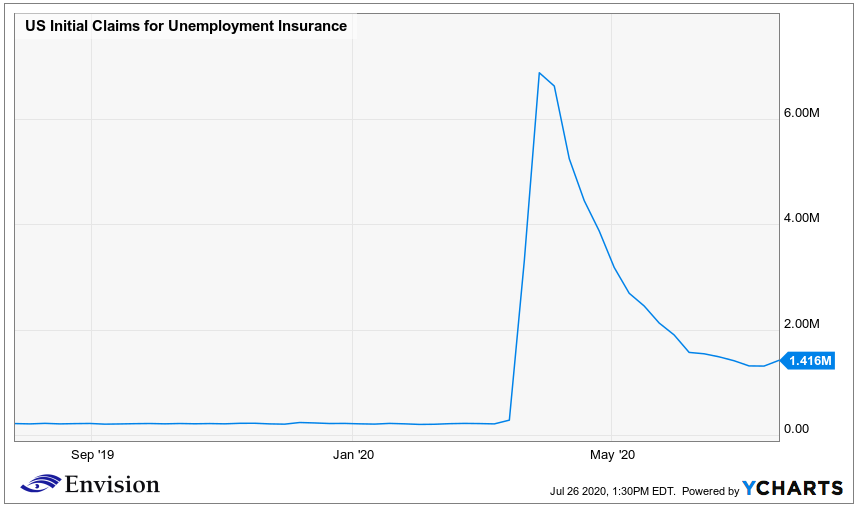

Employers added 1.763 million jobs and the unemployment rate fell to 10.2% in July, showing that the economy continues to improve, however, the rate of job improvement has slowed. In May, 2.7 million jobs were added and in June, there were an additional 4.8 million jobs. Overall, total jobs are down 13 million from February. 30 million people are still receiving jobless benefits.

The IMF projects that the economy in Latin America will fall by 9.4% this year, the worst decline ever, and it will take until 2023 to recover to pre-pandemic levels. That compares to 3% for developing countries and 8% for the US. Millions who climbed out of poverty are threatened. The United Nations said the number of poor people could rise by 45 million to 230 million, and the number of extremely poor can increase by 28 million to 96 million.

Trump is exerting pressure on Tik Tok, a social media platform owned by a Chinese company, to sell itself to Microsoft or be closed down. Chinese state media describe it as a “smash and grab”. On Monday, Trump then insisted that the US government be given a percentage of the sale price! Then on Friday, Trump issued an Executive Orders that seeks to prevent Americans from using the platform, effective in 45-days. You just cannot make this up.

Lord & Taylor filed for bankruptcy. L&T is the oldest US department store at 194 years.

