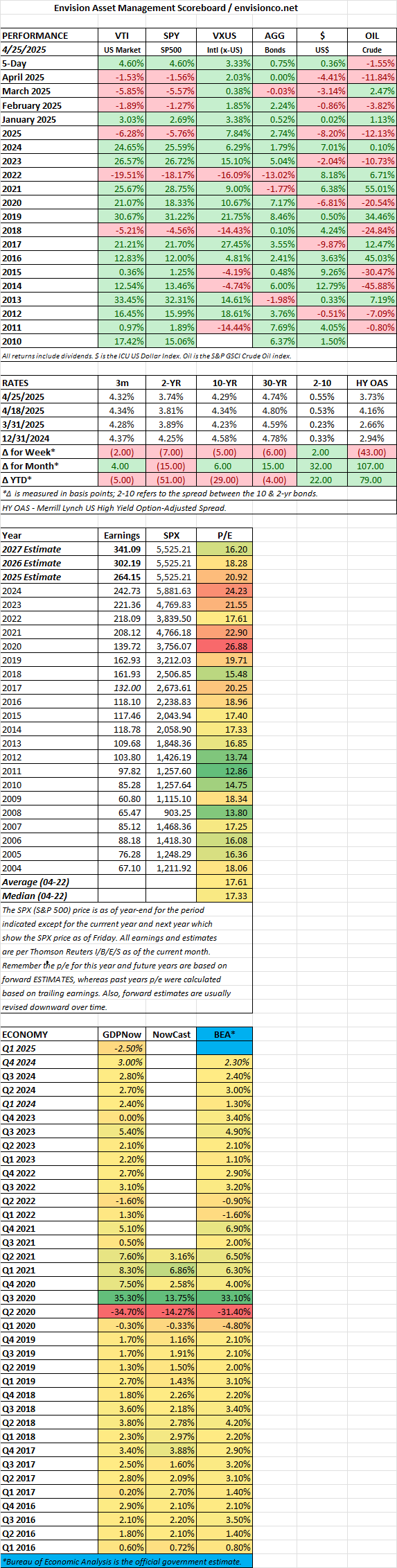

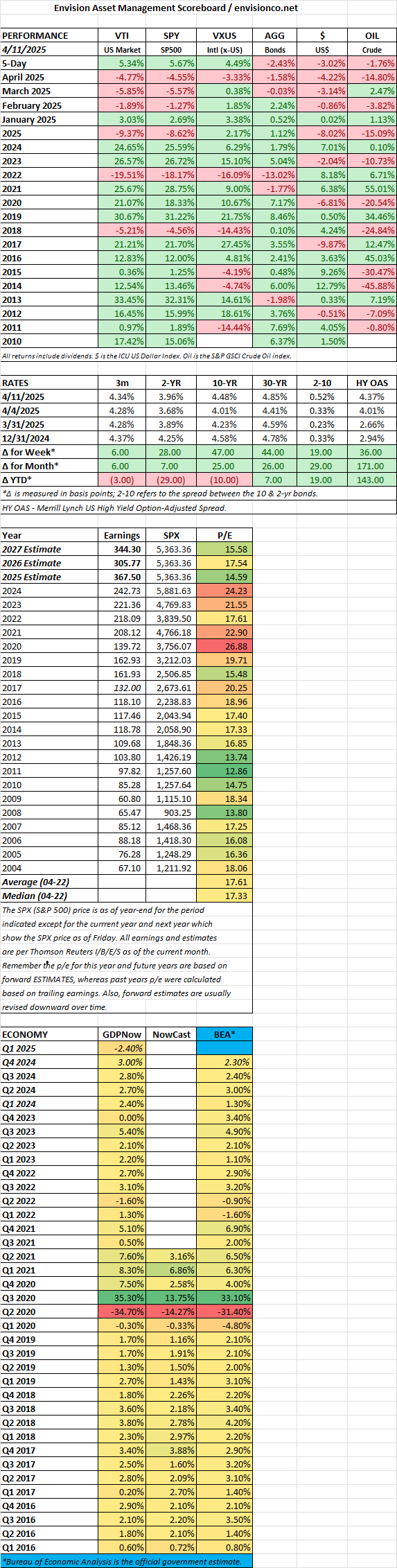

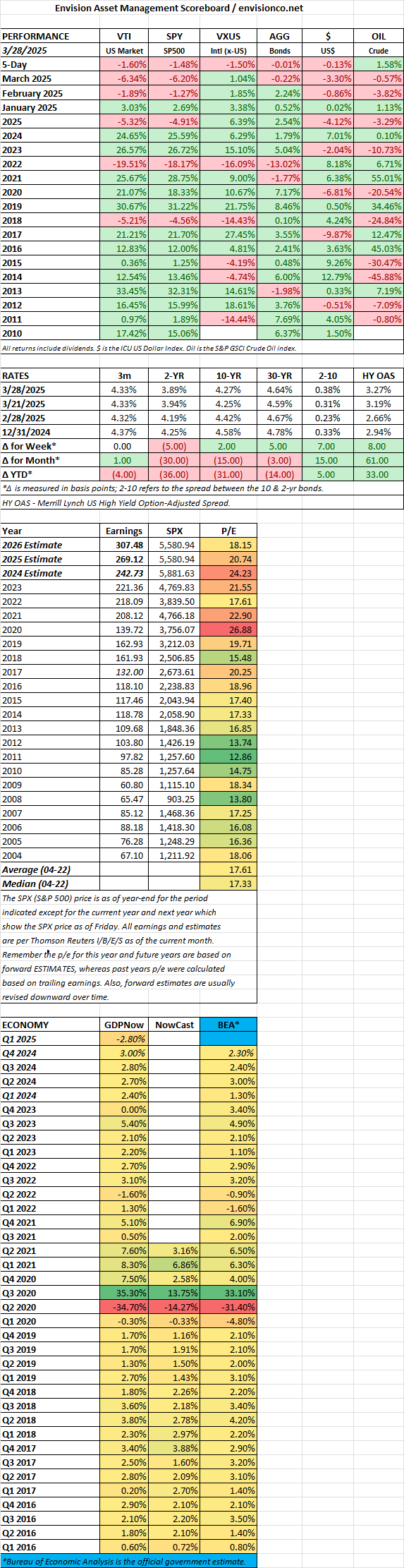

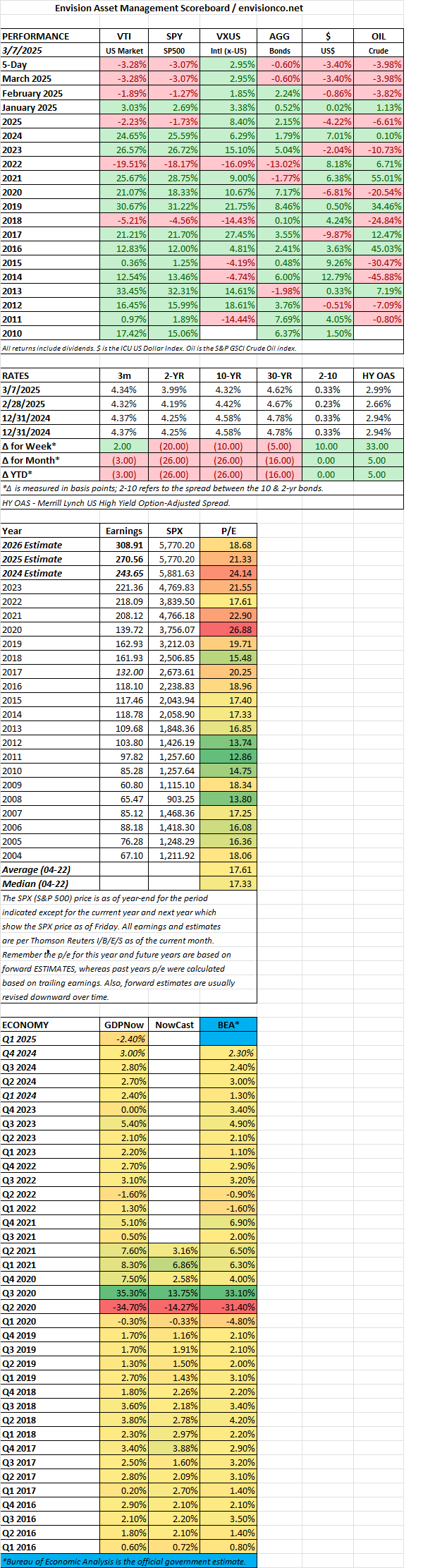

SCOREBOARD

SCOREBOARD

MARKET RECAP

SCOREBOARD

MARKET RECAP

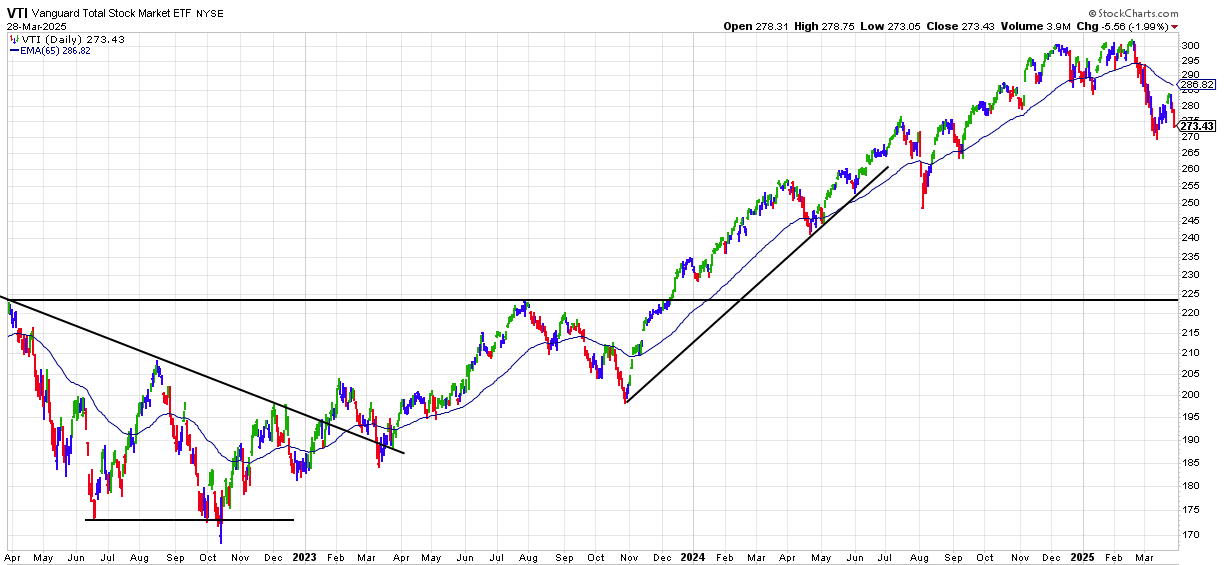

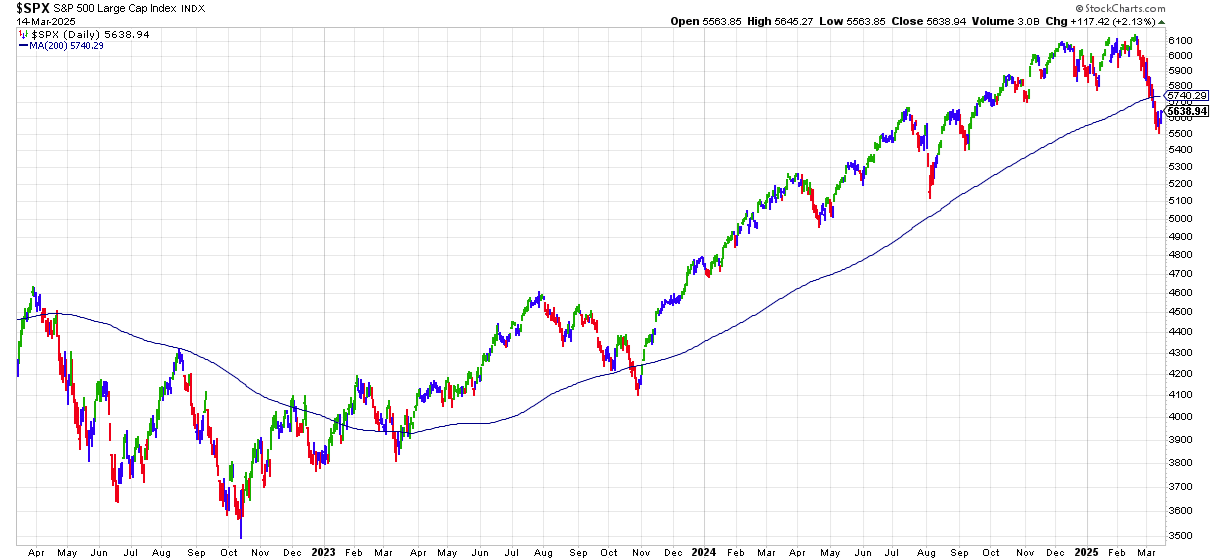

US STOCKS

SCOREBOARD

MARKET RECAP

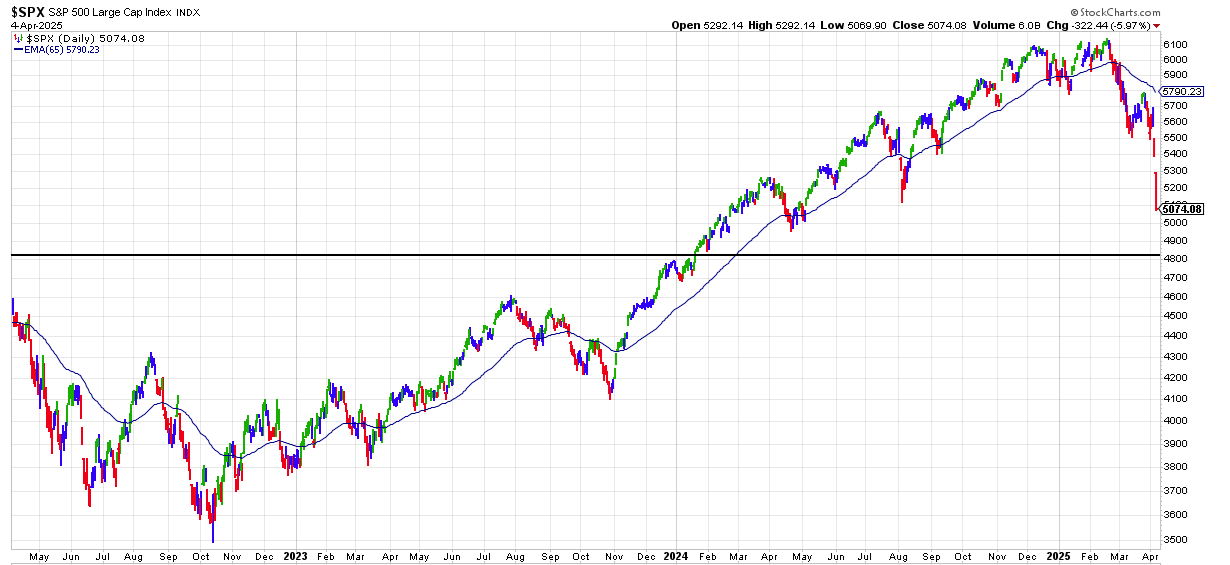

SPX

SCOREBOARD

Trump’s Tariff Policy: Playing with Fire

Trump is playing with fire, and the worst part is he doesn’t even realize it. He was re-elected mainly on the back of a few key issues: high inflation during the Biden era, the crisis of illegal immigration, controversies surrounding gender in