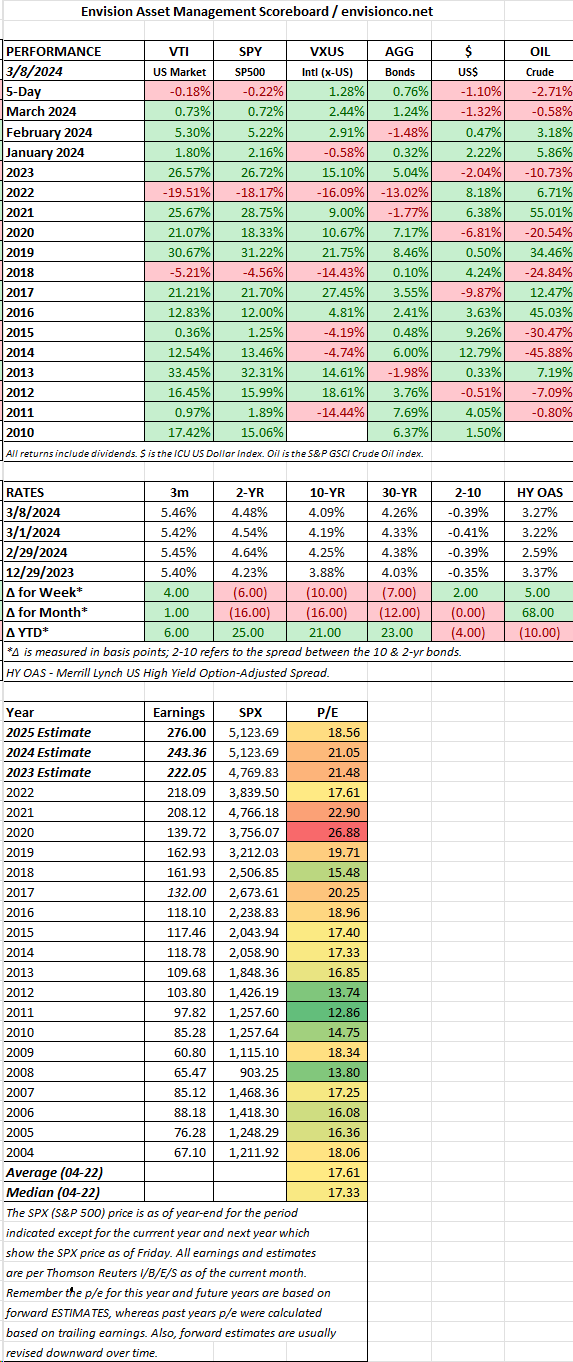

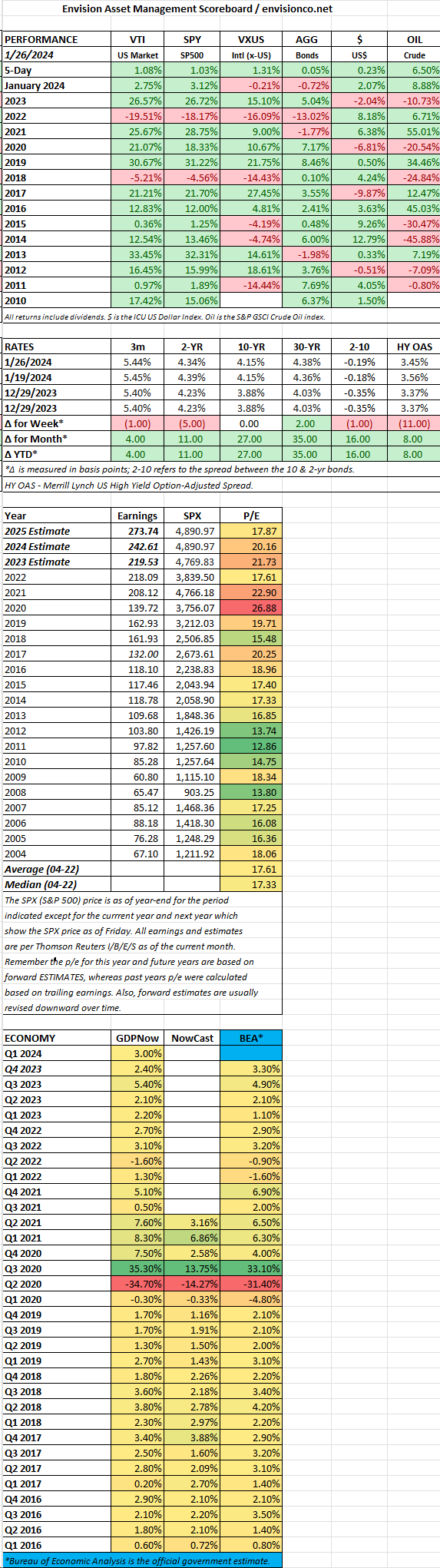

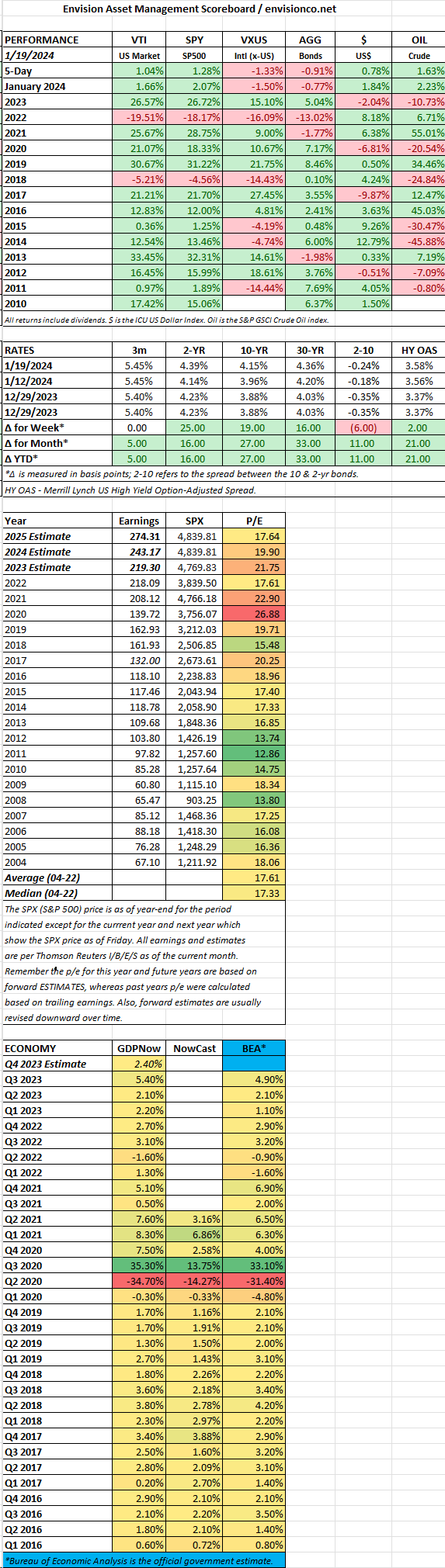

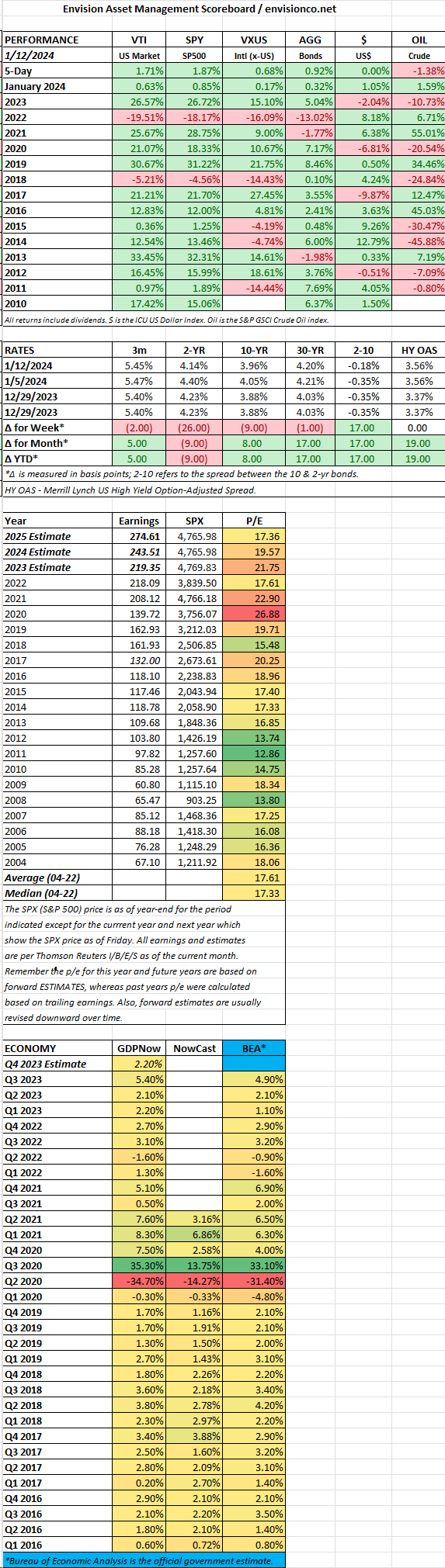

