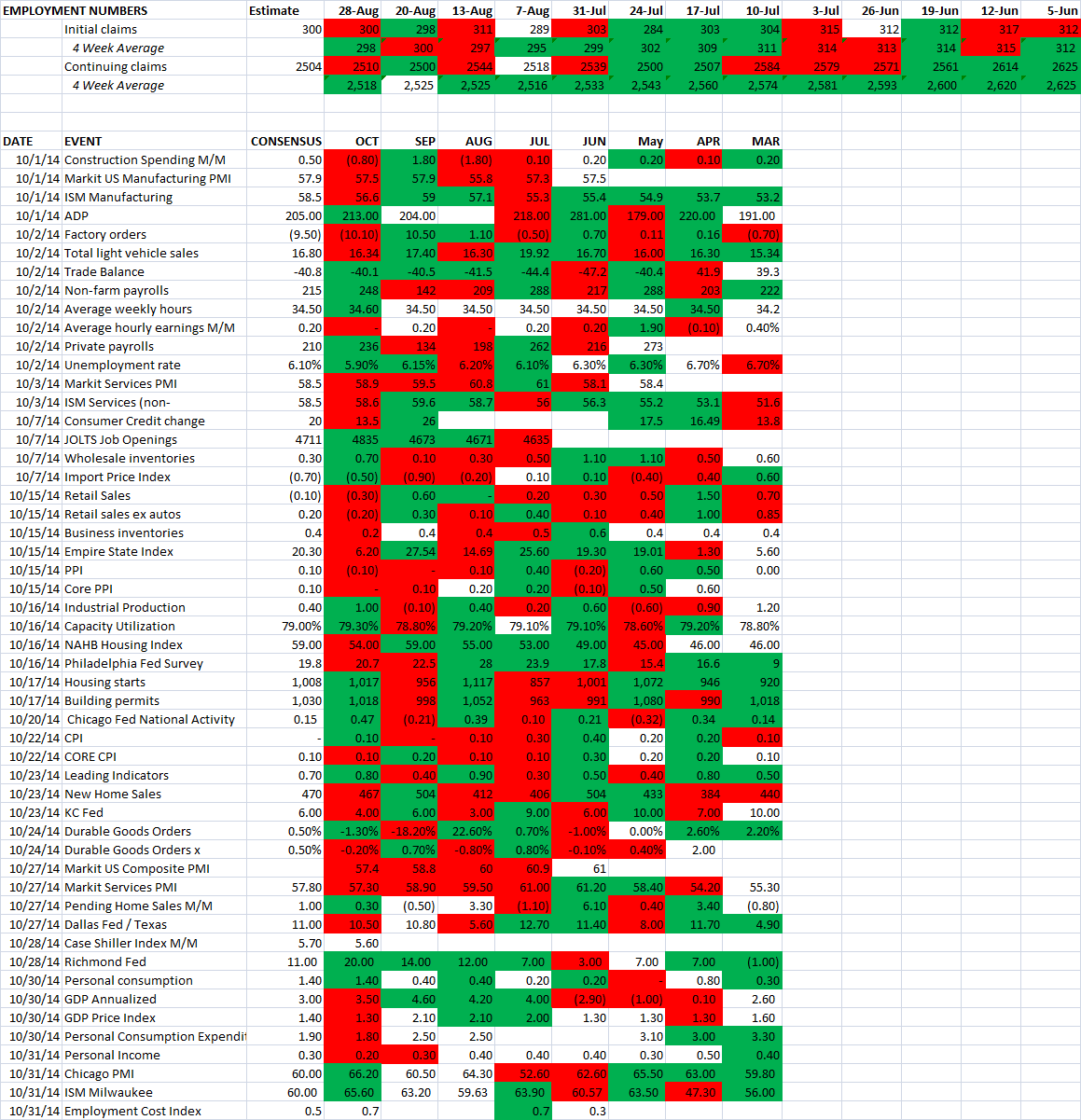

UP AND DOWN WALL STREET

Lower interest rates in Europe have not really helped as the unemployment is high and the economy is still dragging, with GDP close to flat. So Draghi has announced an asset purchase plan and the ECB cut interest rates into effectively negative territory for banks. The benefactor of this might be the rest of the world including the US. A good portion of this new liquidity will end up in the US, pushing the dollar up and lowering inflation and lowering US interest rates. This will ease the impact of a less accommodative Fed. To use a football analogy, Yellen has handed the ball off to Draghi to keep the party is going.

STEAMING AHEAD

Ten top market strategists expect the bull market rally to continue. The SP500 is at 2007.71 which is higher than the average target of 1977 when the panelists met in December. They are looking for 2030 by year-end.

None are negative on the market. 18 to 24 months out 2500 is the high target.

They are looking for a 7% earnings increase this year and 8.1% in 2015, that is up from 5.7% in 2013.

The S&P has a 12-month forward p/e of 15.8 right now. It was 15 at the beginning of the year. The long-term forward p/e average is 15. The strategists do not see a sell off of any major kind (10% or more).

THE TRADER

The ECB cut interest rates to .05% from .15% and announced additional stimulus. The SP500 was up 4.34 points to 2007.71 for the week to close at a record. Economic growth should continue in the US. Adam Parker of Morgan Stanley thinks the SP500 could hit 3000 in five years if the expansion continues. IPOs are up to their highest point since 2000, an increase of 50% over last year.

The column is bullish on Mexico.

SP500 2007.71 +0.22%.

Advances 1371

Declines 1837

Unchanged 65

New Highs 402

New Lows 52