sports, and other “woke” policies. Many voters hoped he would tackle these problems with strong, decisive leadership. And for the most part, he has delivered on some of these, although maybe not in the best way possible. What they didn’t vote for was a radical upheaval of the economic framework that has underpinned America’s rise as the most prosperous nation on Earth.

Instead, Trump is steering the country toward what can only be described as economic suicide, mainly through a reckless and unprecedented expansion of tariffs.

When used strategically, tariffs can serve as a useful bargaining chip in trade negotiations. That was the hope: Trump would leverage tariffs to strike better trade deals and reduce barriers between the United States and its trading partners. But it turns out, it was all just hope.

Rather than aiming for “reciprocal” tariffs—where the U.S. matches other countries’ rates—Trump has embraced a punitive approach based on trade imbalances. This means countries with whom we run trade deficits are being hit with steep tariffs, regardless of their own tariff policies.

Take Israel, for example. It dropped its tariffs on U.S. goods to zero. Instead of rewarding that move with reciprocal free trade, the U.S. slapped Israel with a 17% tariff simply because of a trade imbalance. That’s not reciprocity—that’s retaliation. It is also really bad economics. It punishes countries doing the right thing and distorts the very idea of fair trade.

Vietnam was hit with a staggering 46% tariff, despite becoming a manufacturing alternative to China—ironically, encouraged by the Trump administration during his first term. Now, companies that followed that guidance face devastating costs, with little warning and no clear rationale.

This kind of volatility undermines the trust that makes the U.S. a reliable economic partner. One of the key advantages of investing in America has always been its predictability: rule of law, open markets, stable policies. But if each administration can unilaterally upend the trade system on a whim, what does that say about our credibility?

