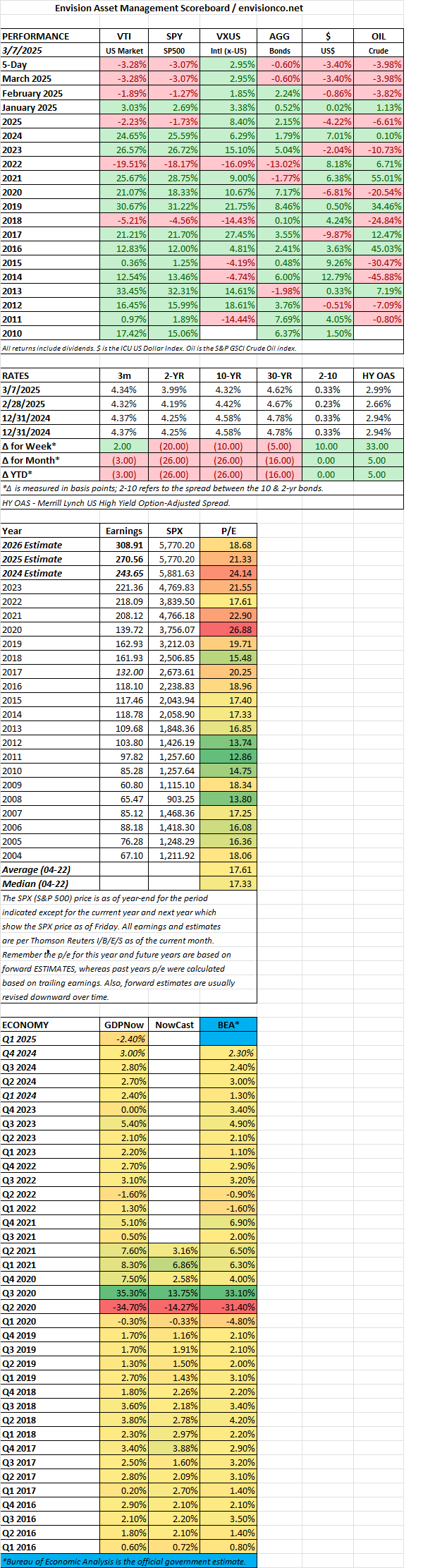

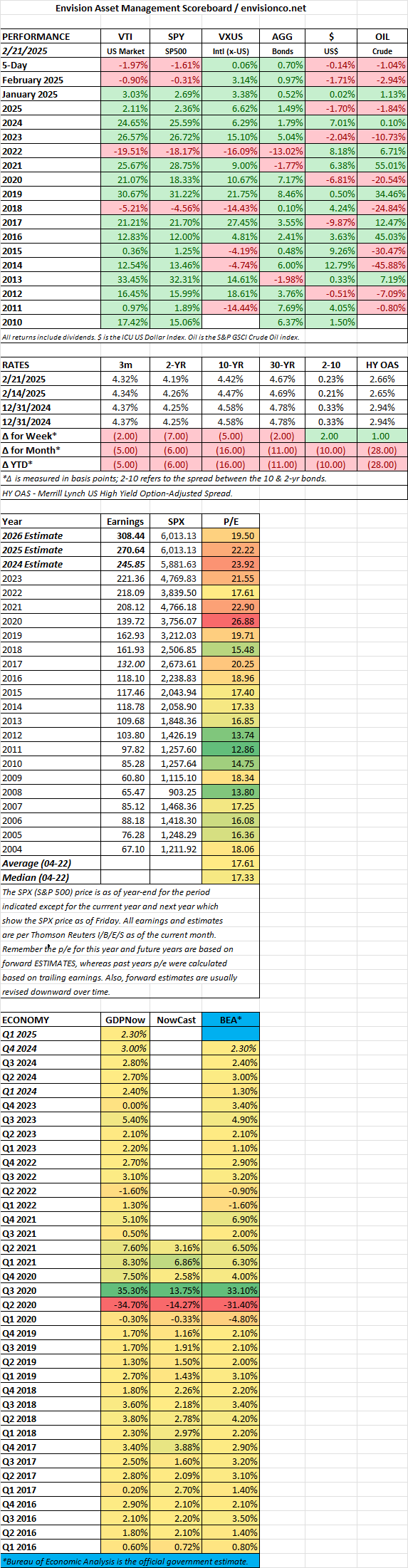

US stocks fell by 2.24%, while international stocks dropped by just 0.53%. Bonds were about flat, down by 0.07%.

