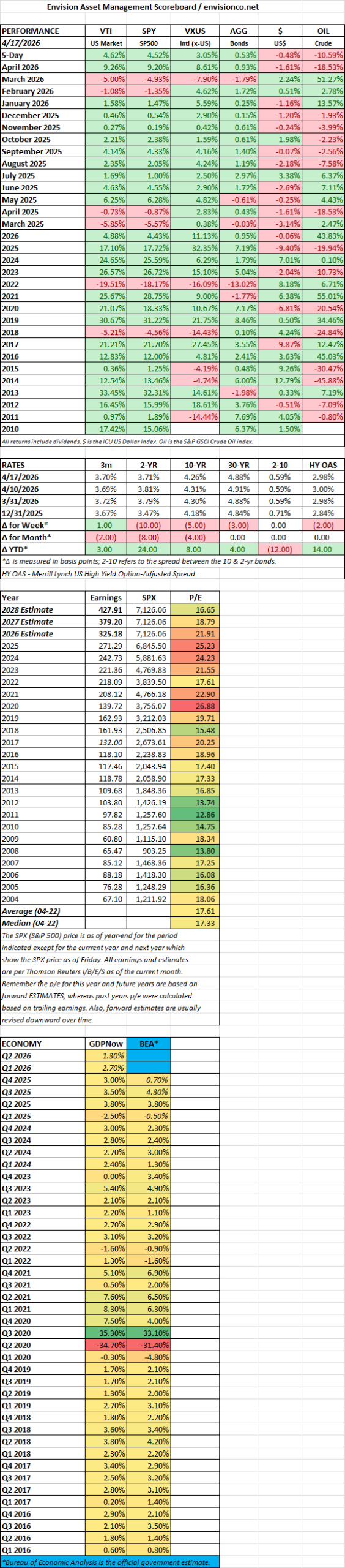

SCOREBOARD

SCOREBOARD

SCOREBOARD

SCOREBOARD

SCOREBOARD

MARKET RECAP

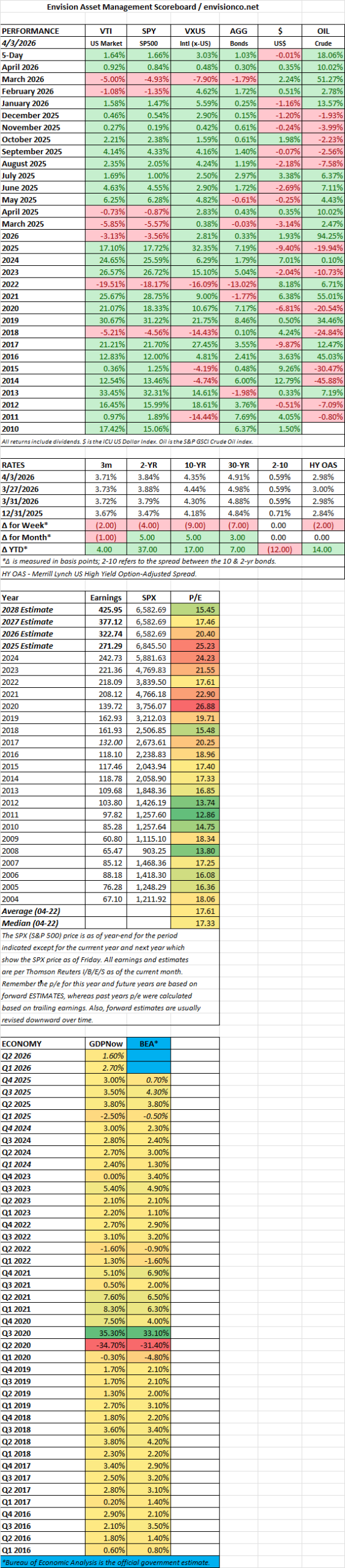

Global Market Divergence: American equities are lagging significantly behind international markets so far this year. While the S&P 500 has remained nearly flat with a 0.60% total return, a broad index of non-U.S. stocks has climbed 11.09% over the same period.