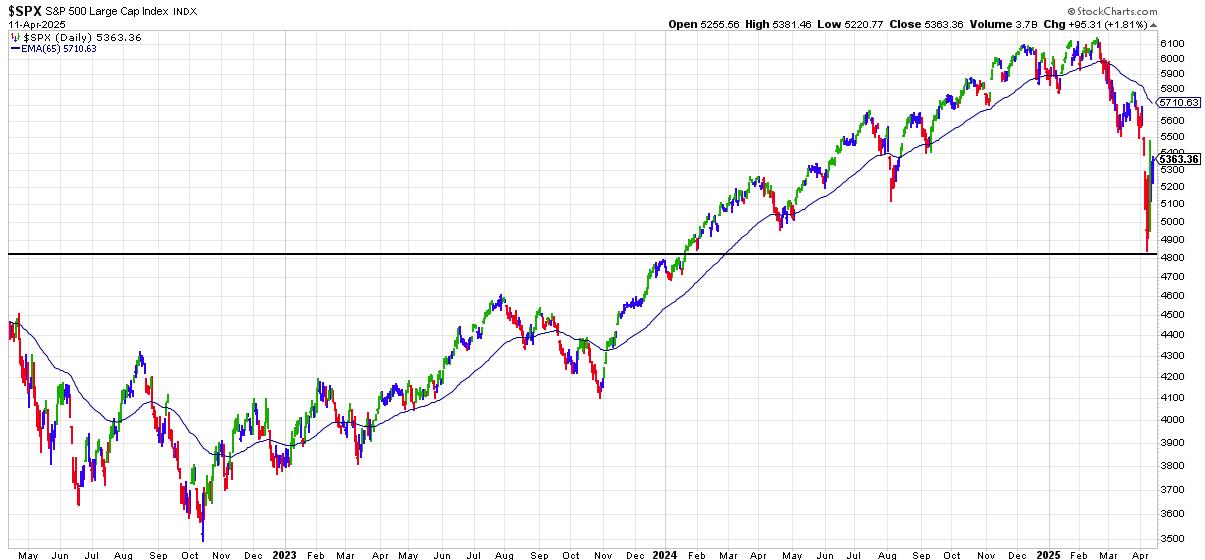

The equity markets have already responded harshly. Over $5 trillion in market value has been erased within the last few days, with businesses and investors now uncertain about the future of trade under Trump’s policies. This is not a temporary blip—if these tariffs persist, the impact on inflation, business confidence, and supply chains will be long-lasting and painful.

Like the “transitory” inflation we saw post-COVID, tariff-driven inflation will be just as sticky and maybe worse. The U.S. cannot simply replicate complex, highly optimized global supply chains overnight—or even over several years. The result will be higher prices for consumers, lower profits for businesses, and a less competitive American economy overall.

Perhaps most alarming is how these tariffs are being enacted. Trump is invoking the International Emergency Economic Powers Act of 1977—a law meant for genuine national emergencies—to justify these sweeping economic changes. But there is no emergency, only a manufactured justification for a deeply flawed policy. This is taxation without representation: hundreds of billions of dollars in new taxes imposed on Americans, without congressional approval or public debate.

Not only does this bypass the legislative process, but it also violates existing trade agreements—including some that Trump himself negotiated. It risks permanently damaging our trade relationships and giving countries like China an opening to deepen ties with nations that feel betrayed by the U.S.

Is there a single respected economist not affiliated with the Trump administration who supports this policy? It’s doubtful. The hope, among some observers, is that Trump is using this strategy as a high-stakes negotiation tactic—an attempt to force other countries to the table to drop their tariffs to zero. But even if that’s the plan, the collateral damage is immense.

If this continues unchecked, it could lead to serious consequences—not just economically, but politically. Voters will punish Republicans in upcoming elections, especially as inflation rises and job losses mount. The tariff policy, as it stands today, is deeply unpopular, economically reckless, and fundamentally un-American in its disregard for free trade and fair competition.

Wasn’t the lesson of the 1930s that the Great Depression was made much worse because of the Smoot-Hawley tariffs? Didn’t everyone learn this in eighth grade? This is from the Senate’s own website (https://www.senate.gov/artandhistory/history/minute/Senate_Passes_Smoot_Hawley_Tariff.htm):

How did this happen? After Herbert Hoover became president in 1929, he called Congress into special session to deal with a troubled farm economy that had fallen into depression during the otherwise prosperous 1920s. President Hoover proposed a “limited revision” of the tariff on agricultural imports to raise rates and boost sagging farm prices. He then made the tactical error of trying to distance himself from the tariff debates. Republican protectionists, who controlled the House Ways and Means Committee chaired by Representative Willis Hawley, put the farm issue aside and took the opportunity to raise industrial tariffs to new highs. Hoover’s failure to object encouraged other economic interests to lobby the Senate Finance Committee, chaired by Utah senator Reed Smoot, for further tariff hikes. In protest, low-tariff Democrats and progressive Republicans slowed the tariff debate over a tedious 15-month process of congressional bargaining.