Economists have been lowering their growth estimates for the year. Goldman Sachs dropped their 2025 outlook to 1.7% growth from 2.4%.

Trump doubled tariffs to 50% on Canadian steel and oil but then decided not to follow through, a pattern that has become typical over the last few weeks.

There was some good inflation news, as CPI and core CPI increased by 0.2% month over month compared to a consensus estimate of 0.3%. Year over year, CPI was up by 2.8%, down from 3.0% in January.

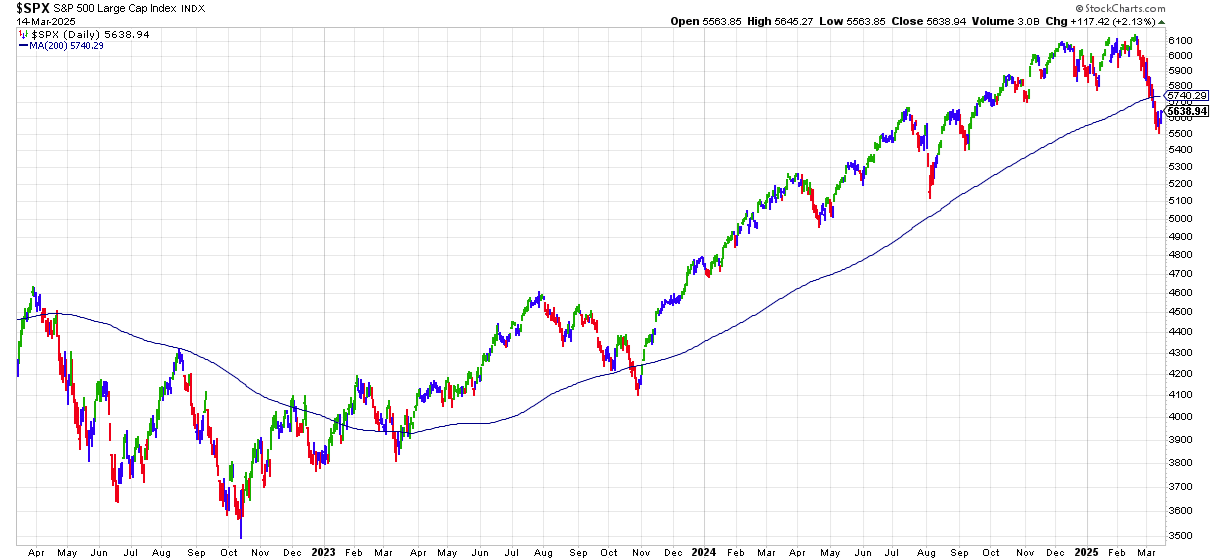

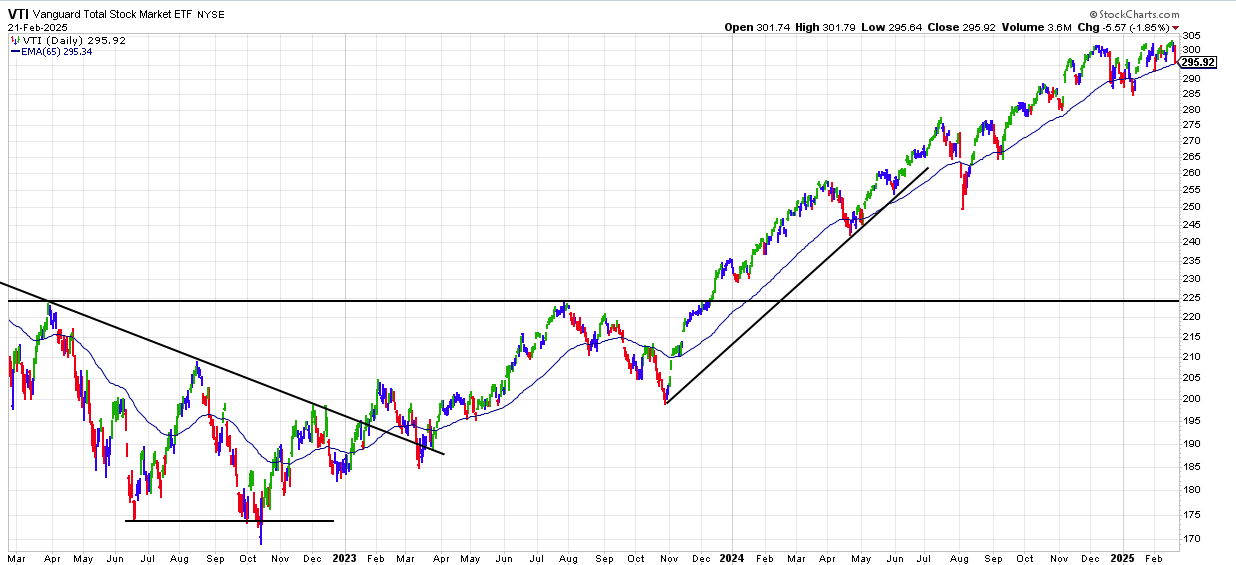

On Thursday, the SP500 fell into correction territory as Trump imposed 200% tariffs on alcohol imports from the EU. The index now trades below its 200-day moving average (see chart below).

Gold hit a record with all of the craziness.

Consumer sentiment is taking a big hit due to tariffs and the administration’s haphazard approach. The University of Michigan survey fell by 11% from last month and is not at the lowest level since November of 2022.

In another warning sign of a slowing economy, airlines have been warning of lower demand.

Trump’s “America First” policy is doing a good job of putting America second or worse. US stocks were down by 3.28% for the week, while international stocks were up by 2.95%. The tariff policy doesn’t make sense, he puts on a tariff only to take it off the next day and then delay it for another 30-days. Trump is singlehandedly pushing the economy into a recession. GDPNow forecasts Q1 growth at -2.4%.

25% tariffs took effect on Tuesday on goods from Mexico and Canada. Canada responded in kind on $100 billion of US imports. Mexico will shortly announce its moves.

On Wednesday, Trump gave automakers a one month exemption from the 25% tariffs.

