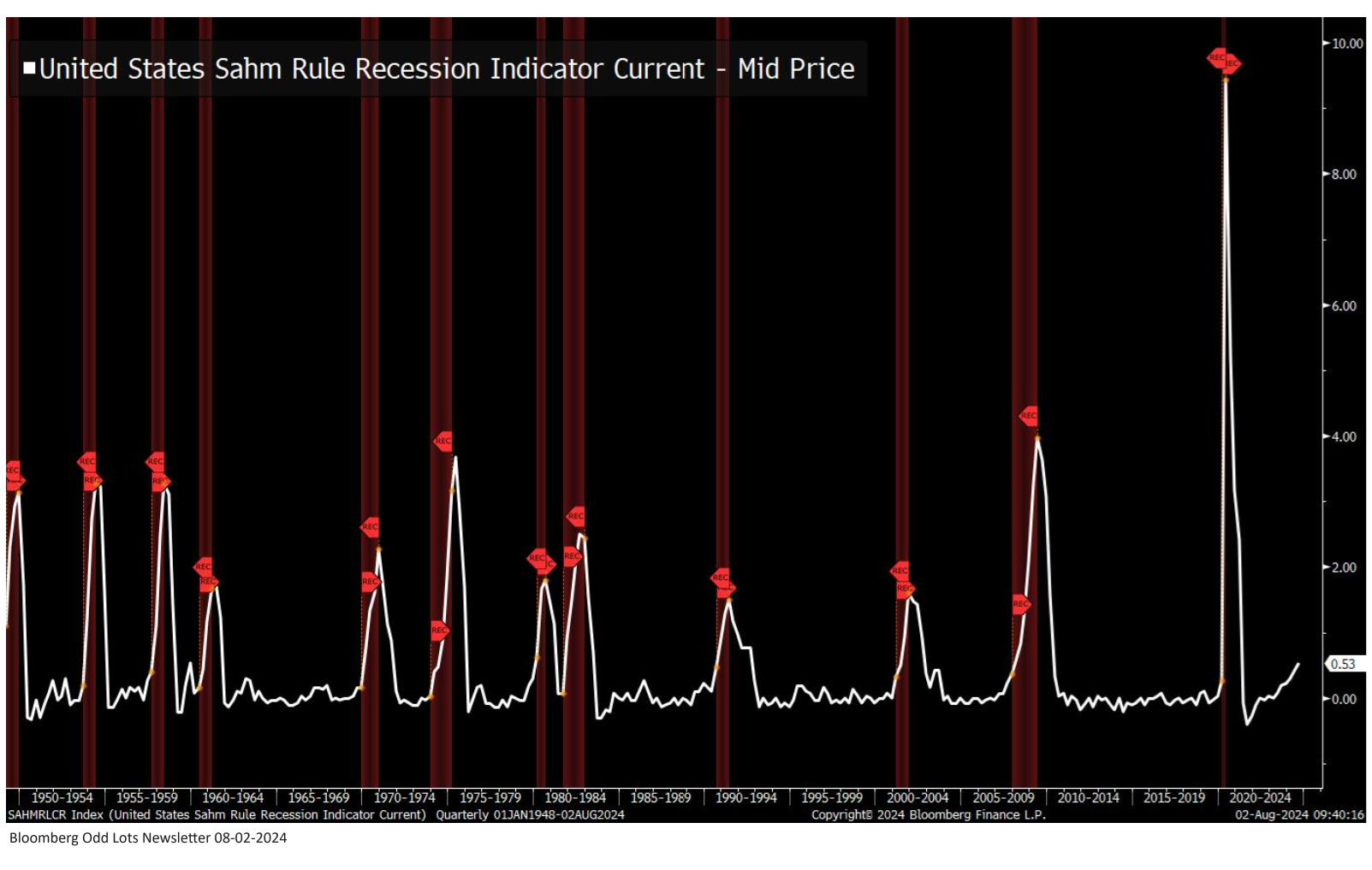

MARKET RECAP

- US stocks decline by 1.66% and international stocks by 2.64%. US small caps increased by 1.7%. The NASDAQ was off by 3.65%.