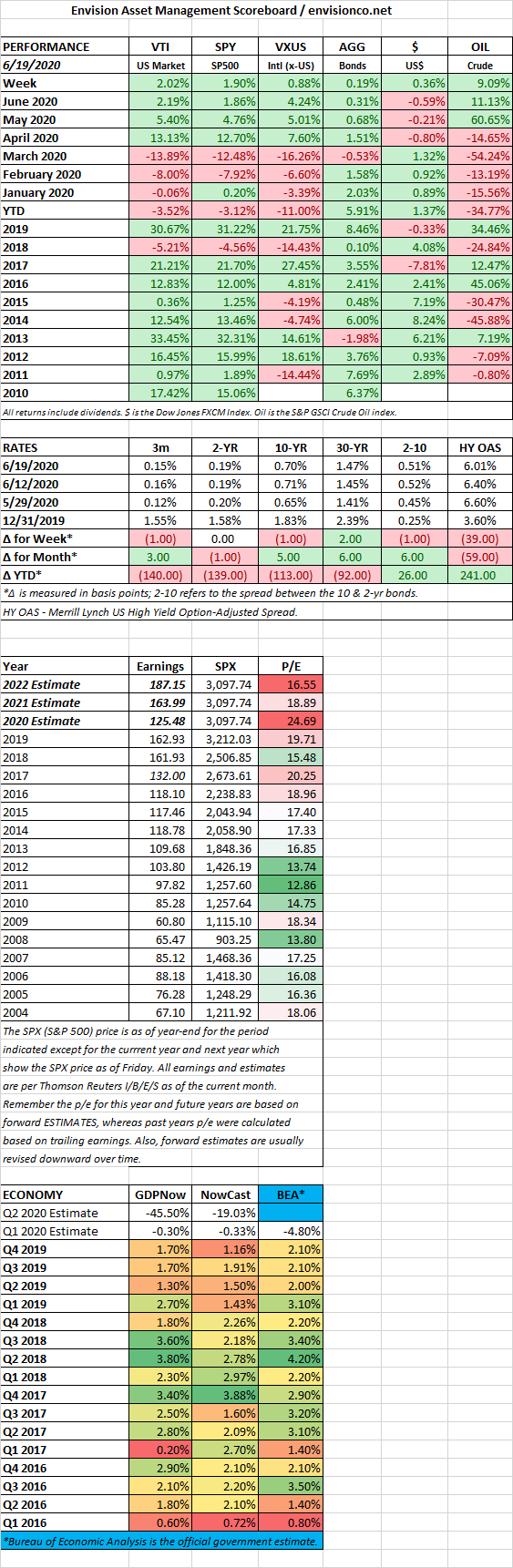

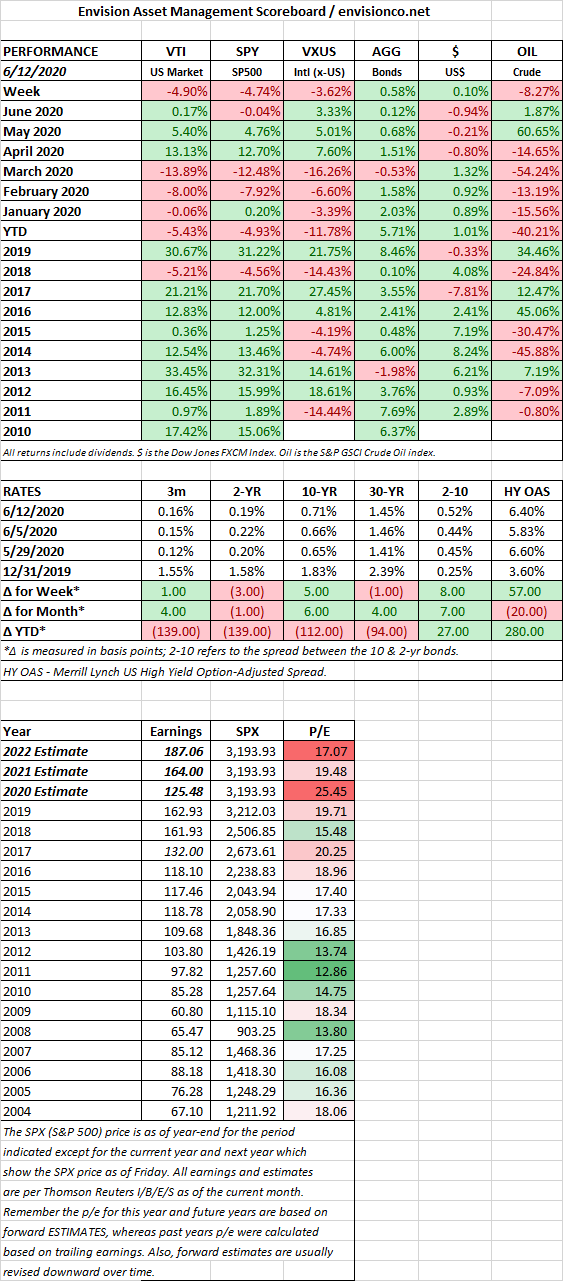

SCOREBOARD