ADP payrolls came in at 77k, less than the 162k forecast. On the regular jobs report on Friday, there were 151k new jobs, less than forecast. There are warning signs that the economy is beginning to slow.

Inflation did not exceed expectations, coming in at 2.5% year over year.

Interest rates have been dropping fast. The White House would say it reflects DOGE efforts to cut spending, others say it reflects a slowing economy. The 2-year is at 3.99% and the 10-year at 4.24%.

Trump continues to threaten tariffs. There seems to be no cogent policy on tariffs, and the uncertainty is beginning to impact markets. It is like he wants a trade war. The only problem is that it will bring down everyone.

The Atlanta Fed’s GDPNow has fallen to an estimated growth rate of 1.5% in the first quarter.

Jobless claims increased.

In a national embarrassment of historic proportions, Trump and Vance railroaded and embarrassed Ukrainian President Zelensky at a press conference. It is pretty clear that Trump is actually siding with Putin and Russia.

The SPX was down by 1.7%, and the Nasdaq by 2.5% on the week. The 10-year treasury yield declined to 4.419%.

The stock market could not hold records set earlier in the week.

Gold is a few cents off its all-time high set on Thursday.

Walmart had great results but its outlook disappointed investors.

The LEI dropped by 0.3% in January.

On Friday, the Dow and SPX had their worst day of 2025.

Existing home sales dropped by 4.9% last month.

Retail sales fell in January.

The University of Michigan sentiment survey shows that 5-year inflation expectations are now at 3.5%, the highest level since the mid-1990s. Much of that is due to Trump’s tariff threats.

Niall Ferguson reminded readers of the WSJ that powers spending more on debt than the military have led to their fall.