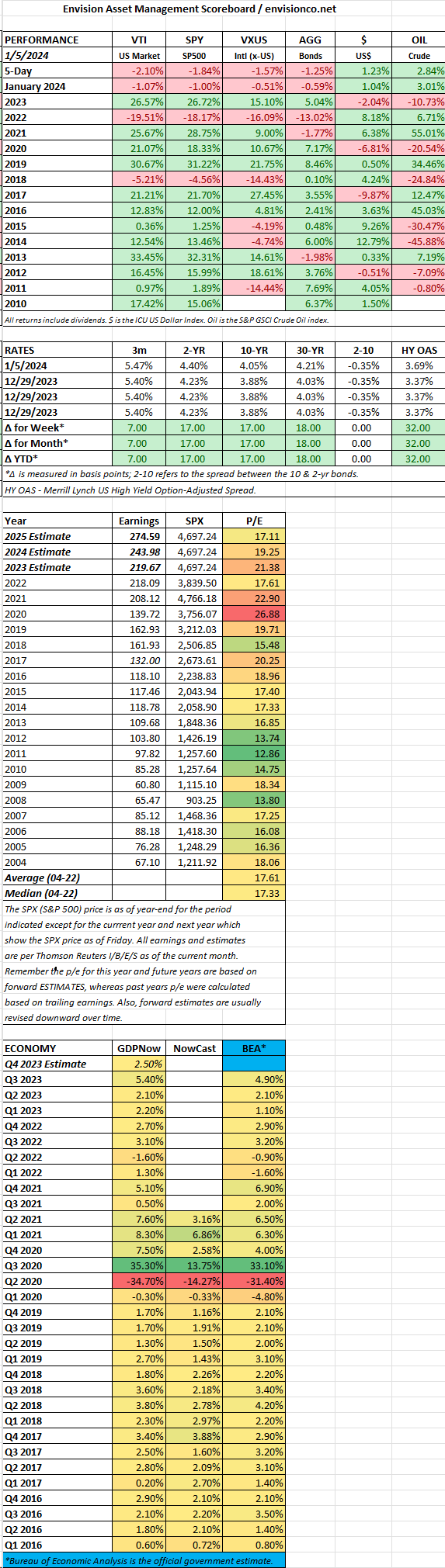

MARKET RECAP

- US stocks -0.18%, international +1.28%, bonds +0.76%.

- Nonfarm payrolls increased by 275,000, beating the estimate of 198,000. But January hiring was revised downward by 124,000. The unemployment rate increased to 3.9%. Average hourly earnings were 0.1% higher compared to January. much lower than the 0.5% increase in January.