- On Wednesday, the Nasdaq had its worst day in two years due to fears of tighter regulation on chip sales to Congress.

- Fears of a trade war weighed on the market as the week progressed, courtesy of the Trump/Vance platform.

- On Friday, a worldwide software failure impacted businesses almost everywhere due to one line of bad code written by Crowdstrike.

TRUMP

Trump had a chance to make a positive statement at the Republican National Convention. Just a few days after the assassination attempt, with most of the entire country ready to give him a chance, he could have made an honest attempt to broaden his coalition and act like he wanted to unite the country. But just like you would think, he opened up his speech with most of the right notes, but it quickly deteriorated into a rambling, hateful, attack-filled, dark diatribe about Democrats and the current state of the world and the country. Of which, of course, only he could solve, often in as little as a day or two, and simply with a phone call. Trump is crazy, and while the Republican convention-goers swallow it up hook, line, and sinker, most of the rest of the nation realizes he is as bad as ever.

He delivered the longest presidential nomination acceptance speech on record; almost all of it was rambling and off the cuff. Trump is mad at the world and paranoid, believing that he has magical powers to solve problems immediately and that only he can do this.

Even with that, he leads in the polls because Biden appeared frail and unable to continue as President. Today (Sunday), Biden announced that he will withdraw from the race, so the Dems have a chance to rally now and can win if they nominate the right person. Kamila Harris appears to be that nominee, and I would not consider her the right person.

Trump is a weak candidate. And I say this knowing full and well that the Republicans left the convention all fired up and confident in what was a high-energy and well-run event, sure that they will win in November.

But as described above, Trump is still Trump, and he is not mentally well, and the voters in the middle understand that, and they will tilt the election, one way or the other. The big problem with the Democrats is that their policies, which seem to be driven by the far left, are so bad and so harmful for America and its culture that a lot of the middle will lean towards Trump despite his meanness, craziness, and mental instability.

If only there were a reasonable centrist candidate. But at least for now, there isn’t so that Americans will be faced with two bad choices. Let’s hope.