Japanese Market Milestone: Japan’s TOPIX reached a new historic peak this week. Since hitting a relative low in January of last year, the index has beaten the S&P 500 by more than 28 percentage points.

SCOREBOARD

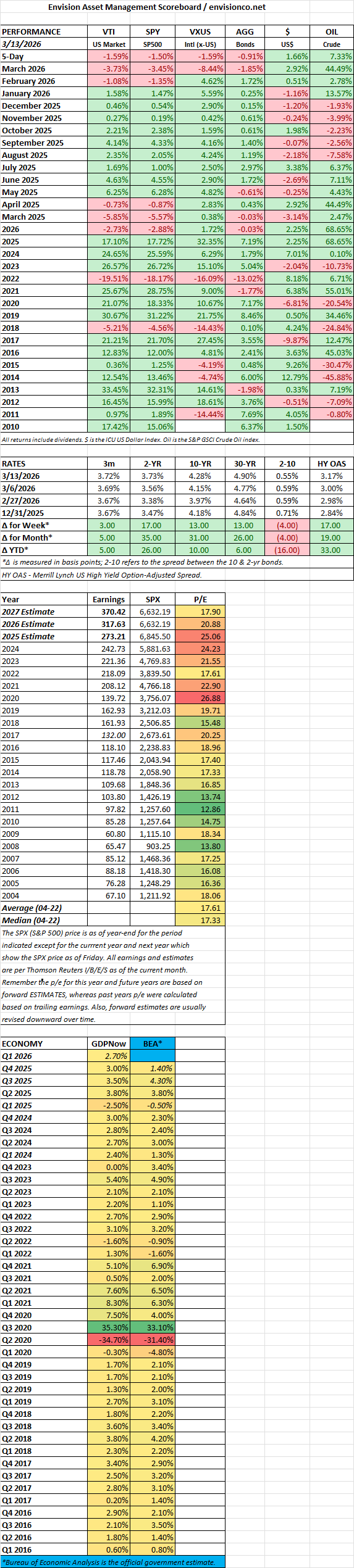

MARKET RECAP

SCOREBOARD

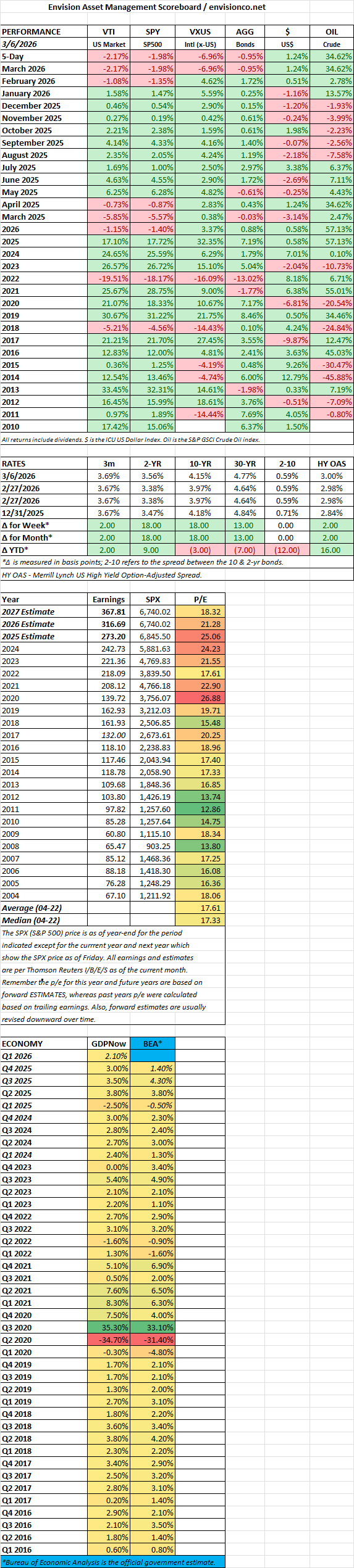

MARKET RECAP

SCOREBOARD

SCOREBOARD

SCOREBOARD