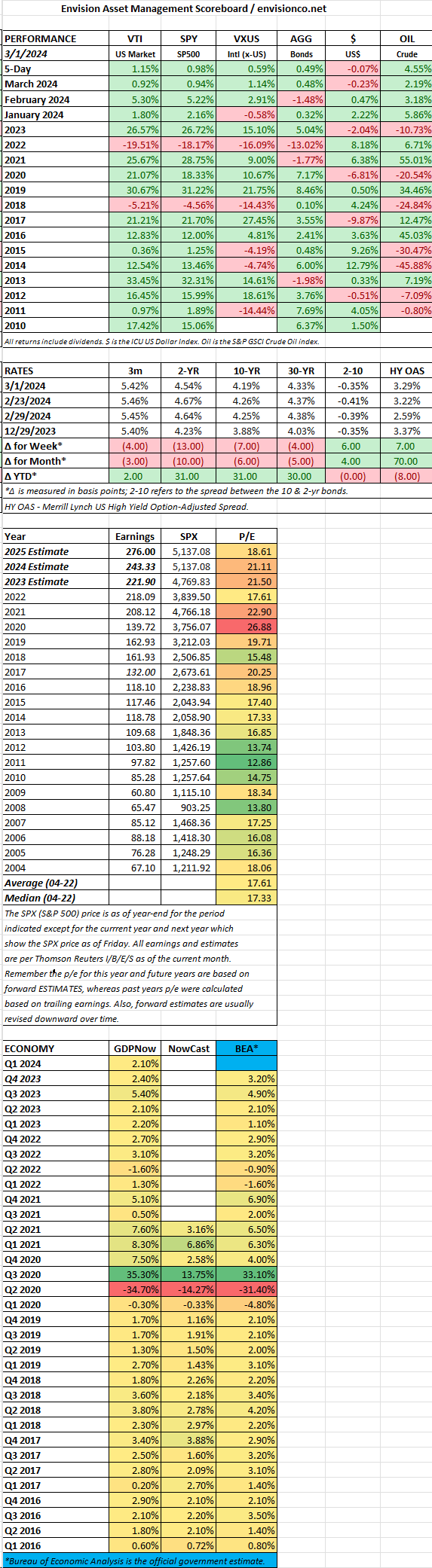

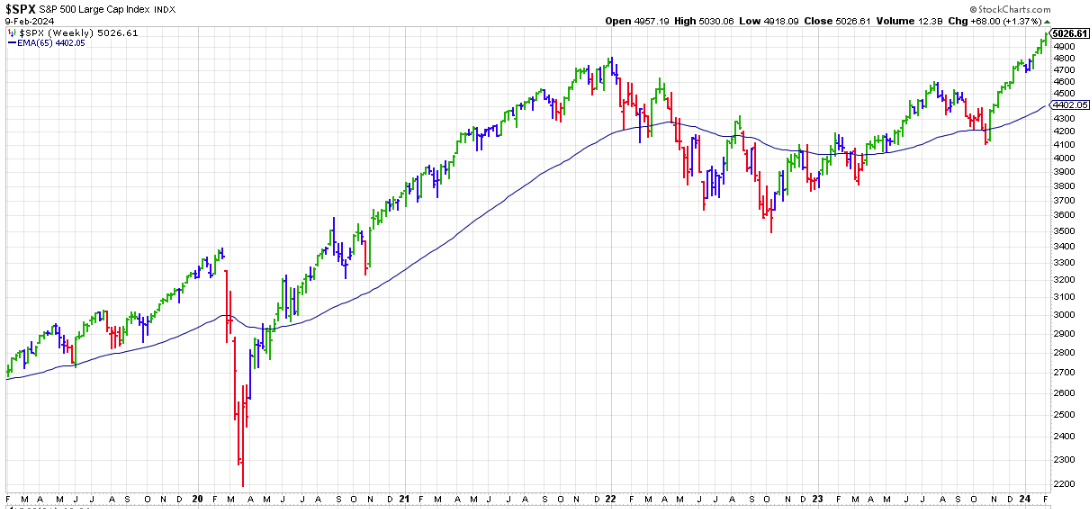

- Through March 1, the SPX has been up 16 out of 18 weeks, the first time that has happened in 53 years, according to Deutsche Bank’s Jim Reid.