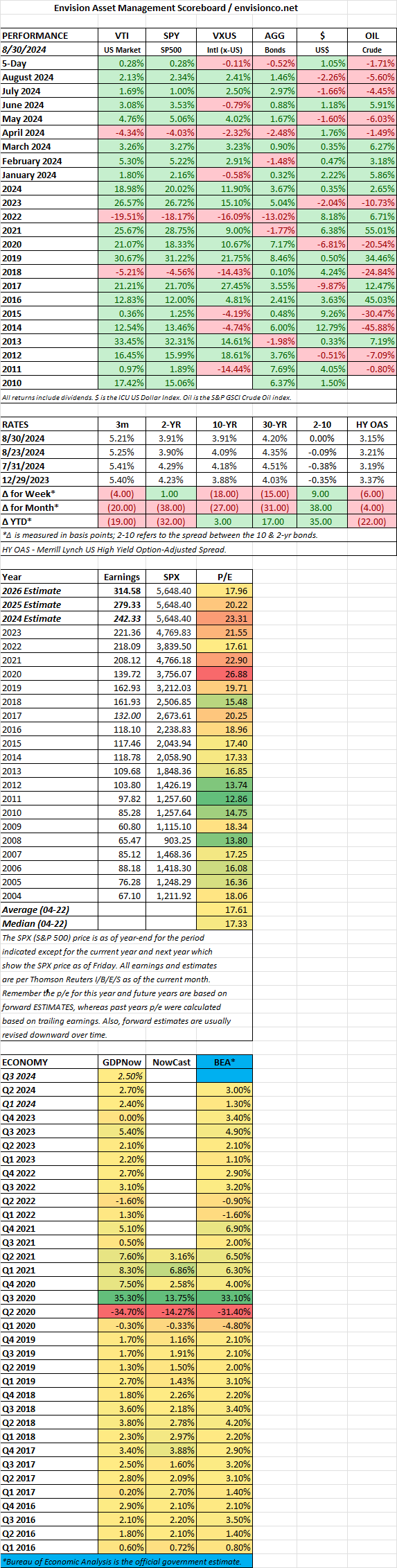

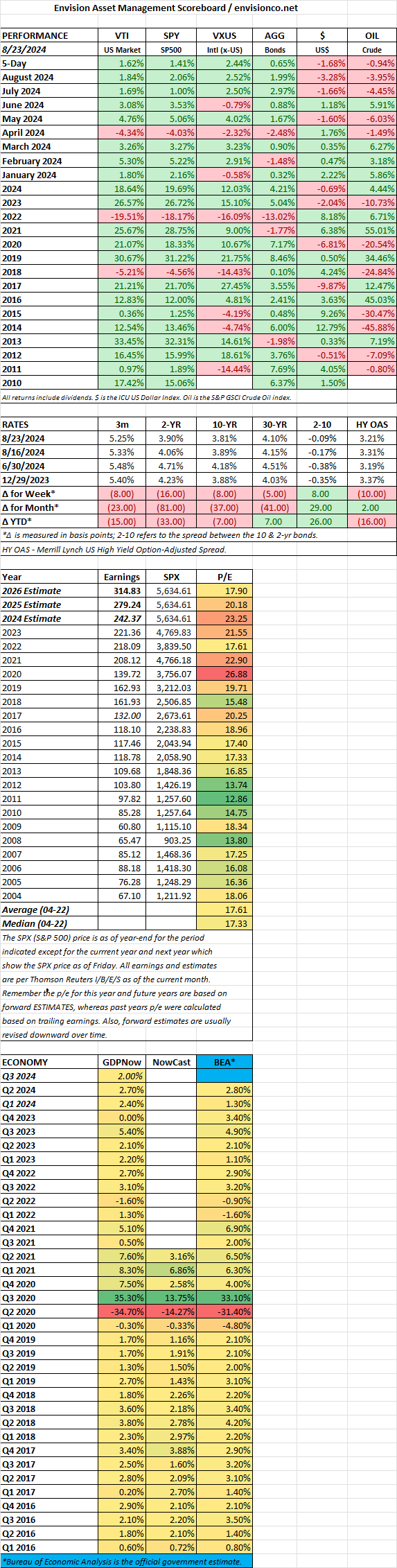