Trump is moving way too fast. He has some good ideas but lots of bad ones, and the way he implements his ideas, in my opinion, is increasing the chances of making a mistake that will hurt the economy and the markets. With valuations at extremely high levels, there is short and intermediate-term risk in the market, and something is bound to go wrong. The way he talks about allies (like Canada and Ukraine), and the way he cozies up to Putin, are sending really bad signals that hurt America around the worrld. The DOGE effort (which could yield a lot of good) is being implemented too fast. For example, laying off 6,000 IRS employees. If one agency needs more help, it is the IRS.

The SP500 was up by 1.47% and the NASDAQ by 2.58%.

The SP500 traded above its all time closing high of 6118 but did not close higher.

Trump’s up and down announcements on tariffs and DOGE’s bull in a China shop approach are putting some fear into investors, something is bound to break.

The CPI came in higher than expected, up 3% year over year. The last thing the economy needs to know is a resurgence of inflation but a carry through on the tariff threat might just lead to that.

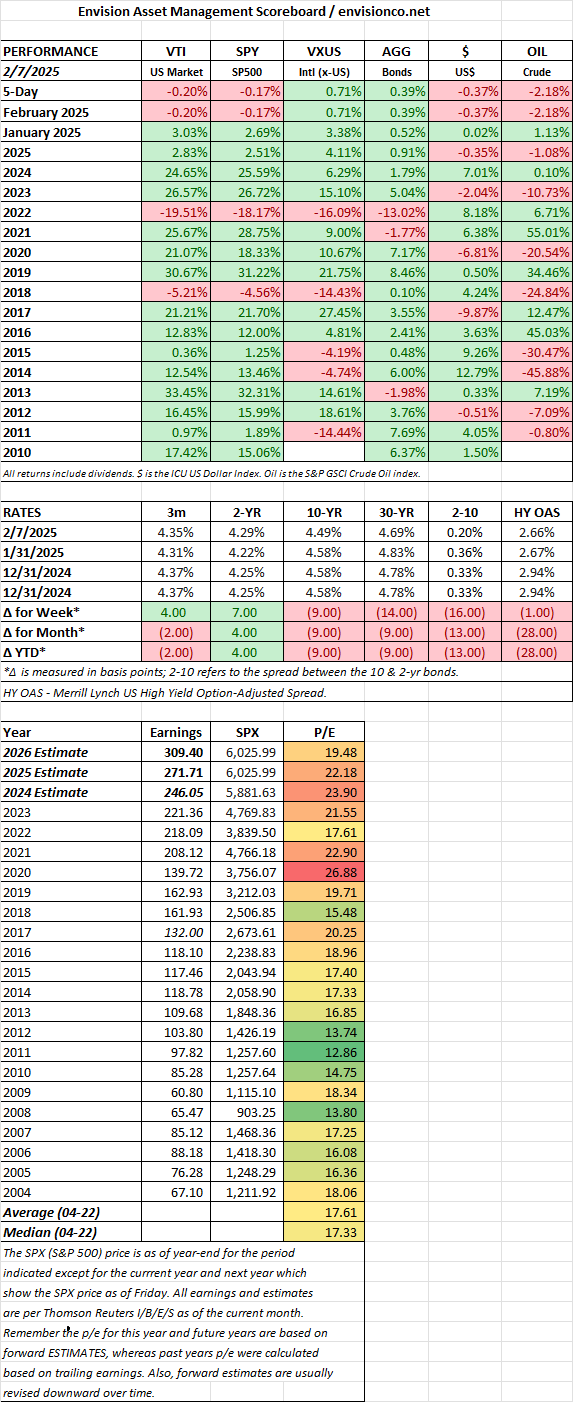

Stocks were down by 0.20%, and bonds were up by 0.39%.

The tariffs on Canada and Mexico that Trump threatened last week were delayed by 30 days.

Job openings fell to 7.6 million in December, a 3-month low. New hires totaled 143,000, a little bit less than expectations. Unemployment declined to 4.0% from 4.1%. Wages were up year over year by 4.1%.