A thousand economists signed a petition, drafted by a Chicago economist, and future U.S. senator, Paul Douglas, that implored the president to veto the tariff. “Poor Hoover wanted to take our advice,” Paul Douglas mused, but he could not bring himself to break with his own party’s congressional leadership. Ignoring the experts, Hoover signed the tariff on June 17, 1930.

As the economists predicted, the high tariff proved to be a disaster. Even before its enactment, U.S. trading partners began retaliating by raising their tariff rates, which froze international trade. The tariff fight solidified Hoover’s ties with Republican regulars, but it shredded his standing among his party’s progressives. Most of the progressive Republican senators who had campaigned for Hoover in 1928 wound up endorsing Franklin D. Roosevelt for president in the next election. Nor did the tariff sit well with the voters. In 1932 they turned the majority in both houses over to the Democrats, by large margins. The voters also made clear their disdain for the Smoot-Hawley tariff by booting Jboth Reed Smoot and Willis Hawley out of office that year.

“This is a moment of testing for Trump’s advisors. The intellectually honest ones know that this reflects the President’s 40-year fixation, not any kind of a proven economic theory. This is the economic equivalent of what creationism is to biology or what ending vaccines is to medicine. The question is whether his advisors are going to have the courage to tell him and the courage to step away from being part of these policies, if he’s not willing to readjust.” (https://x.com/ThisWeekABC).

The U.S. should be leading the world toward freer markets and stronger global partnerships, not retreating into protectionism and economic isolation. The goal should be simple and clear: reduce tariffs to zero and let open markets determine the winners. That’s the best path to prosperity—for America and the world.

If Congress or the courts do not act soon to rein in Trump’s authority on trade, the consequences could be devastating—for the economy, our international relationships, and the long-term credibility of the United States on the world stage.