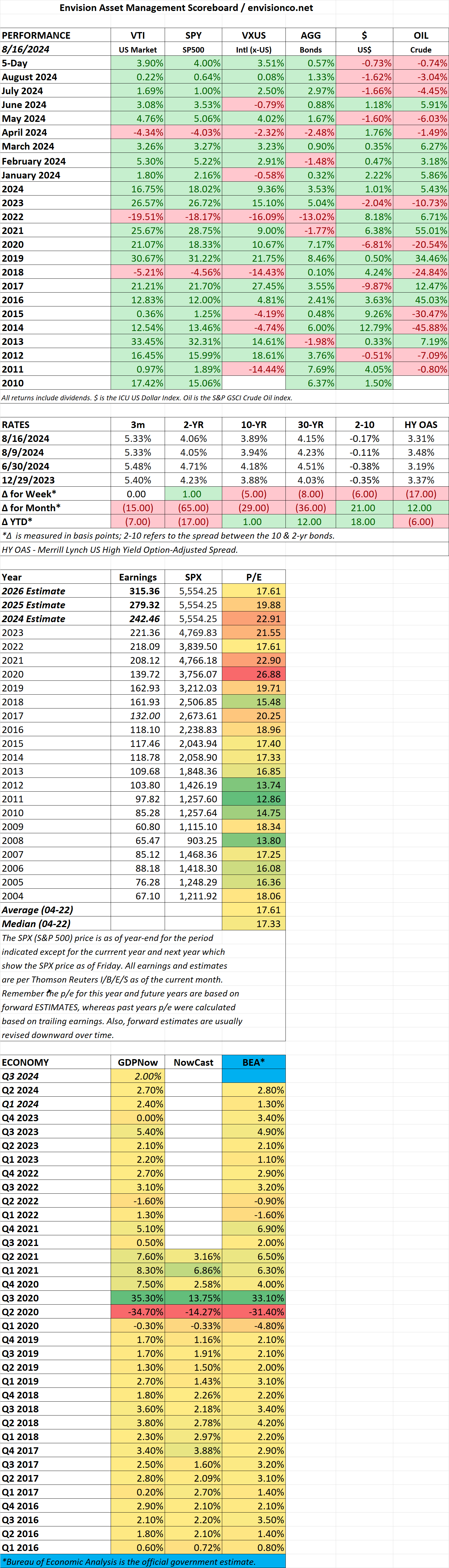

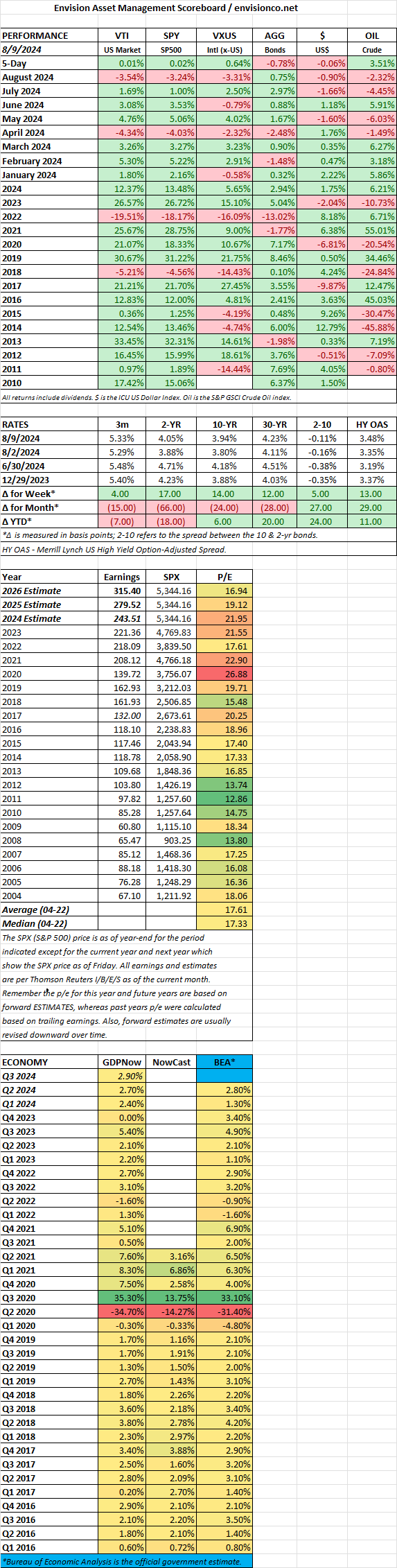