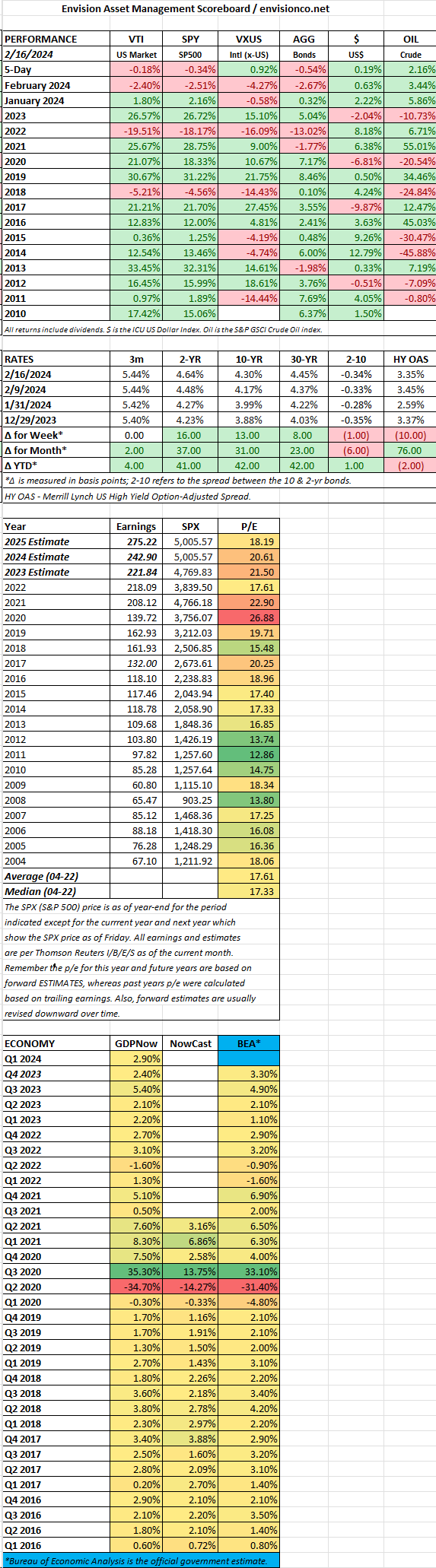

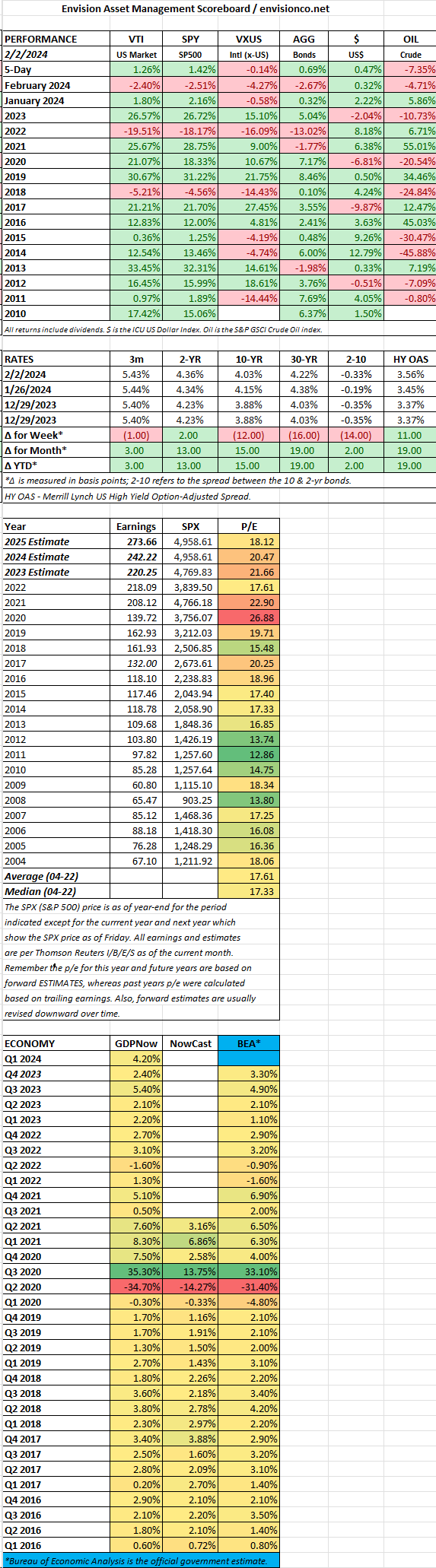

- The SPX is trading at 21x forward earnings.

- Nikki Haley dropped out of the Republican race, setting up a rematch nobody wants. Trump seems to have an edge in the polls, but I think Biden will win. The Democrats have between now and election day to remind everyone of life under Trump, especially January 6th and Trump’s behavior during and after.

SCOREBOARD