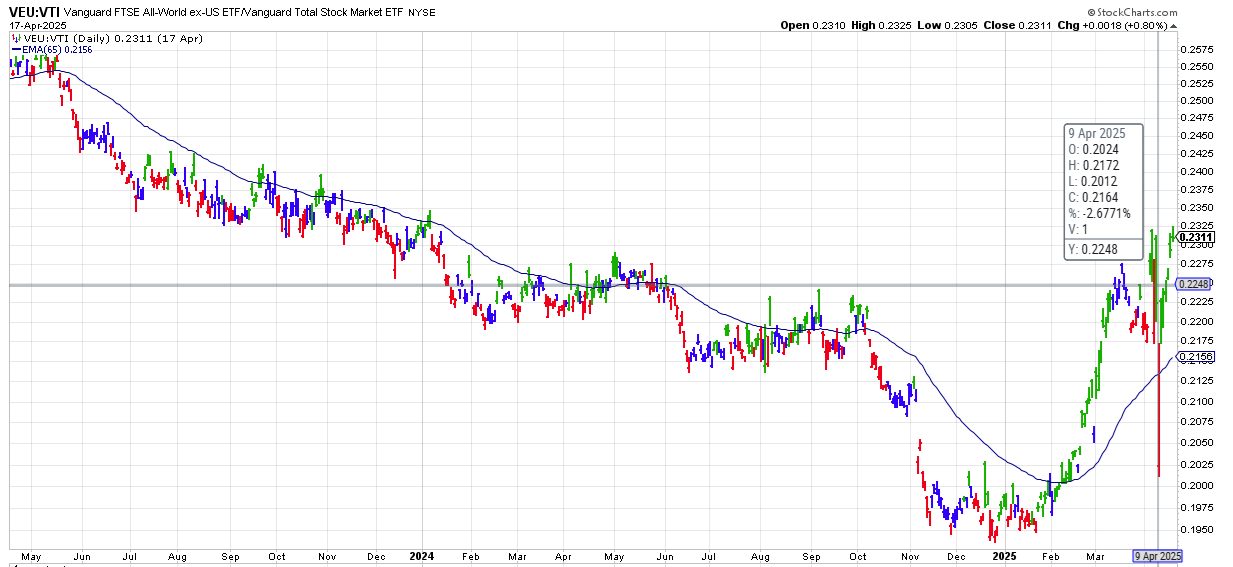

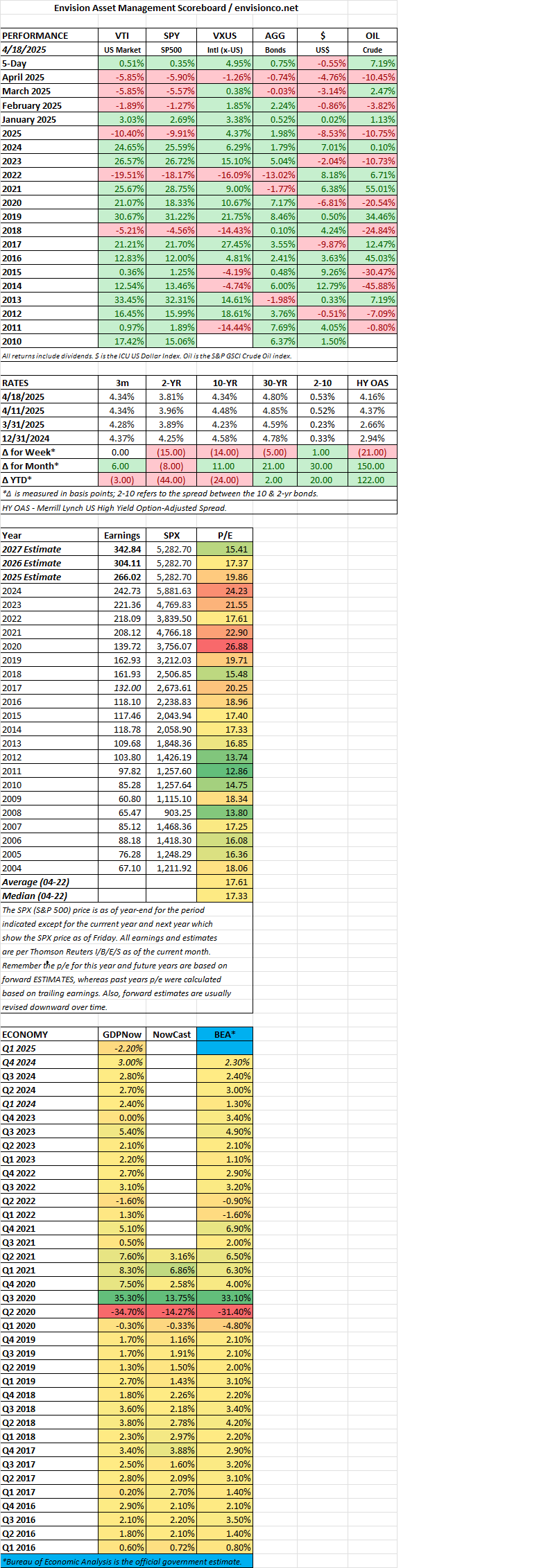

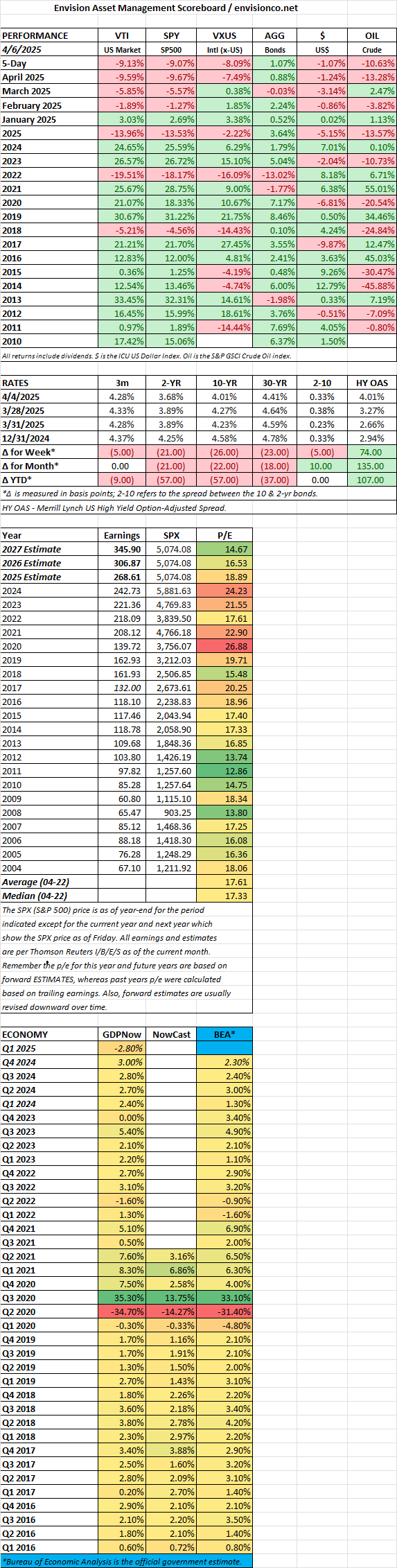

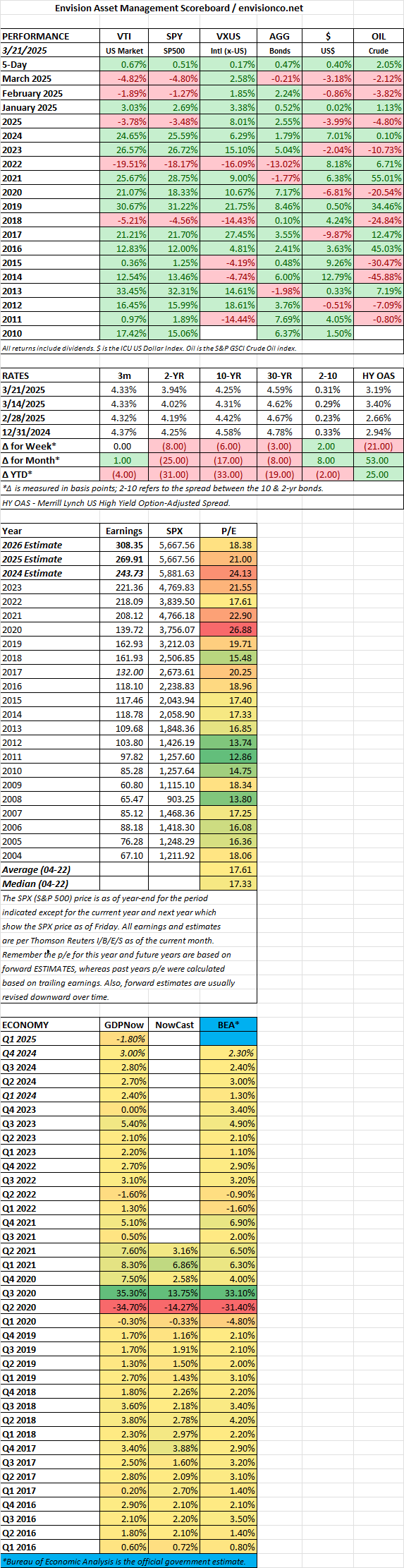