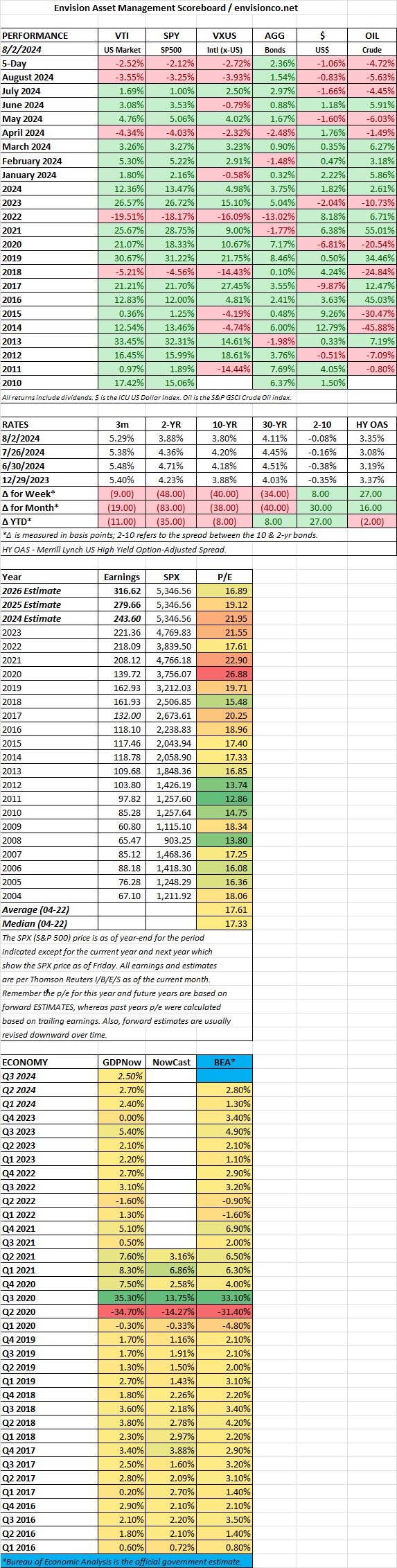

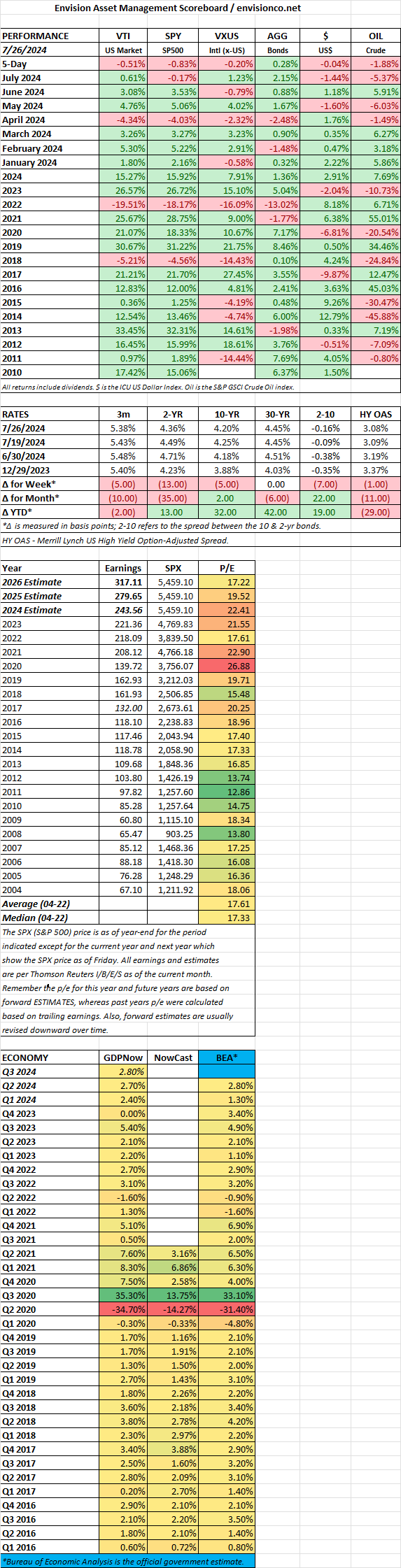