The University of Michigan survey shows that respondents expect inflation to be 4.3% on year from now, leading to a Friday sell-off.

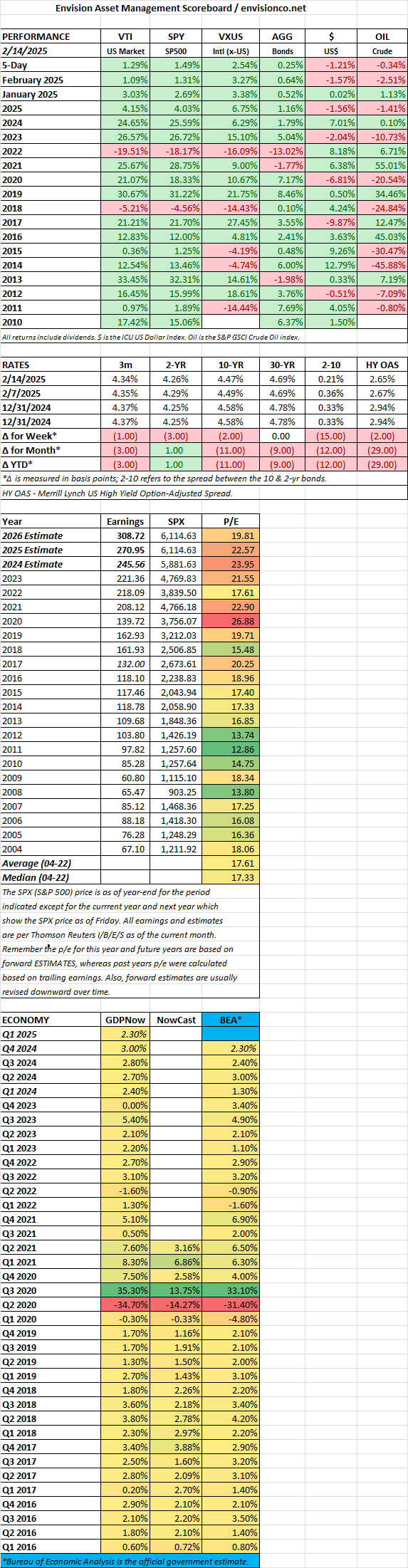

US stocks were down by 0.90% for the week, and bonds were up by 0.40%.

NVDA had a record market cap loss on Monday when the market decided to pay attention to Deep Seek, a Chinese AI application that apparently is as good as American models like ChatGPT and Gemini, and produced at a fraction of the cost. The NASDAQ fell by 3.1% on the day.

Trump is carrying through on his tariff threat, a bad idea that will harm the economy. Putting a 25% tariff on Canada and Mexico and 10% on China, with the EU to follow. Stocks turned down on Friday after the comments. According to Census Bureau data, Canada and Mexico combined for 28% of US imports. In Trump’s make-believe world, there will be no inflationary impact. We agree with many Trump policies, but he is way off-base on this one. Trump’s bullying is going to hurt America long-term, making China seem like a stable partner.

The Fed did not change interest rates.

Inflation forecasts have been slowly rising. Economists estimate 2.6% compared to 2.2% before the election.

Trump was inaugurated, and markets rallied. The SPX was up 1.74% and hit its first record high of 2025 on Thursday.

Trump launched a crypto coin in his name and then one for the first lady, indicating that traditional ethics don’t matter. But who would expect otherwise?

Trump held off closing down TikTok for 75 days and issued pardons to all of the January 6th rioters, even the most violent ones.

Trump announced a $500 billion infrastructure investment by OpenAI, Oracle, Softbank, and a UAE-based company.

At a virtual address at the World Economic Forum, Trump said “I’ll demand that interest rates drop immediately.” Trump is also going to press OPEC to cut prices.

Bitcoin hit a record of 109,000 on Monday but has since fallen back to 101,000.

There were no immediate tariffs on day one, so that helped markets. But indicated that may change on February 1 in regards to Mexico and Canada.

The SPX earnings yield is 4.1% versus a 10-year yield of 4.63%,the biggest disparity since 2002.