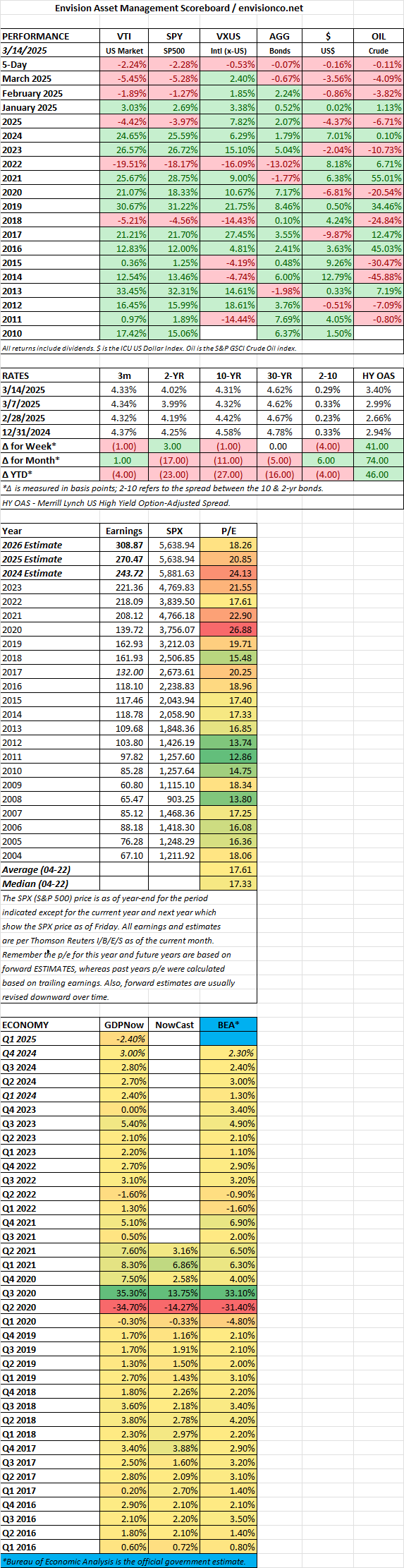

US STOCK MARKET

SCOREBOARD

SCOREBOARD

MARKET RECAP

SP500

SCOREBOARD

MARKET RECAP

SCOREBOARD

MARKET RECAP

SCOREBOARD