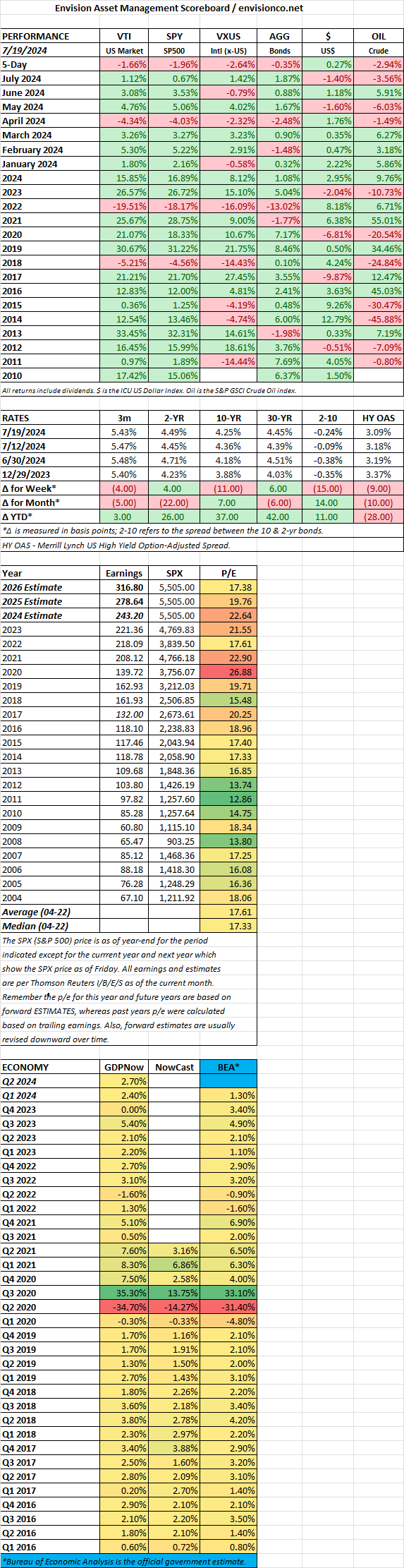

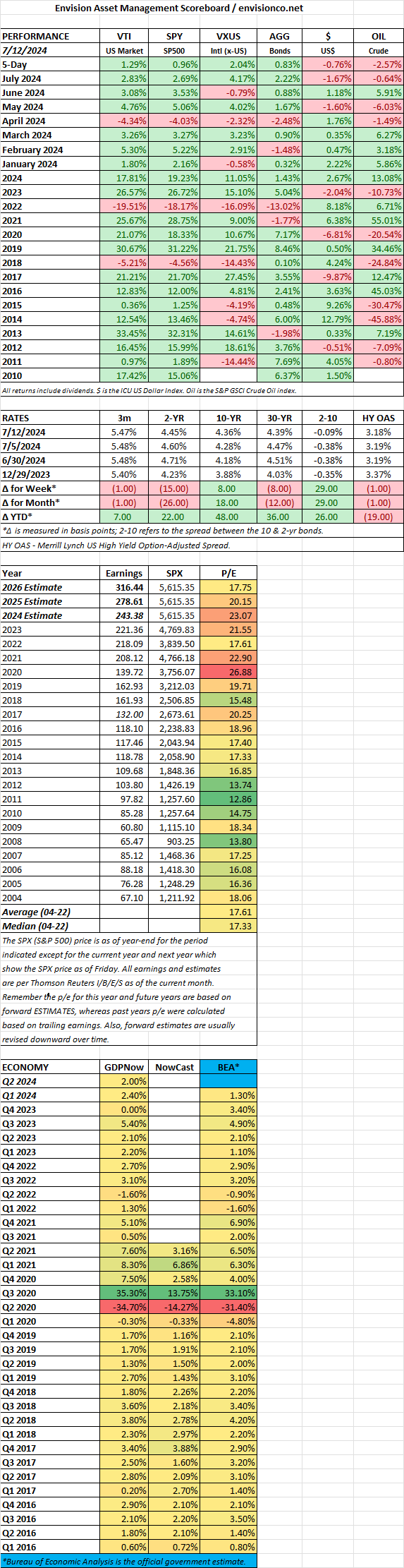

SCOREBOARD