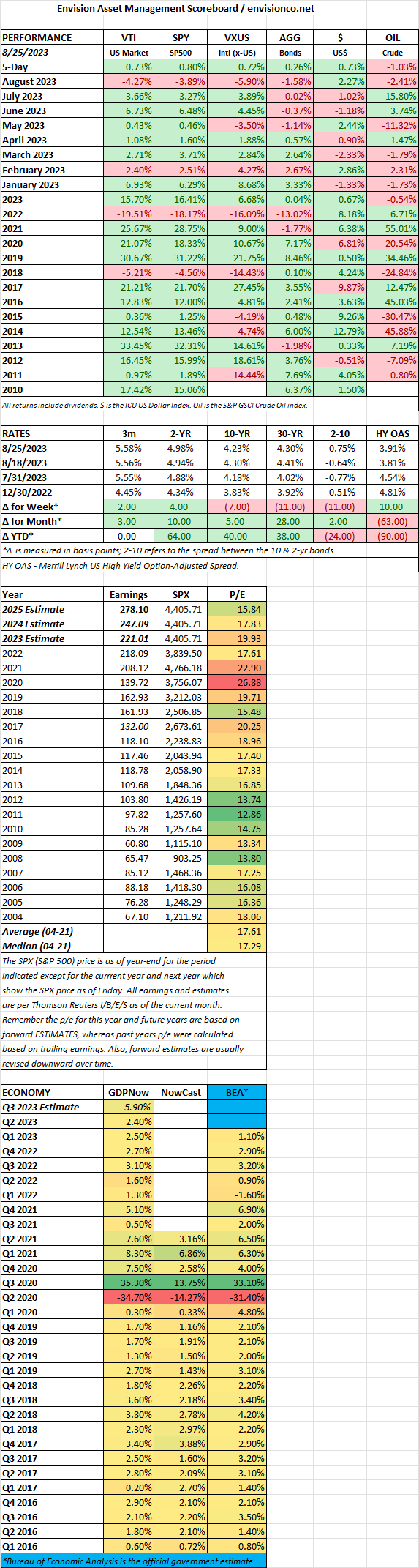

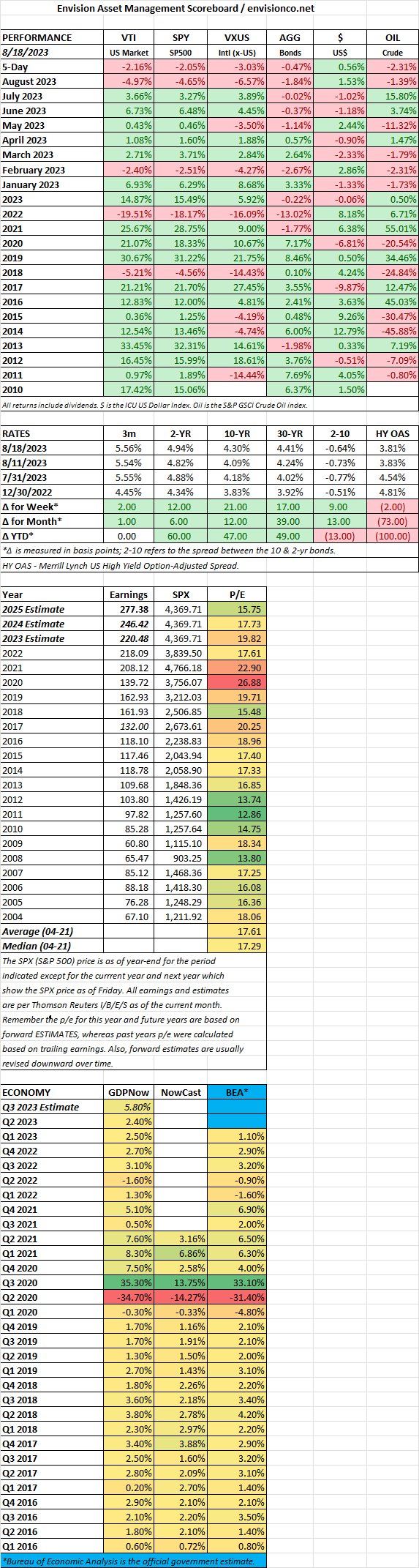

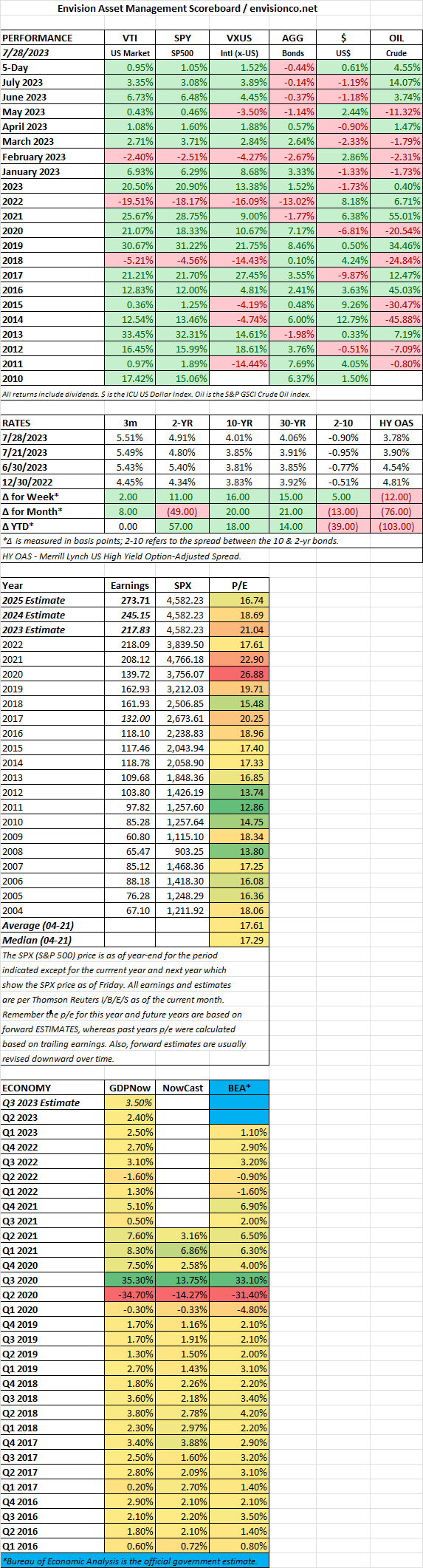

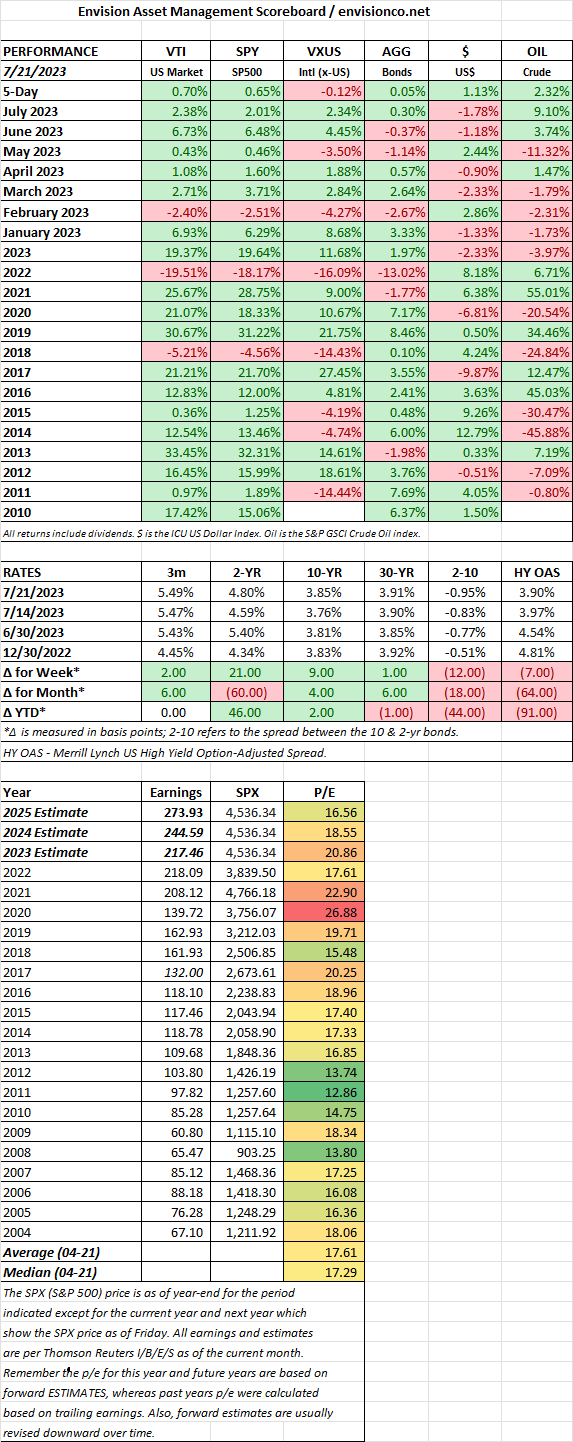

August 2023: A Month of Two Halves for Financial Markets

The summer heat wasn’t the only thing that cooled down in August. After a promising July, financial markets faced a reality check and retreated across most asset classes. Here’s a breakdown of the key themes:

Equity Market Tumble:

- Major indices retreated, ending the month on a sour note.

- The S&P 500 lost 1.5%, the Dow Jones slipped 2.0%, and the NASDAQ dipped 2.1%.

- The first half rally fizzled out, with all major sectors ending the month in negative territory.

Rising Interest Rates:

- Hawkish rhetoric from Fed officials and stronger-than-expected economic data revived concerns about higher interest rates.

- The 10-year Treasury yield climbed from 3.75% to 4.15%, reflecting investor expectations of further tightening.

- This put pressure on equities, particularly growth stocks sensitive to higher borrowing costs.

Mixed Global Performance:

- International markets experienced a more pronounced downturn.

- The MSCI EAFE fell 3.8%, dragged down by European worries and a stronger dollar.

- Emerging markets suffered even more, with the MSCI EM tumbling 6.2% amidst concerns about China’s slowing economy and geopolitical tensions.

Economic Data Rollercoaster:

- Positive job numbers and retail sales were overshadowed by weaker consumer confidence, mortgage applications, and manufacturing activity.

- This mixed bag left investors uncertain about the true state of the economy and its future trajectory.

Other Notable Events:

- China’s property sector turmoil triggered fears of contagion in global markets.

- Tensions between the US and China regarding Taiwan continued to cast a shadow on sentiment.

- The war in Ukraine remained a source of concern and uncertainty.

Overall, August 2023 painted a picture of financial markets adjusting to a changing environment. The initial optimism fueled by easing inflation and strong earnings gave way to anxieties about rising interest rates, slowing economic growth, and geopolitical risks. The next few months will be crucial in determining whether this pullback is a temporary correction or a sign of a more extended downward trend.